Budget Highlights - A Fiscally Prudent Budget

•

0 gefällt mir•1,241 views

Here's a short summary of the budget [ 29 Feb , 2016 ]

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Andere mochten auch

Andere mochten auch (16)

Ähnlich wie Budget Highlights - A Fiscally Prudent Budget

Ähnlich wie Budget Highlights - A Fiscally Prudent Budget (20)

Mehr von Tata Mutual Fund

Mehr von Tata Mutual Fund (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Budget Highlights - A Fiscally Prudent Budget

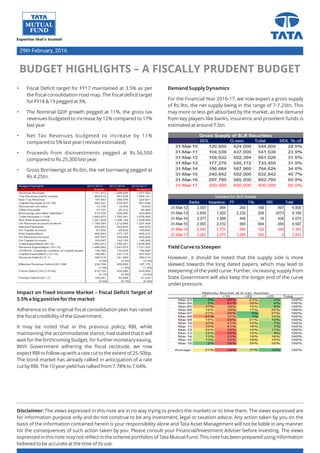

- 1. • Fiscal Deficit target for FY17 maintained at 3.5% as per the fiscal consolidation road map. The fiscal deficit target for FY18 & 19 pegged at 3%. • The Nominal GDP growth pegged at 11%, the gross tax revenues budgeted to increase by 12% compared to 17% last year • Net Tax Revenues budgeted to increase by 11% compared to 5% last year ( revised estimated) • Proceeds from disinvestments pegged at Rs.56,500 compared to Rs.25,300 last year. • Gross Borrowings at Rs.6tn, the net borrowing pegged at Rs.4.25tn. Impact on Fixed Income Market – Fiscal Deficit Target of 3.5% a big positive for the market Adherence to the original fiscal consolidation plan has raised the fiscal credibility of the Government. It may be noted that in the previous policy, RBI, while maintaining the accommodative stance, had stated that it will wait for the forthcoming budget, for further monetary easing. With Government adhering the fiscal rectitude, we now expect RBI to follow up with a rate cut to the extent of 25-50bp. The bond market has already rallied in anticipation of a rate cut by RBI. The 10 year yield has rallied from 7.78% to 7.64%. BUDGET HIGHLIGHTS – A FISCALLY PRUDENT BUDGET 29th February, 2016 Demand Supply Dynamics For the Financial Year 2016-17, we now expect a gross supply of Rs.9tn, the net supply being in the range of 7-7.25tn, This may more or less get absorbed by the market, as the demand from key players like banks, insurance and provident funds is estimated at around 7.5tn Yield Curve to Steepen However, it should be noted that the supply side is more skewed towards the long dated papers, which may lead to steepening of the yield curve. Further, increasing supply from State Government will also keep the longer end of the curve under pressure. Disclaimer: The views expressed in this note are in no way trying to predict the markets or to time them. The views expressed are for information purpose only and do not construe to be any investment, legal or taxation advice. Any action taken by you on the basis of the information contained herein is your responsibility alone and Tata Asset Management will not be liable in any manner for the consequences of such action taken by you. Please consult your Financial/Investment Adviser before investing. The views expressed in this note may not reflect in the scheme portfolios of Tata Mutual Fund. This note has been prepared using information believed to be accurate at the time of its use. Gross Supply of SLR Securities