ICT role in 21st century education and it's challenges.

Average vs-standard-costing1

1. www.Oraclemfgblog.wordpress.com

Inventory Cost Accounting Method selection for a Manufacturing Organization: Average Vs Standard Costing

One decision which is often considered as one of the most important decision to make while implementing an ERP

system is selecting an appropriate Costing method for your organization. Two most commonly used costing methods are

Average and Standard Costing.

The Article presents a quick analysis of important considerations while selecting the costing method for your

manufacturing organization and presents a brief comparison of two Costing Methods. Based on my experience, I have

tried to cover the areas which I think are most important for selecting the right Costing Method.

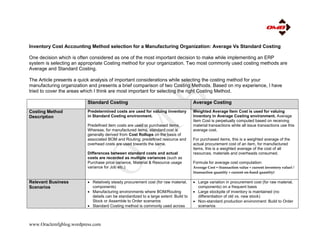

Standard Costing Average Costing

Costing Method

Description

Predetermined costs are used for valuing inventory

in Standard Costing environment.

Predefined item costs are used or purchased items.

Whereas, for manufactured items, standard cost is

generally derived from Cost Rollups on the basis of

associated BOM and Routing; predefined resource and

overhead costs are used towards the same.

Differences between standard costs and actual

costs are recorded as multiple variances (such as

Purchase price variance, Material & Resource usage

variance for Job etc.)

Weighted Average Item Cost is used for valuing

inventory in Average Costing environment. Average

Item Cost is perpetually computed based on receiving

material transactions while all issue transactions use this

average cost.

For purchased items, this is a weighted average of the

actual procurement cost of an item, for manufactured

items, this is a weighted average of the cost of all

resources, materials and overheads consumed.

Formula for average cost computation:

Average Cost = (transaction value + current inventory value) /

(transaction quantity + current on-hand quantity)

Relevant Business

Scenarios

Relatively steady procurement cost (for raw material,

components)

Manufacturing environments where BOM/Routing

details can be standardized to a large extent: Build to

Stock or Assemble to Order scenarios

Standard Costing method is commonly used across

Large variation in procurement cost (for raw material,

components) on a frequent basis

Large stockpile of inventory is maintained (no

differentiation of old vs. new stock)

Non-standard production environment: Build to Order

scenarios

2. www.Oraclemfgblog.wordpress.com

several Manufacturing industries spanning across

Automotive, Electronic goods, FMCG, Food and

Dairy Products, Pharmaceuticals industries

These scenarios are typically present in industries

such as Oil & Petro Chemicals, Agriculture, Heavy

Industry and Industrial Manufacturing involving large

commodities

Cost Control & Variance

Tracking

Standard Costing provides a very good control over

costs as inventory is valued based on predefined item

costs. It also provides robust performance measurement

as multiple variances are recorded based on the

differences between planned and actual costs.

Each of the variances can be monitored and analyzed to

identify the scope for efficiency improvements. Following

types of variances can be tracked:

Purchase Price and Invoice Price Variances

Material usage Variance

Resource, OSP & Overhead efficiency Variance

Standard Cost adjustment Variance

Average Costing perpetually updates the average cost

based on actual transactions and values the inventory

and Jobs based on actual transactions.

As compared to Standard Costing, there is a very limited

control on the Item Cost in Average Costing and very few

variances can be recoded. Invoice Price Variance can be

recorded.

Cost Administration Standard Costing needs active administration and

control. Following activities are typical towards

administering Standard Costing:

Revise Predefined Item Costs for each period

Perform Cost Rollups for make items in each period to

reflect revised cost for "Make" assemblies

Analyze cost variances and root cause analysis for the

recorded variances; take remedial actions to control

the variances in future periods

Perform standard cost adjustments whenever required

Average Costing requires less administration and

minimal intervention is required from business users.

Following activities may be required to administer

average costing:

Review Item Cost History time-to-time

Perform Average Cost adjustments if required

Product Pricing and

Profit Margin Calculation

Both pre-defined costs as well as recorded variances

need to be analyzed for validating Product Pricing and

estimating Product profitability accurately.

Since average costs are computed based on actual

transaction values, no variances are being recorded.

3. www.Oraclemfgblog.wordpress.com

Detailed root-cause analysis must be undertaken to

identify the exact reasons for recorded variances. Some

of them may be attributable to engineering design while

some may be due to operational inefficiencies. Doing

this analysis will help in deciding the Product pricing

realistically for the future.

Up-to-date Average Cost can be reviewed along-with the

cost history to validate Product pricing and estimate the

product profitability.

Benefits Good control over item cost and inventory valuation

Accurate tracking of variances

Good Performance Management tool: Easy to fix

responsibility for each kind of variance

Easy to identify required operational improvements

Automatically value inventory at moving average

item cost

No need to define any pre-defined costs

No need to track variances

Easily determine profit margin based on actual cost

Challenges Higher administration overhead

o Define item costs for each period

o Perform cost rollups for each period

o Variance analysis for each period

Product Profit Margin computation to include direct

costs (planned) as well as variances

Higher standardization required in engineering

phase in order to account for all operational issues.

Very limited control over item costs

No Variances are recorded and all operational

inefficiencies are included as part of actual costing

Difficult to assign responsibility for operational

inefficiencies

PS: I have not covered any system related information or setups in this article (I shall be writing another article to present

a solution to reap benefits of both costing methods in one organization based on Oracle Applications ERP platform).

Hope you will find this analysis interesting; your suggestions and feedback are most welcome!

Regards,

Manu Singhal