Good to have bank info as usual. this is Good to have bank info as usual. It can be Good to have bank info as usual. so have it. Good to have bank info as usual. this is Good to have bank info as usual. It can be Good to have bank info as usual.

1. Facility LGD rating model

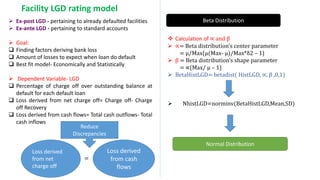

Ex-post LGD - pertaining to already defaulted facilities

Ex-ante LGD - pertaining to standard accounts

Goal:

Finding factors deriving bank loss

Amount of losses to expect when loan do default

Best fit model- Economically and Statistically

Dependent Variable- LGD

Percentage of charge off over outstanding balance at

default for each default loan

Loss derived from net charge off= Charge off- Charge

off Recovery

Loss derived from cash flows= Total cash outflows- Total

cash inflows

Loss derived

from net

charge off

Loss derived

from cash

flows

=

Reduce

Discrepancies

Calculation of ∝ and β

∝= Beta distribution’s center parameter

= μ/Max{μ(Max- μ)/Max*δ2 – 1}

β = Beta distribution’s shape parameter

= ∝{Max/ μ – 1}

BetaHistLGD= betadist( HistLGD, ∝, β ,0,1)

NhistLGD=norminv(BetaHistLGD,Mean,SD)

Beta Distribution

Normal Distribution

2. Independent Variable Description Impact

Dummy

Formation

Collateral Ratio

Collateral Ratio= Collateral Value at default(or 1 year before)/Outstanding Balance at

default LGD( or 1 year before) -ve

Risk Rating Based on Bank’s internal risk rating model +ve

Facility Type/ Other

facility Term Loan , Fixed Loan

Dummy

Variable

Industry Type

Dummy

Variable

Seniority of Loan Senior , Junior -ve

Dummy

Variable

GDP Growth Rate Percentage change from previous year

Revenue -ve

Firm Size -ve

Covenant Structure No covenant, Weak Covenant, Tight Covenant

Dummy

Variable

Current Ratio +ve

Leverage Total Debt/ Capital at default +ve

Default Reason Systematic/ Idiosyncratic

Dummy

Variable

Compromised & Settled -ve

Location Central, North, South Region

Dummy

Variable

Balance Outstanding Balance at default/ one year before default +ve

Independent Variable and its impact on LGD Estimation

3. Validation

R^2

Exploatory Power of the model- F Test, Chi-Square test

Mean Square Error Test

Out of sample and out of time Technique

Satisfy Basel II / III Requirements.

No black-box components

LGD model form:

LGD=∝+β1X1+ β2X2 + β3X3+……..+ βkXk

Model 3 final adjustment:

Discounted LGD=1-(RR × e-r ×T)

T- No. of recovery year

R- risk free rate+ spread

Loss Given Default (LGD) Facility Grade

0% 1

1–15% 2

16–30% 3

31–45% 4

46–60% 5

61–75% 6

76–100% 7

Facility Grading System