What is Cost Segregation?

•

0 gefällt mir•245 views

Accelerate depreciation on commercial building to improve Cash Flow.

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Andere mochten auch (20)

Ähnlich wie What is Cost Segregation?

Ähnlich wie What is Cost Segregation? (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

What is Cost Segregation?

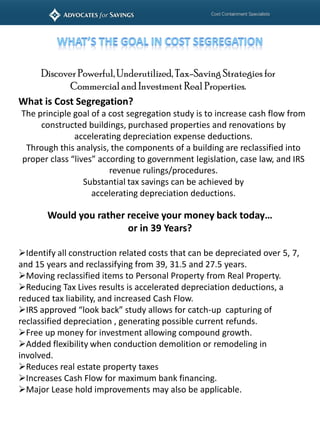

- 1. Discover Powerful, Underutilized, Tax-Saving Strategies for Commercial and Investment Real Properties. What is Cost Segregation? The principle goal of a cost segregation study is to increase cash flow from constructed buildings, purchased properties and renovations by accelerating depreciation expense deductions. Through this analysis, the components of a building are reclassified into proper class “lives” according to government legislation, case law, and IRS revenue rulings/procedures. Substantial tax savings can be achieved by accelerating depreciation deductions. Would you rather receive your money back today… or in 39 Years? Identify all construction related costs that can be depreciated over 5, 7, and 15 years and reclassifying from 39, 31.5 and 27.5 years. Moving reclassified items to Personal Property from Real Property. Reducing Tax Lives results is accelerated depreciation deductions, a reduced tax liability, and increased Cash Flow. IRS approved “look back” study allows for catch-up capturing of reclassified depreciation , generating possible current refunds. Free up money for investment allowing compound growth. Added flexibility when conduction demolition or remodeling in involved. Reduces real estate property taxes Increases Cash Flow for maximum bank financing. Major Lease hold improvements may also be applicable.

- 3. Detailed Engineering Approach Identify the specific project/assets that will be analyzed Obtain a complete listing of all project costs and substantiate the total project costs Inspect the facility to determine the nature of the project and it’s intended use Photograph specific property items for reference Review “as-built” prints, specifications. A/A contracts, bid documents, contractor invoices and other construction documentations Identify and assign specific project items to property classes Prepare quantitative take-offs for all the materials and payment records to compute actual unit costs “Catch up” or “Look Back” provision If a CCS is conducted on an existing structure The unclaimed depreciation on personal property components that were previously classified as real property can be deducted as a Code Sec 481 (a) adjustment in the year of change The automatic change of accounting rules of Rev. Proc. 2002-9 apply If a CCS is conducted on a building that was placed into service in a Tax Year that ended before December 30, 2003 The IRS will allow a tax payer to file amended returns to claim the benefits Interest is payable by the IRS on the refund

- 4. What is Cost Segregation? Does this increase my chances of being audited? The principle goal of a cost segregation study is to No. The chances of getting audited are not increase cash flow from constructed buildings, automatically increased. purchased properties and renovations by accelerating How long does a Cost Segregation study take? depreciation expense deductions. Through this For small to medium size projects, we typically analysis, the components of a building are reclassified issue the final deliverable three to six weeks from into proper class “lives” according to government the point that all information is received. legislation, case law, and IRS revenue Naturally, the time of year matters a great deal, rulings/procedures. Substantial tax savings can be consultant workload is much heavier in the achieved by accelerating depreciation deductions. periods just before filing deadlines. Upon receipt Why have I not heard about Cost Segregation of an engagement letter, a specific schedule for before? completion is assigned to each project based upon Though it has been around, in its current form, since client needs, time of year and, of course, IRS 1987; Cost Segregation was, for some time, almost deadlines. solely offered by Big 4 accounting firms and a handful What if my project is still under construction? of large real estate consulting companies who No problem here. In fact, this situation is good for serviced only the largest of clients. There were very both sides. Our Advisor will work with few qualified practitioners and, for small to medium construction personnel to document costs and size taxpayers, the service was cost prohibitive. Within other information to streamline the process as the last few years however, Cost Segregation has much as possible. become available, at a very reasonable cost, to Could I not just use my own smaller companies and individual property owners. architects/engineers? How does Cost Segregation work? For a few reasons, this is probably not a good Associates For Savings team of experts will gather idea. documentation, such as construction plans, contractor First of all, our architects, engineers and CPA’s are invoices, depreciation schedules, etc. From these specialists, in this field, with decades of Cost documents, we will identify the qualifying items and Segregation experience. They know the ins and associated costs to be reclassified into shorter-life outs not just of the construction project, but also categories. One of our consultants will visit the the accounting side documentation, tax law, etc. property to compare what was actually built against Architects and engineers alone are typically not the plans, and take photographs of the property. familiar with the many subtleties involved in a Results are aggregated and presented in a report, comprehensive study. along with relevant case law data, definitions, photo Secondly, we offer a combination of construction documentation and calculation details. industry professionals; in house CPA’s and full Is this all legal? time research staff provide you with the Absolutely! Over 1000 IRS revenue rulings and court assurance that your study will be fully compliant cases provide the necessary guidelines for proper with the latest changes in the tax law and court conduction of Cost Segregation studies. The IRS has cases. also recently issued an Audit Techniques Guide that Lastly, our team is experienced in defending our defines a quality Cost Segregation study. work in the event of an audit, at no additional charge.

- 5. What sort of documentation do I need? What sort of benefit might I expect? At the front end of a Cost Segregation study, we only The benefit of a Cost Segregation study lies in have to know certain basic information, such as the the timing of tax payments. Assuming a 35% capitalized cost, property location, placed-in-service Federal tax rate, an 8% discount rate, half-year date, etc. to provide an estimated benefit. Once convention, and no bonus depreciation, for engaged, the more information available, the better. every $1,000,000 of property reclassified from The following list is fairly comprehensive: 39 years has a cumulative present value of tax New Construction: deferral equaling approximately: The date of acquisition or “placed in service date” $195,000 for 5-Year Property The capitalized costs $178,000 for 7-Year Property Complete set of plans $108,000 for 15-Year Property Contractor’s final application for payment or similar In other words, the benefit is approximately $.19 document for every dollar reclassified to five years from A complete list of all change orders with a brief thirty-nine years. description of each No amended return? Even if my building was A copy of the specifications (If readily available) acquired/constructed in a prior year? Rent roll or similar document (For multi tenant That’s right. IRS provisions will allow you to “catch buildings only) up” on missed depreciation by filing a 3115. No A list of owner incurred costs above and beyond the need for an amended return. General Contractors costs. Examples include What if there is a 1031 exchange associated with architectural and engineering fees, permits, testing my property? and materials paid for directly by the owner In some situations (certainly not all) this can Purchased Properties: reduce the benefit if the tax basis is decreased. The date of acquisition or “placed in service date” We recommend speaking to us about the specifics The capitalized costs of your property; together we can devise the best Depreciation schedule plan of attack for you. Plans, site plans and surveys (If available) I am interested in learning more. Do you charge Square footage of buildings and site for estimates? Appraisal (If available) No, we would very much like to hear from you. Rent roll or similar document (For multi tenant Let us discuss your property and tax situation in buildings only) order that we might maximize your tax savings. A site visit is an essential part of a good study; Do I need all the documentation available for the sufficient information can be collected, from such a initial estimate of benefits? visit, to accurately perform a Cost Segregation study No. While more information will result in a more in the event that construction drawings and cost accurate estimate, we can utilize information information are not available. collected from similar projects to estimate Will I need to file an amended return? benefits for your situation; of course, more No. IRS Revenue Procedure 96-31 allows a taxpayer detailed information produces a more accurate to file a form 3115 Automatic Change in Accounting estimate. rather than an amended tax return. This form can be used to fix depreciation as far back as 1987. If you wish our team of experts will prepare the 3115 for you. Tactical Leverage LLC / Thomas J. Tysl / 1701 W. Northwest Hwy Grapevine, Texas 76051 817.404.9011 / Fax 817.224.2924 / ttysl@advocatesforsavings.com