MDIA and HVCC Timing Impacts

•

0 gefällt mir•1,068 views

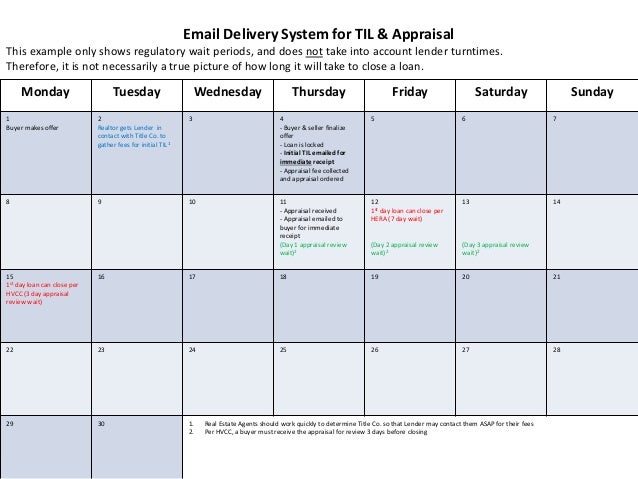

To help you visualize how MDIA and HVCC will affect a typical closing see the slides below. I've included a few calendars to help illustrate various scenarios you may encounter, including email vs. mail delivery system, and how redisclosing the TIL affects the closing date.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Empfohlen

Empfohlen (20)

MDIA and HVCC Timing Impacts

- 1. Monday Tuesday Wednesday Thursday Friday Saturday Sunday 1 Buyer makes offer 2 Realtor gets Lender in contact with Title Co. to gather fees for initial TIL1 3 4 - Buyer & seller finalize offer - Loan is locked - Initial TIL emailed for immediate receipt - Appraisal fee collected and appraisal ordered 5 6 7 8 9 10 11 - Appraisal received - Appraisal emailed to buyer for immediate receipt (Day 1 appraisal review wait)2 12 1st day loan can close per HERA (7 day wait) (Day 2 appraisal review wait)2 13 (Day 3 appraisal review wait)2 14 15 1st day loan can close per HVCC (3 day appraisal review wait) 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 1. Real Estate Agents should work quickly to determine Title Co. so that Lender may contact them ASAP for their fees 2. Per HVCC, a buyer must receive the appraisal for review 3 days before closing Email Delivery System for TIL & Appraisal This example only shows regulatory wait periods, and does not take into account lender turntimes. Therefore, it is not necessarily a true picture of how long it will take to close a loan.

- 2. Email Delivery System for TIL & Appraisal (with TIL redisclosure delay) This example only shows regulatory wait periods, and does not take into account lender turntimes. Therefore, it is not necessarily a true picture of how long it will take to close a loan. Monday Tuesday Wednesday Thursday Friday Saturday Sunday 1 Buyer makes offer 2 Realtor gets Lender in contact with Title Co. to gather fees for initial TIL1 3 4 - Buyer & seller finalize offer - Loan is locked - Initial TIL emailed for immediate receipt - Appraisal fee collected and appraisal ordered 5 6 7 8 9 10 11 -Appraisal received and value is below sales price - Appraisal emailed to buyer for immediate receipt (Day 1 appraisal review wait)2 12 1st day loan can close per HERA (7 day wait) (Day 2 appraisal review wait)2 13 (Day 3 appraisal review wait)2 14 15 1st day loan can close per HVCC (3 day appraisal review wait) -Sales price renegotiated and loan amount lowered - Redisclose TIL via email for immediate receipt 3 (Day 1 TIL review wait)2 16 (Day 2 TIL review wait)2 17 (Day 3 TIL review wait)2 18 1st day loan can close per HERA’s APR redisclosure period (3 day review wait) 19 20 21 22 23 24 25 26 27 28 29 30 1. Real Estate Agents should work quickly to determine Title Co. so that Lender may contact them ASAP for their fees 2. Per HVCC and HERA, a buyer must receive the appraisal and redisclosed TIL for review 3 days before closing 3. Change in loan amount triggered TIL redisclosure. Other changes that will trigger a TIL redisclosure, and delay closing are: 1. Change in interest rate

- 3. Mail Delivery System for TIL & Appraisal This example only shows regulatory wait periods, and does not take into account lender turntimes. Therefore, it is not necessarily a true picture of how long it will take to close a loan. Monday Tuesday Wednesday Thursday Friday Saturday Sunday 1 Buyer makes offer 2 Realtor gets Lender in contact with Title Co. to gather fees for initial TIL 1 3 4 - Buyer & seller finalize offer - Loan is locked - Loan application & disclosures emailed to buyer 5 6 7 8 -Buyer returns loan application & disclosures - Lender submits file to investor - Investor mails initial TIL to buyer 9 (Day 1 TIL mail wait) 2 10 (Day 2 TIL mail wait) 2 11 (Day 3 TIL mail wait) 2 12 Appraisal fees collected & appraisal ordered 13 14 15 16 1st day loan can close per HERA (7 day wait) 17 18 19 Appraisal received & mailed to buyer 20 (Day 1 appraisal mail wait)2 21 22 (Day 2 appraisal mail wait)2 23 (Day 3 appraisal mail wait)2 (Day 1 appraisal review wait)3 24 (Day 2 appraisal review wait)3 25 (Day 3 appraisal review wait)3 26 1st day loan can close per HVCC (3 day appraisal review wait) 27 28 29 30 1. Real Estate Agents should work quickly to determine Title Co. so that Lender may contact them ASAP for their fees 2. It is assumed the buyer receives TIL and/or appraisal 3 days after mailing 3. Per HVCC, a buyer must receive the appraisal for review 3 days before closing

- 4. Mail Delivery System for TIL & Appraisal (with TIL redisclosure delay) This example only shows regulatory wait periods, and does not take into account lender turntimes. Therefore, it is not necessarily a true picture of how long it will take to close a loan. Monday Tuesday Wednesday Thursday Friday Saturday Sunday 1 Buyer makes offer 2 Realtor gets Lender in contact with Title Co. to gather fees for initial TIL 1 3 4 - Buyer & seller finalize offer - Loan is locked - Loan application & disclosures emailed to buyer 5 6 7 8 -Buyer returns loan application & disclosures - Lender submits file to investor - Investor mails initial TIL to buyer 9 (Day 1 TIL mail wait) 2 10 (Day 2 TIL mail wait) 2 11 (Day 3 TIL mail wait) 2 12 Appraisal fees collected & appraisal ordered 13 14 15 16 1st day loan can close per HERA (7 day wait) 17 18 19 -Appraisal received and value is below sales price - Appraisal mailed to buyer 20 (Day 1 appraisal mail wait)2 21 22 (Day 2 appraisal mail wait)2 23 (Day 3 appraisal mail wait)2 (Day 1 appraisal review wait) 3 -Sales price renegotiated and loan amount lowered - Redisclose TIL via mail4 24 (Day 2 appraisal review wait) 3 (Day 1 TIL mail wait)2 25 (Day 3 appraisal review wait) 3 (Day 2 TIL mail wait)2 26 1st day loan can close per HVCC (3 day review wait) (Day 3 TIL mail wait)2 (Day 1 TIL review wait) 3 27 (Day 2 TIL review wait)3 28 29 (Day 3 TIL review wait)3 30 1st day loan can close per HERA’s APR redisclosure period (3 day review wait) 1. Real Estate Agents should work quickly to determine Title Co. so that Lender may contact them ASAP for their fees 2. It is assumed the buyer receives TIL and/or appraisal 3 days after mailing 3. Per HVCC and HERA, a buyer must receive the appraisal and redisclosed TIL for review 3 days before closing 4. Change in loan amount triggered TIL redisclosure. Other changes that will trigger a TIL redisclosure, and delay closing are: 1. Change in interest rate 2. Change in mortgage product (30 yr vs. 15 yr)