MULTIPLE CHOICE QUESTIONS ON DIRECT TAXATION

•Als DOCX, PDF herunterladen•

34 gefällt mir•82,562 views

This notes will cover MCQS OF DIRECT TAXATION. MCQS are designed for MBA Students.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie MULTIPLE CHOICE QUESTIONS ON DIRECT TAXATION

Ähnlich wie MULTIPLE CHOICE QUESTIONS ON DIRECT TAXATION (20)

Mehr von Sonal Patil

Mehr von Sonal Patil (6)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

MULTIPLE CHOICE QUESTIONS ON DIRECT TAXATION

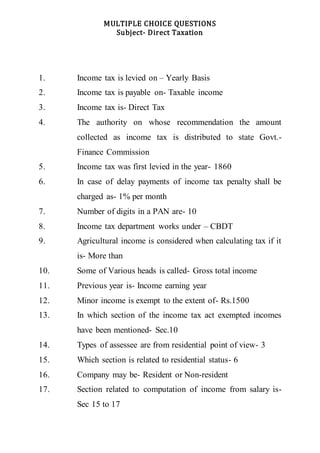

- 1. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 1. Income tax is levied on – Yearly Basis 2. Income tax is payable on- Taxable income 3. Income tax is- Direct Tax 4. The authority on whose recommendation the amount collected as income tax is distributed to state Govt.- Finance Commission 5. Income tax was first levied in the year- 1860 6. In case of delay payments of income tax penalty shall be charged as- 1% per month 7. Number of digits in a PAN are- 10 8. Income tax department works under – CBDT 9. Agricultural income is considered when calculating tax if it is- More than 10. Some of Various heads is called- Gross total income 11. Previous year is- Income earning year 12. Minor income is exempt to the extent of- Rs.1500 13. In which section of the income tax act exempted incomes have been mentioned- Sec.10 14. Types of assessee are from residential point of view- 3 15. Which section is related to residential status- 6 16. Company may be- Resident or Non-resident 17. Section related to computation of income from salary is- Sec 15 to 17

- 2. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 18. Non-monetary allowance includes- Perquisites 19. In HRA, Salary includes- Basic Salary + Commission 20. Entertainment allowance will be deducted from gross salary in case of- Govt. Employee 21. Deduction from salary is allowed under- sec 16 22. Interest credited to RPF is taxable if it is more than- 9.5% 23. Education allowance is exempt for children-2 24. Medical bill reimbursement regarding private hospitals are exempt- up to-15000 25. Deduction allowed against gross salary- professional tax 26. In which section gratuity has been mentioned- sec 10(10) 27. Maximum limit for gratuity is –Rs. 10,00,000 28. Exemption is available for govt. employee at retirement- Gratuity, Statutory P.F, Leave encashment 29. Gratuity received by a govt. employee is fully exempted 30. Property income is exempt for- local authority, Political party, Trade union 31. Annual value is determined under which section of income tax act- Sec 23 32. In case of rental house property only such municipal tax is deducted which is – paid by owner 33. Deduction from annual value is allowed under section- sec 24

- 3. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 34. Standard deduction from annual value is allowed as -30% of AV 35. Interest on loan for self- occupied house taken before 1st 1999 will be allowed up to- Rs 30000 36. Income from house for self- business is Nil 37. An individual assessee can show maximum loss from a self-occupied residential house property – Rs. 150000 38. Give the full name of STT- Security Transaction Tax 39. The rate of Depreciation allowed on machinery is- 15% 40. Section 45 is related to- Capital Gain 41. Capital assets includes-Shares 42. Types of capital gains are-2 43. Indexation will be done on- shares 44. Index no. before31st march,1981 is-100 45. The maximum limit amount of deduction on family pension is- 15000 46. T.D.S is not deducted on lottery income up to – Rs.10000 47. Maximum deduction allowed u/s 80 c- Rs.150000 48. Dedcution in respect of medical insurance premium is allowed under which section- 80 D 49. Maximum deduction allowed for senior citizen under sec 80 D is- 20000

- 4. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 50. Person with disability is allowed a fixed deduction of- 50000. 51. Sale of agricultural land on 1st April, 1970 is an example of transfer of capital asset – True 52. The TDS Certificate issued by an employer to his employees in case of salary income is - Form 16 53. YoungStars, a club, lets out its furnished rooms solely to its members on regular basis. The income earned by the club from such letting-out will be chargeable under the head- Income from Other Sources 54. The rates of Income Tax are specified in- Finance Act 55. The amount of taxable income is to be rounded off to the nearest multiple of Re.1 for income tax calculations.- False 56. Uncommuted pension received by a Government employee is fully exempt from tax – False 57. Interest on capital, borrowed on 10.10.2000, for self-occupied property is deductible upto a maximum amount of – 150000 58. Tax' is imposed on a person by - State Govt. and Central Govt. 59. The first income tax act was introduced in the year – 1860 60. The apex body of Income Tax Department. Is – CBDT 61. The Income Tax Act 1961 came into force on - 13th Sept 1961 62. The rates of income tax are specified in - Finance Act 63. The CBDT consists of- One Chairman & Six Members

- 5. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 64. Assessment year 2006-07 commenced on - 1st April '06 65. The term "Person" includes- A Registered Firm and An Unregistered Firm 66. The taxable Income computed should be rounded off to the nearest multiple of Rs.10.- True 67. House Rent Allowance is exempt from tax – False 68. Expected Rent can be determined in the following way - Higher of Municipal Value & Fair Rent subject to maximum of Standard Rent 69. The amount of interest on borrowed capital allowable as deduction in case of a let out property is - The actual amount of interest 70. The aggregate amount of deductions under chapter VI-A cannot exceed - Gross Total Income 71. For a senior citizen the amount of deduction U/s 80D available is- The actual amount of premium paid or Rs.15,000 whichever is lower 72. If a self-occupied property is converted into HUF property without adequate consideration then- Entire income from such property will be clubbed with the income of the transferor 73. TDS, in case of salary should be deposited within - Within 7 days from the end of the month in which such tax is deducted 74. Income tax is a tax on –Income 75. The Income Tax Act, 1961 has 298 – Sections

- 6. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 76. The ______________ makes the amendment in the form of omissions, insertions and substitutions in the Income Tax Act. – Finance Act 77. The Income Tax Act extends to ______________ of India – Whole India 78. Gross tax liability is calculated on _____________. – Income 79. The term HUF stands for __________. – Hindu Undivided Family 80. Residential has nothing to do with __________. –Nationality 81. AOP is the abbreviation used for __________. Association of Person 82. AOP should consist of __________. – Persons other than individuals also 83. Body of individual should consist of __________. – Individuals only 84. Residential status of an individual depends on the stay of the assesses in India during the – Previous year 85. A person by whom any tax is payable under Income Tax Act 1961 is called __________. – Assessee 86. The financial year in which the income is earned is called as the __________. Previous Year 87. Income Tax Act has _________ schedules. – 14 88. __________ is chargeable u/s 45. - Capital gains

- 7. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 1 Salary Under Section17(1)does not includes : A. Wages B. Pension C. Interest D. Gratuity 2 Taxable Allowance from Salary: A. Conveyance allowance B. Dearness Allowances C. Children education allowance D. Entertainment allowance 3 Sec 22 of Income Tax Act, 1961 does not includes incomeunder the head house property from : A. houses B. buildings C. bungalows D. party plot 4 Capital Gain tax liability arises when following condition getsatisfied: A. There should be a Capital Asset B. There should be a Transfer C. Transfer should be in previous year D. All of the above 5 __________Income is not chargable under Profit/Gainfrom Business/Profession A. Any interest, salary, Bonus, commission or remuneration received by partner of a firm B. Dividend on share C. Income derived by trade/profession D. Income from speculative transaction 6 There are _________types of Capital Assets A. 2 B. 3 C. 1

- 8. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation D. None of the above 7 Long Term Capital Assets (Shares)is held for : A. More than 36 months B. More than 12 months C. More than 24 months D. Not more than 36 months 8 Income from Other Sources includes : A. Dividend B. Duty drawback C. Income from speculative transaction D. All of the above 9 Share of _________ frompartnership firm is exempt u/s 10(2A) A. Interest B. Profit C. Remunaration D. All of the above 10 Interest on Public Provident Fund Investment is _________ A. Taxable under the Head : Income from Other Sources B. Taxable under the Head : Income from Business and Profession C. Allowed as Deduction D. Exempt from Income 11 _________is the Maximum amount of gratuity exempted for Non- Govt. employee not coveredby the payment of Gratuity Act 1972 A. Rs. 5,00,000 B. Rs. 10,00,000 C. Rs. 20,00,000 D. Rs. 25,00,000 12 What is MAT? A. Maximum Alternate Tax B. Maximum Advance Tax C. Minimum Advance Tax D. Minimum Alternate Tax

- 9. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 13 Any sum receivedunder life insurance policy on maturity, including the sum allocatedby wayof bonus on such policy shall be ________from tax. A. Chargable B. Partially Chargable C. Exempt D. None of the Above 14 Transport Allowance is exempt upto : A. Rs. 800 Per Month B. Rs. 1600 Per Month C. Rs. 800 Per Year D. Rs. 1600 Per Year 15 Children Education Allowance is exempt upto Rupees 100 per month per child up to a maximum of ____ children A. 4 B. 3 C. 2 D. 1 16 PAN contains ______Alphabets. A. 5 B. 10 C. 4 D. 6 17 HostelExpenditure Allowance is exempt upto Rs. ____/-per month per child up to a maximum of two children A. 100 B. 1000 C. 500 D. 300 18 Income by way of interest, premium, etc from certain ___________ as specified/ notified in the officialgazette are exempted from tax. A. Securities B. Certificates C. Bonds D. All of the Above

- 10. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 19 What is the Full Form of ITR A. Income Tax Rules B. Income Tax Return C. Income Tax Rectification D. None of the Above 20 In case the income of an individual includes the income of his minor child in terms of sectionof64(1A), such individual shall be entitled to exemption of Rs 1500 in respectof maximum _______ number of minor child A. 1 B. 2 C. No limit D. None of the above 21 Under Sec 80GG, maximum of ________ deductionis allowedto an individual assessee in respectof rent paid by him for an accommodation used for his residential purposes A. Rs. 1600 per month B. Rs. 2000 per month C. Rs. 800 per month D. Rs. 24000 per month 22 The ________ payments/investments qualify for deduction under section80C. A. Donation to Political Party B. Donation to notified temple, mosque, gurudwara, church or other place for renovation and repairs C. Subscription to National Savings Certificates D. All of the Above 23 In which case Deductionu/s. 80 G will be disallowed, If A. Rs. 9999 Paid in Cash B. Rs. 19999 Paid Through Cheque C. Rs. 10001 Paid Through Cheque D. Rs. 10001 Paid Through Cash 24 What is allowable u/s 80 E, in case ofHigher Education Loan A. Principle Amount Only B. Interest Amount Only

- 11. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation C. Interest and Principle Amount D. All of the Above 25 The maximum deduction under sections 80C, 80CCC and80CCD is ___________. A. Rs. 1,00,000 B. Rs. 1,50,000 C. Rs. 2,00,000 D. Rs. 2,50,000 26 Directors Sitting Fees will be Chargeable Under which Head? A. Income From House Property B. Income From Business & Profession C. Income From Capital Gain D. Income From Other Sources 27 Deduction In RespectofMedicalInsurance Premia Sec 80D is not allowedin respectof payment made for A. Own/spouse B. Parents of the assessee(dependent) C. Parents of the assessee(independent) D. None of the above 28 Deduction In RespectofDependent Relative Section80 DD is available to __________. A. Individuals and HUF, who is resident in India B. Individuals , who is resident in India C. Individuals and HUF, who is resident or non resident in India D. Individuals , who is resident or non resident in India 29 Donations made to following are eligible for 100% deduction without any qualifying limit A. Prime Minister’s National Relief Fund B. National Defense Fund C. Prime Minister’s Armenia Earthquake Relief Fund D. All of the above 30 Donations to the following are eligible for 100%deduction subject to qualifying limit (i.e. 10% of adjusted gross totalincome).

- 12. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation A. Donations to the Government or a local authority for the purposeof promoting family planning B. Donation to the Government or any local authority to be utilized by them for any charitable purposes other than the purposeof promoting family planning C. Any authority set up for providing housing accommodation or for town planning D. All of the above 31 Legally valid Digital Signature Certificates are issuedthrough A. NSDl / CDSL B. State Govt. C. licensed Certifying Authorities (CA), such as eMudhra D. All of the above 32 Where canI use DigitalSignature Certificates? A. For sending and receiving digitally signed and encrypted emails B. In e-Tendering or e-Procurement C. For signing documents like MSWord, MS Excel and PDFs D. All of the above 33 Expand the Term 'CA' with reference to the DigitalSignature : A. Chartered Accountant B. CostAccountant C. Certificate of Approval D. Certification Authority 34 What are the different classes ofDigitalSignature Certificates ? A. Class 0 Certificate B. Class 1 Certificate C. Class 2 Certificate D. All of the above 35 An Individual should have a valid _______for registering with the e-Filing application A. TAN B. PAN C. Aadhar D. None of the above

- 13. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation 36 For Registering with e-Filling application ___________is mandatory. A. First Name B. Middle Name C. Surname D. All of the above 37 For Registering with e-Filling application their are ___________no of Secret Questions. A. 1 B. 2 C. 3 D. No limit 38 While Registering with e-Filling application, for Non-ResidentIndian, __________is exempted. A. PAN B. Mobile PIN C. Current Address D. None of the Above 39 e-Filing of Returns/Forms is mandatory if the Totalincome exceeds__________ rupees A. 1 lakh B. 5 lakh C. Basic Exemption Limit D. None of the Above 40 A company and an assesseebeing individual or HUF who is liable to audit u/s 44AB are required to furnish Form BB (Return of NetWealth) _______________. A. Electronically under digital signature B. Electronically without digital signature C. Manually D. None of the Above 41 For e-Filling of ITR, _______file is uploaded. A. .xls B. .xml C. .pdf

- 14. MULTIPLE CHOICE QUESTIONS Subject- Direct Taxation D. .doc