Brief recording

•Als DOCX, PDF herunterladen•

0 gefällt mir•273 views

research article on the unilever foods limited pakistan

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie Brief recording

Ähnlich wie Brief recording (20)

Mehr von Huma Mehir

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Brief recording

- 1. Brief recording Financial analysis of UNILEVER FOODS PAKISTAN LIMITED contributes significantly to the national INTRODUCTION exchequer through tax revenue and is Unilever is one of the largest FMCG committed to developing downstream companies of the world, represented in capability through technology transfer to 150 countries with over 200,000 3P manufacturers, suppliers and employees. In Pakistan, Unilever made its distributors. Globally Unilever is debut in 1948, and today it is one of the increasingly drawing talent from its most prominent multinationals in the operatives in Pakistan, opening new country operating though two affiliated vistas for career development. companies viz. Unilever Pakistan and Unilever Pakistan Foods. The two public FINANCIAL PERFORMANCE FINANCIAL YEAR 2010-2012 listed limited companies have 5 wholly owned and 7 third party manufacturing In a tough operating environment, sales sites across Pakistan and employees growth slowed from 22% in 2011 to 19% around 1,500 people on their payroll and many thousands indirectly. in 2012, the lowest in the last three years, Committed to meet the growing with volume growth contributing to a aspirations of the consumers, Unilever third . Sales of RS.4,940,251 has been in Pakistan Foods Ltd. Has consistently last year and in FY12 Rs.5,861,096 has provided high quality, branded products been earned but the cost on sales is such as Energile, Knorr and Rafhan. greater than previous year but it shows On 24th April, 2007 Rafan Best Foods that cost of sales are also greater than the Limited was renamed Unilever Pakistan Foods. Limited, bringing the same FY11 and FY10. promise of world class products for your During the year the gross profit margin everyday needs. Unilever has a wide has been decreased by 1% by 96 bps. reach and it's distribution network Turnover up by RS. 921 million . Profit reaches remote regions within the from certain operations up by Rs.149 country. With a wide range of offerings, million. including low unit priced packs, Unilever Growth of EPS also declined from 41% in Pakistan addresses all segments of the socio-economic pyramid. 2011 to 16% Rs.116.14 in 2012 with Unilever is a proud part of Pakistan’s gross margin down by 96 bps vs. previous history, contributing to economic growth year. of the nation and catering to the daily needs of 170 million people. It

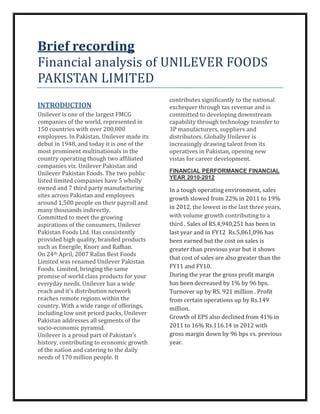

- 2. 1.2 45% 40% 1 35% 30% 0.8 25% 2012 20% 0.6 Current Ratio 15% 2011 10% 0.4 Quick Acid Ratio 5% 2010 0% 0.2 gross net profit gross sales 0 profit margin profit 2012 2011 2010 margin margin Company financial ratio is in FY12 less disposal of fixed assets, but also due to than 1 it is 0.96 mean company is in positive change in mix, higher scale and problem regarding to short term current therefore better cost absorption, Profit obligation. In FY11 market liquidity is after Tax in 2012 rose by 34%. Without about 0.88 and as compared to FY10 is benefit of one-off adjustments, Profit after less in the current years in FY10 current Tax growth would have been 23%. ratio is 1.09 means company was in Despite of all challenges , such as difficult equilibrium position but in FY12 it has economic environment within the difference about 0.13 points. country , severe competition in the Company has lost some sort of control on market and sharp fall in the value rupee current assets in FY11 but it has nearly against the US dollar , the net income ( covered in FY12 but still it is not upto the income after tax has between FY12-FY11 mark as compared to FY10, the lowest in is 15.97% as between FY11 and FY10 it the last three years, with volume growth has 40.97% it means there is a big contributing to a third. Volume growth in the difference in their income ratio. more mature categories – tea, soaps and INTEREST RATE RISK detergents, which together represent two- At December 31, 2012, the Company had thirds of the business, grew at a low 3%. In variable interest bearing financial assets pursuit of reshaping the business, the focus is of Rs. 201.1 million (2011: Rs. 81.6 on growing the emerging categories which million) and liabilities of Rs. 222.7 million presently represent a third of our business. In 2012 these grew by 20% in sales with nearly (2011: Rs. 226.9 million), and had the half through volume. interest rate varied by 200 basis points Partly due to one-off reversals of prior with all the other variables held constant, year restructuring charges and profit on profit before tax for the year would have been approximately Rs. 0.43 million (2011: Rs. 2.91 million) lower / higher, mainly as a result of higher / lower interest expense on floating rate

- 3. borrowings. Credit risk represents the of Rs. 14.67 million (2011: Rs. 34.73 accounting loss that would be recognized million) were past due but not impaired. at the reporting date if counter parties The carrying amount of trade debts failed completely to perform as relates to a number of independent contracted. The maximum exposure to customers for whom there is no recent credit risk is equal to the carrying amount history of default. of financial assets. Out of total financial Company has also increased his trade and assets of Rs. 466.35 million (2011: Rs. payables by RS.182700/-. 344.8 million), the financial assets which Final dividend at the end of the year are subject to credit risk amount to December 31 , 2011 Rs.50 per share but Rs.146.11 million (2011: Rs. 188.56 at the end of the year December 31 ,2012 million).December 31, 2012 trade debts Rs.50 per share it has decreased by RS.14. Unilever food Pakistan limited PROFITABILITY RATIOS UNIT 2012 2011 2010 Gross profit ratio Times 0.38 0.39 0.38 Net profit to sales % 12.20 12.48 11.00 EBITDA margin to sales % 18.99 19.40 17.00 Operating leverage ratio % 0.86 1.72 7.45 Pre Tax return on equity % 179.10 185.00 160.00 Post tax return on equity % 121.02 125.00 108.00 Return on capital employed % 101.77 103.00 88.20 LIQUIDITY RATIO Current Ratio Times 0.96 0.88 1.09 Quick / Acid test ratio Times 0.38 0.36 0.51 Cash to current liabilities Times 0.15 0.08 0.12 Cash flow from operations to sales Times 0.14 0.20 0.09 ACTIVITY Inventory turnover ratio Days 67 58 50 Debtor turnover ratio Days 10 11 8 Creditor turnover ratio Days 113 89 69 Total assets turnover ratio Times 3 3 4 Fixed assets turnover ratio Times 9 8 13 Operating cycle Days 35 (20) (11) Liquidity position has also improved by 0.02 with respect of The liquidity position of the company FY11 but as compare to FY10 it is not so remained evident. in the FY11 it was not much good. satisfied with respect of FY10 it is still not Current asset ratio has been improved by so much good ratio stood on the 0.96 and 3.62% it means that company had current I t is improved by 0.13.its acid test ratio asset than previous year. D/E ratio has been declined by 0.13times.the inventory

- 4. turnover ratio shows that in the FY12 Company has huge inventory. Future outlook The business aims to continue on its journey of profitable growth. This will not be easy due to various external challenges I.e. Law and order conditions, currency depreciation, inflationary pressure, employee attrition, poor GDP growth and Competitive intensity. Our understanding of consumers, access to unilever’s global expertise, R&D capability / innovations and better customer Service will help us to counter the aforementioned challenges. Besides, we will continue to provide our consumers with Better value products driven by strong brand equity. As a means to achieve this, we will also leverage our ability to attract, Develop and retain the best talent in the country.