Internet Usage - India vs China

•Als DOC, PDF herunterladen•

3 gefällt mir•5,505 views

The document provides an analysis of internet access in India and China through comparing key metrics over time and against each other and the global market. It finds that while India's internet access market is growing faster than China's and the global market, China currently has over 6 times as many internet users as India. A Porter's Five Forces analysis indicates the Indian internet access market exhibits moderate buyer power and strong supplier power.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Internet Usage - India vs China

Ähnlich wie Internet Usage - India vs China (20)

Mehr von Nataraj Pangal

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Internet Usage - India vs China

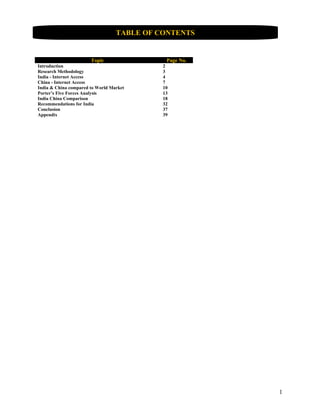

- 1. TABLE OF CONTENTS Topic Page No. Introduction 2 Research Methodology 3 India - Internet Access 4 China - Internet Access 7 India & China compared to World Market 10 Porter’s Five Forces Analysis 13 India China Comparison 18 Recommendations for India 32 Conclusion 37 Appendix 39 1

- 2. INTRODUCTION This study is intended to highlight the importance of the Internet access in the context of India and China, which together are home to approx 40% of world’s population. It compares the recent trends in the growth of Internet users and Internet connections in the two countries. It explores the problems encountered in its proliferation and examines the factors, which might play crucial role in its future growth. China holds the clear edge over India in terms of number of Internet users and Internet hosts; India is better rated when it comes to e-readiness. Internet is still out of reach of rural population in both the countries and both need to have low cost local language based computing devices for the use of rural population to access Internet. Internet has become an important enabling technology. It can improve governance by raising efficiency, transparency and by increasing people’s participation in the governing process. It offers huge economic opportunities through development of information and communication technology. It can help in improving environment management through Geographical Information System and early warning systems. Social and human right conditions can be improved by expanding access to better education and healthcare. It can help in knowledge sharing and creating awareness among people. Above all, it can help in reducing poverty by opening new opportunities for woman, the poor and rural population. This is particularly important for India and China, both of which have a large percentage of impoverished people with a large part of the population living in rural areas lacking even basic telephone services. While China has pursued a policy of strong government initiative coupled with encouraging competitions among government owned organizations, India has set policy through publicly visible task forces. Which policy remains effective in long run remains to be seen. This study compares Internet in India and China with reference to the efforts being carried out in the diffusion of Internet in the national economies, number of users with characteristics and bandwidth availability, relative advantages and disadvantages of Internet in each country, and the future potential of Internet expansion. The intention of the study is to identify key learnings that India can have from observing the Internet growth patterns in China. What should be the future strategies and areas of focus, for India inorder to increase its Internet penetration and widen Internet Access and Usage? What is the role that Government, Corporates and Consumers can play inorder to make the best use of the potential of Internet? An attempt has been made to indentify solutions to these questions in the report. 2

- 3. RESEARCH METHODOLOGY • The Research Methodology has been primarily reviewing Secondary Data. The current statistics of the Internet Access Market in India and China have been obtained from Datamonitor. Inorder to maintain consistency of data, Datamonitor has been used as the prime source of current as well as forecasted statistical information. Inorder to ascertain whether Internet Access market is growing in India and China at a fast pace, the growth rates in both the countries have been compared to that of the world. • A Porter’s Five Forces analysis of Internet Access Market in India was done to understand the dynamics of the Internet Access market in India and get a snapshot of the current situation. • Followed by this, Internet Access in India and China has been compared based on the following 6 parameters : - o Pervasiveness o Geographic Dispersion o Organizational Structure o Connectivity Infrastructure o Sectoral Absorption o Sophistication of Use • After analyzing, how India and China fare in each of the above mentioned parameters, key focus areas for India have been indentified for enhancing the Internet Access Market. The future steps that India ought to take inorder to match steps with China and other global players have been enlisted. 3

- 4. INDIA – INTERNET ACCESS The Indian internet access market generated total revenues of $33.7 billion in 2008, representing a compound annual growth rate (CAGR) of 37.6% for the period spanning 2004-2008. The number of internet subscribers increased with a CAGR of 25% between 2004-2008, to reach a total of 11.1 million in 2008. The performance of the market is forecast to decelerate, with an anticipated CAGR of 18.3% for the five-year period 2008-2013, which is expected to drive the market by the end of 2013. Indian internet access market has exhibited strong growth over the previous five years, but will continue to slow in its growth towards 2013 as internet access penetration becomes more saturated. The Indian internet access market generated total revenues of $33.7 billion in 2008, representing a compound annual growth rate (CAGR) of 37.6% for the period spanning 2004-2008. In comparison, the Chinese market grew with CAGR of 20% over the same period, to reach respective values of $18.6 billion and $4.8 billion in 20081. The number of internet subscribers increased with a CAGR of 25% between 2004- 2008, to reach a total of 11.1 million in 2008. The number of subscribers is expected to rise to 25.7 million by the end of 2013, representing a CAGR of 18.3% for the 2008-2013 period. The performance of the market is forecast to decelerate, with an anticipated CAGR of 18.3% for the five-year period 2008-2013, which is expected to drive the market to a value of $78.1 billion by the end of 20132. The Indian internet access market grew by 29.2% in 2008 to reach a value of $33.7billion. The compound annual growth rate of the market in the period 2004-2008 was 37.6%. (Refer Appendix A) 1 Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657- D9B8-4C96-A51C- 2 Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657- D9B8-4C96-A51C- 4

- 5. The Indian internet access market grew by 19.6% in 2008 to reach a volume of 11.1 million internet subscribers. The compound annual growth rate of the market volume in the period 2004-2008 was 24.9%. (Refer Appendix B) In 2013, the Indian internet access market is forecast to have a value of $78.1 billion, an increase of 131.7% since 2008. The compound annual growth rate of the market in the period 2008-2013 is predicted to be 18.3%. (Refer Appendix C) 5

- 6. In 2013, the Indian internet access market is forecast to have a volume of 25.7 million internet subscribers, an increase of 131.7% since 2008. The compound annual growth rate of the market volume in the period 2008-2013 is predicted to be 18.3%3. (Refer Appendix D) 3 Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657- D9B8-4C96-A51C- 6

- 7. CHINA – INTERNET ACCESS The Chinese internet access market has also exhibited strong growth over the previous five years, but will begin to slow slightly in its growth towards 2013 as internet access penetration becomes more saturated. The Chinese internet access market generated total revenues of $18.6 billion in 2008, representing a compound annual growth rate (CAGR) of 20% for the period spanning 2004-2008. In comparison, the Indian market grew with CAGR of 37.6% over the same period, to reach respective values of $33.7 billion and $4.8 billion in 2008. The number of internet subscribers increased with a CAGR of 20% between 2004-2008, to reach a total of 77.7 million in 2008. The number of subscribers is expected to rise to 155.3 million by the end of 2013, representing a CAGR of 14.9% for the 2008-2013 period. The performance of the market is forecast to decelerate, with an anticipated CAGR of 14.9% for the five-year period 2008-2013, which is expected to drive the market to a value of $37.3 billion by the end of 20134. The Chinese internet access market grew by 19.9% in 2008 to reach a value of $18.6 billion. The compound annual growth rate of the market in the period 2004-2008 was 20%. (Refer Appendix E) 4 Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 7

- 8. The Chinese internet access market grew by 19.9% in 2008 to reach a volume of 77.7 million internet subscribers. The compound annual growth rate of the market volume in the period 2004-2008 was 20%5. (Refer Appendix F) In 2013, the Chinese internet access market is forecast to have a value of $37.2 billion, an increase of 99.9% since 2008. The compound annual growth rate of the market in the period 2008-2013 is predicted to be 14.9%6. (Refer Appendix G) 5 Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 6 Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 8

- 9. In 2013, the Chinese internet access market is forecast to have a volume of 155.3 million internet subscribers, an increase of 99.9% since 2008. The compound annual growth rate of the market volume in the period 2008-2013 is predicted to be 14.9%7. (Refer Appendix H) Thus, though the growth rate of Indian Internet Access Market is currently higher and is forecasted to be higher than Chinese market, the number of Internet users in China currently as well as forecasted in 2013 is much higher as compared to that of India. The geographic penetration of China is much higher as compared to India. 7 Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 9

- 10. INDIA & CHINA – COMPARED TO WORLD MARKET It is also imperative to understand how is India and China’s growth as compared to the growth of Internet Access in the world. The global internet access market grew by 13% in 2008 to reach a value of $184.8 billion. The compound annual growth rate of the market in the period 2004-2008 was 14.9%8. (Refer Appendix I) 8 Datamonitor - Global Internet Access- June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=F85BBC63-3025-4BED-9AA8- 10

- 11. In 2013, the global internet access market is forecast to have a value of $298.8 billion, an increase of 61.7% since 2008. The compound annual growth rate of the market in the period 2008-2013 is predicted to be 10.1%9. Thus, the growth rate of both India and China is much higher as compared to the growth rate of Internet Access Market across the globe. India and China both fare well in terms of current as well as future growth rate. When compared against countries within Asia- Pacific, India leads the internet access market, with 48.6% of the total revenues. In comparison, China accounts for a further 26.9% of the market's revenue.10 9 Datamonitor - Global Internet Access- June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=F85BBC63-3025-4BED-9AA8- 10 Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657- D9B8-4C96-A51C- 11

- 12. By comparing, Indian Internet Access Market growth rate with that of Chinese, it reflects that the Indian market is growing faster than the Chinese market. But it would not be prudent to conclude that this indicates that the Indian Internet Access is performing better. India has currently just 11.1 million subscribers, whereas China has already 77.7 million internet users. Given, the similar population size and demographics of both the nations, this is a huge difference, indicating that India is lagging behind China is the Internet Access market and has a long way to go before it catches up with its neighbour. In the latter sections of the report I have to tried to identify the primary areas in which China has performed better than India, which has led to greater internet penetration. However, first let us try to understand the Internet Access market situation in India currently. This can be ascertained by using the Porter’s five forces analysis as described in the next section. 12

- 13. PORTER’S FIVE FORCES ANALYSIS Summary Figure 1 : Forces Driving Competition in the Internet Access Market in The internet access market has been analyzed taking Internet Service Providers (ISPs) as players. The key buyers are taken as end-users, and network owners and manufacturers of the hardware and software involved as the key suppliers. Buyers in this market have fairly low switching costs, which strengthens their power to an extent. However, buyer power is prevented from becoming more than moderate by the vast amount of potential customers available to market players, and the importance of the service being offered to consumers. This market is characterized by strong supplier power, with the cost of switching for market players and the importance of quality contributing to this. Potential entrants to this market are likely to be attracted by the dynamic market growth in recent years. However, they face a tough job competing with established companies with a strong reputation and the likelihood of price competition with incumbents seeking to see off new competitors. Substitutes to this market are, at present, virtually non-existent. Where substitutes do exist they are often not a strong threat to the Internet as a whole. Strong market growth in recent years prevents rivalry from being any more than moderate. 13

- 14. Buyer Power Figure 2 : Drivers of Buyer Power in the Internet Access Market in India ISPs offer their Internet access services to customers ranging from individual consumers to large corporations. Offers vary according to factors such as speed and price. The large numbers of customers available to market players weakens buyer power to an extent. Switching costs are moderate, and can include the time required to leave one contract and move to a competing contract, or cancellation fees. In practice, customers are prone to changing ISPs in order to gain better value for money. Brand reputation can play an important role in this market. However, price is an important consideration for buyers, along with factors such as speed of access and quality of connection. The market offers some differentiation for example, one player may offer consumer Internet access as a standalone service, while another bundles it with telecom or cable TV services. Internet penetration is currently low in India (less than 10% of the population) with the divide between urban and rural areas very much apparent. However, as internet penetration grows in India, all kinds of customers see Internet access as highly important and for many businesses Internet access is seen as vital. Overall, buyer power is assessed as moderate in this market. 14

- 15. Supplier Power Figure 3 : Drivers of Supplier Power in the Internet Access Market in India ISPs act as intermediaries between their customers and the telecommunication infrastructure that underpins the Internet (and telephony) technology: ADSL lines, servers, packet switching software just to name a few. Some ISP, such as the dominant incumbents VSVL and BSNL own and operate an extensive physical network themselves. For these companies, key suppliers are manufacturers of the hardware and software involved, such as Cisco Systems. There are increasing numbers of ISPs that do not own a network and purchase wholesale access to the necessary infrastructure from an owner-operator, and then offer it at retail to end-users. While it is unlikely that ISPs of either type will integrate backwards, since the upstream businesses are very different to their own, most network owner-operators have already integrated forwards into the retail ISPs market, and are competing directly with ISPs that do not own networks. Network manufacturers are not completely reliant on the ISP market for their revenues, as they can also operate in markets such as corporate intranet; network owners usually generate revenue from telephone services, directory publishing, advertising, and their own ISP retail business as well as wholesale Internet access. Overall, supplier power is assessed as strong. 15

- 16. New Entrants Figure 4 : Factors Influencing the Likelihood of New Entrants in the New players are attracted to this market by the continuing health of growth rates in recent years. Players without their own infrastructure are usually able to buy access to telephony networks. This reduces the capital requirements for market entry, although customer demand for ever-increasing bandwidth may mean that investment in infrastructure will be needed for future growth. Retaliation in terms of price competition is likely in this market. The majority of the market is owned by a small number of large incumbents - 10% of ISPs have around 90% of subscribers - which may be off-putting to potential new entrants. In order to gain clients, new entrants need to differentiate themselves from incumbents, which is not an easy task when selling a commoditized service that can be specified completely with a few parameters such as bandwidth and down/up load time. Overall, there is a moderate likelihood of new entrants to this market. 16

- 17. Substitutes Figure 5 : Factors Influencing the Threat of Substitutes in the Internet The internet is a versatile tool that can be used for a whole spectrum of everyday activities and, presently at least, there are no real alternatives that can match this range. The Internet has developed so rapidly because it is itself a substitute for many other services and products. These include traditional forms of advertising, news providers, music (and increasingly video) physical media such as CDs and DVDs, 'bricks and mortar' outlets for supplying goods and services, and communication services such as mail and telephony. The benefits of some older substitutes are assessed as small, as the Internet alternatives have clearly demonstrated their popularity with consumer and corporate customers. Furthermore, the Internet can exist relatively unthreatened alongside other ‘substitutes’ such as 'bricks and mortar' retail outlets. However, to take two examples, for consumers with concerns over the security of online financial transactions, or businesses who wish to advertise to segments of the population who are not online, the older substitutes will retain advantages. Overall, the threat of substitutes is weak. 17

- 18. INDIA CHINA - COMPARISION India and China account for 40 percent of the world population (primarily in rural areas), have rich histories and aspire to superpower status, share a border with contended territory, have growing middle classes that are an important global market, and are major producers. China and India have very different political and economic systems, but both have assigned high priority to information technology and the Internet, and the Internet may play a pivotal role in the development of the relationship between the two nations. Their differences act as an experiment, shedding light on Internet diffusion and development in general. India and China are home to a large percentage of the world's impoverished people. If the Internet is to improve the state of human development, it Figure 6 : Trends in growth of Internet Users must succeed in India and China. Internet is diffusing rapidly in India and China. It is estimated that by 2010, each of them will have more Internet users than in US. India was connected to Internet earlier than China when Department of Electronics (DOE) established ERNET (Educational and Research Network) in 1986 with the help of United Nations Development Program (UNDP). ERNET was connected to UUNet (UNIX to UNIX Network) technologies in the US through IP Figure 7 : Number of Internet Users in India and China (Internet Protocol) connection in 1989. It was further connected to the US National Science Foundation (NSFNET) in 1990. In contrast, 18

- 19. Internet connectivity in China started in 1993, and by 1994, China had twice the number of Internet hosts and 3.5 times Internet users as compared to India11. The following table and graphs reflects the growth in the number of computers connected to Internet in both India and China. Here as well, it can be observed that China though started late and was in the back foot originally, it gathered momentum and superseded India over the years. Figure 8 : Comparison of Internet Hosts Figure 9 : Trends in growth of computers connected to Internet 11 Yogesh Sumana and V P Kharbanda - Internet diffusion in India and China ¾ Who holds the edge - March 2005 19

- 20. Having ascertained that China is placed better with respect to India in terms of number and consistent growth, let us now try to analyze the reasons behind China’s success in increasing Internet usage. For the study and comparison I have used a comprehensive, six-dimension framework for characterizing the state of the Internet in a nation. Following is the list and details of the 6 parameters used in the study: - PARAMETER DETAILS Pervasiveness The primary indicator of pervasiveness is the number of Internet users per capita. This is the best indicator of the diffusion of Internet across masses. Geographic Nearly all nations have some Internet connectivity today, but access may only be Dispersion available in large cities. As such, I have selected geographic dispersion as my second dimension. This variable measures the concentration of the Internet within a nation, from none or a single city to nationwide availability with points-of-presence (POPs) or toll free access in all first-tier political subdivisions and common rural access. Organizationa Organizational infrastructure is a measure based on the state of the ISP industry and l market conditions. A highly rated nation would have many ISPs and a high degree of Infrastructure openness and competition in both the ISP and telecommunication industries. It would also have collaborative organizations and arrangements like public exchanges, ISP industry associations, and emergency response teams. Connectivity Connectivity infrastructure is the fourth dimension. It is based on domestic and Infrastructure international backbone bandwidth, exchange points, and last-mile access methods. A highly rated nation will have high-speed domestic and international backbone connectivity, public and bilateral exchange points, and a high proportion of homes with broadband connections. Sectoral While widespread access is desirable, the payoff is in use of the Internet. This is Absorption accounted for in the sectoral absorption dimension, a measure of the degree of Internet utilization in the education, business, health care and public sectors. These sectors are seen as key to development, and were suggested by the measures used in the United Nations Development Programme (UNDP) Human Development Index. Sophistication Sophistication of use is a measure ranking usage from conventional to highly of Use sophisticated and driving innovation. A relatively conventional nation would be using the Internet as a straightforward substitute for other communication media like telephone and FAX, whereas in a more advanced nation, applications may result in significant changes in existing processes and practices and may even drive the invention of new technology. PERVASIVENESS 20

- 21. Having determined the various parameters on which we will be comparing China and India, let us look at each of these parameters in detail. Minges and Gray cite seven determinants of Internet pervasiveness: affordability, complementary infrastructure (PCs, telephone lines and electricity), literacy, education, awareness, computer literacy, and language12. Let us look at each of these : - Affordability is a function of income and the cost of Internet access. While both nations are largely impoverished, Chinese income is higher. In the late 1980s, China exchanged Karl Marx's slogan "from each according to his ability, to each according to his needs" for Deng Xiaoping's "getting rich is glorious." by 2005 the per capita GDP of China was higher than that of India. This is illustrated in the below figure 13. Figure 10 : GDP per Capita comparison 12 Michael Minges and Vanessa Gray, "The Impact of Socio-Economic Factors on Intenet Use in South East Asia," Proceedings of the 2002 International Networking Conference, Washington D.C., July 2002. 13 Maps of.net - http://mapsof.net/The_World/static-maps/png/gdp-per-capita-ppp-world-map-2005-copy-one-colour 21

- 22. The following figure also reflects that current and estimated gap in the per capita GDP between the two nation as compared to that of US14 : - China's greater income combines with lower access costs and lower costs of computers, to make the Internet more affordable. Part of China's relative advantage in access cost reflects dramatic improvement in telecommunication since they decided to invest in this area post 1990. This decision predates Figure 11 : Comparison of per capita GDP Chinese awareness of the Internet, but it has certainly facilitated its growth. Chinese telecommunication progress is illustrated by the rapid growth in the number of landline telephones. This can be observed in the Figure 12 : Comparing Teledensity figure 1215. 14 Global Security - http://www.globalsecurity.org/intell/library/reports/2005/nic_globaltrends2020_china_india_risin_gdp.gif 15 Resilience Science - http://rs.resalliance.org/tag/development/ 22

- 23. Furthermore, China has also surpassed the United States as the world's largest mobile market. This growth parallels growth in the general economy - the Chinese made the decision to invest in telecommunication, and they were able to afford it. China also has a commanding lead in PCs. The ITU estimates approximately 25 million PCs in China versus six million in India, and the Computer Industry Almanac estimates 34 million versus 5.2 million16. Electricity to power PCs and network equipment is also more abundant in China. (This can be a limiting factor in a rural area). China also leads in education and literacy indicators. Figure 13 17 illustrates that adult literacy rate in China is much higher than that in India. Figure 11 : Comparison of Adult Literacy Rate Awareness of the Internet is difficult to compare. One would expect it to correlate with usage, but Indian city dwellers see constant ads and information about the Internet. We assume that computer literacy would correlate with installed PCs, since Internet access in public schools is not widespread. Language is multifaceted determinant. India has an advantage in that the educated people who are most likely to use the Internet speak at least some English, the dominant language on the Internet at this time. This advantage is offset by greater language diversity in India. India has 387 living languages and China 201. Their respective language diversity indices are .48 and .93 respectively. (The higher the value, the 16 International Telecommunication Union (ITU), World Telecommunication Development Report 2002, at http://www.itu.int/ITU-D/ict/publications/wtdr_02/index.html; Computer Industry Almanac, at http://www.c-i-a.com/. 17 http://lh4.ggpht.com/fhuebler/SFXEY9hTRkI/AAAAAAAAAWY/XkPzDaN0-bg/20080615-adult-lit.png 23

- 24. less likely it is that two people will speak the same language). This is due in part to 70 percent of the Chinese population speaking Mandarin while only 50 percent speak Hindi in India 18. China is well aware of the importance of English, and has embarked on a program of English-language training. China's advantage over India in the indicators I have presented leads us to expect that the Chinese will continue to lead in pervasiveness for some time. Factors like economic productivity, telecommunication infrastructure, PC production, and literacy cannot be changed rapidly. 18 Larry Press, William Foster, Peter Wolcott & William McHenry - Internet in India and China - http://outreach.lib.uic.edu/www/issues/issue7_10/press/index.html 24

- 25. GEOGRAPHIC DISPERSION Large rural populations are the major block to geographic dispersion in both nations. Both have made commitments to provide telephone connectivity to all villages, but widespread rural Internet connectivity will be difficult for either to achieve. Every factor we discussed under pervasiveness presents a larger problem in rural areas than cities. Both in India and China the gap between Urban and Rural penetration of Telecom is extremely high, as reflected in figures 1419 and 1520. Figure 12 : Urban Rural divide in China Figure 13 : Widening Urban Rural divide in India 19 Gallup News Service - Tao Wu and Steve Crabtree - China's Consumer-Goods Gaps Represent Budding Market Opportunities - March 30, 2007 20 Continuous Computing - Indranil Chakraborty - Ringing in rural India - http://www.ccpu.com/news/inthenews/20051003- india.html 25

- 26. Note that even in villages with telephone connectivity, service may be minimal. There are multiple households sharing a single telephone connection. These are large, geographically diverse nations, and as in other developing nations, there is insufficient demand to justify investment in backbone connectivity to rural areas, particularly where roads are bad. Government policy can help. As a licensing condition, regulators can require operators to cover rural area or a universal service fee may be set aside. Both India and China can learn from the Chilean experience. The Chilean government asked telephone providers to bid for subsidies required to cover rural areas with success21. Low-earth orbiting IP satellite technology may one day solve this problem, but rural connectivity is a daunting challenge in both India and China. While the recent bankruptcy of few IP satellite companies like, Teledesic, is discouraging, this technology will be more feasible in the future. The G8 industrial nations pledged billions of dollars for IT for development. Could they or an organization like the United Nations accept the challenge of rural village connectivity and provide capital for such a venture? India appears to give higher priority to rural networking than China. The Ministry of Information Technology has a Working Group on Information Technology for Masses that issued a report recommending 56 actions in infrastructure and service, electronic governance, education and raising mass IT awareness in October 2000. If they succeed, they may surpass China in rural networking and hence geographic dispersion. 21 Björn Wellenius, "Extending Telecommunications Service to Rural Areas - the Chilean Experience," Public Policy for the Private Sector, Note 105 (February 1997), World Bank, http://www1.worldbank.org/viewpoint/HTMLNotes/105/105welle.pdf. 26

- 27. ORGANIZATIONAL INFRASTRUCTURE The transition from government-owned telecommunication monopoly to greater competition has been driven by politics and government policy in both nations. India and China present a stark contrast in governance. The UNDP surveys five measures of democracy in a nation, and India has a clear lead over China on each of them22. Few would question that there is greater freedom of expression, the press, the vote, and civil liberties in India. India's democracy has spawned many political parties, strong local governments, a coalition national government, and lively public debate. The complex political landscape of India has made it more difficult for them to formulate policy and execute plans than it is for China. This has facilitated China's industrial policy to be focused on infrastructure and high technology. China has been able to execute plans effectively by allocating resources to competing government-owned enterprises. For example, in 1996, the Chinese State Council made the decision to allow the Internet and to connect all provincial capitals. Within a year, there were competing ISPs in every capital, one using fiber, the other VSAT. India set the same goal in 1998, but achieved it many years later. The pattern of government planning combined with competition among partially or wholly government- owned organizations has been observed in Singapore, Vietnam and Cuba as well as China, and the ITU has also observed its efficacy in China: "The main form of competition has been between ministries of the government ... although it is unlikely that this form of competition between state-owned enterprises would feature in many economics textbooks, it has proved remarkably effective. The key underlying factor is the will of the state to invest in, and prioritize, telecommunication development"23 The UNDP also reports six indicators of the rule of law, governance effectiveness and corruption, and, China outscores India on each. This also contributes to China's ability to execute and to the confidence of investors. The Indian government is working to overcome inefficiency and corruption, as evidenced in part by strong support for the IT Action Plan. 22 2002 United Nations Development Programme Human Development Report, http://www.undp.org/currentHDR_E/ 23 Larry Press, William Foster, Peter Wolcott & William McHenry - Internet in India and China - http://outreach.lib.uic.edu/www/issues/issue7_10/press/index.html 27

- 28. CONNECTIVITY INFRASTRUCTURE In addition to factors we have already discussed, a trade policy and other factors that encourage investment and the availability of a skilled work force are also key determinants of connectivity infrastructure. India has a history of ambivalence about openness and trade versus self-sufficiency dating back to Gandhi, and before the 1990s, China was also insular and tied to the Communist block. Since the 1990s, Chinese trade policy has been more open and eclectic, resulting in significantly faster growth in imports, exports and the ability to attract foreign investment than India. This parallels the growth in GDP that we noted earlier. Figure 1624 depicts that FDI confidence index in China is higher that that in India. Some of this increase in trade and ability to attract investment capital is due to pressure from the World Trade Organization (WTO). China has used the process of WTO accession to stimulate and make irreversible substantial trade liberalization and more broadly based reforms. At the same time, India will see increased trade as they continue implementation of their IT Action Plans. In addition to the volume of investment capital, we must consider its allocation. In the long run, India's greater diversity and openness may pay off, and Figure 16 : FDI confidence Index India vs China China may find they have allocated resources sub-optimally, but, as recent events have shown, market economies can do the same. Connectivity infrastructure also requires educated technicians and managers. China has a higher percentage of tertiary school students in science and engineering (43 percent versus 25 percent in India), but India has excellent technical universities and a vibrant trade-school industry. Chinese telecommunication employees may also be more efficient - the number of mainlines per employee is 159 24 Vox - http://raj823.vox.com/library/posts/tags/news/ 28

- 29. in China and only 77 in India25. Networking professionals (and sophisticated users) are also generated by hardware and software industries. India was an early mover in software export and IT-enabled services (which include low-skill work such as data entry). China is however behind India in terms of software exports. China enjoys a clear lead in IT hardware manufacturing. For eg:- Chinese companies produced $23.9 billion in computer products in 2001, an increase of 24 percent over 200026. Thirty-nine percent of Chinese exports are high- and medium-tech products versus 16.6 percent in India, and, as we have seen, the absolute numbers are much greater for China. It remains to be seen whether India's Action Plan for Hardware Development, Manufacture and Export will enable them to close this gap. China's close commercial relationship with Taiwan and the Hong Kong handover provide similar sources of capital and expertise. The Internet and telecommunication in Hong Kong and Taiwan are far more advanced than in China. In spite of long British rule and Taiwanese independence, there are strong cultural and business ties throughout the Chinese world. (Even before the handover, 46.75 percent of China's switched, outbound telephone minutes were to Hong Kong and another 8.02 percent to Taiwan, and Hong Kong ranks second to the U.S. in Internet connectivity from China)27. There are also ties to the Chinese in Singapore. 25 Larry Press, William Foster, Peter Wolcott & William McHenry - Internet in India and China - http://outreach.lib.uic.edu/www/issues/issue7_10/press/index.html 26 "Mainland China," Global Sources (14 January 2002), at http://www.globalsources.com/MAGAZINE/CP/0201/OUTCH.HTM 27 Larry Press, William Foster, Peter Wolcott & William McHenry - Internet in India and China - http://outreach.lib.uic.edu/www/issues/issue7_10/press/index.html 29

- 30. SECTORAL ABSORPTION University networks are growing in both nations, but the Chinese are more effective, and have gained a significant and strategic lead in the university that will trickle down to lower levels of school. Both nations have plans to wire schools, but that does not insure their execution, and very few lower schools are connected in either nation. The greater number of PCs in schools (and concomitant awareness and computer literacy) gives China an edge in this area, but both nations have a long way to go if they are to achieve their plans. Political will is probably the deciding factor in achieving school connectivity. I expect that increased trade will lead to increased use of the Internet to integrate business supply chains and software project management. The expatriate communities mentioned above may play a key role here. There is little evidence of use of the Internet in the health care sector in either India or China. This is typical of developing nations. Since 1995, more than 60 laws have been enacted governing Internet activities in China. More than 30,000 state security employees are currently conducting surveillance of Web sites, chat rooms and private e-mail messages - including those sent from home computers. Thousands of Internet cafes have been closed in recent months, and those remaining have been forced to install "Internet Police 110" software, which filters out more than 500,000 banned sites with pornographic or so-called subversive content. Dozens of people have been arrested for their online activities; in 2001, eight people were arrested on subversion charges for publishing or distributing information online28. While this sort of constraint may seem to promise attractive stability to some potential investors, it may have unintended side effect of slowing applications in education, entertainment, commerce and other areas. 28 Xiao Qiang and Sophie Beach, "The Great Firewall of China," Los Angeles Times (25 August 2002), and at http://www.cpj.org/news/2002/China_Firewall25aug02.html. 30

- 31. SOPHISTICATION OF USE Nearly forty percent of the world population lives in rural areas of nations with low-income economies. In India the rural population is over 70 percent. China has 900 million rural residents, and has recently liberalized restrictions on movement from rural to urban areas. If necessity is the mother of invention, these nations are in a good position to innovate in discovering and deploying applications that are of value to rural populations. If the Internet can improve rural education, health care, entertainment, news, economy, etc., the flow of people to crowded cities, a major demographic trend of the last century, may be diminished. We would welcome innovation in small PCs and Internet appliances, satellite and terrestrial wireless systems, solar energy systems, understanding rural IT requirements, etc. India has several projects pursuing village connectivity, but there has not been widespread deployment as of this time. In anticipation of a proliferation of Internet devices and multimedia applications, China has been developing equipment for and deploying IP v6. This experience and infrastructure may lead to innovative applications, as may their experience with VOIP. 31

- 32. RECOMMENDATIONS FOR INDIA Having compared India and China’s Internet Access across various dimensions, in the previous sections following table enlists the various parameters and which country is more stronger in the same : - Dimension Advantage Pervasiveness Users C Hosts C Geographic dispersion Top-tier political divisions with POPs C Number of cities with POPs C Sectoral absorption Commercial E Education C Government I Health E Connectivity infrastructure Domestic backbone E Broadband access C Exchanges C International bandwidth C Organizational infrastructure Telecommunication competition I International gateway competition I Backbone competition E Access provider competition C Coordinating organizations E Sophistication of use C C = China, I = India, E = Even The above table reflects that India has a lot of catching up to do with China. China has performed better than India in various parameters like Pervasiveness, Geographic Dispersion, Infrastructure and greater competition amongst internet access providers. This comparison has helped me identify the key areas where India needs to progress inorder to catch up with China, if not supersede, in terms of Internet Access. Based on my study I recommend adopting the following framework for ensuring further enhancement and sustainable growth of the Internet infrastructure in India. 32

- 33. Figure 14 : Proposed Framework for India Inorder to improve the Internet Access in India there is an important role that Government, Businesses and Consumers need to play. Only if there is synergy between the three entities, can India witness growth in its Internet segment. Following are my recommendations as to how the three entities can collaborate and script a success story for India : - 33

- 34. GOVERNMENT CORPORATES CONSUME R Figure 15 : Proposed Synergy Government • The main goal of government should be to improve the infrastructure currently available in the country. As observed, the infrastructure currently prevalent is not up to the required level, which is the major impediment in increasing and fostering Internet Usage. The infrastructure should be developed in rural areas as well, and they should be targeted as the next key avenue for growth. Infrastructure development should encompass all entities that directly or indirectly impact Internet Access, like Telephone connectivity, broadband access, availability of computers at cheap price, availability of continuous electricity, etc. • Government should take adequate steps to attract investment from the private sector as well, which could assuage the government from the financial burden. • Government should play key role in making the market more open and increasing competition amongst internet service providers. This would be the most effective way of ensuring greater Internet penetration. • Government should provide tax benefits to corporates who extend internet penetration into rural areas. Since there is dearth of suitable infrastructure and the initial setup costs are too high, currently there is no motivation for corporates to venture into rural areas. In such a scenario government should play a proactive and constructive role in providing the right set of incentives for the Internet Service Providers to venture into rural India. 34

- 35. • Key steps should be taken to increase usage of computers in schools and universities and make IT education as a mandatory subject, given that IT has huge potential for growth in India across various spectrums. Corporates • Internet Service Providers should take adequate steps to improve their technological competitiveness. Rather than having a complacent and reactive approach, firms should be proactive and quick at introducing and adopting latest innovations in the Internet field. This is not only applicable to Internet Service Providers but should also span to other industries that directly or indirectly impact the industry. • Firms should remodel their business models to make it more robust and adaptive to the changing market dynamics. It is imperative to implement cost-effective processes and also ensure quality training of the IT workforce. This will enable Indian Internet Service Providers to not only excel in India but also project on the global canvass. • The dependence on government initiatives and support should be reduced and the firms should strive to become self sustaining and independent. As a result of this, an unstable or complacent government, would have little impact on the growth of the organizations, hence would not be an impediment for the corporate strategies of Internet Service Providers. • Effective steps ought to be taken to educate people about the importance of Internet and the advantages of using Internet. Public-Private Partnerships in this aspect as result in win-win situation for all. • Internet Content providers should cater to all segments on India and not just the urban segment. It is important to develop websites in local languages inorder to increase penetration and acceptability within the rural masses. • IT firms should collaborate horizontally to increase the penetration of Internet and Computers within India. This could be manifested by acollaboration between Internet Service Provider and a PC manufacturing firm, both collectively marketing and providing low cost products and services for the rural population. 35

- 36. Consumers • The consumers have to be more broad minded and open to accepting new technologies and innovations. Being averse to changes would only prove to be detrimental for the masses. It is of paramount importance that people across demographics comprehend the importance and potential of Internet. • Children should be encouraged at an early age to learn computing and understand the basic features and functionality of computers. This will set stage for the future development of IT in India. 36

- 37. CONCLUSION Indian universities joined the Internet in 1988, six years before Chinese universities. Knowing only that, we might expect India to have a commanding lead in Internet diffusion today; however that is only a small part of the story. The Internet was very different in 1988 than it is today. Few outside a small group of researchers and technicians knew of the Internet, and they used it primarily for sharing technical information and facilitating the development of standards and networking technology. In 1995, when China seriously considered the Internet, the wider public, including policy makers and politicians, were aware of its implications and the World Wide Web protocol was beginning its rapid proliferation. In some sense, the race did not really begin until the mid 1990s. After a delay to consider the economic opportunity afforded by the Internet and the cultural and political risks of open access, the Chinese made the Internet a priority, and rapidly overtook India's early lead. This success was due in large part to reform that began in the late 1980s, with no consideration of the Internet. Under Deng Xiaoping, China instituted market reforms and liberalized trade policy. The success of these reforms provided resources for and an openness to Internet diffusion. At the same time, China focused its industrial policy on infrastructure and high technology. This led to dramatic expansion of telecommunication infrastructure, personal computer manufacturing and adoption, awareness of the Internet and information technology applications, and a pool of trained demanding users and the managers and technicians to serve them. These resources were all available when the Chinese decided to connect to the Internet and make it a priority. India was not as well prepared or as quick to act when it became clear to politicians and policy makers that the Internet could be important infrastructure. Their response was a series of publicly visible action plans with high-level industrial and political support. In a sense, India joined the experimental Internet before China, but did not assign high priority to the modern Internet until the first IT Action Plan in 1998. The political systems of the two nations have also led them to different approaches to the Internet. China is attempting to maintain control over access and content, while India's Internet is open. While the incumbent telecommunication companies and their government supporters remain strong in both nations, India has moved toward an open market with licensing of telecommunication and Internet service providers. Privatization has gone more slowly in China, where a strategy of competition among government owned enterprises has been pursued in the large ISP market. Pressure from the WTO and market forces may dilute this policy, bringing the two closer together. For the time being, China has a solid lead over India. However, China is no longer leading or equal on every dimension, as they were earlier, and, when considered on a per-user basis, India is not as far behind as it first appears to be. If the recommendations suggested are implemented India can take the lead and elevate to the pinnacle of 37

- 38. Internet Industry and emerge as leading global player in this segment. India has the potential to grow, all it needs is an impetus and the right direction to move ahead. 38

- 39. APPENDIX A Purpose : - Provides the current market value of Internet Access in India. Source : - Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657-D9B8-4C96-A51C- APPENDIX B Purpose : - Provides the current market volume of Internet Access in India. Source : - Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657-D9B8-4C96-A51C- 39

- 40. APPENDIX C Purpose : - Forecast of the Market Value of Internet Access by 2013 in India. Source : - Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657-D9B8-4C96-A51C- APPENDIX D Purpose : - Forecast of the Market Volume of Internet Access by 2013 in India. Source : - Datamonitor - Internet Access in India - June 2009 - http://www.marketlineinfo.com/library/Download.aspx?R=94CB0657-D9B8-4C96-A51C- 40

- 41. APPENDIX E Purpose : - Provides the current market value of Internet Access in China. Source : - Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- APPENDIX F Purpose : - Provides the current market volume of Internet Access in China. Source : - Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 41

- 42. APPENDIX G Purpose : - Forecast of the Market Value of Internet Access by 2013 in China. Source : - Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- APPENDIX H Purpose : - Forecast of the Market Volume of Internet Access by 2013 in China. Source : - Datamonitor - Internet Access in China - June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=926A4ADC-4335-4419-A29C- 42

- 43. APPENDIX I Purpose : - Forecast of the Market Value of Internet Access by 2013 in World. Source : - Datamonitor - Global Internet Access- June 2009 - http://www.marketlineinfo.com/library/Download.aspx? R=F85BBC63-3025-4BED-9AA8- 43