Reci Q1 2016 Houston MOB Report

•

0 gefällt mir•171 views

An analysis of the Houston Medical Office market.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie Reci Q1 2016 Houston MOB Report

Ähnlich wie Reci Q1 2016 Houston MOB Report (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Reci Q1 2016 Houston MOB Report

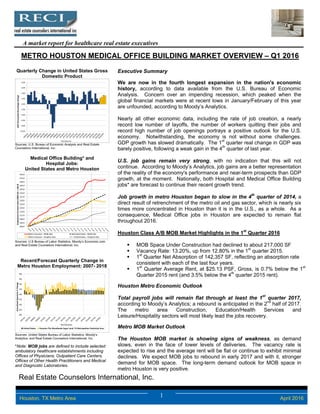

- 1. Real Estate Counselors International, Inc. 1 April 2016Houston, TX Metro Area A market report for healthcare real estate executives METRO HOUSTON MEDICAL OFFICE BUILDING MARKET OVERVIEW – Q1 2016 Quarterly Change in United States Gross Domestic Product Sources: U.S. Bureau of Economic Analysis and Real Estate Counselors International, Inc. Medical Office Building* and Hospital Jobs: United States and Metro Houston Sources: U.S Bureau of Labor Statistics, Moody’s Economic.com and Real Estate Counselors International, Inc. Recent/Forecast Quarterly Change in Metro Houston Employment: 2007- 2018 Sources: United States Bureau of Labor Statistics, Moody’s Analytics, and Real Estate Counselors International, Inc. *Note: MOB jobs are defined to include selected ambulatory healthcare establishments including Offices of Physicians, Outpatient Care Centers, Offices of Other Health Practitioners and Medical and Diagnostic Laboratories. Executive Summary We are now in the fourth longest expansion in the nation's economic history, according to data available from the U.S. Bureau of Economic Analysis. Concern over an impending recession, which peaked when the global financial markets were at recent lows in January/February of this year are unfounded, according to Moody’s Analytics. Nearly all other economic data, including the rate of job creation, a nearly record low number of layoffs, the number of workers quitting their jobs and record high number of job openings portrays a positive outlook for the U.S. economy. Notwithstanding, the economy is not without some challenges. GDP growth has slowed dramatically. The 1st quarter real change in GDP was barely positive, following a weak gain in the 4th quarter of last year. U.S. job gains remain very strong, with no indication that this will not continue. According to Moody’s Analytics, job gains are a better representation of the reality of the economy's performance and near-term prospects than GDP growth, at the moment. Nationally, both Hospital and Medical Office Building jobs* are forecast to continue their recent growth trend. Job growth in metro Houston began to slow in the 4th quarter of 2014, a direct result of retrenchment of the metro oil and gas sector, which is nearly six times more concentrated in Houston than it is in the U.S., as a whole. As a consequence, Medical Office jobs in Houston are expected to remain flat throughout 2016. Houston Class A/B MOB Market Highlights in the 1st Quarter 2016 MOB Space Under Construction had declined to about 217,000 SF Vacancy Rate: 13.20%, up from 12.80% in the 1st quarter 2015. 1st Quarter Net Absorption of 142,357 SF, reflecting an absorption rate consistent with each of the last four years. 1st Quarter Average Rent, at $25.13 PSF, Gross, is 0.7% below the 1st Quarter 2015 rent (and 3.5% below the 4th quarter 2015 rent). Houston Metro Economic Outlook Total payroll jobs will remain flat through at least the 1st quarter 2017, according to Moody’s Analytics; a rebound is anticipated in the 2nd half of 2017. The metro area Construction, Education/Health Services and Leisure/Hospitality sectors will most likely lead the jobs recovery. Metro MOB Market Outlook The Houston MOB market is showing signs of weakness, as demand slows, even in the face of lower levels of deliveries. The vacancy rate is expected to rise and the average rent will be flat or continue to exhibit minimal declines. We expect MOB jobs to rebound in early 2017 and with it, stronger demand for MOB space. The long-term demand outlook for MOB space in metro Houston is very positive. ‐10.0% ‐8.0% ‐6.0% ‐4.0% ‐2.0% 0.0% 2.0% 4.0% 6.0% 8.0% GDP Annualized Percentage Change Year/Quarter 100.0 104.0 108.0 112.0 116.0 120.0 124.0 128.0 132.0 136.0 140.0 144.0 148.0 152.0 156.0 Employment Growth Index (2006 Q4 = 100.0) Metro Houston ‐ MOB Jobs United States ‐ MOB Jobs Metro Houston ‐ Hospital Jobs United States ‐ Hospital Jobs ‐8% ‐6% ‐4% ‐2% 0% 2% 4% 6% 8% Annualized Quarterly % Change Year/Quarter United States Houston‐The Woodlands‐Sugar Land, TX Metropolitan Statistical Area

- 2. Real Estate Counselors International, Inc. 2 April 2016Houston, TX Metro Area A market report for healthcare real estate executives Historical and Forecast Employment for the U.S. and Metro Houston Economies Sources: United States Bureau of Labor Statistics, Moody’s Analytics, and Real Estate Counselors International, Inc. Medical Office Building Jobs: Metro Houston and the United States Sources: United States Bureau of Labor Statistics, Moody’s Analytics, and Real Estate Counselors International, Inc. Metro Houston Oil and Gas Extraction Jobs and Hospital and MOB Jobs Sources: United States Bureau of Labor Statistics, Moody’s Analytics, and Real Estate Counselors International, Inc. MOB job growth will flatten in the face of declining oil & gas extraction jobs. HOUSTON METRO ECONOMY Rapid total payroll job gains were reversed in the 2nd half of 2014. Job growth in metro Houston began to slow in the 4th quarter of 2014, a direct result of retrenchment of the metro oil and gas sector, which is nearly six times more concentrated in Houston than it is in the U.S., as a whole. Nationally, a drop in oil and gas production is clearly taking a toll on oil and gas industry firms regardless of their size. Bloomberg Intelligence reports that in the U.S. alone there are 3,870 idled oil and gas rigs. Even large firms such as Halliburton and Schlumberger, with their numerous operations throughout the world, are feeling the pullback of a lowered commodity price. For every 100 jobs that are lost in the oil and gas industry there is the potential that nearly 400 jobs will be lost in other sectors of the economy, especially Construction, Manufacturing, Professional and Business Services, Transportation/Utilities, Wholesale Trade and Financial Activities. Metro Houston created 4,600 jobs in March, according to the Texas Workforce Commission. In contrast, according to the Greater Houston Partnership, over the past 25 years, March employment growth has averaged around 14,000 jobs. The seasonally adjusted jobs data suggests an even weaker picture – that the metro area actually lost 2,600 jobs in March, 2016. This marks the second consecutive month of seasonally adjusted job losses. Job losses continue in sectors most closely tied to energy - oil and gas extraction, oil field services, the manufacture of fabricated metal products, the manufacture of oil field equipment, transportation and warehousing, engineering, and employment services. Nevertheless, job losses have yet to spill into the consumer oriented sectors. Thus far in 2016, the region added jobs in Construction, Real Estate, Accommodation and Food Services, Arts and Recreation, Healthcare and Government. Houston’s unemployment rate increased to 4.9% in March 2016, only slightly below the U.S. rate of 5.1%. We expect the metro Houston unemployment rate to rise above the U.S. rate sometime this year. U.S. oil production is forecast to continue its drop in 2016, in part, a result of rising inventories, according to Moody’s Analytics and the U.S. Energy Information Administration forecast. United States crude oil inventories have increased 20% since last August. Non-OPEC Oil production, overall, fell by 500,000 bpd in January 2016 as inefficient producers dropped out of the market, leading to job losses. The U.S. Energy Information Administration forecasts U.S production to average 8.6 million bpd in 2016 and 8.2 million bpd in 2017. The Healthcare sector is not immune from the turmoil in the Oil and Gas sector. Moody’s Analytics is forecasting MOB jobs to remain flat throughout 2016. They are also forecasting a slight decline in Hospital jobs this year. Recovery of these sectors is forecast for the second half of 2017. ‐8% ‐6% ‐4% ‐2% 0% 2% 4% 6% 8% 1989Q1 1991Q1 1993Q1 1995Q1 1997Q1 1999Q1 2001Q1 2003Q1 2005Q1 2007Q1 2009Q1 2011Q1 2013Q1 2015Q1 2017Q1 Annualized Quarterly % Change Year/Quarter United States Houston‐The Woodlands‐Sugar Land, TX Metropolitan Statistical Area ‐1.0% ‐0.5% 0.0% 0.5% 1.0% 1.5% 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% Annualized Quarterly % Change Metro Houston ‐ MOB Jobs United States ‐ MOB Jobs 100.0 105.0 110.0 115.0 120.0 125.0 130.0 135.0 140.0 145.0 150.0 155.0 Employment Growth Index (2006 Q4 = 100.0) Metro Houston ‐ MOB Jobs Metro Houston ‐ Hospital Jobs Metro Houston ‐ Oil and Gas Extraction Jobs

- 3. Real Estate Counselors International, Inc. 3 April 2016Houston, TX Metro Area A market report for healthcare real estate executives Metro Houston MOB Construction Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. Metro Houston MOB Demand/Supply: Deliveries, Absorption Vacancy and Change in Average Rent Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. Note: Percentage change in rent represents the quarter to quarter change. Trend of MOB Gross Asking Rents for Houston Metro Market Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. The positive trend of the MOB average asking rent was reversed in the 1st quarter 2016. HOUSTON MEDICAL OFFICE BUILDING DEMAND/SUPPLY The Evolution of Healthcare Real Estate Demand in the U.S. Demand for off-campus medical office buildings (MOBs) over the next several years, will be fueled by increased focus on outpatient services by hospitals and large physician groups; continued movement of outpatient services to superior off-campus locations with high identity and superior accessibility; and an increasing diversity in the mix of practice types at off- campus locations, including those traditionally found at hospital locations. Specific healthcare industry trends shaping the healthcare real estate landscape include: (1) the continuing trend of healthcare network acquisition of physician practices; (2) expansion of hospital based labs that leverage the steadily growing laboratory market and high reimbursement rates; (3) the emergence of freestanding emergency care facilities and evolution of urgent care facilities; and (4) a wide range of industry initiatives intended to increase access to healthcare, deliver care in a cost-effective venue, eliminate “care delivery silos” and improve patient outcomes. Metro Houston’s Class A/B Medical Office Buildings At the end of the 1st quarter 2016, the metro Houston Class A/B MOB inventory encompassed 27.5 million square feet in 751 buildings according to the CoStar property database. Between year-end 2010 and year-end 2015, approximately 3.8 million square feet of MOB space was delivered to the Houston metro market. Over this five year period, approximately 14% of additional square feet had been added to market’s MOB inventory. MOB space under construction had fallen to less the 0.5 million square feet by the end of 2015, well below the 3.1 million square feet that was under construction in mid-2007. Net absorption over the last five years (2010-2015) totaled almost 3.9 million square feet, resulting in a vacancy rate that was 60 basis points lower at the end of 2015 compared to year-end 2010. Looking as far back as 2006, though there were periods when supply exceeded demand, the imbalance was not prolonged. This is especially significant when one considers that this metro market has seen an approximately 50% increase in supply between early 2006 and early 2016. This rapid pace of deliveries placed upward pressure on the vacancy rate and downward pressure on rental rate growth. Notwithstanding, metro Houston net absorption remained strong and exceeded new supply for five of the last nine years. The vacancy rate spiked in 2008 and 2012, but has remained under 15% since 2008. Prior to the 1st quarter 2016, the average Class A/B MOB rent continued to increase during the post-recession period (i.e., since at least 2010). At the end of the 1st quarter 2016, the Houston Class A/B medical office inventory exhibited a vacancy rate of 13.2% and an average rent of $25.15 per square foot, gross. Additional statistics are presented at the top left of the following page. 0.0% 1.0% 2.0% 3.0% 4.0% 5.0% 6.0% 7.0% 8.0% 9.0% 10.0% 11.0% 12.0% 13.0% 14.0% 15.0% 16.0% 0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 1,400,000 1,600,000 1,800,000 2,000,000 2,200,000 2,400,000 2,600,000 2,800,000 3,000,000 3,200,000 % Under Construction / Inventory Square Feet Under Construction Square Feet Under Construction % Under Construction / Inventory 14.1% 15.5% 13.9% 13.2% 13.8% 14.6% 12.3% 12.0% 12.5% 13.2% 7.3% 3.0% 0.5% ‐0.9% 2.7% ‐0.1% 0.6% 4.0% 1.7% ‐3.5% ‐500,000 ‐250,000 0 250,000 500,000 750,000 1,000,000 1,250,000 1,500,000 1,750,000 2,000,000 ‐5.0% ‐2.5% 0.0% 2.5% 5.0% 7.5% 10.0% 12.5% 15.0% 17.5% 20.0% 2007 2008 2009 2010 2011 2012 2013 2014 2015 YTD 2016 Q1 Square Feet (Deliveries and Absorption) Percent (Vacancy Rate and % Change in Asking Rent Deliveries Absorption Vacancy Rate % Change in Asking Rent $22.65 $23.33 $23.45 $23.24 $23.87 $23.84 $23.99 $24.95 $25.37 $25.15 $17.00 $18.00 $19.00 $20.00 $21.00 $22.00 $23.00 $24.00 $25.00 $26.00 $27.00 $28.00 $29.00 $30.00 100.00 101.00 102.00 103.00 104.00 105.00 106.00 107.00 108.00 109.00 110.00 111.00 112.00 113.00 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 Q1 Gross Asking Rent, Per Square Foot Rent Growth Index (2007 = 100.0) Asking Rent Gross Rent Growth Index

- 4. Real Estate Counselors International, Inc. 4 April 2016Houston, TX Metro Area A market report for healthcare real estate executives Metro Houston MOB Demand/Supply Indicators: Q1 2015 and Q1 2016 Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. MOB Sales Capitalization Rates and Average Annual Prices Per Square Foot Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. Note: These data include some properties located in a few other Texas MSAs, but the tabulation results would not be materially different had they been removed from these data. Investor Profile of MOB Investment Sales: Transacted Since January 2011 Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. METRO HOUSTON MOB INVESTMENT SALES TRENDS Since 2007, approximately 35% of all MOB investment sales activity was concentrated in or near three Houston office submarkets – S. Main/Medical Center, totaling $230 million (e.g., Healthcare Trust of America, Inc. - $56 million and Welltower - $79 million), Southwest/Hillcroft, totaling $225 million (i.e., HCP REIT 11 building portfolio), and East Fort Bend County/Sugar Land, totaling $205 million (e.g., St. Luke - $153 million). Since 2006, Houston MOB investment sales have exhibited capitalization rates that peaked around 8.5% in 2009 and reached a low of 6.8% in 2013. Since the recent nadir in 2013, capitalization rates increased by 75 basis points to 7.2%, as of year-end 2015. The average sales price per square foot, reflecting sales since 2014, is approximately 18% below the average sale price reported between 2010 and 2012. This variance more than likely reflects the age and class characteristics of the portfolios purchased over these time frames. The average gross asking rent for the investment sales transacted since year-end 2014 was approximately $21 per square foot compared to the total Class A/B market inventory average of approximately $25 per square foot, gross. The current vacancy rate for these sales has averaged approximately 11%, about 200 basis points lower than the total Class A/B market inventory average of approximately 13%. There are 14 top buyers who each amassed over $20.0 million worth of MOBs since 2011. On average, these buyers paid $240 per square foot which is well above the market average per square foot sale price of the last five years. These portfolio sales ranged in price from $115 per square foot (Dunhill Partners, Inc.) to $449 per square foot (St. Luke’s). These data represent buyers at the time of the transaction, thus the buyers listed below may not represent current ownership. For example, American Realty Capital Healthcare Trust, Inc. was sold to Ventas REIT in January, 2015. Largest Medical Office Building Portfolio Investment Sales Since January 2011 Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. Note: These data include some properties located in a few other Texas MSAs, but the tabulation results would not be not materially different had they been removed from these data. Demand/Supply Variables Class A/B Medical Office Buildings Number of Properties, 2016 Q1 751 Total Net Rentable Square Feet, 2016 Q1 27,508,920 Vacancy Rate, 2016 Q1 13.20% Vacancy Rate, 2015 Q1 12.80% Basis Point Change in Vacancy, 2015 Q1 to 2016 Q1 40 Gross Asking Rent, 2016 Q1 $25.15 Gross Asking Rent, 2015 Q1 $25.33 % Change in Asking Rent, 2015 Q1 to 2016 Q1 ‐0.7% Space Absorbed, 2015 Q1 to 2016 Q1 1,074,510 Space Delivered, 2015 Q1 to 2016 Q1 1,338,695 Space Under Construction, 2015 Q1 1,329,740 Space Under Construction, 2016 Q1 271,275 $165 $157 $148 $99 $228 $207 $230 $71 $181 $214 $25 $50 $75 $100 $125 $150 $175 $200 $225 $250 $275 $300 $325 5.0% 5.5% 6.0% 6.5% 7.0% 7.5% 8.0% 8.5% 9.0% 9.5% 10.0% 10.5% 11.0% 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 Sales Price Per Square Foot Capitalization Rate Average Price Per Bldg SF Average Cap Rate 48% 7% 28% 17% REIT/Public Institutionals Private User # Buyer Acquistion Total Square Feet Price PSF 1 HCP, Inc. $225,000,000 1,281,014 $176 2 St. Luke's Episcopal Health System Corporation $153,000,000 341,000 $449 3 Welltower Inc. $93,000,000 380,513 $244 4 CNL Healthcare Properties, Inc. $76,000,000 226,714 $335 5 Healthcare Trust of America, Inc $55,895,485 279,081 $200 6 Physicians Realty Trust $46,700,000 157,605 $296 7 Dunhill Partners, Inc. $45,000,000 390,521 $115 8 First Washington Realty, Inc. $43,150,000 125,186 $345 9 Duke Realty Corporation $38,750,000 168,850 $229 10 Griffin Capital Corporation $31,824,956 118,000 $270 11 Webster Surgical Specialty Hospital, Ltd $30,000,000 91,082 $329 12 Ventas, Inc. $26,279,000 95,230 $276 13 American Realty Capital Healthcare Trust, Inc. $23,276,000 52,345 $445 14 Sentinel Real Estate Corporation $21,400,000 80,740 $265

- 5. Real Estate Counselors International, Inc. 5 April 2016Houston, TX Metro Area A market report for healthcare real estate executives Since January 2011, Houston MOB investment sale transactions totaled $1.1 billion. Metro Houston MOB sales volume totaled $59.4 million during the 1st quarter 2016 and $340.5 million throughout all of 2015. Some of the largest sales in the S. Main/Texas Medical Center submarket since 2011 include the Plaza Medical Center, Medical Center Crossing, Holcombe Professional Center and 7900 Fannin Street. METRO HOUSTON MOB SALES SINCE 2011 Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. S. MAIN/TEXAS MED CENTER SALES SINCE 2011 Sources: CoStar Group, Inc. and Real Estate Counselors International, Inc. Note: All information is from sources deemed reliable; however, no representation is made as to the accuracy thereof. Real Estate Counselors International, Inc. We have long-term relationships with healthcare providers, major corporations, financial institutions, developers, investors, government agencies, and other public and private concerns. Among our specialties are: Stark law Compliance Fair Market Value Rent Studies Property Appraisals Acquisition Due Diligence Disposition Pricing Forensic Due Diligence/Evaluations Portfolio Valuations Litigation Support/Dispute Resolution Market Feasibility Analysis Since 2007, Real Estate Counselors International Inc. has performed a spring and fall survey of medical office buildings in the metro Chicago market. Our proprietary database contains hundreds of contract and asking lease terms collected over the last several years. In 2010, at the request of a national healthcare network, we expanded our survey to the Boston, MA region. There, we also perform an annual MOB rental survey each spring. RECI is an independently owned, commercial real estate valuation and consulting company headquartered in Chicago, Illinois. With roots to 1935, we have earned the reputation as a full-service firm known for our ability to perform high level, complex projects.