![Aggregate Demand Curve The AD curve shows total demand in an economy, And thus output from households, firms, the government and the international sector at difference price levels. A fall in prices from PL1 toPL2 leads to an increase in real output from Y1 to Y2. Average Price Level P1 P2 AD = C+I+G+[X-M] 0 Y1 Y2 Real Output = National Income = Y C = Consumption I = Investments G = Government Spending X = Exports M = Imports](data:image/gif;base64,R0lGODlhAQABAIAAAAAAAP///yH5BAEAAAAALAAAAAABAAEAAAIBRAA7)

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Ähnlich wie Diagrams for terence

Ähnlich wie Diagrams for terence (20)

Diagrams for terence

- 1. Semester 2 Diagrams Terence Tsui

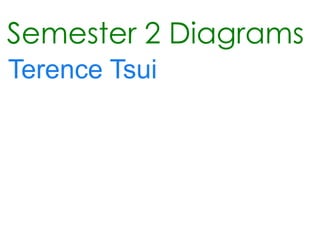

- 2. Aggregate Demand Curve The AD curve shows total demand in an economy, And thus output from households, firms, the government and the international sector at difference price levels. A fall in prices from PL1 toPL2 leads to an increase in real output from Y1 to Y2. Average Price Level P1 P2 AD = C+I+G+[X-M] 0 Y1 Y2 Real Output = National Income = Y C = Consumption I = Investments G = Government Spending X = Exports M = Imports

- 3. Short-Run Aggregate Supply (SRAS) Curve Average Price Level ($) SRAS P2 In the short run, increases in output will normally onlybe achieved in increases in average costs. These are passed onto the consumers through higher prices. So an increase in output from Y1 to Y2 will only be achieved with an increase in prices from P1 to P2. P1 0 Y1 Y2 Real Output (Y)

- 4. Keynesian Long-Run Aggregate Supply Curve LRAS Average Price Level ($) Output maybe increased with no increase in prices, because there is lots of spare capacity in the economy. Spare capacity is being used up and output goes up, but with increases in costs as factors of production cost more Output cannot be increased because all factors are being used. (3) (2) (1) 0 Y1 Real Output (Y)

- 5. Neo-Classical Long Run Average Supply (LRAS) Curve AveragePrice Level ($) Neo-Classical economists believe that the LRAS curve us set by quantity and quality of factors of production in the economy and so it is perfectly inelastic at the full employment level of output (Y1) P2 P1 0 Real Output (Y) Y1

- 6. Short-run Equilibrium Output AveragePrice Level ($) SRAS The economy is in short-run equilibrium where AD equals SRAS and so there will be an output level of Y at a price level of P. P AD 0 Y Real Output (Y)

- 7. Expansionary Demand-Side Policy AveragePrice Level ($) A government may use fiscal and/or monetary policy to shift AD from AD1 to AD2. This would have an effect of expanding the economy from Y1 to Y2, thus increasing employment. However, there will be a “trade-off” as the price level rises from P1 to P2. P2 P1 AD2 AD1 0 Y2 Y1 Real Output (Y)

- 8. LRAS1 LRAS2 The Effect of Supply-Side Policies for Keynesian and Neo-Classical LRAS Curves AveragePrice Level ($) Both Keynesian and Neo-Classical economists believe that an improvement in the quantity and/or quality of factors of production will shift the LRAS curve to the right. P1 P2 0 Real Output (Y) Y2 Y1

- 9. Cost Push Inflation SRAS2 AveragePrice Level ($) SRAS1 P2 When there is an increase in the costs of facts of production such as wage increases in oil prices, then firms’ costs are pushed upwards, the STAS curve shifts from SRAS1 to SRAS2, and the average price level rises from P1 to P2. This is cost-push inflation. Real output also falls from Y1 to Y2. P1 AD 0 Real Output (Y) Y1 Y2

- 10. The Equilibrium Level and the Full Employment Level, of National Income LRAS AveragePrice Level ($) The long-run equilibrium level of national income is where AD is equal to LRAS. The full employment level of national income is where all factors are being employed. Keynesians believe that the two do no necessarily coincide. The equilibrium level is at Y, but the employment level is at Y1. P AD 0 Real Output (Y) Y Y1

- 11. SR Phillips Curve Inflation rate (%) 6 2 NRU 0 SRPC 5 3 Unemployment Rate (%)

- 12. LR Phillips Curve LRPC Inflation rate (%) D E 10 C 6 B SRPC3 SRPC2 2 A 0 3 6 SRPC1 Unemployment Rate(%)

- 13. Perfectly Elastic Supply Price P1 S D1 D2 0 Q1 Q2 Quantity

- 14. An Inelastic Supply Curve Price S P2 P1 D1 D2 0 Q1 Q2 Quantity

- 15. An Elastic Supply Curve Price S P2 P1 D1 D2 0 Q1 Q2 Quantity

- 16. An Perfectly Inelastic Supply Curve Price S P2 P1 D1 D2 0 Q1 Quantity

- 17. Negative Production Externality Price MSC S=MPC=Sum of All Private Costs Negative Externality P1 Welfare loss D= Marginal Private Benefit 0 Q1 Q opt. Quantity

- 18. Negative Consumption Externality Price S=MPC=Sum of All Private Costs P1 Negative Externality Welfare loss D= Marginal Private Benefit MSB 0 Q opt. Q1 Quantity

- 19. Tax and Negative Production Externality Price MSC S=MPC=Sum of All Private Costs Tax P opt P1 Welfare loss D= Marginal Private Benefit 0 Q1 Q opt

- 20. Tax on Producers and Negative Consumption Externality Price Tax S=MPC=Sum of All Private Costs P opt P1 D= Marginal Private Benefit MSB 0 Q1 Q opt Quantity

- 21. Real Wage Unemployment AS L Average (real) wage rage b a W1 We ADL 0 Q1 Q2 Number of Workers

- 22. Demand Deficient Unemployment AS L Average (real) wage rage b a We c W1 ADL ADL1 0 Q1 Qe Number of Workers

Hinweis der Redaktion

- The SRphillips curve shows a trade-off between unemployment and inflation. Unemployment may only be reduced from 5% to 3% at the cost of an increase in the inflation rate from 2% to 6%.

- The LR phillips curve is a neo-classical adaptation and shows that the natural rate of unemployment, here unemployment of 6%, cannot be reduced in the long run using demand-side policies. In the short run, the unemployment rate may be lowered, at the cost of higher inflation (for example A to B), but in the long run, there is a return to the same unemployment rate (for example B to C), but with a higher inflation rate. The only way to reduce the natural rate of unemployment is through supply-side policies.

- If PES is inelastic, it will be difficult for suppliers to react swiftly in changes of price.

- If PES is elastic, supply can react quickly to changes in price

- For example: The chemical firm is polluting the atmosphere as it produces. Thus the cost to society (MSC) is greater than the private cost (MPC). There is a loss of welfare for society as chemicals are overproduced. A negative externality, a cost to third parties, has been created. This is a market failure, as the market does not produce at the socially efficient level of output.

- For example: By consuming air travel there are more flights, and so third parties are affected by increased noise and air pollution. The benefit to the individuals who are flying (MPB) is greater than the benefit to society (MSB). There is a loss of welfare and negative externality has been produced. IN a free market, the level of output is Q1; this is a market failure because the socially efficient level of output Qopt is not acheieved and air travel is over consumed.

- Real wage unemployment occurs when a trade union, or the government, raises the wage rate above the equilibrium, from We to W1. There is unemployment at Q1Q2 where the AS of labour exceeds the AD for labour.

- Demand deficient unemployment occurs when the demand for labour falls from ADL to ADL1, but (real) wages remain at We rather than falling to W1. There is unemployment of Q1Qe.