Create New Division for Small Medium Enterprise Financing

•Als DOCX, PDF herunterladen•

1 gefällt mir•840 views

Building a New Business Model For New Division at Bank of Vietnam

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Create New Division for Small Medium Enterprise Financing

Ähnlich wie Create New Division for Small Medium Enterprise Financing (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Create New Division for Small Medium Enterprise Financing

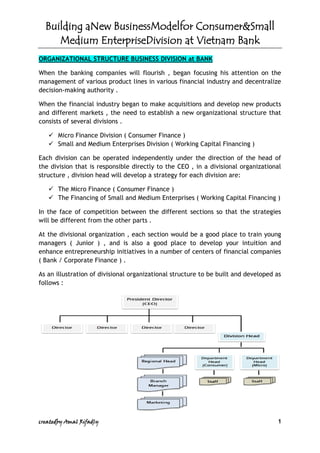

- 1. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 1 ORGANIZATIONAL STRUCTURE BUSINESS DIVISION at BANK When the banking companies will flourish , began focusing his attention on the management of various product lines in various financial industry and decentralize decision-making authority . When the financial industry began to make acquisitions and develop new products and different markets , the need to establish a new organizational structure that consists of several divisions . Micro Finance Division ( Consumer Finance ) Small and Medium Enterprises Division ( Working Capital Financing ) Each division can be operated independently under the direction of the head of the division that is responsible directly to the CEO , in a divisional organizational structure , division head will develop a strategy for each division are: The Micro Finance ( Consumer Finance ) The Financing of Small and Medium Enterprises ( Working Capital Financing ) In the face of competition between the different sections so that the strategies will be different from the other parts . At the divisional organization , each section would be a good place to train young managers ( Junior ) , and is also a good place to develop your intuition and enhance entrepreneurship initiatives in a number of centers of financial companies ( Bank / Corporate Finance ) . As an illustration of divisional organizational structure to be built and developed as follows :

- 2. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 2 Advantages ofdivisionalorganizationalstructurefunctionsbuilt, among others: Coordinationacross functionsbecomes easierandfaster Havingflexibilityinthestructure ofbank specializationin each divisioncan be maintained Openmorecareeropportunities Potentialcompetitionin the organizationCEOroutineexpensesreducedso as to havetimeforstrategicdecisions Inimplementingthestrategy ofa modelof themaintasksthat shouldbe donein theimplementation processare: SUMMARYROLE OFPOSITION HEADDIVISIONhas the dutyand responsibilityof the entire systemandoperationaldivisionsrunningand leadinga special sectionwithin thedivisionaremanaged, and thecoordinationbetween the divisionsforthe purposeof businessmodelsbuiltpassageandprovidereportsto the CEOjob. MAIN TASKSDIVISIONHEAD Build amodel ofretailfinancing business(consumer finance) andsmall and medium enterprises(micro financing) Coordinatemarketingactivities offinancialservicesproducts, in orderto achievethe target. Formulatesegmentation, targetingandpositioningforfinancialservicesproductsin accordancewitha predetermined strategy.

- 3. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 3 Creatingan extensive marketing networkforfinancialservicesproductsaccording to market conditionsineachregion. Perform analysisandevaluation ofcredit marketingprograms. Formulatepromotional activities. Coordinate the activities ofa feasibility studytoassessnewbusiness opportunitiesas well asbusinessconductcustomersatisfactionresearch. Orientationonachievementandincreaseprofits Addressing thefinancing risktocreditrisk Benchmarkingactivitiesinfinancial servicesproductsin order to improvethe performance ofdivis. Identifygovernment regulationthat hamperbusinessandbusinessissues, in ordertoset priorities formarketingstrategy FormulateQuality ObjectivesandQuality ProceduresUnitUnitwhichis a translationof theQuality PolicyandQuality Objectivesestablishedcompany. Divisionprepareactivity reportscorrectlyand on time. BUSINESS PLAN Consistent serving and empowering low-income segments of society as well as small to medium sized small business . Develop a business that focuses on MASS MARKET service and empowerment, strategic steps that will be done is to create a plan and build consumer finance business units that are consumer and consumer financing for small and medium businesses. The business plan is focused on two core components ,namely the empowerment of women and integrated financial program for a better future. Initiatives in line with the Bank's financial inclusion Vietnam , the focus is to develop the business division that is specifically designed to meet the banking needs of low-income segments of society as well as small and medium enterprises , including for pre-prosperous productive society to gain access to banking services, I designed a business model innovation tailored to the needs of the community.

- 4. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 4 The segment not only need access to finance , but also training and mentoring to increase capacity so that customers can grow their business in a sustainable manner . COMPATIBLEPRODUCTPORTFOLIOSEGMENT Classificationgroupingcustomersbased onthe portfolioto be managedcollectively. Optimizethe profit obtainedfrom allcustomersby offeringa differentvaluepropositiontodifferent segments. Forobtainingidentifyingmarketprofitopportunitiesinthe future. MARKETSEGMENTATION(The process of dividing the marketaremorehomogeneousgroupedandcharacteristicsthatwillcreatea different valueineachcustomergroup). MARKETSEGMENTATIONPROCESS DISTRIBUTIONMODEL Application of marketing distribution mix of products and services on the Bank / finance companies ( Triangle Marketing). PRODUCT Attributesthat accompanythe system, proceduresandservicesthatpay attention tomatters relating to thesize, shape, andquality. PRICE Prices in products and services , in the form of counterperformance in the form of

- 5. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 5 interest rates , both for deposits and loan products , as well as fees for banking services. PROMOTION Promotional activities on products and services through advertising in mass media , or television , the overall concept of promotional activities include Interest Rate , Product Sales Promotion , Public Relations , Sales Trainning , Marketing Research & Development . PLACE Distribution channels Bank products and services , such as branch offices , which directly provide products and services offered . PEOPLE Her personal approach dominant element of the ranks of the front office ,back office up to the managerial level. PROCESS Systems and procedures covering the terms and conditions imposed by the Bank's products and services . Systems and procedures reflect an assessment of the service sooner or later , the use of appropriate technology and excellent creativity required for a process that is fast yet safe . OPERATIONAL MODEL The series of value chain activities for the company's operations in the banking industry that are specific to each activity the product gains some value . Activities that provide value -added products products from total value added of all common activity that categorizes the value -added of the primary organization that built the business includes the sale rate . Sales and marketing operations , administrative infrastructure management , human resource management and management technologist . Costs and value drivers are identified for each value activity is divided into 2 types ,namely : 1. PRIMARY ACTIVITY Inbound logistics, activities associated with material handling before use. Operations, activity of which is related to the processing of inputs into outputs. Outbound logistics, activities undertaken to deliver the product into the hands of consumers.

- 6. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 6 Marketing and sales, activities associated with directing consumers to be interested in buying the product . Service, activities that maintain or increase the value of the product. 2. SUPPORT ACTIVITY Procurement, relating to the acquisition of inputs / resources . Human Resources Management, HR settings ranging from recruitment ,compensation, and termination . Technological Development, development tools, software , hardware , procedures , products in the transformation of inputs into outputs. Infrastructure, consisting of departemen-departemen/fungsi-fungsi (accounting , finance , planning and so on) that serve the needs of the organization and bind the parts into a whole. Retail business functions (Consumer financeconsumer goodsand small medium enterprises) which isfocused on Research and Development, Product Design, Service, Production Process, Marketing & Sales of products by providing loans to eligible consumers, Distribution Customer Service. HUMAN RESOURCES Human Resources Training Unit , which is responsible for the development and implementation of human resource development programs , including Management Development , Information Technology Development , Dealer Development , Human Resources Development . Technological DevelopmentInfrastructure, Management Information Systems, Accounting, Operations, Financial, Human Resources Department. Electronic banking servicesDiversion, Delegated Authority and Service Strategy 'from the Central Office to the branch office network . Structure formation , Credit Service Center and Branch Service Center, so that lending is more efficient and improve service and business analysis in the branch office . Infrastructure that was developed based on four main concepts that structure of reporting lines, forms a flat structure, a hierarchical organizational structure, and the structure of the Strategic Business Unit . Internal Control, Internal Audit constructed, Compliance, Risk Management UnitIntranet for all branches .

- 7. Building aNew BusinessModelfor Consumer&Small Medium EnterpriseDivision at Vietnam Bank createdby Amal Rifadly 7 Risk Management as part of the risk management infrastructure. Various committees namely Risk Mitigation , Corporate Governance , Risk Management , Audit , Credit , Products , Assets and Liabilities. Restucturing and Settlement, an independent committee with a special unit handling problem loans. Instutional Banking Group and Asset - Liability Management, As a supporter of the Bank's activities and treasury activities . FINANCIAL MODEL Iattachsamplefinancialmodelanalysisin buildingproductsfinancing : FINANCIAL MODEL Summary Year 1 Year 2 Year 3 Year 4 Year 5 PRODUCTIVITY Sales Person 15 15 15 15 15 Total Customer Acquired 2.376 2.880 2.880 2.880 2.880 Avg Customer Acquired / Mth 198 240 240 240 240 Total Disbursement 7.128 8.640 8.640 8.640 8.640 Avg Disbursement / Mth 594 720 720 720 720 BALANCE SHEET Number of Customer 1.579 2.469 3.098 3.681 4.225 Outstanding Balance 4.936 7.302 7.882 8.127 8.259 PROFIT & LOSS Margin Income 1.752 4.622 5.595 5.875 6.000 FTP (360) (948) (1.148) (1.206) (1.231) Net Margin Income 1.393 3.674 4.447 4.670 4.769 Fee Income 238 288 288 288 288 Total Income 1.630 3.962 4.735 4.958 5.057 Manpower Cost 1.541 1.541 1.541 1.541 1.541 Operational Cost 78 78 78 78 78 Total Cost 1.619 1.619 1.619 1.619 1.619 Profit Before Tax (82) 2.198 2.581 2.852 3.052 Profit After Tax (57) 1.539 1.806 1.997 2.136 NPL 1% 2% 3% 3% 4% START MAKING PROFIT Yes 7 BULAN BREAK EVEN POINT Yes 12 BULAN BRANCH