How to Get Started in Social Media for Art League City

accounts answer.pdf

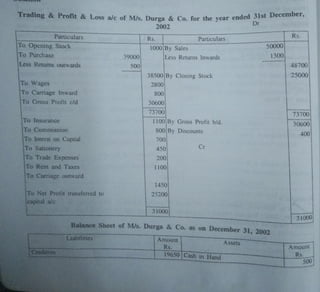

1. rading& Profit & Loss alc of M/s. Durga & Co. for the vear ended 31st December

2002

Dr

Rs

Particulars Rs. Particulars

50000

To Opening Stock 1000By Sales

1300

To Purchase 39000 Less Retuns Inwards

48700

Less Retums outwards 500

25000

38500 By Closing Stock

2800

800

30600

To Wages

To Carriage Inward

To Gross Profit c/d

73700

73700

1100By Gross Profit b/d.

To Insurance

30600

To Commission 800| By Discounts

400

700

To Interst on Capital

To Sationery

To Trade Expenses

Cr

450

200

1

100

To Rent and Taxes

To Carriage outward

1450

25200

To Net Profit transferred to

capital a/c

31000

| 31000

Balance Sheet of M/s. Durga & Co. as on December 31, 2002

Liabilities Amount Assets

Amount

Rs.

Rs.

Creditors 19650 Cash in Hand 500

2. 4750

3000 Cash at Bank

Bills payable

4500

25000

30000

17900 Bill Regivable

Capital

25200 Stock

Add. Net Profit

43100 Sundry Debtors

1000

Office Fixtures

65750

65750

3. 108 Accounting for Managemen

BOORS OF RAJAN JEWELERS

rading and Profit and Loss Account for the year ended 31.12.199

Rs

Particulars Particulars

R

72,000 By Sales

3,50,000

To Opening mventory

80,000

To Purchases

2.25,000 By Closing Inventory

L.ess Retums

1,800

2.23,200

Less Drawings 1,800 2,21,400

To Gross Profit cid 1,36,600

4,30,000

4,30,000

To Salaries 1,36,600

30,000 By Gross Profit b/d

Add Outstanding

33,000 By Commission 7,500

3,000

To Advertisement

22,000

Less Prepard

2.000 20,000

To Reparis and maintenance 13,000

To General Expenses 16,000

To Insurance

7,000

To Depreciation:

Pumiture 750

Motor Car 3,000

Building 21,290

To Interest on Capital 30,000

To Net profit to Capital alc 60

1.44,100

1,44,100

Balance Sheet as on 31.12.1995

Liabilities Rs. Assets Rs.

5,00,000

30,000

4,25,800

21,290 4.04,510

15,000

750

30,000

3,000

Building

Capital

Add Interest on capital Less Depreciation

Net Profit 60 Furniture

S,30,060

1,800 5,28.260 Motor Car

Less Depreciation

14,250

Less Drawings

Sundry Creditors: Less Depreciation

Closing Inventory

56,000Sundry Debtors:

3,000

32,000

24.000

27,000

80,000

Ram

Shyam

Outstanding SaBaries

Sanjay

Kishore

12,000

20,000

18,000

Raghav 50,000

2.000

Prepaid Advertisenment

Cash at bank

6,000

3,500

5.87.260

Cash in hand

5,87.260

4. Note: Goods used tor domestic purpose shouid D

The following is the trial balance of Kamal Enterprises for the year ended 31st December

1996. you are required to prepare a Profit and Loss a/c and Balance Sheet after taking into

Rs.

1,50,300

5,000

llustrátion 3

account the adjustments given below.

Credit balances

Rs.

500 Sales

Debit balances

Cash in hand

1,200 Purchase returns

6,000 Accounts Payable

15,000 Bills Payable

1,200 Discount received

3,500 Dividendreceived

6,000 Rent receive

24,000 Capital

Cash at bank

12,000

Office furniture

8,000

Accounts Receivables

1,000

Commission

2,000

Bills Receivables

3,500

Power and fuel

27,000

Plant and Machinery

2,000

Office expenses

Carriage inwards

Carriage outwards

Rent, rates, and taxes

1,200

3,500

1,700

25,000

Leasehold Premises

Wages 30,000

Salaries 7,000

Opening lnventory

Sales Returns

Purchases

12,000

2,000

60,000

Drawings 7,000

2,08,800 2,08,800

Adjustments:

1. Closing Inventory as on 31.12.1996 Rs. 18,000

2. Depreciate Plant and Machinery at 10%.

3 Salaries outstanding Rs.1,000; Power and fuel outstanding, Rs.2,000.

4 Rs.5,000 was spent on erection of plant and machinery, but wrongly included under

wages.

5. Provide for bad and doubtful debts for Rs.1 500.

6. Discount earned but not received Rs.100.

7 Commission due but not recorded Rs.200

8. Rent received includes Rs.500 received in advance.

[M.C.A., May 1998, Madras University] )

Solution

BOOKS OF KAMAL ENTERPRISES

Trading and Profit and Loss account for the year ended 31-12-1996

ParticularTs

To Opening Inventory

To Purchases

Rs.

Particulars

12,000 By Sales Rs.

1,50,300

2,000 1,48,300

18,000

60,000

Less Returns Less Returns

5,000 55,000 By Closing Inventory

To Carriage inwards

1,200

5. 110

To Wages

Less Erection charges

30,000

5,000

6.000

2,000

25.000

To Power and fuel

Add Outstanding 8,000

65,100

1,66.300

1.66.300

65,100

To Gross Profit c'd

By Gross Profit bid

8,000 By Discounts

received

Add Outstanding

To Salaries 7,000 1,000

1100

2.000

Add Outstanding 1,000

1,200

100

To Commission

1,400By

Dividends received

2,000By Rent received

3,500Less Received in advance

1.700

2,900

1,500

50,200

200

Add Outstanding

To Office expenses

3.500

500 3,000

To Carriage outwards

To Rent, rates and taxes

To Depreciation on Plant

To Provision for bad debts

To Net Profit transferred to Capital

Account

71,200

71,200

Balance Sheet as on 31.12.1996

Rs

500

Liabilities

Rs.

ASsets

Accounts Payable

Bills Payable

12,000Cash in hand

8,000Cash at bank

1,200

Accounts Receivables 15.000

1.500

Outstanding expenses:

Less Provision for bad debts 13.500

1,000

2,000

200

Salaries

Power and fuel

3,200 Bills Receivables

500Closing Inventory

3.500

18.000

100

Commission

Rent received in advance

Discounts eaned but due

27,000

50,200

77.200

Furniture 6,000

Capital

Add Net Profit

Plant and Machinery

Add Erection charges 24,000

5,000

Less Drawings 7,000 70,200

Less Depreciation

Leasehold Premises

93,900

29.000

2900 26,100

25.000

93,900

Tllustration 4

Fromthefollowing particulars taken from the books of Nirmal Traders, prepare Trading

and Profit and Loss account 1or the year ended 31st December 2000 and the Balance Sheet as

on that date.

6. J0,000

114 Buildings 3,000 27 05

19 68

Less Depreciation

79.650

From the following

trial

balance

extracted

from the

books Mr. Ramesh pren

Rs

epare

Trading and Profit and Loss

Account and

Balance

Sheet as on 30th June 1999:

Rs.

Illustration 6

Debit balances

2.630

Debit balances

540 Cash at bank

680

Cash in hand 40,675 Returns inwards

4,730

10,480Fuel

2,040 Carriage outwards

Purchases

3.200

Wages

40,000

Carriage inwards

5,760 Building

1,76,580

Stock [Ist July 1998] 20.000 Credit Balances:

98,780

Machinery 7,500 Sales

500

Goodwill

15,000 Returns outwards

71.000

Salaries

3,600 Capital

Insurance 6300

14,500 Sundry Creditors

Sundry Debtors

5,245

DrawingsS 1,76.580

Take into account the following adjustments:

(a) Depreciate Building at 10% and Machinery at 20%,

(b) Salaries outstanding Rs,2,000.

(c) Create a Reserve for bad and doubtful debts at 5% on sundry debtors.

(d) Closing stock was valued at Rs.6,800. (e) Insurance prepaid Rs.200.

[M.C.A., November 2001, Madras University]

Solution

BOOKS OF RAMESH

Trading Account for the year ended 30th June 1999

Particulars Rs. Particulars Rs.

Opening stock 5,760 By Sales

98,780

To Purchases 40,675 Less Retuns inwards bo 680 98,100

Less Returns outwards 500 40,175|By Cloasing stock 6800

To Carriage inwards 2,040

To Wages 10,480

To Fuel 4,730

To Gross Profit to P&L alc 41,715

1,04,900 1,04,900

7. 115

Preparation of Final Accounts

Profit and Loss Account for the year ended 30th June 1999

Particulars Rs. Particulars Rs.

To Salaries 15,000 By Gross Profit b/d 41,715

Add Outstanding

2,000 17,000

To Insurance

3,600

Less Prepaid 200 3,400

To Carriage outwards

3,200

To Reserve for bad debts o L 725

4,000 01

4,000

9,390

To Depreciation: Building

Machinery

To Net Profit to Capital a/c

41,715 41,715

Balance Sheet as on 30th June 1999

Liabilities Rs. Assets Rs.

Sundry Creditors 6,300 Cash in hand

540

Salaries outstanding 2,000 Cash at bank

2,630

Capital 71,000 Sundry debtors 14,500

Add Net Profit

9,390 Less Resserve for bad debts 725 13,775

80,390 Closing Stock

6,800

Less Drawings 5,245 75,145|Prepaid Insurance

200

Machinery 20,000

Less Depreciation

4,000 16,000

Building 40,000

Less Depreciation

4,000 36,000

Goodwill

7,500

83,445

83,445

llustration 7