1. Srisawad

Power1979 (SAWAD:TB)

Business Description

Srisawad Power 1979 Public Company Limited is a Thailand-based company engaging in financial services. The

company operates two business segments: hire purchase and loans. SAWAD also offers a wide range of hire

purchase financing and secured loans for houses, land, personal and commercial vehicles, motorcycles,

international labors, agricultural machinery and equipment, hire purchase of new cars, and unsecured personal

loans for retail customers in Bangkok and its surrounding areas as well as upcountry provinces, including

Ratchaburi, Suphanburi, Lopburi, Chonburi, Saraburi and Ayutthaya. Its operation process include provision of

credits, follow-up overdue payment, installment payment plans and asset management service.

The Company’s subsidiaries comprise Fast Money Company Limited, and Srisawad Asset Management

Company Limited.

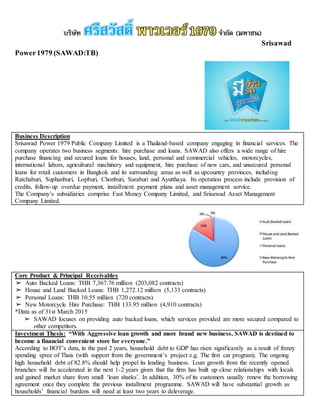

Core Product & Principal Receivables

➢ Auto Backed Loans: THB 7,367.76 million (203,082 contracts)

➢ House and Land Backed Loans: THB 1,272.12 million (5,133 contracts)

➢ Personal Loans: THB 10.55 million (720 contracts)

➢ New Motorcycle Hire Purchase: THB 133.95 million (4,910 contracts)

*Data as of 31st March 2015

➢ SAWAD focuses on providing auto backed loans, which services provided are more secured compared to

other competitors.

Investment Thesis: “With Aggressive loan growth and more brand new business, SAWAD is destined to

become a financial convenient store for everyone.”

According to BOT’s data, in the past 2 years, household debt to GDP has risen significantly as a result of frenzy

spending spree of Thais (with support from the government’s project e.g. The first car program). The ongoing

high household debt of 82.8% should help propel its lending business. Loan growth from the recently opened

branches will be accelerated in the next 1-2 years given that the firm has built up close relationships with locals

and gained market share from small ‘loan sharks’. In addition, 30% of its customers usually renew the borrowing

agreement once they complete the previous installment programme. SAWAD will have substantial growth as

households’ financial burdens will need at least two years to deleverage.

2. SAWAD also has a competitive advantage due to its coverage network that is larger than its peers. The faster the

company can secure locations for new branches, the better its market position in underpenetrated areas.

Furthermore, there is no product differentiation in vehicle-pledging loans, but what can attract customers is a fast

approval process and strong presence in the area. In addition, the company has set ambitious long-term ROE

targets of 33-35% per year during 2015-2017, hence the profit growth thus experienced double digit profit

growth by 49 per cent at the end of 2015 1st quarter. It tends to focus on providing loan-loss reserves (with 62%

of NPLs) with well managed asset quality and new business from debt collection services and Nanofinance. With

strong loan growth largely branch expansion and new business in Nanofinance for SME and debt collection

business, SAWAD surely will become a financial convenient store where they can get any financial product

suited their needs with lightning speed.

Key Thesis Points:

➢ Ambitious ROE target of 30-35%, propelled by high loan growth - deriving key earnings drivers

❖ The company's leaders set their loan growth target of 20-30% during 2015-2017, driven by aggressive

lending in the bank's untapped market. According to the National Statistical Office (NSO) : 25 million

members of the workforce were "out of system" (not on a payroll or drawing a fixed salary) - expecting

its 2015 loan growth to reach 20%. Targeting low-income clients (those difficult to receive loans from

large banks)

➢ Nanofinance and debt collection services to support growth in 2015

❖ Management has set its lending budget at THB 500m for this project and it will commence in 2015 3rd

quarter. Its potential clients will be buyers (franchisees) of local franchise brand names, such as Jiang

Fish Ball, Kieng Empire, Hong Kong Noodles, and Joke Bangkok.

❖ Moreover, the company will diversify into distressed asset management, wet market loans and debt

collection services through its subsidiary (SWP). The company has set a budget of THB 1bn for these

new ventures.

*SWP bought THB 200m of NPLs during 2nd quarter of 2015 at the discount rate of more than 20 per

cent from face value.

❖ The company has already signed contracts with Toyota Leasing (Thailand) Co.,Ltd., Nissan Leasing

(Thailand) Co.,Ltd. and SME Bank to offer debt collection services. The company will receive fee

income on a fixed rate or revenue-sharing basis, depending on the agreement with those financial

institutions. The firm is also negotiating with other large commercial banks to offer debt collection

services. This new business will boost bottom line because SAWAD can utilise its wide branch network

coverage and effective in-house debt collection department to deliver services to clients. The management

expected revenue contribution from this business to be 15-20% of total revenue within 5 years.

❖ According to Asean Confidential, an FT research service on South East Asia, Thai household debt will

approach or exceed 100 per cent of GDP by 2020 under likely macroeconomic scenarios – and this does

not include large amounts of borrowing from illegal money lenders by the poorest Thais.

➢ Branch Expansion - Financial Convenience Store (Largest branch network among its peers)

❖ SAWAD plans to raise its branch network to 1,300 offices in 2015 and 1,500 offices in 2016 from 1,059

offices in 2014. The company also plan to expand its business overseas.

❖ Branch expansion will increase debt collection efficiency and also boost company’s loan growth.

➢ Plan to launch bonds of THB 2.5bn in late 2015 3rd Quarter to boost expansion

❖ The company plan to launch THB 2.5bn of bonds in 2015 to support the firm's rapid expansion outlook.

The increase in number of branches could allow the firm to boost its lending as well as its efficiency in

debt collection.

❖ SAWAD came up with a low net-D/E ratio of 1.7x at end of March 2015. The new borrowing will bring

its D/E ratio up to 2.4x, which is far below than the Bank sector’s mean of 10x. This implies how

SAWAD could leverage its D/E ratio for aggressive expansion for the next couple of years without a cash

call. For now SAWAD are free of concerning about its financial positions for this year and next.

Risk Analysis:

➢ High NPL ratio compared with consumer finance peers

❖ SAWAD’s NPL Ratio is the highest among its consumer finance peers, because some clients have

income streams on a quarterly or half-yearly basis. However, We believe that its low loan-to-value at 30-

3. 70% and high interest rate charged cover any default risks, which therefore results in an impressive bad

debt recovery rate of 50% in the first year after customers go into default.

➢ Sale of repossessed vehicles

❖ SAWAD resells repossessed vehicles through its local branches instead of outsourcing to third parties.

We think that the risk of carrying high foreclosed collaterals is manageable because SAWAD has

experience in the used-vehicles markets. Its strategy is to resell repossessed vehicles as soon as possible

to ensure good recovery.

➢ Dependance on senior management

❖ Major shareholders and management has a strong background in the vehicle pledging loan business in the

vehicle-pledging loan business in the provincial markets.

➢ Provisions charged remain high which are in line with SAWAD’s larger portfolio. However, we believe

that its effective in-house debt collection unit will mitigate rising NPL amid high household debt

Tailwinds:

➢ Specialise in offering personal and small loans

➢ Government support for Nano-finance license

commencement

➢ More NPL (as Bank’s NPL has risen) and Bad

Debt portfolio to be collected

➢ New business development: debt collection & bad

debt management

➢ Possible M&A with local operators

Headwinds:

➢ Sluggish domestic economy

➢ Competition within Thai economy despite in the

past and future

➢ Aggressive expansion of its rivals

➢ Strong presence of local operators

➢ Regulatory changes in the future about leasing

business i.e. more restriction

Important Data Points:

➢ Market Cap: THB 40289.92 M

➢ Growth rate YoY (Q1/2015) : Revenue +39.12% Earning +49.18%

➢ ROE 31.8% Vs. Industry’s ROE 12%

➢ % shares held by Major shareholders: 55.52% Kaewbootta family

➢ % shares held by Institutional Investors : 6.63%

➢ Awarded Nanofinance licenses from the Ministry of Finance in May 2015. The company planned to offer

nanofinance loans for THB 500M due to high risk nature of the loan.

➢ Strong performance compared to Financial Industry and SET (Characteristic of Leader)

4. Valuation

According to our forecast model and Professor Aswath Damodaran’s Two-Stage growth discount model, the

target price of SAWAD will be THB 48.17 per share. It implies an upside ~20%. Hence, we would like to give a

“Buy” rating with target price THB 48 per share.

Moreover, as of Jun 26, 2015, the consensus forecast (since August 2014) amongst 7 polled investment analysts

covering SAWAD advises that the company will outperform the market.

Previous consensus forecast advised investors to hold their position for SAWAD.

Recommendation : BUY

Price Target : THB 48 (+23.8%) as of 07/06/2015