Nsl Product Guide Fixed Rate Interest Only

•

0 gefällt mir•360 views

Nsl Product Guide Fixed Rate Interest Only

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Ähnlich wie Nsl Product Guide Fixed Rate Interest Only

Ähnlich wie Nsl Product Guide Fixed Rate Interest Only (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Nsl Product Guide Fixed Rate Interest Only

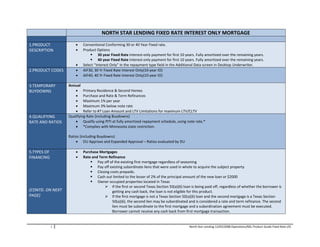

- 1. NORTH STAR LENDING FIXED RATE INTEREST ONLY MORTGAGE 1.PRODUCT • Conventional Conforming 30 or 40 Year Fixed rate. DESCRIPTION • Product Options 30 year Fixed Rate Interest‐only payment for first 10 years. Fully amortized over the remaining years. 40 year Fixed Rate Interest‐only payment for first 10 years. Fully amortized over the remaining years. • Select “Interest Only” in the repayment type field in the Additional Data screen in Desktop Underwriter. 2.PRODUCT CODES • AIF30, 30 Yr Fixed Rate Interest Only(10‐year IO) • AIF40, 40 Yr Fixed Rate Interest Only(10‐year IO) 3.TEMPORARY Annual BUYDOWNS • Primary Residence & Second Homes • Purchase and Rate & Term Refinances • Maximum 1% per year • Maximum 3% below note rate • Refer to #7 Loan Amount and LTV Limitations for maximum LTV/CLTV 4.QUALIFYING Qualifying Rate (including Buydowns) RATE AND RATIOS • Qualify using PITI at fully amortized repayment schedule, using note rate.* • *Complies with Minnesota state restriction. Ratios (including Buydowns) • DU Approve and Expanded Approval – Ratios evaluated by DU 5.TYPES OF • Purchase Mortgages FINANCING • Rate and Term Refinance Pay off of the existing first mortgage regardless of seasoning Pay off existing subordinate liens that were used in whole to acquire the subject property Closing costs prepaids. Cash out limited to the lesser of 2% of the principal amount of the new loan or $2000 Owner occupied properties located in Texas If the first or second Texas Section 50(a)(6) loan is being paid off, regardless of whether the borrower is (CONTD. ON NEXT getting any cash back, the loan is not eligible for this product. PAGE) If the first mortgage is not a Texas Section 50(a)(6) loan and the second mortgage is a Texas Section 50(a)(6), the second lien may be subordinated and is considered a rate and term refinance. The second lien must be subordinate to the first mortgage and a subordination agreement must be executed. Borrower cannot receive any cash back from first mortgage transaction. 1 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 2. If a Texas Section 50(a)(6) second lien is being paid off, the loan is not eligible for this product. The title policy will reference Texas Section 50(a)(6). Equity Refinances • No seasoning requirements on first mortgage or junior liens. (except 6 months on cashout refinances) • Owner occupied properties located in Texas subject to Texas Section 50(a)(6) are NOT eligible. Paying off loans that are not Texas Section 50(a)(6) but are defined as a cash out refinance based on agency guidelines are eligible for this product. Borrower cannot receive any cash back from the transaction. 6.MAXIMUM LOAN Minimum Loan Amount for all NSL Products is $30,000.00 AMOUNT Units Maximum Loan Amount Continental US Alaska & Hawaii 1 $417,000 $625,500 2 $533,850 $800,775 3 $645,300 $967,950 4 $801,950 $1,202,925 2 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 3. 7.LOAN AMOUNT • Refer to #8 Secondary Financing AND LTV • HCLTV (HELOC CLTV) = first mortgage balance + total Heloc amount (funded + unfunded portion) divided by the lesser LIMITATIONS of the appraised value or sales price (if applicable) PRIMARY RESIDENCES DU Approve Units LTV LTV W/ CLTV Max Credit W/O Sec Fin W/Sec HCLTV Score Sec Fin Fin Purchase and Rate & Term Refinance 1 Unit 95% 90% 95% 95% n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a 2 Unit 90% 85% 90% 90% n/a n/a n/a n/a n/a n/a 3‐4 Unit 75% 70% 75% 75% n/a Cash Out Refinance 1‐2 Unit 85% 80% 85% 85% n/a 3‐4 Unit 75% 70% 75% 75% n/a SECOND HOMES DU Approve Units LTV LTV W/ CLTV Max Credit W/O Sec Fin W/Sec HCLTV Score Sec Fin Fin Purchase and Rate & Term Refinance 1 Unit 90% 85% 90% 90% n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a n/a Cash Out Refinance (CONTD. ON NEXT 1 Unit 85% 805% 85% 85% n/a PAGE) 3 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 4. INVESTMENT PROPERTIES 1 DU Approve 1 Units LTV LTV W/ CLTV Max Credit W/O Sec Fin W/Sec HCLTV Score Sec Fin Fin Purchase 1‐2 unit 85% 80% 85% 85% n/a Rate & Term Refinance 75% 70% 75% 75% n/a Cash Out Refinance 1‐2 unit 70% 65% 70% 70% n/a ALL INVESTMENT PROPERTY LOANS MUST BE FULL DOC, DOC WAIVER INELIGIBLE 8.SECONDARY • Permitted – Refer to # 7 Loan Amount and LTV Limitations. FINANCING 9. PROPERTY TYPES Eligible Property Types • 1‐4 units • PUDs1 – Fannie Mae warrantable projects. • Condo1 – Fannie Mae warrantable projects. Ineligible Property Types • Co‐ops • Manufactured homes 1 Refer to NSL Underwriting Guidelines 10.OCCUPANCY • Primary Residence • Second Homes 4 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 5. • Investment Properties 11.GEOGRAPHIC Continental US, Hawaii and Alaska LOCATIONS/ RESTRICTIONS 12.ASSUMPTIONS Not permitted 13.ESCROW Refer to NSL Underwriting Guidelines WAIVER 14.PREPAYMENT None PENALTY 15.UNDERWRITING Automated Underwriting Requirements • All loans must be submitted to Desktop Underwriter Version 7.1 • Must receive a DU “Approve/Eligible” for Fixed Rate IO and Fixed Rate IO w/ Sub Financing • May follow DU decision and documentation requirements 16.BORROWER US Citizens ELIGIBILITY Permanent Resident Aliens • Provide Alien Registration Card. Trust Agreements • Refer to NSL Underwriting Guidelines 17.CO‐BORROWER • Co‐borrower does not have to occupy the subject property 18.CREDIT • DU Approve, credit evaluated by AUS 19.ASSETS Borrower Investment • Primary residence and second homes require 5% from borrower’s own funds. • Investment property loans require 10% from borrower’s own funds Seller Contributions‐Basis for the limit is now based on CLTV ratio • Primary Residence & Second Homes 3% for CLTV > 90.01 5 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 6. 6% for CLTV 75.01% ‐ 90.00% 9% for CLTV < 75% • Investment Properties 2% Gifts • Primary and Second Homes: Acceptable provided Borrower Investment is met. The Borrower Investment is waived when gift funds reduce the LTV/CLTV to <= 80% Reserves • Primary Residence and Second Homes None, unless required by DU/LP • Investment Properties 1‐unit ‐ 2 months PITI required 2‐4 units – 6 months PITI required • Rate & Term Refinance have no reserve requirements unless needed as a compensating factor • Equity Refinances – The cash out may not be used to meet the reserve requirement 20.LIMITATIONS Multiple Loans to the Same Borrower ON OTHER R.E. • Maximum 20% concentration in any one project or subdivision OWNED • Primary Residences Limit of 10 financed properties • Second Homes and Investment Properties Up to a total of 4 financed properties including the subject property or $2 million whichever is less • New multiple loans must be underwritten simultaneously Refer to #15 Underwriting joint or total ownership in a property that is held in the name of a corporation, even if the borrower is the owner of the corporation, is not counted towards the four financed property limit. 21.APPRAISER Current license required REQUIREMENTS 22.APPRAISAL Refer to NSL Underwriting Guidelines 6 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 7. REQUIREMENTS Follow DU recommendation. For properties in Kansas the Form 2075/2070 is not permitted. 23.MORTGAGE • Required on all loans exceeding an 80% LTV INSURANCE • NY State‐ Use the appraised value to determine if mortgage insurance is required. If mortgage insurance is required, use the lesser of the sales price or appraised value to determine the appropriate coverage • Follow MI Coverage per DU/LP Findings or use standard coverage below. MI Coverage (i.e. Reduced or Lower Cost MI) associated with a loan level price adjustment indicated on the DU/LP findings is NOT permitted. • Coverage LTV Coverage 80.01% – 85% 12% 85.01% – 90% 25% 90.01 %– 95% 30% Acceptable BPMI Payment Options • Monthly and Zero Monthly • Level Annual • Standard Annual • Split Premium (with or without options) • Single Premium 24. CONVERSION Current primary must have 30% equity to use rental income, evidenced by appraisal, BPO or AVM. If rental income is being used OF CURRENT must be evidenced by fully executed lease agreement. Evidence security deposit received and deposited into borrowers account. PRIMARY TO If 30% equity cannot be documented rental income cannot be used. 6 months PITI are required for new and current primary RENTAL properties, even when not using rental income. 7 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 8. 25. CONTINUITY Continuity of obligation is required for all refinance transactions and can be established with the following: OF OBLIGATION Outstanding lien: 1. At least one borrower must be an obligor on the existing lien being paid off. 2. Liens in the name of an LLC are eligible if the borrower was an owner of the LLC prior to the LLC acquiring the property. Title must be transferred to borrower and recorded prior to date of application, and may not be transferred back to LLC after funding. If LLC consists of more than one person, provide a statement from all owners verifying any payment due, if applicable. 3. The borrower has been on title and residing in the property for at least 12 months and has either paid the mortgage for the last 12 months as evidenced by cancelled checks or can demonstrate a relationship with the current obligor. 4. The borrower has recently inherited or was legally awarded the property. Transfer of ownership from a corporation to an individual does not meet the continuity of obligation requirement. If the borrower is currently on title but is unable to demonstrate an acceptable continuity of obligation, or there is an outstanding lien against the property, the loan is still eligible but with additional restrictions. The loans must be underwritten and priced as a cash‐out refinance transaction with these additional limits: o No outstanding liens (e.g. purchased for cash or previous mortgage loans have been paid off): o If the property was purchased within the 6 to 12 month period prior to the application date for new financing, the LTV ratios will be based on the lesser of the original sales price/acquisition cost (documented by the HUD‐1 Settlement Statement) or the current appraised value; OR o If the property was purchased more than 12 months prior to the application date for new financing, the current appraised value may be used to calculate the LTV ratios. o If property was purchased within 6 months prior to application date, loan is not eligible for cash out refinance. o Outstanding liens with no continuity of obligation: If the borrower has been on title for at least 6 months but continuity of obligation does not exist, the maximum LTV ratios will be limited to 50 percent based on the current appraised value. 26. RECENTLY Primary Residence R/T transactions: Property must have been taken off the market prior to application and must confirm LISTED their intent to occupy the property PROPERTIES All other occupancies and transactions: Property listed within 6 months of the application date are limited to 70% LTV. 8 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O

- 9. Properties must have been taken off the market prior to application date. 27. PROPERTY o If the property was purchased by the borrower within the 6 months preceding the application for new financing, the OWNERSHIP borrower is ineligible for a cash out transaction. SEASONING o Any new subordinate financing within 6 months of the application date that was not used to purchase the property is REQUIREMENT: considered cash out. o Any refinance of that loan will also be considered cash out. o Requires previous HUD‐1 from any refinance transactions with past 6 months. o If previous transaction was a cash‐out refinance or if it combined a first and non‐purchase money subordinate lien into a new first, the new transaction is to be identified as a cash‐out transaction. 28. DECLINING For Properties located in declining markets, additional guidelines and restrictions may apply see NSL underwriting for MARKET loan eligibility, including MI requirements. 9 North Star Lending 12/03/2008 Operations/NSL Product Guide Fixed Rate I/O