1. Page 1 of 6

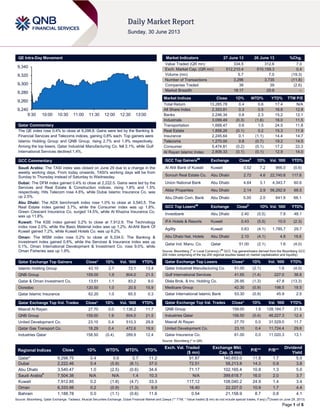

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.4% to close at 9,298.8. Gains were led by the Banking &

Financial Services and Telecoms indices, gaining 0.8% each. Top gainers were

Islamic Holding Group and QNB Group, rising 2.7% and 1.9% respectively.

Among the top losers, Qatar Industrial Manufacturing Co. fell 2.1%, while Gulf

International Services declined 1.4%.

GCC Commentary

Saudi Arabia: The TASI index was closed on June 29 due to a change in the

weekly working days. From today onwards, TASI's working days will be from

Sunday to Thursday instead of Saturday to Wednesday.

Dubai: The DFM index gained 0.4% to close at 2,222.5. Gains were led by the

Services and Real Estate & Construction indices, rising 1.8% and 1.5%

respectively. Hits Telecom rose 4.6%, while Dubai Islamic Insurance Co. was

up 2.5%.

Abu Dhabi: The ADX benchmark index rose 1.0% to close at 3,540.5. The

Real Estate index gained 3.7%, while the Consumer index was up 1.8%.

Green Crescent Insurance Co. surged 14.5%, while Al Khazna Insurance Co.

was up 11.8%.

Kuwait: The KSE index gained 0.2% to close at 7,912.9. The Technology

index rose 2.0%, while the Basic Material index was up 1.2%. Al-Ahli Bank Of

Kuwait gained 7.2%, while Kuwait Hotels Co. was up 6.2%.

Oman: The MSM index rose 0.2% to close at 6,334.0. The Banking &

Investment index gained 0.8%, while the Services & Insurance index was up

0.1%. Oman International Development & Investment Co. rose 9.0%, while

Oman Fisheries was up 1.9%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Islamic Holding Group 43.10 2.7 72.1 13.4

QNB Group 159.00 1.9 804.0 21.5

Qatar & Oman Investment Co. 13.51 1.1 83.2 9.0

Ooredoo 120.50 1.0 20.5 15.9

Qatar Islamic Insurance 62.20 1.0 65.5 0.3

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Masraf Al Rayan 27.70 0.0 1,138.2 11.7

QNB Group 159.00 1.9 804.0 21.5

United Development Co. 23.10 0.4 510.3 29.8

Qatar Gas Transport Co. 18.29 0.4 472.6 19.9

Industries Qatar 158.50 (0.4) 289.9 12.4

Market Indicators 27 June 13 26 June 13 %Chg.

Value Traded (QR mn) 334.5 312.6 7.0

Exch. Market Cap. (QR mn) 512,210.4 510,159.3 0.4

Volume (mn) 5.7 7.0 (19.3)

Number of Transactions 3,296 3,735 (11.8)

Companies Traded 38 39 (2.6)

Market Breadth 18:17 25:8 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 13,285.78 0.4 0.6 17.4 N/A

All Share Index 2,353.81 0.3 0.5 16.8 12.8

Banks 2,246.34 0.8 2.3 15.2 12.1

Industrials 3,099.49 (0.3) (1.6) 18.0 11.5

Transportation 1,668.47 0.6 1.5 24.5 11.8

Real Estate 1,858.26 (0.1) 0.2 15.3 11.9

Insurance 2,245.64 0.1 (1.1) 14.4 14.7

Telecoms 1,270.00 0.8 (0.7) 19.2 14.5

Consumer 5,474.81 (0.2) (0.1) 17.2 22.3

Al Rayan Islamic Index 2,808.33 (0.1) (0.1) 12.9 14.0

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Al Ahli Bank of Kuwait Kuwait 0.52 7.2 966.0 (0.6)

Sorouh Real Estate Co. Abu Dhabi 2.72 4.6 22,740.8 117.6

Union National Bank Abu Dhabi 4.64 3.1 4,343.7 60.6

Aldar Properties Abu Dhabi 2.14 2.9 56,292.9 68.5

Abu Dhabi Com. Bank Abu Dhabi 5.00 2.0 641.9 66.1

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

Investbank Abu Dhabi 2.40 (5.5) 7.8 48.1

IFA Hotels & Resorts Kuwait 0.43 (5.5) 10.0 (2.3)

Agility Kuwait 0.63 (4.1) 1,785.7 29.7

Abu Dhabi Nat. Hotels Abu Dhabi 2.10 (4.1) 4.8 18.6

Qatar Ind. Manu. Co. Qatar 51.00 (2.1) 1.6 (4.0)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Industrial Manufacturing Co. 51.00 (2.1) 1.6 (4.0)

Gulf International Services 41.65 (1.4) 227.0 38.8

Dlala Brok. & Inv. Holding Co. 26.95 (1.3) 47.8 (13.3)

Medicare Group 42.30 (0.9) 198.5 18.5

Qatar International Islamic Bank 53.30 (0.9) 45.9 2.5

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

QNB Group 159.00 1.9 128,184.7 21.5

Industries Qatar 158.50 (0.4) 46,227.3 12.4

Masraf Al Rayan 27.70 0.0 31,529.0 11.7

United Development Co. 23.10 0.4 11,724.4 29.8

Qatar Insurance Co. 61.00 0.0 11,020.3 13.1

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 9,298.75 0.4 0.6 0.7 11.2 91.87 140,653.0 11.8 1.7 5.0

Dubai 2,222.46 0.4 (5.9) (6.1) 37.0 72.51 58,213.8 14.3 0.9 3.8

Abu Dhabi 3,540.47 1.0 (2.5) (0.6) 34.6 71.17 102,165.4 10.8 1.3 5.0

Saudi Arabia#

7,504.38 N/A N/A 1.4 10.3 N/A 399,618.7 16.0 2.0 3.7

Kuwait 7,912.85 0.2 (1.8) (4.7) 33.3 117.12 108,040.2 24.9 1.4 3.4

Oman 6,333.98 0.2 (0.9) (1.3) 9.9 16.40 22,227.0 10.9 1.7 4.4

Bahrain 1,188.78 0.0 (1.1) (0.6) 11.6 0.54 21,158.9 8.7 0.8 4.1

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) (

#

Closed on June 29, 2013)

9,240

9,260

9,280

9,300

9,320

9,340

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.4% to close at 9,298.8. The Banking &

Financial Services and Telecoms indices led the gains. The

index rose on the back of buying support from Qatari

shareholders despite selling pressure from non-Qatari

shareholders.

Islamic Holding Group and QNB Group were the top gainers,

rising 2.7% and 1.9% respectively. Among the top losers, Qatar

Industrial Manufacturing Co. fell 2.1%, while Gulf International

Services declined 1.4%.

Volume of shares traded on Thursday declined by 19.3% to

5.7mn from 7.0mn on Wednesday. Further, as compared to the

30-day moving average of 11.6mn, volume for the day was

51.5% lower. Masraf Al Rayan and QNB Group were the most

active stocks, contributing 20.1% and 14.2% to the total volume

respectively.

Source: Qatar Exchange (* as a % of traded value)

Ratings, Earnings and Global Economic Data

Ratings Updates

Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change

Saudi Basic

Industries

Corporation

(SABIC)

Fitch

Saudi

Arabia

LT IDR/ ST IDR/ Senior

unsecured rating/

Senior unsecured rating

on SABIC Capital's

guaranteed bonds

A+/F1/A+/ A+ A+/F1/A+/ A+ – Stable –

Union National

Bank (UNB)

CI

Abu

Dhabi

FSR/ LT FCR/ ST FCR/

SR

A+/A+/A1/1 A+/A+/A1/1 – Stable –

United Gulf Bank

(UGB)

CI Bahrain

LT FCR/ ST FCR/

Support Level/ FSR

BBB/A3/3/BBB

BBB/A3/3/BB

B

– Stable –

Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, ICR – Issuer Credit Rating, SR – Support Rating)

Earnings Releases

Company Market Currency

Revenue

(mn)

% Change

YoY

Operating Profit

(mn)

% Change

YoY

Net Profit (mn)

% Change

YoY

Al Firdous Holdings (AFD)* Dubai AED 13.2 9.5% – – 0.8 (68.9%)

Source: Company data, DFM (*FY2013 Results)

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

06/27 US Department of Labor Initial Jobless Claims 22-June 346K 345K 355K

06/27 US Department of Labor Continuing Claims 15-June 2,965K 2,953K 2,966K

06/27 US Bloomberg Bloomberg Consumer Comfort 23-June -28.3 – -29.4

06/27 EU Eurostat Euro-Zone Economic Confidence June 91.3 90.4 89.5

06/27 EU Eurostat Business Climate Indicator June -0.68 -0.65 -0.75

06/27 EU Eurostat Euro-Zone Indust. Confidence June -11.2 -12.3 -13

06/27 EU Eurostat Euro-Zone Consumer Confidence June -18.8 -18.8 -21.9

06/27 EU Eurostat Euro-zone Services Confidence June -9.5 -8.5 -9.2

06/27 France INSEE Consumer Confidence Indicator June 78 81 79

06/28 France INSEE Producer Prices (MoM) May -1.20% -0.30% -1.20%

06/28 France INSEE Producer Prices (YoY) May -0.10% 1.00% 0.20%

06/28 France INSEE Consumer Spending (MoM) May 0.50% -0.10% -0.50%

06/28 France INSEE Consumer Spending (YoY) May 0.60% 0.30% 0.10%

06/27 Germany Destasis Import Price Index (MoM) May -0.40% -0.20% -1.40%

06/27 Germany Destasis Import Price Index (YoY) May -2.90% -2.60% -3.20%

06/27 Germany Bundesbank Unemployment Rate June 6.80% 6.90% 6.80%

06/28 Germany Destasis Retail Sales (MoM) May 0.80% 0.40% -0.10%

06/28 Germany Destasis Retail Sales (YoY) May 0.40% 0.20% 2.70%

06/28 Germany Destasis CPI MoM June 0.10% 0.00% 0.40%

06/28 Germany Destasis Consumer Price Index (YoY) June 1.80% 1.70% 1.50%

06/27 UK ONS GDP (QoQ) 1Q2013 0.30% 0.30% -0.20%

06/27 UK ONS GDP YoY 1Q2013 0.30% 0.60% 0.00%

06/27 UK Lloyds Bank Lloyds Business Barometer June 36 – 39

06/27 Japan Markit Markit/JMMA Manufacturing PMI June 52.3 – 51.5

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Overall Activity Buy %* Sell %* Net (QR)

Qatari 58.04% 55.56% 8,255,499.95

Non-Qatari 41.97% 44.43% (8,255,499.95)

3. Page 3 of 6

News

Qatar

Qatar lifts 2013 GDP growth forecast to 5.3% in 2013 –

According to a report released by the General Secretariat for

Development Planning (GSDP), Qatar's real GDP growth in

2013 is forecasted to increase to 5.3% from the earlier 4.8%,

citing changes to its expected output of oil & gas. Further, the

report indicated that 4.5% growth is predicted for 2014. The

report said the country’s pipeline gas production will rise in 2013

and unscheduled shutdowns, which limited the energy output in

2012, are unlikely to be repeated. The report also said that in

2014, upstream oil & gas is expected to reduce as output from

maturing oil fields tapers off and gas production hits installed-

capacity limits. The GSDP said the Qatar government's fiscal

surplus is expected to drop to 4.7% of GDP in 2014 from an

upwardly revised 8.1% in 2013. The GSDP also said that the

overall surplus is expected to narrow down in 2014 in the wake

of the substantial increases in capital spending needed to keep

Qatar's infrastructure projects on track. The inflation is expected

to be at 3.6% in both 2013 and 2014, up from 1.8% in 2012.

Meanwhile, according to a report released by the Ministry of

Development Planning & Statistics (MDPS), Qatar’s GDP at

constant prices (inflation-adjusted GDP) is estimated at

QR88.4bn in 1Q2013, which shows an increase of 6.2% YoY

(+1.6% QoQ). The report showed that the constant price gross

value added (GVA) of the Mining & Quarrying sector in 1Q2013

has been estimated at QR37.6bn, indicating an increase of 0.8%

YoY. The report also showed that the GVA estimate of non-

mining & quarrying sectors, totaled QR50.9bn, showing 10.6%

YoY increase in 1Q2013. (Peninsula Qatar, GulfBase.com)

QNB Group: Gas prices likely to continue outperforming oil

– According to a report released by QNB Group, gas prices are

likely to continue outperforming oil prices over the near future.

The report said oil & gas prices exhibited opposite trends; the

global oil production grew more rapidly than consumption,

whereas the gas demand growth outstripped supply in 2012.

This meant that average gas import prices rose much more

strongly than oil prices. QNB Group said the relative trend is

likely to continue over the near term, even though the global

demand for petroleum products is likely to soften in the months

ahead. QNB Group’s weighed average basket of the three main

benchmark gas import prices (Japan, Europe and the US)

increased by 15.6%, led by the Japanese LNG import price,

which averaged at a record $16.6/mBTU (million British thermal

unit), while European gas imports reached $11.5/mBTU, the

second highest on record after 2008. (Gulf-Times.com)

Ooredoo gets Myanmar mobile contract, still interested in

Maroc Telecom stake – Ooredoo (formerly QTEL) said it has

obtained a telecom license from Myanmar’s government

telecom bid committee to become one of the country’s first

foreign operators. Meanwhile, Ooredoo’s Strategy Officer

Jeremy Sell said that the company may still be interested in

Vivendi’s stake in Maroc Telecom if Emirates

Telecommunications Corporation’s (Etisalat) bid fails.

(GulfBase.com, Bloomberg)

Nakilat to disclose 2Q2013 financials on July 14 – Qatar Gas

and Transport Co. announced its intent to disclose 2Q2013

financial statements on July 14, 2013.

ABQK to disclose 2Q2013 financials on July 14 – Ahli Bank

announced its intent to disclose 2Q2013 financial statements on

July 14, 2013.

MARK to disclose 2Q2013 financials on July 22 – Masraf Al

Rayan announced its intent to disclose 2Q2013 financial

statements on July 22, 2013.

QPI’s UK power plant plan accepted by NIPA – According to

sources, Qatar Petroleum International’s (QPI) plan to build a

500 MW power plant at South Hook LNG import terminal in

Wales has been accepted for examination by the UK National

Infrastructure Planning Authority (NIPA). The approval process

for this project is expected to take 12-15 months. (Bloomberg)

TFI, Investra acquires first two properties of UK-based fund

– Barwa Bank Group’s investment banking division, The First

Investor (TFI) and Investra Investments have jointly acquired

two properties of a UK-based distribution, logistics and light-

industrial income generating fund, which was launched in April

2013. (AME Info)

Qatar’s population reaches 1.96mn in May – According to the

data published in the Qatar Economic Outlook (QEO) 2013-14,

the influx of foreign labor due to the burgeoning infrastructure

activity in the country has pushed the country’s population to

1.96mn as of end of May 2013, an increase of 9.3% YoY. The

report has also forecasted that the upward trend is expected to

continue in 2014, with the population reaching about 2.2mn by

2013. The bulk of the influx is expected to enter the labor force,

with the vast majority entering low-productivity activities such as

construction and engineering. (Qatar Tribune)

Doha Clinic, SCH pact on Health Insurance Law soon – The

Doha Clinic Hospital will soon sign a long-awaited contract with

the Supreme Council of Health (SCH) in order to start serving

the patients covered by the new Health Insurance Law. (Qatar

Tribune)

International

Fitch affirms US AAA rating; outlook Negative – Ratings

agency Fitch has affirmed the US’ credit rating at AAA, but

maintained the outlook at Negative, saying that still-elevated

debt levels leave the country vulnerable to shocks without more

deficit reduction. Fitch said the affirmation reflects strong

economic and credit fundamentals, and the decline in the

federal budget deficit to levels consistent with debt stabilization.

Fitch said it will conduct another review of the credit rating by

the end of 2013, although it is technically supposed to conduct it

in June next year. Fitch also said the Negative outlook reflects

the near-term risk associated with the expiration of federal

appropriations authority at the end of the current fiscal year.

(Reuters)

France to seek €14bn budget cuts in 2013 – France will

reportedly pursue €14bn in spending cuts next year as it

attempts to reduce its budget deficit to 3% of economic output

by 2015. The French government aims to tame the public deficit

by trimming ministerial budgets, cutting state aid to companies

and reducing local government funding. Annual growth in overall

wage costs for French public employees will be cut to 0.15%

from 3%, chiefly through pay restraint. Ministries will also be

expected to trim 2% from operating budgets through public

purchasing reform. (Reuters)

Spain sets limits to regions' deficit and debt until 2016 –

The Spanish government has set limits on budget deficits and

debt issuance by the country's 17 autonomous regions until

2016, in a drive to help meet budget goals agreed with the EU.

After a meeting with regional officials, the Treasury Minister

Cristobal Montoro said the maximum annual budget gap for the

4. Page 4 of 6

regions as a group would be 1.3% of their economic output in

2013. (Reuters)

Bloomberg: OPEC June output falls in June – According to

the data from a Bloomberg survey, crude output from the

Organization of Petroleum Exporting Countries (OPEC) dropped

in June – for the first time in five months in 2013 – led by

declines from African producers such as Libya, Angola and

Nigeria. The survey showed that the OPEC output slipped

227,000 barrels (0.7%) in June, to an average 0.7mn barrels a

day from a revised 30.9mn barrels in May. The survey also

showed that production in May was revised lower by 110,000

barrels a day because of changes to Venezuelan and Kuwaiti

production estimates. (Bloomberg)

Regional

Airbus: Mideast airlines will need aircraft worth $408bn in

two decades – Airbus said in its forecast that Middle Eastern

airlines will need some 1,963 new passenger and cargo aircraft

valued at $408bn over the next 20 years. Airbus also said that

passenger traffic in the Middle East is set to increase by 6.2%

annually over the next 20 years, and airline fleets are expected

to grow nearly three times by 2031 to meet this demand. (Gulf-

Times.com)

UAE’s Central Bank: money supply reaches AED60bn in

May, steady growth in loans & deposits – According to the

data released by the UAE Central Bank, the money supply

aggregate M0 increased by 2% MoM to AED60bn at the end of

May 2013. The data also showed that the money supply

aggregate M1 increased by 1.6% MoM to AED341.4bn, while

M2 increased by 1% to AED917.9bn and M3 increased by 0.1%

to AED1.2tn. The data also showed that total bank deposits in

UAE banks increased by 0.4% during May to close at AED1.2tn

as a result of a rise in resident deposits by 0.5%, while total

bank loans & advances increased by 0.8% to reach AED1.1tn.

Moreover, the data showed that during the first five months of

2013, monetary aggregate M2 increased by 6.4%, while bank

loans & advances rose by 2.9% and total bank deposits climbed

by 6.7% as a result of 8.4% increase in resident deposits.

(GulfBase.com)

UNCTAD: FDI inflow to UAE rises 25% to $9.6bn – According

to a report released by the United Nations Conference on Trade

& Development (UNCTAD), UAE’s foreign direct investment

(FDI) inflow increased by 25% to $9.6bn in 2012, continuing a

recovery initiated in 2010 but remaining well below the $14bn

level reached in 2007. The report showed that despite the strong

decline registered in Saudi Arabia, FDI to the GCC region as a

whole remained at almost the same level in 2012 ($26bn),

because of significant FDI growth in all other countries within the

group. The report said high public spending by Abu Dhabi and a

strong performance by Dubai’s non-hydrocarbon sectors helped

rebuild foreign appetite for FDI in the Emirates. The report also

said that Saudi Arabia and UAE alone accounted for 83% of FDI

inflows into the GCC region. Meanwhile, the report said that FDI

into Kuwait more than doubled, reaching $1.9bn while it also

rose in Bahrain, Oman and Qatar. (GulfBase.com)

DGCX to list Sensex futures from July 5 – The Dubai Gold &

Commodities Exchange (DGCX) is set to launch a futures

contract based on India-based blue-chip stock index, “Sensex”.

The contract will be formally listed on the DGCX on July 5, 2013.

(AME Info)

UAE’s GCAA signs open skies agreement with Niger – The

General Civil Aviation Authority of the UAE (GCAA) has signed

an open skies agreement with the Government of Niger.

(GulfBase.com)

BofAML: Fiscal rein helping Abu Dhabi lower oil breakeven

price – Bank of America Merrill Lynch’s (BofAML) Global

Research division said gradual fiscal consolidation is bringing

the Abu Dhabi government’s fiscal oil breakeven price lower to

$95 per barrel in 2013, after a spike due to exceptional support

to banks and government-related entities in 2012. The UAE’s

breakeven price for oil had risen to $107 per barrel in 2012, the

highest in the GCC, amid higher spending. (GulfBase.com)

DDF re-pricing its $1.8bn loan – Dubai Duty Free (DDF) is set

to re-price a $1.8bn, 6-year syndicated loan which was signed in

July 2012. The original loan was split between a dirham-

denominated tranche and a dollar-denominated facility, which

were both priced at 325 basis points (bps) over LIBOR. As part

of the re-pricing exercise, margins will be reduced by 100 bps on

the dirham-denominated tranche and by 75 bps on the US dollar

tranche. This re-pricing is expected to close next week.

(GulfBase.com)

Emaar, Meraas launches new hotel brand – Emaar Properties

and Meraas Holding have launched a new hotel brand named

“Dubai Inn”, which is focused on the affordable segment. (AME

Info)

Emirates plans new A380 lease deal, to upgrade Warsaw

service – The Emirates Airline is planning to lease a new Airbus

A380 superjumbo aircraft from a finance company that will issue

$630mn of bond-type certificates to fund the purchase. Emirates

said that it will upgrade and deploy a Boeing 777-300 aircraft for

the flight to Warsaw from January 1, 2014. (GulfBase.com)

MAF to invest AED3bn for further expansion in Dubai –

Majid Al Futtaim (MAF) has planned to invest AED3bn for

enhancing its Dubai businesses over the next five years. These

plans include: developing two new hotels; upgrading two

existing hotels; enhancements to its flagship Mall of the

Emirates and Deira City Centre; opening four Carrefour

supermarkets and two hypermarkets; as well as building a new

14-screen cinema complex. MAF is also evaluating options for

the development of a new 50-store community mall in a prime

residential area of Dubai. (AME Info)

Orion acquires AED22.1mn property from Memon – Orion

Holdings has acquired a property worth AED22.1mn under

development from Memon Investments. Located at the Dubai

Sports City, nearly 41% of the construction of this property has

been completed and it is scheduled for delivery by September

2014. (AME Info)

Al Islami to establish AED100mn processed food facility in

Dubai – Al Islami Foods is set to establish a new food

processing facility in Dubai at an investment of AED100mn, to

meet the increasing regional demands for high-quality halal food

products. (AME Info)

FPIG acquires Spainsh Protecciones Plásticas – Future Pipe

Industries Group (FPIG) has acquired a Spain-based fiberglass

pipe manufacturing business, Protecciones Plásticas, which

conducts business under the trade name, “Protesa”. (AME Info)

ADNOC plans to create new crude blend – The Abu Dhabi

National Oil Company (ADNOC) is planning to blend its Lower

Zakum and Umm Shaif oils into a new export crude called “Das”

from early 2014. (GulfBase.com)

Abu Dhabi media group, Murdoch eye FT Group – Abu

Dhabi’s state media group and media mogul Rupert Murdoch

are in talks to acquire the Financial Times (FT) Group for about

$1.2bn. (Peninsula Qatar)

KIA MD: Kuwait invests $24bn in UK – The Kuwait Investment

Authority’s (KIA) Managing Director Bader Mohammed Al-Saad

5. Page 5 of 6

said the country has more than doubled its investment in Britain

over the past 10 years to more than $24bn. (GulfBase.com)

Agility’s shareholders approve capital increase through

bonus shares – Shareholders of the Agility Public Warehousing

Company have approved to increase the company’s capital from

KD104.7bn to KD109.9bn through the distribution of 5% bonus

shares. (DFM)

OAB goes ahead with planned IPO – The Oman Arab Bank

(OAB) said it expects to complete the procedures and required

approvals for an IPO of its shares by the end of this summer.

(Gulf-Times.com)

Hits Telecom to write off KD28.2mn in losses – Kuwait-based

Hits Telecom Holding Company’s shareholders have approved

writing off its accumulated losses amounting to KD28.2mn. Hits

Telecom said it will use KD27.3mn of its share premium and

about KD925,000 of its reserves to write off the losses. Hits

Telecom’s shareholders have also approved the board’s

proposal not to distribute any dividends for FY2012. (Gulf-

Times.com)

OIFC declares 12% cash dividend, 4.3 shares as stock

dividend – The Oman Investment & Finance Company’s (OIFC)

shareholders has approved the board’s recommendation to

distribute cash dividends wroth 12% of its capital (12 baisa per

share) and a stock dividend of 4.3 shares for every 10 shares

held for FY2013. This will increase OIFC’s share capital from

140mn shares to 200mn shares. (MSM)

OHIC’s AGM approves 15% cash dividend – Oman Holdings

International Company’s (OHIC) AGM has approved the

distribution of a cash dividend of 15% (OMR0.015 per share) for

FY2013. (MSM)

Bankers prepare debt financing for Investcorp’s Skrill sale –

According to sources, bankers are putting together around

£300mn of debt financing to back a potential sale of Investcorp's

UK-based online payments services firm, Skrill. Bahrain-based

Investcorp has hired Barclays to oversee Skrill’s sale, which is

expected to fetch around £600mn, and first-round bids are due

by July 9, 2013. (Reuters)

6. Contacts

Ahmed M. Shehada Keith Whitney Saugata Sarkar Sahbi Kasraoui

Head of Trading Head of Sales Head of Research Manager - HNWI

Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6534 Tel: (+974) 4476 6544

ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa saugata.sarkar@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg (*Closed on June 29)

Source: Bloomberg Source: Bloomberg

80.0

90.0

100.0

110.0

120.0

130.0

140.0

Jan-10 Jul-10 Jan-11 Jul-11 Jan-12 Jul-12 Jan-13

QEIndex S&P Pan Arab S&P GCC

0.0%

0.4%

0.2%

0.0%

0.2%

1.0%

0.4%

0.0%

0.4%

0.8%

1.2%

SaudiArabia*

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,234.57 2.8 (4.8) (26.3) DJ Industrial 14,909.60 (0.8) 0.7 13.8

Silver/Ounce 19.67 6.3 (2.3) (35.2) S&P 500 1,606.28 (0.4) 0.9 12.6

Crude Oil (Brent)/Barrel 102.23 (0.3) 0.8 (9.4) NASDAQ 100 3,403.25 0.0 1.4 12.7

Natural Gas (Henry

Hub)/MMBtu

3.56 (4.6) (8.7) 3.5 STOXX 600 285.02 (0.5) 1.6 1.9

LPG Propane (Arab Gulf)/Ton 801.00 0.0 1.4 (17.3) DAX 7,959.22 (0.4) 2.2 4.6

LPG Butane (Arab Gulf)/Ton 791.00 0.0 1.4 (18.3) FTSE 100 6,215.47 (0.4) 1.6 5.4

Euro 1.30 (0.2) (0.9) (1.4) CAC 40 3,738.91 (0.6) 2.2 2.7

Yen 99.14 0.8 1.3 14.3 Nikkei 13,677.32 3.5 3.4 31.6

GBP 1.52 (0.3) (1.3) (6.4) MSCI EM 940.33 2.3 4.4 (10.9)

CHF 1.06 0.0 (1.1) (3.1) SHANGHAI SE Composite 1,979.21 1.5 (4.5) (12.8)

AUD 0.91 (1.5) (0.9) (12.1) HANG SENG 20,803.29 1.8 2.7 (8.2)

USD Index 83.14 0.3 1.0 4.2 BSE SENSEX 19,395.81 2.8 3.3 (0.2)

RUB 32.84 0.2 0.0 7.6 Bovespa 47,457.13 (0.3) 0.9 (22.1)

BRL 0.45 (1.5) 0.6 (8.1) RTS 1,275.44 1.0 2.4 (16.5)

133.6

117.9

107.2