The Athens Hotel Industry after the Athens Olympics

•

1 gefällt mir•157 views

The Athens Hotel Industry after the Athens Olympics. What was the impact of the Athens Olympics on the Athens Hotel Industry?

Empfohlen

Weitere ähnliche Inhalte

Mehr von GBR Consulting

Mehr von GBR Consulting (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

The Athens Hotel Industry after the Athens Olympics

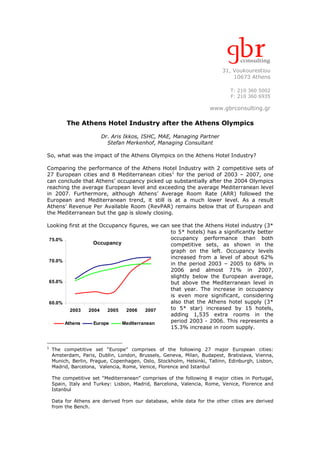

- 1. 31, Voukourestiou 10673 Athens T: 210 360 5002 F: 210 360 6935 www.gbrconsulting.gr The Athens Hotel Industry after the Athens Olympics Dr. Aris Ikkos, ISHC, MAE, Managing Partner Stefan Merkenhof, Managing Consultant So, what was the impact of the Athens Olympics on the Athens Hotel Industry? Comparing the performance of the Athens Hotel Industry with 2 competitive sets of 27 European cities and 8 Mediterranean cities1 for the period of 2003 – 2007, one can conclude that Athens’ occupancy picked up substantially after the 2004 Olympics reaching the average European level and exceeding the average Mediterranean level in 2007. Furthermore, although Athens’ Average Room Rate (ARR) followed the European and Mediterranean trend, it still is at a much lower level. As a result Athens’ Revenue Per Available Room (RevPAR) remains below that of European and the Mediterranean but the gap is slowly closing. Looking first at the Occupancy figures, we can see that the Athens Hotel industry (3* to 5* hotels) has a significantly better 75.0% occupancy performance than both Occupancy competitive sets, as shown in the graph on the left. Occupancy levels increased from a level of about 62% 70.0% in the period 2003 – 2005 to 68% in 2006 and almost 71% in 2007, slightly below the European average, 65.0% but above the Mediterranean level in that year. The increase in occupancy is even more significant, considering 60.0% also that the Athens hotel supply (3* 2003 2004 2005 2006 2007 to 5* star) increased by 15 hotels, adding 1,535 extra rooms in the Athens Europe Mediterranean period 2003 - 2006. This represents a 15.3% increase in room supply. 1 The competitive set “Europe” comprises of the following 27 major European cities: Amsterdam, Paris, Dublin, London, Brussels, Geneva, Milan, Budapest, Bratislava, Vienna, Munich, Berlin, Prague, Copenhagen, Oslo, Stockholm, Helsinki, Tallinn, Edinburgh, Lisbon, Madrid, Barcelona, Valencia, Rome, Venice, Florence and Istanbul The competitive set “Mediterranean” comprises of the following 8 major cities in Portugal, Spain, Italy and Turkey: Lisbon, Madrid, Barcelona, Valencia, Rome, Venice, Florence and Istanbul Data for Athens are derived from our database, while data for the other cities are derived from the Bench.

- 2. The Athens Hotel Industry after the Athens Olympics Seasonality of Athens’ Occupancy Further analysis of occupancy data 90% shows that the increase is mainly 85% in the months of March to 80% 75% September. The creation of a 70% Metropolitan Conference Centre 65% and an active CVB would greatly 60% contribute to reducing seasonality 55% by increasing occupancy in the 50% other months. 45% 40% Nov Feb Aug May Dec Jan Jun Sep Apr Jul Oct Mar 2003 2007 Average Room Rate While the occupancy is 140 (ARR) outperforming in comparison with both competitive sets, the gap in 135 terms of ARR remains stable after 130 2004 as shown in the graph on the 125 left. After the exceptionally high ARR 120 in 2004 due to the Olympic Games, 115 the ARR fell back in 2005 to around Euro 106, slightly under the average 110 rate of 2003. The years 2006 and 105 2007 showed improvement to about 100 Euro 111 and Euro 117 respectively, 2003 2004 2005 2006 2007 but stayed behind that of the European and Mediterranean cities. Athens Europe Mediterranean Revenue per available room (RevPAR) Overall, with the closing gap in 95 occupancy and the difficulty of Athens to 90 keep up with the trend in ARR, the RevPAR of Athens remains below the 85 European and Mediterranean RevPARs 80 with the gap closing very slowly. 75 70 65 60 2003 2004 2005 2006 2007 Athens Europe Mediterranean 2

- 3. The Athens Hotel Industry after the Athens Olympics So what is the verdict? Clearly, the hope after the Olympics was that the performance of the Athens hotels would have been much better than the average of Europe or the Mediterranean. On the other hand, the period prior to the Olympics had been disastrous for Athens hotels and the Olympics clearly marked a reversal of this (see graph below). Long term trends have been even more pronounced as Athens had 8.9 mn overnight stays in 1980 compared to 4.5 mn in 20032! As a result of this, 85 hotels3 of various categories closed down in the 80’s and 90’s. Arrivals - Overnights 2006 - 2000 2,600,000 5,500,000 2,500,000 5,250,000 2,400,000 5,000,000 Overnights Arrivals 2,300,000 4,750,000 2,200,000 4,500,000 2,100,000 2,000,000 4,250,000 1,900,000 4,000,000 2000 2001 2002 2003 2004 2005 2006 Arrivals Overnights In conclusion one could say that the Athens Olympics marked a reversal of fortune for the Athens Hotel Industry but more could have been achieved if Conference Tourism had been developed and if the Tourism Product of Athens was marketed effectively. Particularly as the Olympics helped transform Athens into an attractive city with its must-see unique archeological sites and Europe’s largest archaeological park around the Acropolis, beautiful islands within one hour’s reach, efficient public transport, clean beaches (EU ‘Blue Flag’ carriers), extensive shopping, vibrant night life and much more. Furthermore a UBS study4 has shown that a city break in Athens was among the five cheapest of the 27 cities in the competitive set ‘Europe’ and the cheapest in the competitive set ‘Mediterranean’. 2 Source: National Statistical Service of Greece 3 Source: Athens Hotel Association 4 UBS, Price and Earnings, 2006. 4 cities were not listed in the UBS study, namely Edinburgh, Valencia, Venice and Florence. A partial update of the study in 2008, relating to cost-of-living data, shows that Athens is still cheaper than 18 cities and more expensive than 5 of the cities in the 2 competitive sets. 3