The Most Attractive Hyderabad Call Girls Kothapet 𖠋 6297143586 𖠋 Will You Mis...

Otc markets group vic init writeup apr 2020

1. Inbox Signed in as ydavidli@gmail.com. Logout

Ideas

Topics 3032

Messages

More

Profile

About

APPLY

OTC MARKETS GROUP INC OTCM

April 15, 2020 - 6:17pm EST by

Astor

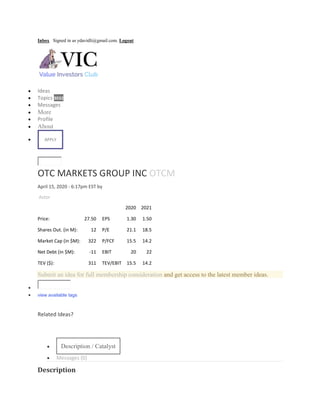

2020 2021

Price: 27.50 EPS 1.30 1.50

Shares Out. (in M): 12 P/E 21.1 18.5

Market Cap (in $M): 322 P/FCF 15.5 14.2

Net Debt (in $M): -11 EBIT 20 22

TEV ($): 311 TEV/EBIT 15.5 14.2

Submit an idea for full membership consideration and get access to the latest member ideas.

view available tags

Related Ideas?

Description / Catalyst

Messages (0)

Description

2. OTC MARKETS GROUP INC. (OTCM) – Long

Market Cap: $322mm (Last Sale: $27.50)

TEV: $311b (~$11mm Net Cash)

30 Day Avg Daily Volume: ~6k shares/day (~$160k)

Investment Horizon: ~36-60 months

Summary

OTC Markets (OTCM) is a high quality, defensive business that is run by an owner-operator who is more

than capable at navigating the company through the current COVID-19 related market malaise. The

company has a net cash balance sheet and, despite a challenging macro backdrop, will see a >20%

increase in free cash flow this year as investment spend steps down to more normalized levels. Trading

at ~15x trailing twelve-month free cash flow (adjusting capex to normalized levels) we believe the stocks

valuation is undemanding. Overall, we believe the current drawdown provides an attractive opportunity to

establish a long position in the equity, and, including dividends, we believe OTCM can reasonably

compound shareholder value at a high-teens IRR over the next 3-5 years.

Business Overview

OTCM operates the OTCQX Best Market, the OTCQB Venture Market, and the Pink Open Market for

10,000 U.S. and global securities. Through OTC Link ATS, the company connects a diverse network of

broker-dealers that provide liquidity and execution services. Overall, OTCM generates about 85%-90% of

its revenue through a subscription-based sales model.

OTCM operates several businesses:

- OTC Link (19% of 2019 total revenue)

o Alternative Trading System (ATS) – broker-dealers pay subscription and usage fees

related to the number of quotes and messaging volumes. 89 broker-dealer subscribe to

OTC Link ATS today.

o Electronic Communication Networks (ECN) – fees are transaction-based with rebates

for liquidity provision.

- Market Data Licensing (39%)

o Users subscribe to licenses for market data, compliance data, company data, and

security information collected by OTC Link and Corporate Services. Users include

investors, traders, institutions, accountants and regulators. OTCM Market Data is

distributed by most major financial data distributors, including Bloomberg, Thomson

Reuters, Interactive Data, Factset, Fidessa, NASDAQ and SIX Financial.

- Corporate Services (42%)

o OTCQX / OTCQB / Pink Sheets – corporates pay application and annual (or semi-

annual) subscription fees. Number of securities: ~10,000, including 5,300 international

securities, 550 banks, 3,400 non-penny stocks and 2,300 SEC reporting companies.

o Other – the OTC Disclosure & News Service and Virtual Investor Conferences

revenues are usage dependent.

3. Summary Thesis

- While not fully insulated from recessionary conditions, OTCM will hold up well in the current

environment. Consensus (which consists of only 2 analysts) is calling for ~5% sales increase in 2020 –

while this estimate will see downward revisions given current market conditions, almost 90% of OTCM’s

revenue is recurring in nature, providing reassurance that such revisions will be modest in size (we

assume flat revenue in 2020). Over the last decade, OTCM has grown revenue ~8.5% per annum on

average (and this has largely been accomplished through organic growth initiatives).

- OTCM is a relatively high moat business

o Entrenched relationships w/ broker-dealers – once they are on the platform, they’re

highly likely stay on the platform

o Very strong relationships w/ Bloomberg, Factset, and other data redistributors

o Very high ROE (88% in 2019) indicative of the business quality.

- The operating cost base is largely fixed, which should provide for substantial operating leverage

going forward.

o In particular ~65% of operating costs are personnel related. OTCM expanded their

team in 2019 resulting in heightened costs, though they have now indicated that that

expansion is complete.

o Looking out over the next several years, and assuming mid-single digit organic growth

we would expect that by 2023 EBITDA margins to expand by at least 500bps from 2019's

relatively depressed levels.

- Investment cycle completed in 2019

o OTCM spent $5.7mm in capex in 2019 (new office in London, new HQ in NYC, tech

related capex, personnel expansion) – this is about 10x the level of 2018. We expect

more normalized capex levels in the ~$1.0mm range in each of the next several years.

- New initiatives will be additive to growth – namely Virtual Investor Conferences, a business OTCM

bought in 2019 seems like a timely and well-suited offering for today’s environment.

- Strong owner-operator led management team

o Cromwell Coulson (CEO) bought the company in 1997. Prior to OTCM, Coulson was

a trader and portfolio manager at Carr Securities Corp, an institutional broker-dealer and

market maker.

o Today Coulson and his family own ~36% of the shares.

- Fortress balance sheet and shareholder friendly capital allocation policy

o OTCM consistently runs a very conservative balance sheet, and had net cash

~$11mm at 12/31/19.

o The company pays a consistent quarterly dividend ($0.15/sh now), and in each of the

past 8 years has paid a special dividend ($0.65/sh in FY19).

o Management is repurchases OTCM stock at a modest clip (bought back ~$1-$2mm

shares in each of last several years).

- Valuation undemanding

o OTCM trades ~20x ttm (or 2019) FCF. Adjusting 2019 capex lower to normalized

levels the stock trades at ~15x 2019 FCF.

§ The exchanges (CME, ICE, etc.) generally trade in the 18x-28x ttm FCF range.

§ Fintech comps (MSCI, INFO, etc. trade in the 25x-40x ttm FCF range.