BlackRock’s 2014 Outlook—The List: What to Know, What to Do

•

2 gefällt mir•1,444 views

As 2013 draws to a close, you may be wondering what to expect in the year ahead, and how to prepare your portfolio accordingly. A new piece, BlackRock’s 2014 Outlook—The List: What to Know, What to Do is here to help you.

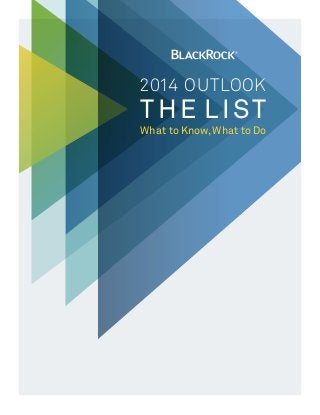

![2014: (Mostly) Moving in

the Right Direction

A Strong 2013…And

Potential Upside for 2014

2013

Asset Class

Returns

U.S. Stocks

+29.1%

International

Stocks

2014

+21.0%

Emerging

Markets Stocks

-1.2%

10-Year U.S.

Treasury Yield

Outlook

2.75%

Source: Bloomberg. As of November 30, 2013.

U.S. Stocks are represented by the S&P 500

Index, International Stocks by the MSCI EAFE

Index, and Emerging Markets Stocks by the MSCI

Emerging Markets Index. Past performance does

not guarantee future results. You cannot invest

directly in an index.

In 2014, we see a world of opportunities—even if they often appear

elusive. While uncertainty is high, your goals haven’t changed. You

still need to save for retirement or find a way to get the income you

need from your investments. We understand that investors feel

overwhelmed by the challenges and don’t know what steps to take.

That’s why we collected our 10 best ideas for the year ahead, which

we call The List. We offer five “what to know” items and five “what

to do” ideas, each with a specific takeaway—designed to help you

navigate the markets in 2014.

So what to expect in 2014? Many of the conditions of the last few years—

slow growth, low interest rates, and very low inflation—are likely to persist.

Not an ideal environment, but one that should support further gains in

stocks, and perhaps hints at a virtuous cycle of global growth that could

be possible if the stars align.

However, there are risks to consider. We expect interest rates to climb, which

could expose traditional bonds to potential losses. Given the strong run-up

in stocks over the past few years, now is a good time to consider diversifying

outside the U.S. Moreover, political dysfunction in Washington (and geopolitical

events) presents a risk of increased volatility.

Where does this leave investors? Although many continue to sit on the sidelines,

we believe the risks of not investing—missing out on market gains, having

your cash holdings erode due to inflation—outweigh the risks of being in the

market. There is no free lunch, and there are risks to be aware of (and to

manage), but meeting your financial goals means taking steps today.

And The List is our guide to helping you do exactly that.

Investment Actions for 2014

Rethink Your

Bonds

[2]

2 0 1 4 O u tlook : T he L ist

Generate Income,

But Don’t Overreach

Seek Growth,

Manage Volatility](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Mehr von João Pinto

Mehr von João Pinto (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

BlackRock’s 2014 Outlook—The List: What to Know, What to Do

- 1. 2014 OUtlook THE LIST What to Know, What to Do

- 2. 2014: (Mostly) Moving in the Right Direction A Strong 2013…And Potential Upside for 2014 2013 Asset Class Returns U.S. Stocks +29.1% International Stocks 2014 +21.0% Emerging Markets Stocks -1.2% 10-Year U.S. Treasury Yield Outlook 2.75% Source: Bloomberg. As of November 30, 2013. U.S. Stocks are represented by the S&P 500 Index, International Stocks by the MSCI EAFE Index, and Emerging Markets Stocks by the MSCI Emerging Markets Index. Past performance does not guarantee future results. You cannot invest directly in an index. In 2014, we see a world of opportunities—even if they often appear elusive. While uncertainty is high, your goals haven’t changed. You still need to save for retirement or find a way to get the income you need from your investments. We understand that investors feel overwhelmed by the challenges and don’t know what steps to take. That’s why we collected our 10 best ideas for the year ahead, which we call The List. We offer five “what to know” items and five “what to do” ideas, each with a specific takeaway—designed to help you navigate the markets in 2014. So what to expect in 2014? Many of the conditions of the last few years— slow growth, low interest rates, and very low inflation—are likely to persist. Not an ideal environment, but one that should support further gains in stocks, and perhaps hints at a virtuous cycle of global growth that could be possible if the stars align. However, there are risks to consider. We expect interest rates to climb, which could expose traditional bonds to potential losses. Given the strong run-up in stocks over the past few years, now is a good time to consider diversifying outside the U.S. Moreover, political dysfunction in Washington (and geopolitical events) presents a risk of increased volatility. Where does this leave investors? Although many continue to sit on the sidelines, we believe the risks of not investing—missing out on market gains, having your cash holdings erode due to inflation—outweigh the risks of being in the market. There is no free lunch, and there are risks to be aware of (and to manage), but meeting your financial goals means taking steps today. And The List is our guide to helping you do exactly that. Investment Actions for 2014 Rethink Your Bonds [2] 2 0 1 4 O u tlook : T he L ist Generate Income, But Don’t Overreach Seek Growth, Manage Volatility

- 3. the BL ACKROCK list What to Know—and Do—in the Year Ahead The Economy: Growing, Albeit Slowly Inflation: The Risk Is to the Downside Employment: Jobs Are Growing, But Wages Are Not What to Know Interest Rates: Higher, But Not Through the Roof More Policy Uncertainty Means More Volatility Stick With Stocks…For Now Seek Greater Growth Opportunities Abroad What to DO Bond Buyers Beware: Once Thought Safe, Now Risky? Consider Munis for Tax-Exempt Income Go Beyond Traditional Stocks and Bonds W hat to k n ow , what to do [3]

- 4. 1 The Economy: Growing, Albeit Slowly The U.S. economy We expect U.S. economic growth to improve in 2014. should edge past the With the Federal Reserve’s easy-money policies as a tailwind, stronger household balance sheets, a healing housing market and lower energy prices should bolster corporate and consumer confidence and support a pickup in growth. 2% growth rate of recent years, with global growth also improving— good news for stocks. Risks remain, however. First, the level of dysfunction coming out of Washington, D.C. presents a significant risk to both the economy and markets. Given the ongoing weakness in the labor market, including subdued wage growth, we are cautious about how strong the economy could be. All told, we believe the U.S. economy will edge past the 2% growth rate that has defined the post-recession environment and come in at around 2.5%. Global growth should accelerate from 3% in 2013 to around 3.5% next year. This should be a positive for stocks, and is also a range that provides the Federal Reserve with some flexibility in managing policy. What to Know SL [4] OW Grow th 2 0 1 4 O u tlook : T he L ist Ke y Take away Fed policy, healing housing markets and lower energy prices should all support modest economic growth and equity markets.

- 5. 2 Interest Rates: Higher, But Not Through the Roof Modestly stronger growth should lead to slightly higher interest rates—but we do not expect a sharp or rapid acceleration. As the Federal Reserve begins to slow its extraordinary bond-buying program, we believe the 10-year Treasury yield will modestly climb around 0.5% by the end of 2014. Even a small increase in interest rates can erode the value of your bonds and hit your net worth, as well as increase your cost of borrowing for everything from homes to cars. Question for your portfolio: Are you prepared for a higher-interest-rate environment? To avoid these sorts of negative economic consequences, the Fed will likely promise to keep short-term interest rates low for some time. Ke y Take away What to Know We don’t expect a sharp rise in rates, but even a small increase would weigh on your SI N G te RI rethink your bonds. s bonds and possibly your net worth. Time to In t erest R a W hat to k n ow , what to do [5]

- 6. 3 Inflation: The Risk Is to the Downside Question for Inflation remains close to historic lows, not just in the United your portfolio: How should you invest in a slow-growth, low-inflation world? States but also in other large developed markets. We don’t see that changing in 2014. If anything, the risk in some developed regions is actually deflation. It is a question we often hear from investors: Why is inflation so low? Essentially, there are three reasons: wages are not growing very strongly, factories still have excess capacity (which means they don’t charge higher prices for their goods) and lending activity remains depressed. Some developed regions, notably Europe and Japan, will continue to flirt with outright deflation. None of this suggests that inflation won’t eventually increase. But for now, conditions indicate inflation is likely to remain low, at least for the next year or so. What to Know Ke y Take away Be cautious of asset classes like TIPS, commodities and gold that are often used e [6] r- I O N a N to protect against inflation. Fl a t INFL AT 2 0 1 4 O u tlook : T he L ist

- 7. 4 Employment: Jobs Are Growing, But Wages Are Not We should see more people getting jobs in 2014 Weak wage growth and the unemployment rate should continue to go down. is bad news for the However, that good news is tempered by the strong possibility that U.S. wage growth is likely to remain subdued. While improving economic growth may provide some upward pressure on wages, factors such as demographics, technology and global labor competition are long-term trends that are working to keep income levels low. stocks of companies Why does this matter? If income growth remains weak, household spending is also likely to remain soft. And that means consumer spending is not the driving force for the economy like it once was. Unless we see a drop in savings or a pickup in borrowing, this factor could mean we see slower overall growth for a longer period, and potentially, lower stock market returns for certain companies most dependent on consumer spending. Ke y Take away that rely on discretionary spending by consumers —better value can be found elsewhere. What to Know Slow income growth and sluggish consumer spending could make consumer for some time. E SS E growth in low gear PR may keep economic S discretionary companies less attractive. It also URe ON WA G W hat to k n ow , what to do [7]

- 8. 5 More Policy Uncertainty Means More Volatility Should Washington’s political drama continue, it likely means higher volatility—a reason to look outside the U.S. for investment opportunities. Centered in Washington, political partisanship and dysfunction continue to represent a risk for the economy and the markets. We may see ongoing political wrangling around budget and debt issues, and topics such as implementing the Affordable Care Act are likely to promote additional uncertainty. 2014 also brings with it the midterm elections—an environment that is certain to promote bitter partisanship. Meanwhile, a trend of growing populism—not just in the U.S. but globally— which can lead to economically unsound policy decisions, represents an additional risk. As always, geopolitical risks lurk as well—we would cite escalating tensions in Asia and the Middle East. All of this creates the potential for increased market volatility. What to Know Ke y Take away Expect volatility to increase if— or when—political dysfunction again emerges. [8] t Po li y This is also one reason why it makes sense cy Uncer i ta n 2 0 1 4 O u tlook : T he L ist to be diversified outside the U.S. and consider minimum volatility strategies.

- 9. 6 Stick With Stocks...For Now U.S. stocks had an extraordinary year in 2013, particularly after Equities are no longer accounting for the fact that economic growth has disappointed. Given the magnitude of the gains, investors are increasingly concerned that global stocks are once again getting overvalued, if not in an outright bubble. a bargain, but we Our take: stocks are no longer cheap, but are not in a bubble. There are some areas of the market that we believe are unjustifiably expensive (U.S. small caps are a chief example), but overall we think prices still can go higher. It is important to remember that stocks still represent a better value than cash and bonds. In short, we would remain overweight equities. still overweight stocks believe investors should for the time being. However, there is an important caveat. Further gains in the market will need to come alongside growth in corporate earnings. Given the environment we described—slow economic growth, sluggish wage growth, lackluster consumer spending—that may be hard for companies to achieve. If we do see market gains without a corresponding increase in corporate earnings, we would take that as a warning sign. Ke y Take away What to DO If you’re out of the market, there’s still time to get off the sidelines. YO We would still overweight equities. UR P OR TFO LI O W hat to k n ow , what to do [9]

- 10. 7 Seek Greater Growth Opportunities Abroad Question for The United States is one area of the world that is looking fully valued. However, outside the U.S., stocks appear more reasonably your portfolio: priced. This may be a good time to seek greater growth opportunities abroad. Should you increase For investors still underweight international equities (and that includes most U.S. investors), we’d consider paring back some U.S. holdings in favor of nonU.S. stocks. Europe, in particular, is an area that seems reasonably valued. To be sure, Europe suffers from numerous challenges, including sluggish economic growth, and has a long way to go in implementing the reforms that could spark stronger growth. But stock prices in Europe are much more attractive than those in the U.S. your allocation to non-U.S. stocks? What about to emerging markets? In addition, for those investors with a strong stomach and long time horizon, we would suggest considering emerging markets, which offer a combination of attractive value and compelling growth prospects. What to DO Ke y Take away Pare back some U.S. holdings and e r na t tio n a l s Em r e International dividend-producing stocks are an attractive way to get exposure outside the U.S. and gain some incremental yield. [10] 2 0 1 4 O u tlook : T he L ist k o ts O e P OR TF I OL t UR ped Mar c In YO lo ks v e et De s consider non-U.S. stocks. gi ng M ar k In addition to developed markets, don’t ignore emerging markets.

- 11. 8 Bond Buyers Beware: Once Thought Safe, Now Risky? Put simply, there are few bargains in traditional bonds Question for (meaning investments concentrated in Treasuries). The main reason is the Fed and other central banks have been on a buying spree in recent years, propping up bond prices (and, thus, driving yields lower). Given the Fed’s plan to pull back on its extraordinary bond-buying program, the risks to traditional bonds are elevated. your portfolio: While the Fed appears set to begin pulling back on these programs (i.e., “tapering”), the leaders of the Fed’s policy committee have been working hard to assure investors that interest rates will remain low for longer. For that reason, we expect the central bank to act gingerly to smooth any market reaction. Do you need to rethink the way you’re investing in bonds? In this context of low rates and ample liquidity, investments such as high yield bonds should remain an attractive source for income. Being flexible and diversified globally remains key, as the possibility for more accommodative central bank actions in Europe creates potential opportunities there, and selectivity in emerging markets along with cheaper valuations could make these areas good diversifiers to U.S. fixed income portfolios. Ke y Take away What to DO With rising interest rates, bond portfolio principal is at risk. BONDS B uy ers Bew ar e Seek managers with flexibility and security selection expertise. W hat to k n ow , what to do [11]

- 12. 9 Consider Munis for Tax-Exempt Income Municipal bonds remain an attractive source of income, particularly on an Detroit and Puerto Rico make for rousing headlines, but they do not characterize the broader municipal market. In our view, muni market fundamentals remain sound and municipal bonds look attractive. We believe current market levels for municipal bonds offer an opportunity to reposition portfolios for the future. We find tax-exempt bonds, supported by strong fundamentals, to be reasonably valued relative to taxable alternatives. The onus of higher taxes should also bolster the asset class. Overall, munis remain a high-quality, attractive option for investors focused on tax-advantaged income and capital preservation. after-tax basis. What to DO Ke y Take away Look past the headlines—the finances IG H E R TA XE S AD At H D M U NIS The key for investors is to be selective. Munis are still an attractive asset class—especially at a time when many are paying higher taxes. [12] 2 0 1 4 O u tlook : T he L ist e of municipalities in general are actually getting stronger. tr ac ti v e In c o m

- 13. 10 Go Beyond Traditional Stocks and Bonds Volatility looks to be high and finding growth and income are major challenges. But stocks are no longer cheap, neither bonds nor cash offer compelling value, and all could be vulnerable to increases in interest rates. That’s why we advise incorporating alternative strategies that can help broaden your diversification, protect against rising rates and contribute to growth. (Remember, however, that diversification does not ensure profits or protect against loss.) Question for your portfolio: What non-traditional investment opportunities should you consider? Diversifying with alternatives means adding new asset classes such as physical real estate and infrastructure investments. It also means finding managers that have the flexibility to seek out income and returns across a wide variety of investments. Additionally, you may want to consider new strategies such as long/short approaches that can be employed with both stocks and bonds to mitigate volatility, seek out returns and contribute to diversification. While the risks of long/short strategies include the possibility of losses larger than invested capital, we believe they can offer a powerful differentiated source of return and the potential for more consistent results over time. Ke y Take away What to DO Use non-traditional tools to diversify and smooth the ride. Infrastructure Long/Short Strategies T raditio n a L stocks a nd B o nds Flexible Investments ad if Br o y S EEK A S M O O T HER R ID E en & Div er s Real Estate Consider long/short strategies, infrastructure, real estate, and flexible investments. W hat to k n ow , what to do [13]

- 14. Turning Insight Into Investment Actions With economic and market conditions slowly improving, but uncertainty high and income and returns still tough to come by, we suggest you make adjustments to your portfolio to take advantage of upside opportunities. We would encourage you to work with your financial professional to seek out new ways to grow your portfolio. 1 2 3 Investment actions for 2014 Rethink Your Bonds Generate Income, But Don’t Overreach Seek Growth, Manage Volatility } llocate to adaptable A strategies } Take a flexible approach to income } eek returns beyond S traditional U.S. bonds } Overweight credit for yield } Diversify into unconstrained and alternative strategies } educe your interest R rate sensitivity } dapt to higher taxes A } llocate to higher A growth opportunities } anage volatility with M conservative equities REL ATED RESOURCES Squeezing Out More Juice The latest publication from the BlackRock Investment Institute provides a more in-depth discussion of the global trends that may drive financial markets in the coming year. BlackRock Investment Directions BlackRock’s monthly asset allocation recommendations, with a focus on ways to position your portfolio in the coming year. [14] 2 0 1 4 O u tlook : T he L ist

- 15. About the authors Russ Koesterich, Jeffrey Rosenberg and Peter Hayes are prolific commentators on the markets, can regularly be seen on CNBC, Fox Business News and Bloomberg TV, and are often quoted in the print media, including The Wall Street Journal, USA Today and Barron’s. Russ Koesterich Jeffrey Rosenberg Peter Hayes Global Chief Investment Strategist Chief Investment Strategist for Fixed Income Head of BlackRock’s Municipal Bonds Group W hat to k n ow , what to do [15]

- 16. Why BlackRock As the world’s largest investment manager, we believe it’s our responsibility to help investors of all sizes succeed in the New World of Investing. We were built to provide the global market insight, breadth of capabilities, unbiased investment advice and deep risk management expertise these times require. The Resources You Need for a New World of Investing Investing with BlackRock gives you access to every asset class, geography and investment style, as well as extensive market intelligence and risk analysis, to help build the dynamic, diverse portfolios these times require. The Best Thinking You Need to Uncover Opportunity With deep roots in all corners of the globe, our 100 investment teams in 30 countries share their best thinking to translate local insight into actionable ideas that strive to deliver better, more consistent returns over time. The Risk Management You Need to Invest With Clarity With more than 1,000 risk professionals and premier risk management technology, BlackRock digs deep into the data to understand the risk that has to be managed for the returns our clients need and bring clarity to the most daunting financial situations. BlackRock. Investing for a New World.® The stated investment preferences are the opinions of the authors and do not reflect individual investors’ risk and return goals. Individual investors should consult with their financial professional about how to implement these opinions in a portfolio that is suitable for their goals and risk tolerance. These views do not necessarily reflect the investment decisions made within specific BlackRock portfolios. This material is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of December 9, 2013, and may change as subsequent conditions vary. Individual portfolio managers for BlackRock may have opinions and/or make investment decisions that, in certain respects, may not be consistent with the information contained in this report. The information and opinions contained in this material are derived from proprietary and nonproprietary sources deemed by BlackRock to be reliable, are not necessarily all-inclusive and are not guaranteed as to accuracy. Past performance is no guarantee of future results. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader. Investment involves risks. Stock and bond values fluctuate in price so that the value of an investment can go down depending on market conditions. International investing involves additional risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks are typically heightened for investments in emerging markets. Typically, when interest rates rise, there is a corresponding decline in the market value of bonds. Credit risk refers to the possibility that the issuer of the bond will not be able to make principal and interest payments. There may be less information available on the financial condition of issuers of municipal securities than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. A portion of the income from municipal securities may be taxable. FOR MORE INFORMATION: www.blackrock.com ©2013 BlackRock, Inc. All Rights Reserved. BLACKROCK, BLACKROCK SOLUTIONS, iSHARES, SO WHAT DO I DO WITH MY MONEY and INVESTING FOR A NEW WORLD are registered trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners. Not FDIC Insured • May Lose Value • No Bank Guarantee Lit. No. OUTLOOK-1213 AC6683-1213 / USR-3133