Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Interest Rate Risk

Ähnlich wie Interest Rate Risk (20)

Mehr von nikatmalik

Mehr von nikatmalik (17)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Interest Rate Risk

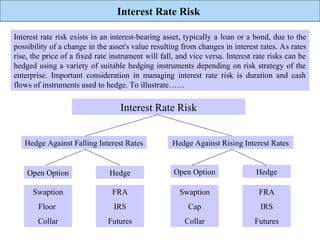

- 1. Interest Rate Risk Interest rate risk exists in an interest-bearing asset, typically a loan or a bond, due to the possibility of a change in the asset's value resulting from changes in interest rates. As rates rise, the price of a fixed rate instrument will fall, and vice versa. Interest rate risks can be hedged using a variety of suitable hedging instruments depending on risk strategy of the enterprise. Important consideration in managing interest rate risk is duration and cash flows of instruments used to hedge. To illustrate…… Interest Rate Risk Hedge Against Falling Interest Rates Hedge Against Rising Interest Rates Open Option Hedge Open Option Hedge Swaption FRA Swaption FRA Floor IRS Cap IRS Collar Futures Collar Futures

- 2. Interest Rate Risk Swaption Objective - To hedge long-term interest rate risks. Brief - A swaption is a call option on an interest rate swap (IRS). At the option maturity date, an option exists to enter into an IRS at predefined conditions. If the IRS market rate is lower than stated in the predefined conditions when the swaption expires, allow the swaption to expire and buy the IRS with the lower rate. Profit Potential - The IRS can be exercised at favorable market conditions at maturity than at the time of purchase. Risk - Limited to the premium Floor Objective - To hedge investments against falling interest rates. Brief Description - A floor hedges an investment with variable interest rates against falling interest rates. The buyer profits from this as long as interest rates remain high or even rise. If they fall below the agreed lower limit, the seller pays the difference between the agreed exercise price and the market interest rate. Floors are interest rate options which are normally written for several years while the interest rate is fixed several times over the course of the maturity period. At each fixing, the market interest rate is compared with the floor exercise price. If Libor is below the exercise price, the seller pays the floor purchaser the difference. A premium is paid for a floor. Profit Potential – Hedge against falling interest rates whilst you continue to profit from stable or rising interest rates. Risk - Premium cost

- 3. Interest Rate Risk Cap Objective - To hedge variable-rate loans against rising interest rates. Brief - A cap hedges a variable-rate product (eg.mortgage) against rising interest rates. The buyer continues to profit from stable or falling interest rates. If they rise above the agreed upper interest limit the seller pays the difference between the agreed basic rate and the market interest rate. Caps are normally written for several years, with the interest rate fixed several times over the duration. On each fixing date, the market interest rate is compared with the agreed cap rate. If Libor is greater than the cap rate, the seller pays the cap purchaser the difference. Profit Potential - Hedge against rising interest rates whilst you continue to profit from stable or falling interest rates. Risk - Premium cost Financial Futures Objective - To hedge market risks - in this case, interest rate risks. Brief - Financial futures are forward transactions traded on futures exchanges. A large number of interest rate instruments are traded in all major currencies on these exchanges. Since the prices of futures contracts, like bond prices, move in the opposite direction to interest rates, futures contracts must be bought as a hedge against falling interest rates. Profit Potential – A Future can be exercised at varying points depending on type of future at favorable market conditions or terminated at maturity. Risk – Premium cost

- 4. Interest Rate Risk Collar Objective - To hedge investments against falling interest rates. Brief - A collar is a combination of interest rate options. It involves buying an out-of-the-money (below the market interest rate) floor, and simultaneously selling a cap that is also out-of-the-money (above the market interest rate). The premium costs for the floor can be partially or completely financed using the premium income from the sale of the cap. This strategy hedges the interest income within a specific band (between the two exercise prices). Collars are normally written for several years, with the interest rate being fixed several times during the course of the maturity period. At each fixing, the market interest rate is compared with the exercise price and any difference in interest rates is paid. Objective - To hedge investments against rising interest rates. Brief - A collar is a combination of interest rate options. It involves buying an out-of-the-money (above the market interest rate) cap, and simultaneously selling a floor that is also out-of-the-money (below the market interest rate). The premium costs for the cap can be partially or completely financed using the premium income from the sale of the floor. This strategy keeps the interest costs within a defined band (between the two exercise prices). Profit Potential - None; a low-cost form of hedge Risk - None; a low-cost form of hedge

- 5. Interest Rate Risk Forward Rate Agreement Brief - With a Forward Rate Agreement (FRA), it is possible to hedge the current interest rate for a certain period of time in the future. The FRA is activated separately from the underlying transaction. It can be effected or terminated at any time. All major currencies can be traded. Hedging against Falling Interest Rates - With the sale of an FRA, the current interest rate level can be hedged for a future investment. If interest rates fall by the time the investment is made, the FRA will return a profit. The capital itself must be invested at the lower levels, but the profit on the FRA raises the interest income to the current level. If interest rates rise, a loss is made with the FRA. However, the capital can be invested at better terms. On the other hand, the loss reduces the interest income to the current level. Hedging against Rising Interest Rates - With the purchase of an FRA, the current interest rate level can be hedged for a future investment. If interest rates rise by the time the loan is taken out, a profit is made on the FRA. The capital itself must be borrowed at the higher levels, although the profit on the FRA lowers the interest costs to the current level. If interest rates fall, a loss is made on the FRA. However, the capital can be borrowed at better terms. On the other hand, the loss lifts the interest costs to the current level. Conditions - An OTC framework agreement and a credit limit are required. The actual credit exposure is usually < 5% of the capital as this is not exchanged and risk is limited to possible interest rate movements over the maturity period.

- 6. Interest Rate Risk Interest Rate Swap Objective - To hedge long-term interest rate risks. Brief - The interest rate swap is a derivative interest instrument in which both parties agree to make interest payments at fixed dates in the future. Normally, one party pays the other a fixed interest rate, while the other party makes interest payments in line with the future interest rate trend. The interest rate swap is mainly used for the management of large credit or asset portfolios, otherwise known as Asset and Liability Management (ALM). Loans, bonds, or bond portfolios cannot always simply be switched if interest rate changes are expected. With the interest rate swap the interest rate linking can be changed whilst keeping the basic position. Example: a borrower who has taken out a long-term loan with a maturity of three years anticipates falling interest rates. The conclusion of a receiver swap (fixed recipient) enables him to hedge the interest rate risk without having to change the loan terms. He pays the bank a fixed rate of interest for the loan and gets this fixed interest rate back from the bank in the IRS. The bank, in return, charges him the variable interest. The fixed interest rate payments thus offset each other and the borrower pays a lower rate of interest at every fixing (if interest rates are actually falling). However, if his expectations are not borne out he pays more interest. Profit Potential - As a hedging instrument: none Risk - Limited to the interest rate difference, as capital is not exchanged. Prerequisite - An OTC framework agreement and a credit limit. Depending on the term, the credit limit is only debited by usually < 5% of the capital as this is not exchanged. Risk is limited to possible interest rate movements over the term of the swap.