China: VAT in Inter-Company Service Transactions

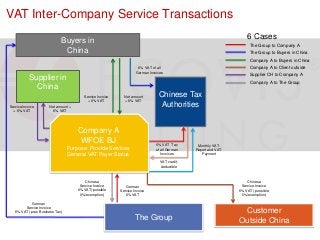

A European company decided to set up their own WFOE in Beijing. This subsidiary “Company A” almost completely provides its IT services to the ”Group’s” subsidiaries and some Chinese companies but seldom to other companies. But because of the new VAT regulations it was necessary to have a clear look at all the possible occurring transactions among the different parties mentioned above and bring light into the VAT reform. Assuming that Company A will have the status of a General Tax Payer and thus be allowed to deduct Input VAT from their Output VAT. The typical cases are listed below and in detail shown in the graphic. Although IT services belong to the pilot services of the VAT reform, depending on different factors they will be applicable to 6% VAT, 0% VAT or Tax Exemption. To get an insight of how the services will be invoiced and what amount of VAT will apply, the six different cases are shown in the graphic below. The Group is considering to set up its own WFOE not only because it could ease their work flow but also because they want to optimize their tax structure. The VAT reform in China started in Shanghai and only in certain industries but is now rolled out in whole China with more industries. These are the planned transactions between Company A and its clients and between The Group and China based companies. Below a list of the direction of the service provided. The Group provides services to Company A The Group provides services to Buyer in China Company A provides services to Buyer in China Company A provides services to Client outside China Supplier CH provides services to Company A Company A provides services to The Group The questioner was not sure about the current situation also because of the change from Business Tax (BT) to VAT in China. In the past BT was charged for most of the transactions but now it’s only applicable to a few industries. These were the main concerns of the questioner: Currently the foreign subsidiary provides services to companies in China, but they don’t know which VAT rate applies. Because they have trouble handling the Services provided to China, they want to set up a WFOE. They also want to know when VAT applies and how to handle it. Concerning the first point, the IT service they will provide, belongs to the pilot, and will we be taxed with 6% VAT on the foreign invoice. The Buyers in China which are General VAT Tax Payer (GP), have to withhold 6% VAT before transferring money to the foreign subsidiaries. That means they can use the 6% withheld VAT to credit it as its input VAT. Thus the overall effect is neutral. Taking a look at point 2 we see parallels to the first point, as Company A, the WFOE of The Group is also a General VAT Payer and thus has the right to deduct its Input VAT from its Output VAT. On a monthly basis it will then pay any excess Output VAT to the Tax Authorities. Find more on our blog!

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Empfohlen

Empfohlen (20)

China: VAT in Inter-Company Service Transactions

- 1. VAT Inter-Company Service Transactions 6 Cases Buyers in China The Group to Company A The Group to Buyers in China Company A to Buyers in China Supplier in China Supplier CH to Company A Company A to The Group Service Invoice + 6% VAT Service Invoice + 6% VAT Company A to Client outside 6% VAT of all German Invoices Net amount + 6% VAT Net amount + 6% VAT Company A WFOE BJ Chinese Tax Authorities 6% VAT Tax of all German Invoices Purpose: Provide Services General VAT Payer Status Monthly VATReport and VATPayment VAT credit, deductible Chinese Service Invoice 6% VAT( possible 0%/exemption) German Service Invoice 6% VAT German Service Invoice 6% VAT (prev. Business Tax) The Group Chinese Service Invoice 6% VAT ( possible 0%/exemption) Customer Outside China