Choosing a de-risking roadmap

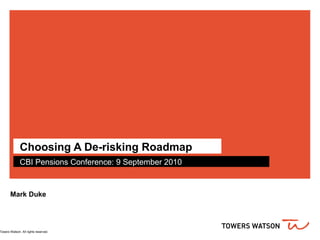

The document discusses various options for de-risking pension plans including enhanced transfer values, pension increase exchanges, early retirement exercises, and reducing liabilities through changing plan design or buying annuities. It notes that options need to be chosen in the right order while locking in asset gains and continuing to reduce interest rate and inflation risk. Surveys show schemes are taking steps like asset de-risking, funding improvements, and using insurance products to control risk. Frameworks with clear philosophies, metrics, and targets are important to establish strategy and operationalize de-risking over time. Plans should monitor funding ratios and pricing to determine optimal times to purchase de-risking options.

![Risk reduction: A Shopping List ,[object Object],[object Object],[object Object],[object Object],[object Object],Reducing the liabilities De-risking the assets Insurance solutions Buy-in (annuity) Longevity swaps Synthetic buy-in Pension captives Phased/structured buy-out Need to choose the right options in the right order Lock into asset gains – set triggers Diversify return seeking assets Use options to manage equity risk Continue to reduce interest rate and inflation risk](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Andere mochten auch

Andere mochten auch (7)

Ähnlich wie Choosing a de-risking roadmap

Ähnlich wie Choosing a de-risking roadmap (20)

Mehr von Confederation of British Industry

Mehr von Confederation of British Industry (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Choosing a de-risking roadmap

- 1. Choosing A De-risking Roadmap CBI Pensions Conference: 9 September 2010 Mark Duke

- 3. Fitting It All Together Control Hedge Shrink Governance

- 4. What de-risking steps are schemes taking? Source – 2010 Towers Watson survey

- 5. Where it begins Major risk factors: Equity, Credit, Currency, Longevity, Rates, Inflation

- 6. Planning options Funding level Time Buy-out Ongoing gilts Ongoing 1. How much? 2. By when? A B C 3. How? (balance of contributions + investment returns + risk tolerance) How much? By when? How? BUSINESS PLAN

- 8. Risk measurement and aspirations Risks being run within the Pension Scheme INSERT SECTION TITLE Risk budget

- 9. Is the window open? Optimal purchase time? Pensioner only funding ratios (illustrative) Track pricing against your targets and be ready to act

- 10. Managing the plan Be able to act swiftly when the time is right Asset de-risking and funding Data cleansing Liability management Governance and monitoring Insurance products

Hinweis der Redaktion

- Subsidiary thinking can: Reduce target Reach target more quickly Lower contributions along the way by MAKING YOUR PENSION SCHEME WORK HARDER (just like a subsidiary) So, how do we tackle this?

- 5b. “how we think about and measure risk…” Challenge here is to give a better flavour what we’d really do. Having got into the what ifs earlier in the deck helps because it illustrates that talking scenarios is a very practical way of thinking about risk and is probably the only sensible way of thinking about uncertainty. Further it ensures that you stress test your preferred solution and don’t end up disappointed eg “my hedge has holes!” Big message is that we can help you do what matters most (and is achievable) first so that you don’t expend a huge amount of effort on clever things and miss the big problem or think you’ve solved a problem that pops up again. And measurement only has a purpose if it leads to outcomes. One of the annexes needs to be some intuitive/interesting risk tools and the way they help you make decisions about price and value. Another annexe needs to be about spending the risk budget efficiently (or opportunistically) on the asset side. There can also be a sense here that in order to deliver good corporate advice the corporate adviser needs to have all the data needed to run numbers and that we can do this very efficiently.

- Using Settlement Watch, which monitors the buy in price for a scheme to assess the time to transact a buy in, for a fictitious DB scheme, these graphs indentify windows of opportunity last year. When might it be possible to purchase a buy in as an investment and de-risking decision for less? Certain times last year clearly were better times to transact. A series of partial buy ins for different tranches of the scheme may be more cost effective than one buy out transaction – and different insurance providers may be more of less competitive Question which this raises are When might such a window open up again for my scheme? Will you spot it when it does? Will you be ready to transact at that time? Will your scheme be well positioned to transact at the best price possible without passing too much profit opportunity to the provider? Have you the tools and data needed to negotiate effectively with that insurer, or indeed for your insurance consultant to do so? Are you confident that there will not be any unexpected surprises? For example, the insurer discovering a £30m liability which you were not aware of? So how do we prepare schemes to spot their window of opportunity and be ready to take advantage of it cost effectively?

- Round table discussion. Family fortunes style quiz. Results used from corporate consulting seminar. Security 75% Track record of provider 12% Managing data risk 7% Speed of execution 4% Innovative approaches 1% Administration capability 1%