Chp 15. amalgamation

•

7 gefällt mir•3,553 views

M.Com Final (University of Peshawar, Pakistan) Chapter 15. Amalgamation Solutions Part I Advanced Financial Accounting

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Ähnlich wie Chp 15. amalgamation

Ähnlich wie Chp 15. amalgamation (20)

Mehr von Arshad Islam

Mehr von Arshad Islam (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Chp 15. amalgamation

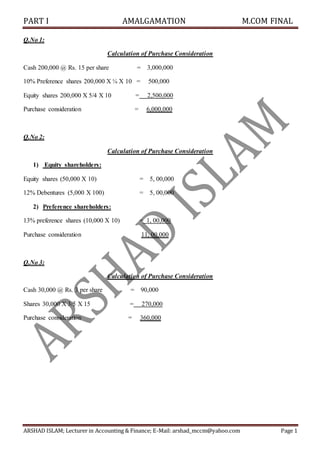

- 1. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 1 Q.No 1: Calculation of Purchase Consideration Cash 200,000 @ Rs. 15 per share = 3,000,000 10% Preference shares 200,000 X ¼ X 10 = 500,000 Equity shares 200,000 X 5/4 X 10 = 2,500,000 Purchase consideration = 6,000,000 Q.No 2: Calculation of Purchase Consideration 1) Equity shareholders: Equity shares (50,000 X 10) = 5, 00,000 12% Debentures (5,000 X 100) = 5, 00,000 2) Preference shareholders: 13% preference shares (10,000 X 10) = 1, 00,000 Purchase consideration 11, 00,000 Q.No 3: Calculation of Purchase Consideration Cash 30,000 @ Rs. 3 per share = 90,000 Shares 30,000 X 3/5 X 15 = 270,000 Purchase consideration = 360,000

- 2. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 2 Q.No 4: Calculation of Purchase Consideration (X Ltd): Assets taken over = 100,000 (-) Liabilities taken over = 25,000 P.C = 75,000 In the Books of X Ltd Ledger Accounts (1) REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Sundry assets A/C 120,000 By Sundry creditors A/C 25,000 By Shares in XY Ltd A/C 75,000 By Sundry Shareholders A/C (loss) 20,000 Total 120,000 Total 120,000 (2) XY Ltd. ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Realization A/C 75,000 By Shares in XY Ltd A/C 90,000 To Loan: Y Ltd A/C 15,000 Total 90,000 Total 90,000 (3) SHARES IN XY Ltd. ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To XY Ltd A/C 75,000 By Sundry Shareholders A/C 90,000 Total 90,000 Total 90,000 (4) SUNDRY SHAREHOLDERS ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Realization A/C 20,000 By Share Capital A/C 100,000 To Shares in XY Ltd A/C 90,000 By Profit & loss A/C 10,000 Total 110,000 Total 110,000

- 3. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 3 Q.No 5: In the Books of A Co Ltd (Transferee Company) Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Good Will A/C To Land & Building A/C To Plant & Machinery A/C To Stock A/C To Debtors A/C 350,000 50,000 150000 83000 35000 32000 2. 12% Debentures A/C To Realization A/C 100,000 100,000 3. B Co Ltd A/C To Realization A/C 245,000 245,000 4. Shares in B Co Ltd A/C Cash A/C To B Co Ltd A/C 165,000 80,000 245,000 5. Creditors A/C To Cash A/C 30,000 30,000 6. Realization A/C To Cash A/C 3,000 3,000 7. Equity share capital A/C General reserve A/C Profit & loss A/C To Sundry shareholders 200,000 50,000 20,000 270,000 8. Sundry shareholders A/C To Realization A/C 8,000 8,000 9. Sundry shareholders A/C To Cash A/C To Shares in B Co Ltd A/C 262,000 97,000 165,000 Working Notes: Payment of PC: Calculation of Purchase Consideration: Equity Shares (1650 x 100) 165000 Goodwill 75,000 Cash (245000 – 165000) 80000. Land & Building (150,000 X 90/100) 135,000 Total PC 245000 Plant & Machinery (83,000 X 90/100) 74,700 Stock (35,000 X 90/100) 31,500 Debtors (32,000 X 90/100) 28,800 Total Assets 345,000 12% Debentures (100,000) P.C Value 245,000

- 4. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 4 Q.No 6: In the Books of X Ltd (Transferee Company) (1) REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Land & Building A/C 350,000 By Creditors A/C 210,000 To Plant & Machinery A/C 670,000 By Debentures A/C 150,000 To Stock A/C 450,000 To Debtors A/C 250,000 By Y Ltd A/C (PC due) 1,000,000 To Bank A/C 30,000 By Sundry Shareholders A/C (loss) 390,000 Total 1,750,000 Total 1,750,000 (2) Y Ltd. ACCOUNT (Transferor Co) Particulars Amount(Rs) Particulars Amount(Rs ) To Realization A/C 1,000,000 By Shares in Y Ltd A/C 1,000,000 Total 1,000,000 Total 1,000,000 (3) SHARES IN Y Ltd. ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Y Ltd A/C 1,000,000 By Sundry Shareholders A/C 1,000,000 Total 1,000,000 Total 1,000,000 (4) PROFIT & LOSS ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Preliminary Exp. A/C To S. Shareholders A/C 10,000 20000 By Balance b/d 3,0000 Total 30,000 Total 30,000 SUNDRY SHAREHOLDERS ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Realization A/C 390,000 By Share Capital A/C 1,000,000 To Shares in Y Ltd A/C 1,000,000 By Profit & loss A/C 20,000 By Reserve A/C 370,000 Total 1,390,000 Total 1,390,000

- 5. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 5 Journal entries in the books of Y Ltd. (Transferor Co) Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To Liquidator of X Ltd. A/C 1,000,000 1,000,000 2. Land & Building A/C Plant & Machinery A/C Stock A/C Debtors A/C Bank A/C To 12% Debentures A/C To Creditors A/C To Reserve A/C To Profit & loss A/C To Business purchase A/C 350,000 670,000 450,000 250,000 30,000 150,000 210,000 370,000 20,000 1,000,000 3. Liquidator of X Ltd. A/C To Equity Share capital 1,000,000 1,000,000 4. Reserve A/C To Bank A/C 10,000 10,000 5. 12% Debentures A/C To Bank A/C 150,000 150,000 Q.No 8: Calculation of Purchase Consideration: 100,000 ÷ 10 = 10,000 × 11.55 = Rs 115,500 In the books of B Ltd. (Transferee Company) Journal entries Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Fixed Assets A/C To Stock A/C To Cash and Bank A/C 200,000 125,000 60,000 15,000 2. Creditors A/C To Realization A/C 50,000 50,000 3. A Ltd A/C To Realization A/C 115,500 115,500 4. Shares in A Ltd A/C To A Ltd A/C 115,500 115,500 5. Equity share capital A/C General Reserve A/C Profit & loss A/C To Sundry shareholders A/C 100,000 20,000 30,000 150,000 6. Sundry Shareholders A/C To Realization A/C 34,500 34,500 7. Sundry Shareholders A/C To Shares in Y Ltd A/C 115,500 115,500

- 6. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 6 Journal entries In the books of A Ltd. (Transferor Company) Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To Liquidator of B Ltd. A/C 115,500 115,500 2. Fixed Assets A/C Stock A/C Cash A/C To Creditors A/C To Reserve A/C To Profit & loss A/C To Business purchase A/C 125,000 60,000 15,000 50,000 4,500 30,000 115,500 3. Liquidator of B Ltd A/C To Equity Share Capital A/C 115,500 115,500 BALANCE SHEET Q.No 9: Journal entries in the books of A Ltd, B Ltd Date. Particulars. L/F. Debit (Rs.) Credit (Rs.) A Ltd B Ltd A Ltd B Ltd 1. Realization A/C To Land & building A/C To Plant & machinery A/C To Investments A/C To Stock A/C To Debtors A/C To Bank A/C 1,700,000 850,000 400,000 500,000 100,000 300,000 350,000 50,000 100,000 400,000 100,000 100,000 150,000 --------- 2. Creditors A/C To Realization A/C 450,000 200,000 450,000 200,000 3. C Ltd A/C To Realization A/C 1,200,000 600,000 1,200,000 600,000 4. Shares in C Ltd A/C To C Ltd A/C 1,200,000 600,000 1,200,000 600,000 5. Equity share capital A/C General reserve A/C To Sundry shareholders A/C 1,000,000 250,000 500,000 150,000 1,250,000 650,000 6. Sundry Shareholders A/C To Realization A/C 50,000 50,000 50,000 50,000 7. Sundry Shareholders A/C To Share in C Ltd A/C 1,200,000 600,000 1,200,000 600,000 Liabilities Amount(Rs) Assets Amount(Rs) Equity Share Capital (150,000 + 115,500) 265,500 Fixed assets (140,000 + 125,000) 265,000 Reserve (60,000 + 4,500) 64,500 Stock (30,000 +60,000) 90,000 Profit & loss (15,000 + 30,000) 45,000 Cash (80,000 + 15,000) 95,000 Creditors (25,000 + 50,000) 75,000 Total 450,000 Total 450,000

- 7. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 7 Journal entries in the books of C Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To liquidator of A Ltd. A/C To liquidator of B Ltd. A/C 1,800,000 1,200,000 600,000 2. Land & building A/C Plant & machinery A/C Investments A/C Stock A/C Debtors A/C Bank A/C To Creditors A/C To Reserve A/C To Business purchase A/C 500,000 900,000 200,000 400,000 500,000 50,000 650,000 100,000 1,800,000 3. Liquidator of A Ltd A/C Liquidator of B Ltd A/C To Equity Share capital A/C 1,200,000 600,000 1,800,000 4. Creditors A/C To debtors A/C (Mutual Indeptness) 50,000 50,000 5. General Reserve A/C To Stock A/C (25000 x 20/100) (Un realized profit in Stock) 5,000 5,000 BALANCE SHEET Liabilities Amount(Rs) Assets Amount(Rs) Equity Share Capital 1,800,000 Land & building 500,000 Reserve (100,000 - 5,000) 150,000 Stock (400,000 - 5,000) 395,000 Creditors (650,000 - 50,000) 600,000 Debtors (500,000 - 50,000) 450,000 Plant & machinery 900,000 Investments 200,000 Bank 50,000 Total 2,495,000 Total 2,495,000

- 8. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 8 Q.No 10 Journal entries in the books of B Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Fixed assets A/C To Stock A/C To Debtors A/C To Cash A/C 175,000 100,000 25,000 30,000 20,000 2. Creditors A/C To Realization A/C 10,000 10,000 3. A Ltd A/C To Realization A/C 120,000 120,000 4. Shares in A Ltd A/C (12000 x 10) To A Ltd A/C 120,000 120,000 5. Provision for bad debts A/C To Profit & Loss A/C 5,000 5,000 6. Profit & loss A/C To Advertisement Suspense A/C 10,000 10,000 7. Equity share capital A/C General reserve A/C Profit & loss A/C To Sundry shareholders A/C 100,000 40,000 25,000 165,000 8. Sundry Shareholders A/C To Realization A/C 45,000 45,000 9. Sundry Shareholders A/C To Shares in A Ltd A/C 120,000 120,000 Journal entries in the books of A Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To Liquidator of B Ltd. A/C 120,000 120,000 2. Fixed assets A/C Stock A/C Debtors A/C Cash A/C To Creditors A/C To Reserve A/C To Profit & loss A/C To Business purchase A/C 100,000 25,000 30,000 20,000 10,000 20,000 25,000 120,000 3. Liquidator of B Ltd A/C To Share capital A/C 120,000 120,000

- 9. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 9 BALANCE SHEET Q.No 11 Net Assets of A & B A Ltd : B Ltd Share Capital 150,000 : 100,000 General reserve 35,000 : 30,000 Profit & loss 15,000 : 10,000 Increase in the value of Assets Land & Building 15,000 : 5,000 Plant & machinery 10,000 : 5,000 Net Assets 225,000 : 150,000 225 : 150 15 : 10 3 : 2 Purchase Consideration: A Ltd: - 30,000 X 3/5 = 18,000 x 10 = Rs 180000 B Ltd: - 30,000 X 2/5 = 12,000 x 10 = Rs 120000 Liabilities Amount(Rs) Assets Amount(Rs) Equity Share Capital 270,000 Fixed assets 220,000 Reserve (30,000 + 20,000) 50,000 Stock (20,000 +25,000) 45,000 Profit & loss (20,000 + 25,000) 45,000 Debtor (50,000 + 30,000) 80,000 Creditors (20,000 + 10,000) 30,000 Cash ( 30,000 + 20,000) 50,000 Total 395,000 Total 395,000

- 10. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 10 Journal entries in the books of A Ltd, B Ltd. Date. Particulars. L/F. Dr. (Rs.)A Dr. (Rs.)B Cr. (Rs.)A Cr. (Rs.)B 1. Realization A/C To Land & building A/C To Plant & machinery A/C To Furniture & Fixture A/C To Stock A/C To Debtors A/C To Cash and Bank A/C 250,000 175,000 75,000 50,000 40,000 35,000 25,000 25,000 60,000 40,000 25,000 15,000 20,000 15,000 2. Creditors To Realization A/C 50,000 35,000 50,000 35,000 3. AB Ltd A/C To Realization A/C 180,000 120,000 180,000 120,000 4. Shares in AB Ltd A/C To AB Ltd A/C 180,000 120,000 180,000 120,000 5. Equity share capital A/C General reserve A/C Profit & Loss A/C To Sundry shareholders A/C 150,000 35,000 15,000 100,000 30,000 10,000 200,000 140,000 6. Sundry Shareholders A/C To Realization A/C 20,000 20,000 20,000 20,000 7. Sundry Shareholders A/C To Share in AB Ltd A/C 180,000 120,000 180,000 120,000 Journal entries in the books of AB Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To liquidator of A Ltd. A/C To liquidator of B Ltd. A/C 300,000 180,000 120,000 2. Land & building A/C Plant & machinery A/C Furniture & fixture A/C Stock A/C Debtors A/C Cash and Bank A/C To Creditors A/C To Reserve A/C To Profit & loss A/C To Business purchase A/C 135,000 90,000 65,000 50,000 45,000 40,000 85,000 15,000 25,000 300,000 3. Liquidator of A Ltd A/C Liquidator of B Ltd A/C To Share capital A/C 180,000 120,000 300,000

- 11. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 11 BALANCE SHEET OF AB Ltd. Q.No 12: Journal entries in the books of X Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To liquidator of Y Ltd. A/C (6,00,000 x 110/100) 660,000 660,000 2. Plant & machinery A/C Furniture A/C Stock A/C Debtors A/C Bank A/C To Creditors A/C To Capital Reserve A/C To Foreign Projects Reserve A/C To Profit & loss A/C To General reserve A/C To 11 % Debenture A/C To Business purchase A/C 550,000 135,200 315,800 129,300 74,360 182,480 13,000 9,700 24,130 15,350 300,000 660,000 3. Liquidator of Y Ltd A/C To Share capital A/C 660,000 660,000 4. 11% Debentures A/C To Debenture holder A/C 300,000 300,000 5. Debenture holders A/C To 12% Debentures A/C 300,000 300,000 Liabilities Amount(Rs) Assets Amount(Rs) Equity Share Capital 300,000 Land & building 135,000 Reserve 15,000 Stock 50,000 Creditors 85,000 Debtors 45,000 Profit & loss A/C 25,000 Plant & machinery 90,000 Furniture & fixtures 65,000 Cash 40,000 Total 425,000 Total 425,000

- 12. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 12 IN THE BOOKS OF “Y LTD” REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Machinery A/C 550,000 By 11 % Debentures A/C 300,000 To Furniture A/C 135,200 By Creditors A/C 182,480 To Stock A/C 315,800 By Sundry Shareholders A/C (loss) 62,180 To Debtors A/C 129,300 By X Ltd A/C 660,000 To Cash at Bank A/C 74,360 Total 1,204,660 Total 1,204,660 SUNDRY SHAREHOLDERS ACCOUNT Particulars Amount (Rs) Particulars Amount (Rs) To Realization A/C 62,180 By Share Capital A/C 600,000 To Share in X Ltd A/C 660,000 By Profit & loss A/C 24,130 By Capital Reserve A/C 13,000 By F. P Reserve A/C 9,700 By General Reserve A/C 75,350 Total 722,180 Total 722,180

- 13. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 13 Q.No 13: Journal entries in the books of B Co Ltd Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Building A/C To Plant & machinery A/C To Investments A/C To Stock A/C To Debtors A/C To Cash at Bank A/C 277,500 70,000 60,000 60,000 27,500 50,000 10,000 2. Sundry Creditors A/C Employees Provident fund A/C To Realization A/C 30,000 20,000 50,000 3. A Co Ltd A/C To Realization A/C 290,000 290,000 4. Equity Shares in A Co Ltd A/C Cash A/C To A Co Ltd A/C 260,000 30,000 290,000 5. Cash A/C To Realization A/C 55,000 55,000 6. Share capital A/C General reserve A/C Profit & loss appropriation A/C Accident Insurance Fund A/C Dividend Equalization Fund A/C To Sundry shareholders A/C 100,000 80,000 10,000 20,000 20,000 230,000 7. Sundry shareholders A/C To Preliminary expenses A/C 2,500 2,500 8. Realization A/C To Sundry shareholders A/C 117,500 117,500 9. Sundry shareholders A/C To Shares in A Co Ltd A/C To Cash A/C 345,000 260,000 85,000

- 14. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 14 Journal entries in the books of A Co Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase A/C To liquidator of B Ltd A/C 290,000 290,000 2. Plant & machinery A/C Buildings A/C Stock A/C Debtors A/C Cash at Bank A/C Goodwill A/C To Employees provident fund A/C To Creditors A/C To Business purchase A/C 60,000 70,000 27,500 50,000 10,000 122,500 20,000 30,000 290,000 3. Liquidator of Y Ltd A/C To Share capital A/C To Share premium A/C To Cash A/C 290,000 160,000 100,00 30,000 4. Good Will A/C To Cash A/C 2,000 2,000 Calculation of Purchase Consideration: Equity Shares in A Co Ltd (10,000 x 2 = 20,000 x13) Rs 260,000 Cash (10,000 x 3) 30,000 P.C 290,000 Q.No 14: Journal entries in the book of Y Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization account To Goodwill To Land & building To Plant & machinery To Closing Stock 462,000 50,000 200,000 100,000 30,000

- 15. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 15 To Debtor To Cash 50,000 32,000 2. Creditors Bills payable To Realization A/C 30,000 50,000 80,000 3. X Ltd To Realization A/C 495,000 495,000 4. Shares in X Ltd Cash 6% preference shares To X Ltd 360,000 30,000 10,500 495,000 5. 5% Preference shares Realization To Preference share holders 100,000 5,000 105,000 6. Preference shareholder To 6% preference shares of X 105,000 105,000 7. Equity share capital To Sundry shareholders 300,000 300,000 8. Sundry Shareholder To Prepaid Expense To Profit & loss A/C 15,000 5,000 10,000 9. Realization A/C To Cash 3,000 3,000 10. Realization A/C To Sundry shareholder 105,000 105,000 11. Sundry shareholders To Share capital To Cash 390,000 360,000 30,000 Journal entries in the book of X Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of B Ltd. 495,000 495,000 2. Land & building Plant & machinery Closing Stock Debtor Cash Goodwill To Creditors To Bills payable To Business purchase 200,000 183,000 30,000 50,000 32,000 80,000 30,000 50,000 495,000 3. Liquidation of Y Ltd To Share capital To 6% preference shares To Cash 120,000 360,000 105,000 30,000 Calculation of P.C Equity Shares 30,000 X 12/10 X 10 = 360,000 Cash = 30,000 6% preference shares ( 100,000 X 10/10) = 105,000 P.C = 495,000

- 16. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 16 Q.No 18 SOLUTION:- Journal entries in the book of Y Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Sundry assets 858,300 858,300 2. 5% Debentures Sundry creditors Dividend To Realization A/C 250,000 80,500 24,000 354,500 3. M Ltd To Realization 528,000 528,000 4. Equity shares in M Ltd Cash To M Ltd 520,000 8,000 528,000 5. Cash To Realization A/C 45,500 45,500 6. Cash (8,000 X ¼ X 63) Realization (8,000 X ¼ X 2) To Equity shares in M Ltd 126,000 4,000 130,000 7. Provision for tax To Cash 48,200 48,200 8. Share capital General reserve Profit & Loss To Sundry shareholders 400,000 50,000 5,600 455,600 9. Realization A/C To Sundry shareholder 65,700 65,700 10. Sundry shareholder To Equity shares in M Ltd To Cash 521,300 390,000 131,300 Journal entries in the book of M Ltd. Calculation of P.C Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of B Ltd. 528,000 528,000 2. Building Plant & machinery Debtor Stock Bank Goodwill To Provision for doubtfuldebts To Creditors To 5% Debentures To Dividend To Business purchase 170,000 380,000 140,500 80,700 16,500 86,515 4,215 80,500 237,500 24,000 528,000 3. Liquidation of D Ltd To Share capital To Share premium To Cash 528,000 480,000 40,000 8,000 4. Goodwill To Cash 1,500 1,500 5. 5% Debentures To 2% Debentures 237,500 237,500

- 17. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 17 Equity Shares 4,000 X 2 = 8,000 X 65 = 520,000 Cash 4,000 X 2 = 8,000 P.C = 528,000 REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) Assets 858,300 Liability 354,500 Share in M Ltd 4,000 P.C 528,000 Profit 65,700 Investment 45,500 Total 928,000 Total 928,000 Q.No 21 SOLUTION:- Requirement 1. Ratio of exchange of shares P.C calculation on take over basis Assets : Strong : Small Goodwill : --------- : 50,000 Fixed assets : 195,000 : 75,000 Stock : 42,000 : 47,000 Debtor : 30,000 : 50,000 Bank : 80,000 : 10,000 Total Assets = 347,000 232,000 Less:- Liability 10% Debentures : -------- : 20,000 Creditors : 15,000 : 32,000 Net Assets = 300,000 : 180,000 No. of shares = 15,000 : 12,000 Intrinsic Value = Net Assets/No. of shares 300,000/15,000 : 180,000/12,000

- 18. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 18 20per share : 15per share No of shares to be issued by Strong Ltd to Small Ltd to discharge P.C value of Small Ltd = Net Assets/per share value 180,000/20 = 9,000 Rate of exchange 12,000 : 9,000 4 : 3 3Shares of strong will be issued for every 4 shares of small Ltd held. Requirement 2. Journal entries in the book of M Ltd. Requirement 3. BANK ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To balance 80,000 Liquidation expense 3,000 To business purchase 10,000 Balance 87,000 Total 90,000 Total 90,000 Note:- It is assumed that strong Ltd will pay the debenture holder on subsequent date. May be after a week time. Q.No 25 SOLUTION:- Requirement 1. Calculation of P.C Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of Small Ltd. 528,000 528,000 2. Goodwill Fixed assets Debtor Stock Bank To 10% Debentures To Creditors To Business purchase 50,000 75,000 50,000 47,000 10,000 20,000 32,000 180,000 3. Liquidation of D Ltd To Share capital To Share premium 180,000 90,000 90,000 4. Liquidation expense To Bank 3,000 3,000 5. Goodwill To Liquidation expense 3,000 3,000

- 19. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 19 Assets : A : B Fixed assets : 830,000 : 1,600,000 Depreciation : 40,000 : ------------- : 79,000 : 1,600,000 Investment : 170,000 : ----------- Current Assets : 690,000 : 1,680,000 Total Assets = 1,650,000 : 3,280,000 Less:- Liability Secured loan : -------- : 400,000 Unsecured loan : 220,000 : ---------- Provision for tax : 110,000 : 520,000 Proposed dividend : ---------- : 100,000 Creditors : 420,000 : 460,000 Net Assets = 900,000 : 80,000 No. of shares = 5,000 : 80,000 Intrinsic Value = Net Assets/No. of shares 900,000/5,000 : 1,800,000/80,000 180per share : 22.5per share No of shares to be issued by B Ltd to Small Ltd to discharge P.C value of A Ltd = Net Assets/per share value 900,000/22.5 = 40,000 Rate of exchange 5,000 : 40,000 1 : 8 8Shares will be allotted of B to shareholders of A Ltd for One share held. Requirement 2.

- 20. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 20 Journal entries in the book of M Ltd. Requirement 3. BALANCE SHEET Particulars Amount(Rs) Particulars Amount(Rs) Share capital 1,200,000 Fixed assets 2,390,000 Share Premium 500,000 Investment 170,000 Secured Loan 400,000 Current Assets 1,370,000 Unsecured Loan 220,000 Creditor 880,000 Provision for tax 630,000 General Reserve 1,000,000 Dividend 100,000 Total 4,930,000 Total 4,930,000 Q.No 26 SOLUTION:- Requirement 1. Capital employed S M Fixed Assets (Revalued) : 35,500 : 195,000 Current assets : 149,750 : 87,875 Total Assets : 504,750 : 273,875 (-) Liability : 298,500 : 90,125 Capital employed : 206,250 : 183,750 Requirement 2. Average Profit Year : S : M 1993 : 224,788 : 136,950 1994 : (1,250) : 171,050 1995 : 188,962 : 179,500 Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of Small Ltd. 900,000 900,000 2. Fixed assets Current Assets Investment To Unsecured loan To Creditors To Provision for tax To Business purchase 790,000 690,000 170,000 220,000 420,000 110,000 900,000 3. Liquidation of A Ltd To Share capital To Share premium 900,000 400,000 500,000

- 21. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 21 : 412,500 : 487,500 Divide By 3 We get:- 137,500 : 162,500 Ration of net average profit 137,500 : 162,500 1,375 : 1,625 11 : 13 No. of Shares to be issued:- 30,000 at ratios S : M 30,000 X 11/24= 13750 : 30,000 X 13/24 = 16,250 Total value of shares S = 13,750 X 5 = 68,750 M = 81,250 X 5 = 81,250 Debentures to be issued:- To give income equivalent to 8% capital employed by their respective business. So their 8% income of capital employed S = 206,250 X 8/100 = 16,500 M = 183,750 X 8/100 = 14,700 Amount of debenture to be issued:- S = 165,000 X 100/15 = 110,000 M = 147,000 X 100/15 = 98,000 No P.C Value:- S : M Shares : 68,750 : 81,250 Debentures : 110,000 : 98,000 178,750 : 179,250 BALANCE SHEET

- 22. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 22 Particulars Amount(Rs) Particulars Amount(Rs) Share Capital (30,000X5) 150,000 Fixed assets (355,000 + 195,000) 550,000 Debentures (110,000 + 98,000) 208,000 C. Assets (149,750 + 78,875 – 21,675) 266,950 C. Liability (298,500 +90,125 – 21,675) 366,950 Capital reserve 32,000 Total 756,950 Total 756,950 Q.No 28 SOLUTION:- Requirement 1. Average Profit Year : River : Canal 1995 : 352,500 : 275,000 1996 : 440,000 : 320,000 1997 : 445,000 : 342,500 : 1,237,500 : 937,500 Divide By 3 We get:- 412,500 : 312,500 Requirement 2. Return on capital Rate 10% : River : Canal Total assets : 3,500,000 : 4,500,000 Less: Liability : (1,000,000) : (2,750,000) : 2,500,000 : 1,750,000 Return rate 2,500,000X10/100 : 1,750,000X10/100 Std Profit : 250,000 : 175,000 Requirement 3. Goodwill Calculation 2.5 times of average profit after deducting the Std profit of C. employed : River : Canal Std profit : 412,500 : 312,500 Less : 250,000 : 175,000 : 162,500 : 137,500

- 23. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 23 Multiply By : 2.5 : 2.5 Goodwill : 406,250 : 343,750 Calculation of P.C River Canal Goodwill : 406,250 : 343,750 Fixed Assets : 2,250,000 : 1,450,000 Current assets : 1,250,000 : 3,050,000 Total Assets : 3,906,250 : 4,843,750 (-) Liability : 1,000,000 : 2,750,000 Net assets : 2,906,250 : 2,093,750 Per share value : 12.5 : 12.5 No of shares to be issued 232,500 : 167,500 BALANCE SHEET Particulars Amount(Rs) Particulars Amount(Rs) Share Capital (500,000X10) 5,000,000 Goodwill (406,250 + 343,750) 750,000 Share premium (500,000X2.5) 1,250,000 Current Assets 4,300,000 Creditors (1,000,000 +2,750,000) 366,950 Fixed assets 3,700,000 Bank (100,000 X 12.5) 1,250,000 Total 10,000,000 Total 10,000,000 INTER-COMPANY INVESTMENT Q.No 30 SOLUTION:- Journal entries in the book of Y Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Sundry assets 340,000 340,000 2. Sundry creditors To Realization A/C 140,000 140,000 3. XY Ltd To Realization 60,000 60,000 4. Equity shares in XY Ltd To XY Ltd 60,000 60,000 5. Share capital To Shareholders 200,000 200,000 6. Shareholders To Realization 140,000 140,000 7. Shareholders A/C To Shares in XY Ltd 60,000 60,000

- 24. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 24 Journal entries in the book of X Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Sundry assets 500,000 500,000 2. Sundry creditors Debentures To Realization A/C 150,000 100,000 250,000 3. XY Ltd To Realization 50,000 50,000 4. Equity shares in XY Ltd To XY Ltd 50,000 50,000 5. Share capital Profit & loss A/C To Shareholders 400,000 50,000 450,000 6. Shareholders To Realization 200,000 200,000 7. Shares in XY Ltd Shareholders A/C To Investment in Y Ltd 45,000 155,000 200,000 8. Sundry Shareholders To Shares in XY Ltd 95,000 95,000 Journal entries in the book of XY Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of X Ltd To Liquidation of Y Ltd 340,000 50,000 60,000 2. Sundry assets To 15% debentures To creditor To Business purchase 500,000 100,000 290,000 110,000 3. Liquidation of XY To Share capital 110,000 110,000 Calculation of P.C X Ltd Y Ltd Assets taken over 300,000 : 200,000 Less Liability 15% Debentures 100,000 : -------- Creditors 150,000 : 140,000 P.C 50,000 : 60,000 REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) Assets 340,000 Creditors 140,000 XY Ltd 60,000 Loss 140,000 Total 340,000 Total 340,000 SHAREHOLDERS ACCOUNT

- 25. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 25 Particulars Amount(Rs) Particulars Amount(Rs) Assets 140,000 Capital 200,000 Share 60,000 Total 200,000 Total 200,000 OPENING BALANCE SHEET XY Liability Amount(Rs) Assets Amount(Rs) Share capital 110,000 Sundry Assets 500,000 Debentures 290,000 Creditors 100,000 Total 500,000 Total 500,000 Q.No 31 SOLUTION:- Calculation of Purchase Consideration Cash 1,000,000/10 = 100,000 100,000 X 20 M.R = 2,000,000 2,000,000 / 25 = 80,000 Less Already in hand = 15,000 New shares to be issue = 65,000 Purchase consideration(65000X25) = 1,625,000 In the book of Summit REALIZATION ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) Sundry Assets 1,000,000 Debentures 1,000,000 Stock 700,000 P. Tax 200,000 Debtor 1,450,000 Other liabilities 800,000 Cash 50,000 Apex Ltd P.C 1,625,000 Profit 425,000 Total 3,625,000 Total 3,625,000 INVESTMENT IN SHARES OF APEX Particulars Amount(Rs) Particulars Amount(Rs) To balance 300,000 By shareholders 2,000,000

- 26. PART I AMALGAMATION M.COM FINAL ARSHAD ISLAM; Lecturer in Accounting & Finance; E-Mail: arshad_mccm@yahoo.com Page 26 Apex Ltd P.C 1,625,000 Shareholders 75,000 Total 2,000,000 Total 2,000,000 SHAREHOLDERS ACCOUNT Particulars Amount(Rs) Particulars Amount(Rs) To Share in Apex Ltd 2,000,000 By capital 1,000,000 Reserve 500,000 Profit(R.A) 425,000 Profit(investment) 75,000 Total 2,000,000 Total 2,000,000 Journal entries in the book of Summit. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Realization A/C To Sundry assets 3,200,000 3,200,000 2. Debentures P. Tax Other liability To Realization A/C 1,00,000 200,000 800,000 2,000,000 3. Apex Ltd To Realization 1,625,000 1,625,000 4. Equity shares in Apex Ltd To Apex Ltd 1,625,000 1,625,000 5. Realization A/C To Shareholders 425,000 425,000 6. Shares in Apex To Investment To realization 375,000 300,000 75,000 7. Shareholders A/C To Shares in Apex Ltd 2,000,000 2,000,000 Journal entries in the book of Apex Ltd. Date. Particulars. L/F. Dr. (Rs.) Cr. (Rs.) 1. Business purchase To Liquidation of summit 1,625,000 1,625,000 2. Goodwill Fixed assets Stock Debtor Cash To Debenture To provision for tax To Other liabilities To Business purchase 475,000 1,000,000 700,000 1,450,000 50,000 1,050,000 200,000 800,000 1,625,000 3. Liquidation of summit To Share capital To Share premium 1,625,000 650,000 975,000