Hotelmarkt Deutschland: München weiter auf Wachstumskurs

•

1 gefällt mir•809 views

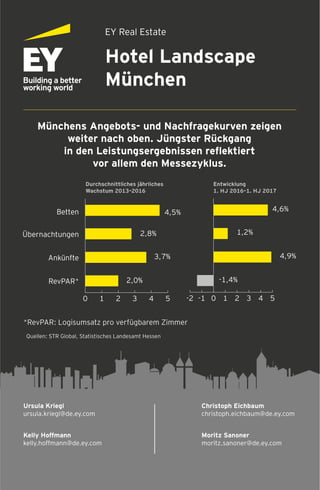

Hotelmarkt Deutschland: München weiter auf Wachstumskurs, sowohl beim Angebot als auch bei der Nachfrage. Der jüngste Rückgang hängt nur mit dem Messezyklus zusammen, das zeigt unser EY Real Estate Hotel Landscape.

Melden

Teilen

Melden

Teilen

Empfohlen

Hotelmarkt Deutschland: Frankfurt wächst weiter

Unser Hotel Landscape zeigt, dass die Übernachtungszahlen sowie die Bettenauslastung in Frankfurter Hotels weiter gut sind. Aber der anhaltende Hotelbauboom lässt den Wettbewerbsdruck spürbar steigen.

Infographik: EY Hotel Landscape

Das EY Hotel Landscape 2018 zeigt: Die Hotelperformance entwickelte sich 2017, gemessen am Umsatz je verfügbarem Zimmer, in den sechs größten deutschen Städten im Schnitt positiv. Bedingt durch Angebotswachstum und Messezyklus gab es jedoch differenzierte Entwicklungen innerhalb der großen deutschen Hotelmärkte – während Köln noch von einem verhaltenen Angebotswachstum profitiert, nimmt in München der Wettbewerbsdruck aufgrund des starken Zimmerwachstums zu.

Büromarkt München Update Q3 - 2013

- Büromarkt verliert an Fahrt

- Verlangsamter Leerstandsabbau

- Mieten stabil

Büromarkt München Update 3. Quartal 2012

1. UMSATZSTÄRKSTES QUARTAL IN DIESEM JAHR

2. LEERSTANDSQUOTE 10% UNTER VORJAHRESWERT

3. WENIGER GROSSABSCHLÜSSE

4. ANTEIL KLEINFLÄCHIGER VERMIETUNGEN CA. 38 %

bc.lab Kanzlerduell - jetzt wird's spannend: Steinbrück erstmals in Merkels Nähe

Spannung auf den letzten Metern: Steinbrück konnte durch sein spektakuläres Stinkefinger-Foto massiv an Aufmerksamkeit gewinnen. Aber auch die TV-Wahlarena half dem Kanzlerkandidaten, sich thematisch in seinen Kernkompetenzen Wirtschaft, Arbeit & Soziales sowie Finanzen zu profilieren. Die Untersuchung wurde mit bc.lab monitor durchgeführt, dem Social Media Monitoring Tool von bc.lab. Mehr Informationen ›› http://www.bclab.de/social-media-monitoring.html

Pressemitteilung PLATOW Prognose 2017

Die internationalen Notenbanken haben seit der großen Finanzkrise ihren geldpolitischen Instrumenten-Kasten massiv erweitert. Mit gewaltigen Anleihekaufprogrammen versuchen EZB und Bank of Japan der Inflation Beine zu machen und die Konjunktur anzukurbeln. Sie experimentieren mit Negativzinsen und die japanische Notenbank will sogar die Zinsstrukturkurve steuern. Trotzdem kommen Inflation und Konjunktur kaum vom Fleck. Die von der US-Zentralbank Fed vor einem Jahr eingeleitete Zinswende geriet schnell wieder ins Stocken. Die scheinbar so mächtigen Notenbanken sind offensichtlich am Ende ihres Lateins angelangt.

In zinslosen Zeiten bleiben Aktien für Anleger weiterhin erste Wahl. Da jedoch die Schwankungen an den Börsen zugenommen haben, kommt es mehr denn je auf die richtige Auslese an. In der PLATOW Prognose 2017 hat das PLATOW-Börsenteam für Sie die 50 aussichtsreichsten Aktien aus Deutschland, Europa, Nordamerika, Japan und den Emerging Markets zusammengestellt. Außerdem werden die weltweiten Perspektiven für Wachstum, Währungen, Zinsen und die Immobilienmärkte analysiert.

DER BÜROMARKTBERICHT MÜNCHEN, 3. Quartal 2014

+++ BUROMARKT AUF VORJAHRESNIVEAU

+++ KEINE GROSSABSCHLÜSSE über 5.000 m2

+++ MIETEN GESTIEGEN

Immobilienreport 2014

Mit der neuen Ausgabe unseres Immobilienreports bieten wir Ihnen eine aktuelle Momentaufnahme über Deutschlands wichtigste Immobilienmärkte. Wie haben sich Märkte und Preise entwickelt? Welche Prognosen gibt es für 2015?

Basis für den Report bildet Deutschlands größte Immobiliendatenbank: Es wurden über eine Million Immobilienangebote ausgewertet, die in den letzten 12 Monaten auf ImmobilienScout24 angeboten wurden.

Den Immobilienreport 2014 stellen wir Ihnen ab sofort kostenfrei zum Download zur Verfügung.

Empfohlen

Hotelmarkt Deutschland: Frankfurt wächst weiter

Unser Hotel Landscape zeigt, dass die Übernachtungszahlen sowie die Bettenauslastung in Frankfurter Hotels weiter gut sind. Aber der anhaltende Hotelbauboom lässt den Wettbewerbsdruck spürbar steigen.

Infographik: EY Hotel Landscape

Das EY Hotel Landscape 2018 zeigt: Die Hotelperformance entwickelte sich 2017, gemessen am Umsatz je verfügbarem Zimmer, in den sechs größten deutschen Städten im Schnitt positiv. Bedingt durch Angebotswachstum und Messezyklus gab es jedoch differenzierte Entwicklungen innerhalb der großen deutschen Hotelmärkte – während Köln noch von einem verhaltenen Angebotswachstum profitiert, nimmt in München der Wettbewerbsdruck aufgrund des starken Zimmerwachstums zu.

Büromarkt München Update Q3 - 2013

- Büromarkt verliert an Fahrt

- Verlangsamter Leerstandsabbau

- Mieten stabil

Büromarkt München Update 3. Quartal 2012

1. UMSATZSTÄRKSTES QUARTAL IN DIESEM JAHR

2. LEERSTANDSQUOTE 10% UNTER VORJAHRESWERT

3. WENIGER GROSSABSCHLÜSSE

4. ANTEIL KLEINFLÄCHIGER VERMIETUNGEN CA. 38 %

bc.lab Kanzlerduell - jetzt wird's spannend: Steinbrück erstmals in Merkels Nähe

Spannung auf den letzten Metern: Steinbrück konnte durch sein spektakuläres Stinkefinger-Foto massiv an Aufmerksamkeit gewinnen. Aber auch die TV-Wahlarena half dem Kanzlerkandidaten, sich thematisch in seinen Kernkompetenzen Wirtschaft, Arbeit & Soziales sowie Finanzen zu profilieren. Die Untersuchung wurde mit bc.lab monitor durchgeführt, dem Social Media Monitoring Tool von bc.lab. Mehr Informationen ›› http://www.bclab.de/social-media-monitoring.html

Pressemitteilung PLATOW Prognose 2017

Die internationalen Notenbanken haben seit der großen Finanzkrise ihren geldpolitischen Instrumenten-Kasten massiv erweitert. Mit gewaltigen Anleihekaufprogrammen versuchen EZB und Bank of Japan der Inflation Beine zu machen und die Konjunktur anzukurbeln. Sie experimentieren mit Negativzinsen und die japanische Notenbank will sogar die Zinsstrukturkurve steuern. Trotzdem kommen Inflation und Konjunktur kaum vom Fleck. Die von der US-Zentralbank Fed vor einem Jahr eingeleitete Zinswende geriet schnell wieder ins Stocken. Die scheinbar so mächtigen Notenbanken sind offensichtlich am Ende ihres Lateins angelangt.

In zinslosen Zeiten bleiben Aktien für Anleger weiterhin erste Wahl. Da jedoch die Schwankungen an den Börsen zugenommen haben, kommt es mehr denn je auf die richtige Auslese an. In der PLATOW Prognose 2017 hat das PLATOW-Börsenteam für Sie die 50 aussichtsreichsten Aktien aus Deutschland, Europa, Nordamerika, Japan und den Emerging Markets zusammengestellt. Außerdem werden die weltweiten Perspektiven für Wachstum, Währungen, Zinsen und die Immobilienmärkte analysiert.

DER BÜROMARKTBERICHT MÜNCHEN, 3. Quartal 2014

+++ BUROMARKT AUF VORJAHRESNIVEAU

+++ KEINE GROSSABSCHLÜSSE über 5.000 m2

+++ MIETEN GESTIEGEN

Immobilienreport 2014

Mit der neuen Ausgabe unseres Immobilienreports bieten wir Ihnen eine aktuelle Momentaufnahme über Deutschlands wichtigste Immobilienmärkte. Wie haben sich Märkte und Preise entwickelt? Welche Prognosen gibt es für 2015?

Basis für den Report bildet Deutschlands größte Immobiliendatenbank: Es wurden über eine Million Immobilienangebote ausgewertet, die in den letzten 12 Monaten auf ImmobilienScout24 angeboten wurden.

Den Immobilienreport 2014 stellen wir Ihnen ab sofort kostenfrei zum Download zur Verfügung.

Nora Reich – Die Metropolregion Hamburg im Vergleich

Ob die Metropolregionen dem Anspruch gerecht werden, Entwicklungsmotoren zu sein, wurde kürzlich für die Metropolregion Hamburg untersucht. „Hamburg 2020 – Chancen nutzen, Zukunft gestalten“ heißt die Studie, die gemeinsam vom Hamburgischen WeltWirtschaftsInstitut (HWWI) (Nora Reich, Silvia Stiller, Ulrich Zierahn) und PricewaterhouseCoopers (Andreas Borcherding, Tatjana Hansen) im Frühjahr 2012 veröffentlicht wurde. Hier wird Hamburg mit den Metropolregionen Stuttgart, Rhein-Ruhr, München, Frankfurt/Rhein-Main sowie Berlin-Brandenburg bezüglich wichtiger Wachstumsindikatoren verglichen. Die Studie geht dabei auf die ökonomische Dynamik sowie Spezialisierungsvorteile der Region Hamburg ein, beleuchtet die Ausstattung mit den „Arbeitskräften der Zukunft“, präsentiert Szenarien zur Entwicklung der Erwerbstätigenzahlen und zeigt zentrale standortpolitische Handlungsfelder auf. Nora Reich, Wissenschaftlerin am HWWI beschreibt in einem Artikel im HWWI-Update (04/2012) die wichtigsten Ergebnisse der Studie bezüglich der Fachkräfteausstattung. Darin erklärt Nora Reich, dass das Potenzial an Fachkräften von großer Bedeutung für die Entwicklung von Produktivität, Wirtschaftswachstum und Arbeitsplätzen ist. Das zukünftige Fachkräftepotenzial hängt dabei unter anderem von der Entwicklung der Bevölkerung, der Attraktivität der Metropolregion Hamburg und der Bildungsperformance ab. Nach Nora Reichs Datenanalysen hat sich die Metropolregion Hamburg beim Bevölkerungswachstum in den vergangenen Jahren positiv von den anderen Metropolregionen abgehoben. Auch die Offenheit gegenüber Zuwanderern – gemessen an der Zuwanderungsrate der Stadt Hamburg aus dem Ausland – bewertet Nora Reich positiv. Gleichzeitig weist Nora Reich auf einige Verbesserungsbedarfe hin. So zeigt die Analyse der Erwerbstätigenstruktur, dass besonders bei Personen mit ausländischer Herkunft sowie bei Frauen Potenzial zur besseren Eingliederung in den Arbeitsmarkt und damit zur Nutzung der vorhandenen Humanressourcen bestehen.

Kanzlerduell: TV-Duell, Erpressung, Syrien sind Top-Themen

Während sich das Verhältnis der Nennungen im Social Web von 1/3 zu 2/3 zugunsten der Bundeskanzlerin gegenüber der Vorwoche nicht geändert hat, konnte sich Merkel bei den Wahlkampfthemen wieder deutlich vor ihrem Herausforderer behaupten. Treibende Themen waren allerdings nicht die Wahlprogramme von CDU und SPD, sondern das TV-Duell, der Erpresungsversuch an Peer Steinbrück und Merkels verspätete Zustimmung zum amerikanischen Syrien-Kurs nach dem G20 Gipfel in St. Petersburg, der ihr deutlich negative Kommentare einbrachte.

Die Untersuchung wurde mit bc.lab monitor durchgeführt, dem Social Media Monitoring Tool von bc.lab ... mehr Informationen ›› http://www.bclab.de/social-media-monitoring.html

Büromarkt München Update 3. Quartal 2011

- Flächenumsatz übertrifft die Erwartungen

- Deutlich mehr Großabschlüsse

- Spitzenmiete steigt moderat

- Leerstandsquote sinkt

- Nachfrage homogen verteilt

Der Büromarkt München Update Q1/2012

+++ LEERSTANDSQUOTE SINKT UM FAST 10 % +++ VERHALTENER FLÄCHENUMSATZ IM 1. QUARTAL +++ SPITZENMIETE SCHEINT ZENIT ERREICHT ZU HABEN +++ WESTLICHES STADTGEBIET GEFRAGT +++

Wirtschaft, Wachstum, Verteilung, Beschäftigung

Von 1996 bis 2016 hat die nominale Wirtschaftsleistung der Schweiz (Bruttoinlandprodukt) trotz Wirtschaftskrise in 2008/9 um 62% auf rund 659 Milliarden Franken zugenommen. Real teuerungsbereinigt betrug die Zunahme 47% oder 2,3% pro Jahr. Gleichzeitig ist auch die Zahl der Erwerbstätigen (Vollzeitäquivalente) um 20% auf 3,83 Millionen gestiegen, so dass sich im Durchschnitt 23% reales Wirtschaftswachstum pro Vollzeiterwerbstätigen ergab. Daraus resultierte ein Wachstum der Produktivität von 1,1% pro Jahr. Da die Zahl der Erwerbstätigen insgesamt sogar um 27% auf 4,95 Millionen gestiegen ist - infolge mehr Teilzeitbeschäftigter, verblieben real noch 16% Wirtschaftswachstum pro Erwerbstätigen (0,8% pro Jahr) . Beitrag von Fegermarketing.ch

bc.lab kanzlerduell - Wahlkampf bleibt inhaltlich konturlos

Merkel weiterhin Nr. 1 im Social Web - Wahlkampf bleibt inhaltlich konturlos - Wahl-Events stehen im Vordergrund - Steinbrück erntet wenig positives Feed Back.

Immobilienpreise in Köln und der Region - KSK-Marktbericht 2014

Beim Stichwort Immobilienboom denken die meisten Bürger an die großen Städte wie München, Hamburg und natürlich auch Köln. Doch die Dynamik bei den Haus- und Wohnungspreisen hat längst die angrenzenden Gebiete erreicht. Mittlerweile können sich Verkäufer hier sogar über in der Relation stärkere Preissprünge als in den Metropolen freuen, zeigt sich im aktuellen Marktbericht der KSK-Immobilien GmbH, den ksta.de hier dokumentiert.

The CEO guide to China's future

For ten years or more, China has been a uniquely powerful engine of the global economy, regularly posting high single-figure or even double-digit annual increases in GDP. More recently, growth has slowed, prompting sharp falls in international commodity prices and casting a shadow over the near-term prospects for developed and emerging markets.

What will happen next? Pessimists struggle to see what China can do for an encore after what they say was an extraordinary, one-off period of catching up. Optimists believe that during the next 10 to 15 years, China has the potential to continue to outperform the rest of the world and to take its place as a full-fledged advanced economy (see summary infographic, “What’s next for China?”).

New models of healthcare, Oliver Wyman at For Later Life 2014

This document discusses establishing an Extensivist model of care to coordinate care for high-cost, high-need patients. It describes how an Extensivist clinic would function, with an Extensivist leading a care team to provide integrated care for patients' medical, behavioral and social needs. It also outlines challenges in implementing this model, such as gaining hospital privileges, changing patient behaviors, and developing new capabilities. The goal is to improve outcomes and lower costs through coordinated, preventative and patient-centered care for the most complex patients.

A.T. Kearney 2017 State of Logistics Report: Accelerating into Uncertainty

2017 could be a pivotal year for logistics. Demand patterns are shifting, technological advances are altering industry economics, and new competitors are challenging old business models. This year could bring significant moves that reshape individual sectors and even the industry as a whole. Major business combinations, large-scale shifts in distribution flows, deep capacity cuts, massive infrastructure investments–anything is possible. Here are the ten key takeaways from the 2017 State of Logistics report, as well as the four potential scenarios for the future of logistics.

The Art of Presentation

First attempt to launch this approach in our country, Spain. Tribute to Reynolds, Weissman and Atckinson.

EY's European Banking Barometer – 2015

EY's European Banking Barometer – 2015 identifies the views of 226 senior European bankers across 11 markets regarding their views of the macro-economic outlook and the impact they think it will have on the banking industry in 2015.

For further information visit: www.ey.com/ebb

Oliver Wyman

The digital travel revolution poses a threat to the hotel industry as new digital competitors are poised to disrupt distribution and capture significant market value. Large digital players have demonstrated the ability to rapidly gain scale in targeted segments. Winners will be those that solve customer hassles along the entire guest journey and build interactional and collaborative relationships rather than purely transactional ones. To respond, hotel companies must rethink distribution's role, build a holistic operating model, define segment and channel strategies, develop a comprehensive revenue agenda, and measure performance using RevPARD.

Bain & Co. GDRoadshow Presentation

The document discusses Bain & Company's pursuit of a 5-star employee experience. Bain is a top global management consulting firm with over 5,700 employees in 51 offices worldwide. It aims to be the #1 best place to work and achieve high levels of employee advocacy. The company measures its success through client results and impact, and supports employees with onboarding, training, mentors, and a culture that ensures no one fails.

Digital Europe: Pushing the frontier, capturing the benefits

What is the speed at which digital is and will change our world?

How is Europe performing in digital compared to the United States? Where is the progress? And where is the paralysis?

What some of the challenges and risks of digital – its potential to divide business and society – between the highly digitized: the “have-mores,” and the “haves:” those who are not able or willing to adapt fast enough.

And what is our share our vision with you for how Europe needs to capture the huge digital prize. What can start-ups, companies, public authorities – everyone in this room – do, to make it happen?

Oliver Wyman - Aerospace Capabilities

The document summarizes Oliver Wyman's capabilities in the aviation and aerospace industry across several areas: business and growth strategy, M&A, partnerships, sales and go-to-market, innovation and R&D efficiency, digital transformation, agile organization design, empowerment and leadership, turnaround and recovery, manufacturing and lean, customer support and MRO, program management, technical problem solving, logistics and supply chain optimization, procurement, and operations excellence. Oliver Wyman leads clients to sustainable and profitable growth, fast and agile transformations, and excellence and increased customer centricity.

Achieving digital maturity: Adapting your company to a changing world

Take a look at three key practices organizations that achieve digital maturity employ.

To read more and download the full report, visit: http://deloi.tt/2fm3Stq

Global flows in a digital age

One in three goods crosses national borders, and more than one-third of financial investments are international transactions. And in the next decade, global flows could triple, powered by rising prosperity and participation in the emerging world. In a new McKinsey Global Institute (MGI) report, "Global flows in a digital age: How trade, finance, people, and data connect the world economy," scenarios show that global flows could reach $54 trillion to $85 trillion by 2025.

Deloitte

Deloitte is a global professional services firm founded in 1845 in London. It has 225,400 employees and revenue of $35.2 billion in 2015. Deloitte provides audit, tax, consulting, financial advisory, enterprise risk, and legal services to clients worldwide. The company is headquartered in New York City and has offices in over 150 countries including major cities in India like Ahmedabad, Bangalore, Chennai, Delhi, Hyderabad, Kolkata, Mumbai, and Pune. Deloitte recruits new employees through an application process involving resume submission, transcript submission, aptitude and personal interviews.

Five keys to marketing's "new golden age"

New trends have moved marketing the cusp of a new golden age. To deliver on the promise, marketing needs to execute on the 5S approach: science, simplicity, substance, speed, and story. This presentation walks through what marketers and business leaders need to get right to execute all of them. This presentation is based on a public webinar given by McKinsey partners Jonathan Gordon and Jesko Perrey.

Find out more from our Marketing and Sales practice: http://www.mckinsey.com/client_service/marketing_and_sales

Weitere ähnliche Inhalte

Was ist angesagt?

Nora Reich – Die Metropolregion Hamburg im Vergleich

Ob die Metropolregionen dem Anspruch gerecht werden, Entwicklungsmotoren zu sein, wurde kürzlich für die Metropolregion Hamburg untersucht. „Hamburg 2020 – Chancen nutzen, Zukunft gestalten“ heißt die Studie, die gemeinsam vom Hamburgischen WeltWirtschaftsInstitut (HWWI) (Nora Reich, Silvia Stiller, Ulrich Zierahn) und PricewaterhouseCoopers (Andreas Borcherding, Tatjana Hansen) im Frühjahr 2012 veröffentlicht wurde. Hier wird Hamburg mit den Metropolregionen Stuttgart, Rhein-Ruhr, München, Frankfurt/Rhein-Main sowie Berlin-Brandenburg bezüglich wichtiger Wachstumsindikatoren verglichen. Die Studie geht dabei auf die ökonomische Dynamik sowie Spezialisierungsvorteile der Region Hamburg ein, beleuchtet die Ausstattung mit den „Arbeitskräften der Zukunft“, präsentiert Szenarien zur Entwicklung der Erwerbstätigenzahlen und zeigt zentrale standortpolitische Handlungsfelder auf. Nora Reich, Wissenschaftlerin am HWWI beschreibt in einem Artikel im HWWI-Update (04/2012) die wichtigsten Ergebnisse der Studie bezüglich der Fachkräfteausstattung. Darin erklärt Nora Reich, dass das Potenzial an Fachkräften von großer Bedeutung für die Entwicklung von Produktivität, Wirtschaftswachstum und Arbeitsplätzen ist. Das zukünftige Fachkräftepotenzial hängt dabei unter anderem von der Entwicklung der Bevölkerung, der Attraktivität der Metropolregion Hamburg und der Bildungsperformance ab. Nach Nora Reichs Datenanalysen hat sich die Metropolregion Hamburg beim Bevölkerungswachstum in den vergangenen Jahren positiv von den anderen Metropolregionen abgehoben. Auch die Offenheit gegenüber Zuwanderern – gemessen an der Zuwanderungsrate der Stadt Hamburg aus dem Ausland – bewertet Nora Reich positiv. Gleichzeitig weist Nora Reich auf einige Verbesserungsbedarfe hin. So zeigt die Analyse der Erwerbstätigenstruktur, dass besonders bei Personen mit ausländischer Herkunft sowie bei Frauen Potenzial zur besseren Eingliederung in den Arbeitsmarkt und damit zur Nutzung der vorhandenen Humanressourcen bestehen.

Kanzlerduell: TV-Duell, Erpressung, Syrien sind Top-Themen

Während sich das Verhältnis der Nennungen im Social Web von 1/3 zu 2/3 zugunsten der Bundeskanzlerin gegenüber der Vorwoche nicht geändert hat, konnte sich Merkel bei den Wahlkampfthemen wieder deutlich vor ihrem Herausforderer behaupten. Treibende Themen waren allerdings nicht die Wahlprogramme von CDU und SPD, sondern das TV-Duell, der Erpresungsversuch an Peer Steinbrück und Merkels verspätete Zustimmung zum amerikanischen Syrien-Kurs nach dem G20 Gipfel in St. Petersburg, der ihr deutlich negative Kommentare einbrachte.

Die Untersuchung wurde mit bc.lab monitor durchgeführt, dem Social Media Monitoring Tool von bc.lab ... mehr Informationen ›› http://www.bclab.de/social-media-monitoring.html

Büromarkt München Update 3. Quartal 2011

- Flächenumsatz übertrifft die Erwartungen

- Deutlich mehr Großabschlüsse

- Spitzenmiete steigt moderat

- Leerstandsquote sinkt

- Nachfrage homogen verteilt

Der Büromarkt München Update Q1/2012

+++ LEERSTANDSQUOTE SINKT UM FAST 10 % +++ VERHALTENER FLÄCHENUMSATZ IM 1. QUARTAL +++ SPITZENMIETE SCHEINT ZENIT ERREICHT ZU HABEN +++ WESTLICHES STADTGEBIET GEFRAGT +++

Wirtschaft, Wachstum, Verteilung, Beschäftigung

Von 1996 bis 2016 hat die nominale Wirtschaftsleistung der Schweiz (Bruttoinlandprodukt) trotz Wirtschaftskrise in 2008/9 um 62% auf rund 659 Milliarden Franken zugenommen. Real teuerungsbereinigt betrug die Zunahme 47% oder 2,3% pro Jahr. Gleichzeitig ist auch die Zahl der Erwerbstätigen (Vollzeitäquivalente) um 20% auf 3,83 Millionen gestiegen, so dass sich im Durchschnitt 23% reales Wirtschaftswachstum pro Vollzeiterwerbstätigen ergab. Daraus resultierte ein Wachstum der Produktivität von 1,1% pro Jahr. Da die Zahl der Erwerbstätigen insgesamt sogar um 27% auf 4,95 Millionen gestiegen ist - infolge mehr Teilzeitbeschäftigter, verblieben real noch 16% Wirtschaftswachstum pro Erwerbstätigen (0,8% pro Jahr) . Beitrag von Fegermarketing.ch

bc.lab kanzlerduell - Wahlkampf bleibt inhaltlich konturlos

Merkel weiterhin Nr. 1 im Social Web - Wahlkampf bleibt inhaltlich konturlos - Wahl-Events stehen im Vordergrund - Steinbrück erntet wenig positives Feed Back.

Immobilienpreise in Köln und der Region - KSK-Marktbericht 2014

Beim Stichwort Immobilienboom denken die meisten Bürger an die großen Städte wie München, Hamburg und natürlich auch Köln. Doch die Dynamik bei den Haus- und Wohnungspreisen hat längst die angrenzenden Gebiete erreicht. Mittlerweile können sich Verkäufer hier sogar über in der Relation stärkere Preissprünge als in den Metropolen freuen, zeigt sich im aktuellen Marktbericht der KSK-Immobilien GmbH, den ksta.de hier dokumentiert.

Was ist angesagt? (9)

Nora Reich – Die Metropolregion Hamburg im Vergleich

Nora Reich – Die Metropolregion Hamburg im Vergleich

Kanzlerduell: TV-Duell, Erpressung, Syrien sind Top-Themen

Kanzlerduell: TV-Duell, Erpressung, Syrien sind Top-Themen

bc.lab kanzlerduell - Wahlkampf bleibt inhaltlich konturlos

bc.lab kanzlerduell - Wahlkampf bleibt inhaltlich konturlos

Immobilienpreise in Köln und der Region - KSK-Marktbericht 2014

Immobilienpreise in Köln und der Region - KSK-Marktbericht 2014

Andere mochten auch

The CEO guide to China's future

For ten years or more, China has been a uniquely powerful engine of the global economy, regularly posting high single-figure or even double-digit annual increases in GDP. More recently, growth has slowed, prompting sharp falls in international commodity prices and casting a shadow over the near-term prospects for developed and emerging markets.

What will happen next? Pessimists struggle to see what China can do for an encore after what they say was an extraordinary, one-off period of catching up. Optimists believe that during the next 10 to 15 years, China has the potential to continue to outperform the rest of the world and to take its place as a full-fledged advanced economy (see summary infographic, “What’s next for China?”).

New models of healthcare, Oliver Wyman at For Later Life 2014

This document discusses establishing an Extensivist model of care to coordinate care for high-cost, high-need patients. It describes how an Extensivist clinic would function, with an Extensivist leading a care team to provide integrated care for patients' medical, behavioral and social needs. It also outlines challenges in implementing this model, such as gaining hospital privileges, changing patient behaviors, and developing new capabilities. The goal is to improve outcomes and lower costs through coordinated, preventative and patient-centered care for the most complex patients.

A.T. Kearney 2017 State of Logistics Report: Accelerating into Uncertainty

2017 could be a pivotal year for logistics. Demand patterns are shifting, technological advances are altering industry economics, and new competitors are challenging old business models. This year could bring significant moves that reshape individual sectors and even the industry as a whole. Major business combinations, large-scale shifts in distribution flows, deep capacity cuts, massive infrastructure investments–anything is possible. Here are the ten key takeaways from the 2017 State of Logistics report, as well as the four potential scenarios for the future of logistics.

The Art of Presentation

First attempt to launch this approach in our country, Spain. Tribute to Reynolds, Weissman and Atckinson.

EY's European Banking Barometer – 2015

EY's European Banking Barometer – 2015 identifies the views of 226 senior European bankers across 11 markets regarding their views of the macro-economic outlook and the impact they think it will have on the banking industry in 2015.

For further information visit: www.ey.com/ebb

Oliver Wyman

The digital travel revolution poses a threat to the hotel industry as new digital competitors are poised to disrupt distribution and capture significant market value. Large digital players have demonstrated the ability to rapidly gain scale in targeted segments. Winners will be those that solve customer hassles along the entire guest journey and build interactional and collaborative relationships rather than purely transactional ones. To respond, hotel companies must rethink distribution's role, build a holistic operating model, define segment and channel strategies, develop a comprehensive revenue agenda, and measure performance using RevPARD.

Bain & Co. GDRoadshow Presentation

The document discusses Bain & Company's pursuit of a 5-star employee experience. Bain is a top global management consulting firm with over 5,700 employees in 51 offices worldwide. It aims to be the #1 best place to work and achieve high levels of employee advocacy. The company measures its success through client results and impact, and supports employees with onboarding, training, mentors, and a culture that ensures no one fails.

Digital Europe: Pushing the frontier, capturing the benefits

What is the speed at which digital is and will change our world?

How is Europe performing in digital compared to the United States? Where is the progress? And where is the paralysis?

What some of the challenges and risks of digital – its potential to divide business and society – between the highly digitized: the “have-mores,” and the “haves:” those who are not able or willing to adapt fast enough.

And what is our share our vision with you for how Europe needs to capture the huge digital prize. What can start-ups, companies, public authorities – everyone in this room – do, to make it happen?

Oliver Wyman - Aerospace Capabilities

The document summarizes Oliver Wyman's capabilities in the aviation and aerospace industry across several areas: business and growth strategy, M&A, partnerships, sales and go-to-market, innovation and R&D efficiency, digital transformation, agile organization design, empowerment and leadership, turnaround and recovery, manufacturing and lean, customer support and MRO, program management, technical problem solving, logistics and supply chain optimization, procurement, and operations excellence. Oliver Wyman leads clients to sustainable and profitable growth, fast and agile transformations, and excellence and increased customer centricity.

Achieving digital maturity: Adapting your company to a changing world

Take a look at three key practices organizations that achieve digital maturity employ.

To read more and download the full report, visit: http://deloi.tt/2fm3Stq

Global flows in a digital age

One in three goods crosses national borders, and more than one-third of financial investments are international transactions. And in the next decade, global flows could triple, powered by rising prosperity and participation in the emerging world. In a new McKinsey Global Institute (MGI) report, "Global flows in a digital age: How trade, finance, people, and data connect the world economy," scenarios show that global flows could reach $54 trillion to $85 trillion by 2025.

Deloitte

Deloitte is a global professional services firm founded in 1845 in London. It has 225,400 employees and revenue of $35.2 billion in 2015. Deloitte provides audit, tax, consulting, financial advisory, enterprise risk, and legal services to clients worldwide. The company is headquartered in New York City and has offices in over 150 countries including major cities in India like Ahmedabad, Bangalore, Chennai, Delhi, Hyderabad, Kolkata, Mumbai, and Pune. Deloitte recruits new employees through an application process involving resume submission, transcript submission, aptitude and personal interviews.

Five keys to marketing's "new golden age"

New trends have moved marketing the cusp of a new golden age. To deliver on the promise, marketing needs to execute on the 5S approach: science, simplicity, substance, speed, and story. This presentation walks through what marketers and business leaders need to get right to execute all of them. This presentation is based on a public webinar given by McKinsey partners Jonathan Gordon and Jesko Perrey.

Find out more from our Marketing and Sales practice: http://www.mckinsey.com/client_service/marketing_and_sales

A.T. Kearney Energy Transition Institute - 10 Facts, An Introduction to Energ...

The A.T. Kearney Energy Transition Institute is a nonprofit organization. It provides leading insights on globaltrends in energy transition, technologies, and strategic implications for private sector businesses and publicsector institutions. The Institute is dedicated to combining objective technological insights with economicalperspectives to define the consequences and opportunities for decision makers in a rapidly changing energylandscape. The independence of the Institute fosters unbiased primary insights and the ability to co-createnew ideas with interested sponsors and relevant stakeholders.

Winning competition through organizational agility

1) What is agility and what is the value of being agile?

2) Elements of agile organization

3) How to become agile?

EY India Attractiveness Survey 2015 – Top Reasons to Invest to Invest in India

Investors see India speeding up pace towards becoming world's top destinations for manufacturing. Check out this detailed infographic on what’s activating growth in India.

Andere mochten auch (16)

New models of healthcare, Oliver Wyman at For Later Life 2014

New models of healthcare, Oliver Wyman at For Later Life 2014

A.T. Kearney 2017 State of Logistics Report: Accelerating into Uncertainty

A.T. Kearney 2017 State of Logistics Report: Accelerating into Uncertainty

Digital Europe: Pushing the frontier, capturing the benefits

Digital Europe: Pushing the frontier, capturing the benefits

Achieving digital maturity: Adapting your company to a changing world

Achieving digital maturity: Adapting your company to a changing world

A.T. Kearney Energy Transition Institute - 10 Facts, An Introduction to Energ...

A.T. Kearney Energy Transition Institute - 10 Facts, An Introduction to Energ...

Winning competition through organizational agility

Winning competition through organizational agility

EY India Attractiveness Survey 2015 – Top Reasons to Invest to Invest in India

EY India Attractiveness Survey 2015 – Top Reasons to Invest to Invest in India

Mehr von EY

EY Price Point Q3 2022

The theme for this quarter is momentum meets uncertainty. The upward trend in crude oil, natural gas, LNG and refined product prices that began in Q1 continued into Q2. Crude oil markets began the quarter just below $100/bbl and have closed below that level on only two days since late April. As we begin Q3, there are increasing concerns about the health of the global economy and how that might affect oil and gas demand.

Quarterly analyst themes of oil and gas earnings, Q1 2022

Financial questions continued to attract the most attention of the analyst community, with major focus on how companies will respond to the war in Ukraine, elevated commodity prices and improved cash flows. Strategic questions focused on how the changing geopolitical environment will affect capital allocation in the short and long term. Operationally, all eyes were on the capacity of companies to step up asset utilization and bring new projects to market quickly. Explore the latest EY quarterly analysts themes.

EY Price Point: global oil and gas market outlook, Q2 | April 2022

The theme for this quarter is rearrangement. The loss, or potential loss, of Russian oil and gas supplies is forcing producers, refiners and traders to rethink the flow of crude oil and refined products from the wellhead to the gas pump in light of sanctions, potential sanctions and the risk of reputational damage. Countries, companies and consumers will all be searching for ways to adapt, and the outcome of the race to bring alternatives to market could alter the global energy landscape for years to come.

It is likely crude oil and LNG prices will remain elevated for some time. The process of diverting Russian oil through countries unwilling to sanction it will take time and there is little indication OPEC members are willing (or able) to increase production to make up for the loss of Russian crude. Spare capacity sat at 3.7 mbpd at the end of 2021, just above where it was in January 2020. Currently, sanctioned Venezuelan and Iranian production (about 3 mbpd below their peak) could fill the gap, but political and commercial obstacles remain. At today’s prices, US shale production is attractive, but the fastest the industry has been able to grow is between 1mbpd and 2mbpd per year. The LNG infrastructure was already stretched before the war in Ukraine and there is little prosect of finding new supplies soon.

As the largest buyer of Russian energy, Europe will be the epicenter. There is a deeply embedded bias there in favor for renewable energy, and the current crisis is certain to result in an all-out effort to accelerate the build-out of wind and solar power. The capacity to add new green energy is limited though by the project pipeline and supply chains for solar panels and wind turbines, and it is likely that much of the shortfall will be made up with the new LNG infrastructure.

EY Price Point: global oil and gas market outlook

As the last quarter of the second pandemic year draws to a close, we continue to see heightened contrast

between the medical and economic points of view. While COVID-19 cases are close to their all-time highs, so

are equity prices, and a leading investment bank declared (on 2 December, 2021 after the Omicron outbreak in South Africa) that it was “optimistic about the possibility of a vibrant 2022.” When news of the variant hit in

late November, the markets were rocked by the prospect of yet another round of local mobility restrictions and

an interrupted return to normal international travel patterns, on top of the Biden Administration’s announced

release of 50 million barrels of crude from the US Strategic Petroleum Reserve. So far though, with OPEC

standing by its planned gradual return to normal production, oil prices have stabilized, albeit below where they

were in mid-November. Henry Hub prices, always at the mercy of the weather, responded predictably to a

warmer-than-normal early winter in the US, falling from US$6.60/MMBtu in early October to below

US$4.00/MMBtu by mid-December. In Europe and Asia, following a short reprieve at the start of the quarter,

piped natural gas prices have spiked again on concerns triggered by Russian troop buildups on the Ukraine

border and uncertainties surrounding the Nordstream 2 pipeline. Looking forward, OPEC and the U.S. Energy

Information Administration (EIA) in their last forecasts of the year both projected that 2022 oil demand would

be above what we saw in 2019. Although time will tell if those forecasts are realized and other events could

intervene, the response to new virus outbreaks is well-practiced and the trade-off between public health and

economic reality has tipped toward a cautiously optimistic view.

EY Price Point: global oil and gas market outlook, Q2 April 2021

The theme for this quarter is governed. Apparent market balance at prices that could be sustainable is the product of calculated choices by market leaders and the cooperation of those who follow them. Economics played their customary role as well, with capital scarcity in North America taking about 2 million barrels per day out of the market, about half of the remaining gap in demand. While inventories are close to their pre-COVID-19 levels, there is still uncertainty. The resolution of the pandemic is in sight, but timing is unclear. Vaccine distribution in the US is having an impact but Europe is struggling to contain a third wave of infections. The taps have opened on economic stimulus, but it remains to be seen if policymakers have done enough or if they have overshot the mark.

The shape of the crude oil forward curve has fundamentally changed since the end of the last quarter. In late December of last year, the Brent forward curve was gradually increasing while today, the curve is backwardated. This is a clear sign that the market sees a short-term dynamic that is disconnected from the medium-to-long-term fundamentals. The lasting impact of the COVID-19 pandemic remains to be seen. While many have opined that COVID-19 marks a turning point in energy transition, the IEA recently released a five-year forecast of oil demand that shows steady growth, albeit at rates that are below historical expectations.

Gas markets are a paradox. At the Henry Hub and at LNG destinations, demand grows, investment lags and prices will occasionally attract attention. Traders, so far though, are unconvinced and futures prices don’t indicate imminent scarcity at any link in the value chain.

Tax Alerte - Principales dispositions loi de finances 2021

Note about the main provisions of Finance bill 2021

EY Price Point: global oil and gas market outlook

We enter 2021 on a note of cautious optimism for global health, the world economy, and the oil and gas markets. The first weeks of December brought approval in the US and the UK of the first of several COVID-19 vaccines. The speed with which vaccine development occurred is unprecedented, but certainly welcome. In the weeks following the early November announcement of 90+% effectiveness by the manufacturer of the first approved vaccine, the price of WTI crude oil increased by US$10/bbl to US$48/bbl, the highest level since early March. Sustainability hasn’t returned yet, and whatever time it takes to get the world to normal, it will take even longer for normalization within the oil and gas markets. Inventories remain at historically high levels and, optimistically, it will take until April before inventory returns to levels observed in the preceding five years. That’s an estimate, and there has obviously been some difficulty properly calibrating the expectations of how balance will return and how long it will take. In late November, OPEC met to adjust its output plans because of the anemic rebound in demand. In mid-December, the IEA lowered its demand forecast for 2021 due mostly to continued sluggishness in aviation fuel demand.

A mild winter has interrupted a recovery in North American natural gas prices after a run-up motivated by curtailed capital expenditures, upstream activity and production. After an initial meltdown, with cargo cancellations and dramatic price reversal, LNG markets have made a remarkable comeback, and the spread between Asia and Henry Hub has reached a level we haven’t seen in almost three years. It may be the case that interruption in FIDs has brought us to the cusp of a balance that can support reliable returns.

Tax Alerte - prix de transfert - PLF 2021

L'alerte détaillant les propositions PLF pour l’année 2021 relatives à la documentation des prix de transfert.

EY Price Point: global oil and gas market outlook (Q4, October 2020)

Oil and gas prices have recovered steadily from their lows and are relatively stable, but that stability is supported by the combination of purposeful withholding of production by oil-producing countries and economic stress on upstream independents. Oil prices closed the quarter roughly where they started it, while refining spreads were down slightly. LNG spreads were substantially higher at the end of Q3 than they were at the beginning of the quarter but are still roughly half of what is generally thought of as sustainable.

Going forward, the market will be looking closely at how the economy and demand respond to new developments with respect to a potential COVID-19 vaccine and the US election.

EY Price Point: global oil and gas market outlook

As we close the second quarter of 2020, in most of Europe and Asia, the first (and hopefully last) wave of the COVID-19 crisis appears to be abating. In the parts of the US where the virus hit early, the profile has largely matched Europe’s, while in other parts, the urge to reopen businesses has trumped the desire to contain the virus and uncertainty looms. In the developing world, the crisis has just begun, but without the economic headroom and resources necessary to contain it. As the crisis unfolded, the effect on oil and gas demand has been predictable but difficult to gauge precisely and therefore difficult to manage.

Oil prices have crept up steadily as production has been curtailed through coordinated action (OPEC+) and because of economic reality (unconventional oil in North America). That trend has been subject to momentary spasms when bad news hit the market. It would be understandable if traders were nervous, and it seems that they are. Although nowhere near where it was at the peak of the crisis, option implied volatility is still at historically high levels. Gas markets, without the benefit of coordination on the supply side, continue to deal with the market implications of storage at or near capacity. Interfuel competition in power generation has always provided something of a floor, but those lows have been, and will continue to be, tested.

Zahl der Gewinnwarnungen steigt auf Rekordniveau

Immer mehr deutsche börsennotierte Unternehmen müssen ihre eigenen Umsatz- oder Gewinnprognosen nach unten korrigieren. Im ersten Quartal stieg die Zahl der Prognosekorrekturen auf ein neues Rekordniveau: Insgesamt 77 Gewinn- oder Umsatzwarnungen wurden registriert.

Versicherer rechnen mit weniger Neugeschäft

Die Corona-Krise trifft auch die Versicherungsbranche mit voller Wucht. Die Versicherer rechnen mit weniger Neugeschäft. Jeder Fünfte mit Personalabbau und Prämienerhöhungen.

Liquidity for advanced manufacturing and automotive sectors in the face of Co...

The document discusses the impacts of COVID-19 on the liquidity and cash management of advanced manufacturing and mobility companies. It notes that companies are searching for short-term solutions to issues securing liquidity to fund operations as the global economy falls due to actions taken in response to the pandemic. It provides an overview of various challenges companies may face, such as cash shortages, credit squeezes, supply chain disruptions, and reduced access to capital. The document also outlines some measures companies can take to enhance short-term liquidity.

IBOR transition: Opportunities and challenges for the asset management industry

This document provides an agenda and overview of a webinar discussing the IBOR transition for the asset management industry. The webinar covers topics such as the progress of the transition, impact on asset managers and products, perspectives from European central banking working groups, and how firms are migrating. It introduces the speakers and their topics. In addition, it provides background on the drivers for IBOR reform, timeline of key milestones, and summaries of transition progress for different jurisdictions.

Fusionen und Übernahmen dürften nach der Krise zunehmen

Folgt auf die Corona-Krise ein M&A-Boom? Laut Capital Confidence Barometer von #EY hoffen 40 Prozent der deutschen Unternehmen auf sinkende Bewertungen von Übernahmekandidaten.

Start-ups: Absturz nach dem Boom?

2019 stiegen die Start-up-Investitionen um 46% auf 31 Mrd. Euro. Für 2020 wir mit massivem Einbruch gerechnet.

EY Price Point: global oil and gas market outlook, Q2, April 2020

The first quarter of this year has seen some extraordinary events. As if chronic oversupply, prices stuck below sustainable levels, the looming energy transition, and investor pressure to decarbonize weren’t enough, our industry now faces a dramatic, but hopefully temporary, downturn in demand as a result of the ongoing COVID-19 outbreak.

Riding the crest of digital health in APAC

A primer on key areas where Life Sciences companies can prioritize digital investments across the value chain in APAC.

EY Chemical Market Outlook - February 2020

Our Global Chemical Industry Leader Frank Jenner explores the trends and drivers that will shape the chemical industry of tomorrow in our latest Chemical Market Outlook.

Jobmotor Mittelstand gerät ins Stocken

Die Geschäftslage im Mittelstand hat sich leicht verschlechtert, ist in den meisten Branchen aber weiter überwiegend gut - die Einstellungsbereitschaft sinkt.

Mehr von EY (20)

Quarterly analyst themes of oil and gas earnings, Q1 2022

Quarterly analyst themes of oil and gas earnings, Q1 2022

EY Price Point: global oil and gas market outlook, Q2 | April 2022

EY Price Point: global oil and gas market outlook, Q2 | April 2022

EY Price Point: global oil and gas market outlook, Q2 April 2021

EY Price Point: global oil and gas market outlook, Q2 April 2021

Tax Alerte - Principales dispositions loi de finances 2021

Tax Alerte - Principales dispositions loi de finances 2021

EY Price Point: global oil and gas market outlook (Q4, October 2020)

EY Price Point: global oil and gas market outlook (Q4, October 2020)

Liquidity for advanced manufacturing and automotive sectors in the face of Co...

Liquidity for advanced manufacturing and automotive sectors in the face of Co...

IBOR transition: Opportunities and challenges for the asset management industry

IBOR transition: Opportunities and challenges for the asset management industry

Fusionen und Übernahmen dürften nach der Krise zunehmen

Fusionen und Übernahmen dürften nach der Krise zunehmen

EY Price Point: global oil and gas market outlook, Q2, April 2020

EY Price Point: global oil and gas market outlook, Q2, April 2020

Hotelmarkt Deutschland: München weiter auf Wachstumskurs

- 1. Hotel Landscape München EY Real Estate Ursula Kriegl ursula.kriegl@de.ey.com Christoph Eichbaum christoph.eichbaum@de.ey.com Kelly Hoffmann kelly.hoffmann@de.ey.com Moritz Sanoner moritz.sanoner@de.ey.com Münchens Angebots- und Nachfragekurven zeigen weiter nach oben. Jüngster Rückgang in den Leistungsergebnissen reflektiert vor allem den Messezyklus. *RevPAR: Logisumsatz pro verfügbarem Zimmer Quellen: STR Global, Statistisches Landesamt Hessen Betten Übernachtungen Ankünfte RevPAR* 4,6% 1,2% 4,9% -1,4% Entwicklung 1. HJ 2016–1. HJ 2017 -2 -1 0 1 2 3 4 50 1 2 3 4 5 4,5% 2,8% 3,7% 2,0% Durchschnittliches jährliches Wachstum 2013–2016