RSA Conference Exhibitor List 2024 - Exhibitors Data

Retirement - How To Tax Diversify Your Retirement Income

1. How to:

Tax Diversify Your Retirement Income

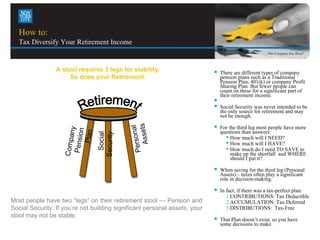

A stool requires 3 legs for stability. There are different types of company

So does your Retirement. pension plans such as a Traditional

Pension Plan, 401(k) or company Profit

Sharing Plan. But fewer people can

count on these for a significant part of

their retirement income.

Social Security was never intended to be

the only source for retirement and may

not be enough.

Assets

For the third leg most people have more

al

ny

n

questions than answers:

Plan

Person

Social

Security

Pensio

• How much will I NEED?

Compa

• How much will I HAVE?

• How much do I need TO SAVE to

make up the shortfall and WHERE

should I put it?

When saving for the third leg (Personal

Assets) – taxes often play a significant

role in decision-making.

In fact, if there was a tax-perfect plan:

1.CONTRIBUTIONS: Tax Deductible

Most people have two “legs” on their retirement stool — Pension and 2.ACCUMULATION: Tax Deferred

Social Security. If you’re not building significant personal assets, your 3.DISTRIBUTIONS: Tax-Free

stool may not be stable.

That Plan doesn’t exist, so you have

some decisions to make.

2. It’s all about Taxes… CONSIDER PERMANENT LIFE INSURANCE:

You can implement plans that combine Generally, an income tax free death benefit

1 & 2 (Qualified Plans) or 2 & 3 (Roth IRA) • Which can replace income lost in retirement when

one spouse dies (such as pension income or Social

Security).

• Which can complete your family’s retirement plan if

you’re not there to complete it for them.

BEFORE tax AFTER tax

contribution contribution Self-completing upon total disability through the purchase

of the optional waiver of premium rider.

Flexible enough to meet individual needs.

Life insurance can be pledged as collateral for a loan.

Protection from creditors (in some states)

ADDITIONAL BENEFITS:

Premiums are paid with AFTER tax dollars

Cash value accumulation is TAX DEFERRED

DISTRIBUTIONS can be structured to be tax-free

• First, policy values are withdrawn* up to the policy

owner's cost basis, which is not a taxable distribution.

Distributions Distributions (providing the policy is not a Modified Endowment

TAXABLE TAX FREE Contract (MEC))***.

• Then loans* can be made against the cash value of the

policy. Loan interest will be at current rates and can

Where do you think tax rates are going? simply be added to the outstanding loan. Neither the

Would it make sense to “tax diversify” your retirement savings? loan nor the loan interest needs to be repaid.**

AS A PART OF YOUR “PERSONAL ASSET LEG” ON YOUR RETIREMENT PLANNING “STOOL” Protect your family’s retirement income! Consider

adding permanent life insurance to help supplement your retirement income – potentially income-tax free

*Loans and withdrawals will reduce the policy’s cash value and death benefit. Policy loans accrue interest at the current rate.

** The Internal Revenue Code requires that taxes be paid on all gains when a policy is surrendered or lapsed for non-payment of premiums. Policy loans, which exceed cost basis, are treated as gains, if the policy goes out of

force prior to death. Therefore, policies should be kept in force until death.

***When too much money is put into a life insurance policy the IRS characterizes the policy as a Modified Endowment Contract (MEC) and withdrawals and loans from the policy are taxed less favorably. MEC policies are not

usually considered suitable for providing supplemental retirement income. 00334360CV