1. The China Analyst

Now online at

www.thebeijingaxis.com/tca

A knowledge tool by The Beijing Axis for executives with a China agenda September 2011

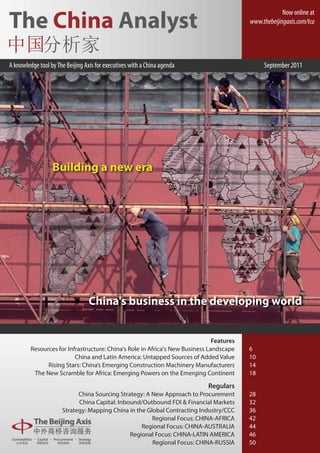

Building a new era

China's business in the developing world

Features

Resources for Infrastructure: China's Role in Africa's New Business Landscape 6

China and Latin America: Untapped Sources of Added Value 10

Rising Stars: China’s Emerging Construction Machinery Manufacturers 14

The New Scramble for Africa: Emerging Powers on the Emerging Continent 18

Regulars

China Sourcing Strategy: A New Approach to Procurement 28

China Capital: Inbound/Outbound FDI & Financial Markets 32

Strategy: Mapping China in the Global Contracting Industry/CCC 36

Regional Focus: CHINA-AFRICA 42

Regional Focus: CHINA-AUSTRALIA 44

Regional Focus: CHINA-LATIN AMERICA 46

Regional Focus: CHINA-RUSSIA 50

2.

3. Tanzania National Stadium Modern Sports Stadium

Dar es Salaam, Tanzania Ndola, Zambia

Capacity: 60,000 people Capacity: 40,000 people

Completed in 2007 Construction to commence in 2011

EMBLEMS OF A NEW ERA

Sheraton Hotel & Towers Dakar Grand Theatre

Oran, Algeria Dakar, Senegal

The first Sheraton hotel in Algeria Covers two hectares; capacity of 1,800 people

Completed in 2002 Completed in 2011

Notable Chinese Construction Projects in Africa

Lom Pangar Hydropower Project African Union Conference Centre

Cameroon Addis Ababa, Ethiopia

Includes 30-megawatt power station Covers a floor area of 51,887 square metres

Construction to commence soon Under construction

4. The China Analyst The Beijing Axis 中外商桥

At the Highest Level

Reflecting on the momentous events happening in the world right now and in the last few turbulent

years, it is clear that the world is changing significantly. China is a big part of this change; in fact, its emer-

gence has become instrumental to a new era that is affecting every region of the world, yet none more

so than the developing world. China is bringing unprecedented change to Latin America and Africa, and

a changing business landscape brings new opportunities.

In the last edition of The China Of course this edition also features all the usual sections on

Analyst, we looked at the changing China's trade and investment, procurement, and regional busi-

business landscape within China, ness. And I am also pleased to announce the launching of a

focusing on certain key industries new website dedicated to The China Analyst, at www.thebeijin-

and outlining the opportunities gaxis.com/tca, where the contents of this and previous editions

that can still be found for foreign can be found in an interactive online format.

companies. In this edition, we shift

our focus to China's impact on the I trust our readers will enjoy this edition of The China Analyst,

wider world, and especially on and as always we welcome your feedback.

the regions where China's pres-

ence and influence have been Kobus van der Wath

strongest, namely the developing Founder & Group Managing Director, The Beijing Axis

world. kobus@thebeijingaxis.com

Africa and Latin America have experienced the most signifi- The China Analyst - September 2011

cant impact of China's newfound engagement with the

developing world, an impact which the cover of this maga- Published by The Beijing Axis

zine has boldly dubbed 'a new era'. China's expanding reach

3806 Central Plaza

is having a profound impact on Africa. Here, China's brand

of state-led capitalism is serving to breach a heritage of risk 18 Harbour Road

aversion by foreign investors, and in doing so, contribute to Wanchai

economic growth in many parts of the continent. As our first Hong Kong, PRC

lead feature illustrates, by means of an essential exchange of

resources for infrastructure, China is playing a crucial role in Tel: +86 (0)10 6440 2106

a new construction boom on the continent. Fax: +86 (0)10 6440 2672

www.thebeijingaxis.com

With a rapidly growing trade and investment relationship

Executive Editor Kobus van der Wath

in recent years, China's business with Latin America has to a

large extent been characterised by an exchange of resources kobus@thebeijingaxis.com

for manufactured goods. Yet as our second lead feature envi- Editor Barry van Wyk

sions, the relationship is now set to enter a new phase of barryvanwyk@thebeijingaxis.com

higher value added investment and trade, with wide impli-

cations for Latin America. Editorial Board Lilian Luca

luca@thebeijingaxis.com

China is not the only new player in these developing regions, Cheryl Tang

however. In our fourth lead feature we outline the trade and cheryl@thebeijingaxis.com

investment activities in Africa of the other BRICS nations,

revealing how the likes of India and Brazil are in their own Javier Cuñat

ways contributing to the shaping of Africa's new business javiercunat@thebeijingaxis.com

landscape.

Dirk Kotze

dirk@thebeijingaxis.com

With the business that these emerging nations, and espe-

cially China, are doing in the developing world, the landscape To view the contents of previous editions of The China Analyst, see Previ-

in regions such as Africa and Latin America is changing, and ous Editions on page 55. To subscribe free of charge to The China Analyst,

please visit www.thebeijingaxis.com or www.thebeijingaxis.com/tca.

opportunities for businesses are doing likewise. This edition

of The China Analyst is also about these changes and oppor- For advertising opportunities, please contact Haiwei Huang at

tunities, and about how China's business in the developing haiweihuang@thebeijingaxis.com.

world is indeed building a new era.

4 The Beijing Axis

5. Table of Contents

September 2011

6 FEATURES Resources for Infrastructure: China's Role in Africa's New Business Landscape

Chinese companies active in Africa are reshaping the continent’s business landscape, yet at its core the rela-

tionship rests on one simple although vital exchange.

10 FEATURES China and Latin America: Untapped Sources of Added Value

Trade and investment between China and Latin America have increased ten-fold in the last decade, yet the

two regions are now set to enter a new higher value added stage of their relationship.

14 FEATURES Rising Stars: China’s Emerging Construction Machinery Manufacturers

China's three largest construction machinery manufacturers, XCMG, Sany and Zoomlion, have been success-

ful in emerging markets and are aiming to catch up with global leaders in the industry. How did they do it?

18 FEATURES The New Scramble for Africa: Emerging Powers on the Emerging Continent

Led by China, the BRICS nations are at the forefront of a new scramble for projects and deals in Africa. Yet

apart from China, how are the other four BRICS doing in this new scramble on the continent?

22 MACROECONOMY Macroeconomic Monitor: Chinese Inflation - One of the Biggest Fears of 2011

With inflation having reached 6.5% in July 2011, this edition looks at the Chinese government’s monetary and

fiscal policy options to fight a scourge for which China's central planners have a legendary fear.

24 NEWS China Business News Highlights

Recent headline business stories in China, leading with the business deals following foreign trips by China’s

leaders, China's power shortage in H1 2011, and China's latest construction marvels.

26 TRADE China Trade Roundup

A review of China’s trade performance in Jan-Aug 2011, and an overview of China's trade in services.

28 PROCUREMENT China Sourcing Strategy: A New Approach to Procurement

China procurement is changing, and procurement managers need to adapt to a new opportunity landscape.

32 INVESTMENT China Capital: Inbound/Outbound FDI & Financial Markets

Analysis on the latest on FDI in China and OFDI by Chinese firms, and a review of China's OFDI approval processes.

36 STRATEGY Mapping China in the Global Contracting Industry

In this edition we illustrate the presence of China's contractors in different markets of the world.

38 STRATEGY CCC: China Inc.'s Leading EPC Contractor

A closer look at the corporate strategy of arguably China's most internationalised contractor.

41 REGIONS Regional Overview: BRIICS

A macro overview of the leading developing economies: Brazil, Russia, India, Indonesia, China and South Africa.

42 REGIONS Regional Focus CHINA-AFRICA

China-Africa trade and investment analysis, and the series 'Chinese Contractors in Africa', featuring CCECC.

44 REGIONS Regional Focus CHINA-AUSTRALIA

China-Australia trade and investment analysis, and the series 'Australia State Watch', featuring Victoria.

46 REGIONS Regional Focus CHINA-LATIN AMERICA

China-Latin America trade and investment analysis, and an interview with the Mexican Ambassador to China,

Jorge Guajardo.

50 REGIONS Regional Focus CHINA-RUSSIA

China-Russia trade and investment analysis, including the series 'China-Russia Resources Watch'.

52 The Beijing Axis News - March-September 2011

The latest The Beijing Axis Group news.

54 EVENTS Upcoming Events

A selection of upcoming China and global events focusing on the mining and engineering sectors.

Back About The Beijing Axis

page Company profile and contact information.

6. The China Analyst Features 专题

Resources for Infrastructure: China's Role in Africa’s

New Business Landscape

Chinese companies active in Africa are reshaping the continent’s business landscape as part of a complex

partnership that has reignited and vastly expanded ties from a previous era. China’s ways of doing busi-

ness in Africa today is different from all those of yesteryear, yet the broad engagement can be under-

stood through the prism of one vital exchange: Resources for infrastructure. By Barry van Wyk

I

n the 1970s, China’s financing and construction of a 1,870 customers inland are on average 50% higher than the costs

km-long railway giving landlocked Zambia access to the of shipping costs in other low-income developing regions.

Tanzanian port of Dar es Salaam was a monument to

Chinese engagement and solidarity with Africa in a previous Yet now a new China with vastly different priorities and stra-

era. In a flush of post-colonial exuberance, Africa was under- tegic outlook is back in Africa, where it is instrumental in

going a construction boom. Drawing on colonial-era plans, Africa’s new construction boom that is reshaping the busi-

various schools, hospitals and roads were being built in ness landscape on the continent. In contrast to its piecemeal

Ghana, for example, and in the Democratic Republic of Congo interaction with African countries in previous decades, China

(then Zaire), the Inga hydroelectric project was completed in is now comprehensively engaged with almost all of Africa’s 54

1977 at a cost of USD 260 million, while a 1,100 mile power countries – lending money, providing aid, trading, investing,

line to Katanga also saw the light of day. and more than all else: building infrastructure and extracting

resources. This over-simplified description of China’s business

Yet when the Katanga line was eventually completed in 1982 in Africa goes to the heart of how Africa’s business landscape

at a cost of USD 1 billion, it was four times over the original is changing under the influence of a new superpower hungry

budget. Only 18% of Inga’s hydroelectric capacity and 20% for natural resources and well-suited to provide Africa with

of the capacity of the new power lines were ever used, and something it is sorely in need of: infrastructure.

the sharp fall in the price of cocoa in 1961 put paid to Kwame

Nkrumah’s construction projects in Ghana. Designed to carry Levels of engagement: Trade and investment

five million metric tonnes of cargo annually, with a lack of new

investment, mounting debt, poor management and mainte- The China that built the railway in Africa in the 1970s is a

nance, moreover, Zambia’s new railway never carried more distant shadow of the China of today that routinely builds

than 300,000. From being a symbol of a new era of Africa’s railways, roads, ports and other infrastructure in various parts

development, this railway – badly managed and insufficiently of the world. In the 2000s, as the size of China’s economy in

maintained – became emblematic of Africa’s lost construc- quick succession surpassed that of Italy, France, the UK, and

tion boom turned to protracted bust. Germany, China’s energy consumption expanded four times

faster than expected to 16% of global demand in 2006. While

Instead of a boom of new steel and concrete, Africa expe- China’s GDP expanded at an annual rate of 10% over 2000-

rienced decades of lost growth. In 2008, the World Bank1 2008, its annual demand for industrial raw materials such as

estimted that access to the most basic services in Africa steel (16%), aluminium (20%), copper (13%) and nickel (23%)

increased only modestly between the early 1990s and the all grew even faster. In the ten years preceding 2008, China’s

early 2000s, and only slightly in the last decade. Electricity, consumption of crude oil nearly doubled, and during the

for example, is still available to little more than 20% of Africa’s same period its consumption of copper and iron ore tripled

total population, and piped water to just 12%. while that of aluminium quadrupled. Between 2000 and

2008, China accounted for two-thirds of the world’s entire

Compounding the problem was the fact that Africa was growth in demand for steel and aluminium and virtually all

largely left to its own devices in terms of infrastructure in the growth in global demand for copper and nickel.

1990s when both African and donor investment in infrastruc-

ture was scaled back relative to other priorities such as child This rapid growth in China’s natural resource use contrib-

immunisation and education, partly due to the mistaken uted to a windfall in trade between China and Africa, a major

belief that private investors would step up to fill the infra- supplier of raw materials. Bilateral trade stood at just over

structure financing gap. As a result, while Africa’s construc- USD 10 billion in 2000, yet in 2010 it breached USD 125 billion,

tion sector deteriorated, poor road, rail and harbour infra- exceeding Africa’s trade with any other partner, the closest

structure added 30-40% to the costs of goods traded among ones being the US with around USD 115 billion, France with

African countries, and the costs of moving foreign imports to around USD 66 billion, and the UK with around USD 31 billion

(see chart on next page). This China-Africa trade pattern basi-

1 See ‘Access, Affordability and Alternatives: Modern Infrastructure Services

in Africa', Africa Infrastructure Country Diagnostic. The International Bank cally encompasses an exchange of a diverse range of Chinese

for Reconstruction and Development, World Bank, Feb. 2008 manufactured goods for African raw materials.

6 The Beijing Axis

7. Features

Features 专题 The China Analyst

Africa's Major Trade Partners (USD bn, 2000-10) Major Investors in Africa OFDI Flow (USD bn, 2003-09)

China UK US France

150 France

120

2003

US

2004

90

2005

2006

60 UK

2007

2008

30

2009

China

0

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 0 5 10 15 20

Source: UN Comtrade; The Beijing Axis Analysis Source: OECD Statistical Database; China National Bureau of Stistics; The Beijing Axis Analysis

Along with the US and emerging economies such as Brazil • Export credits to support national exporters. In 2009,

and India, China’s imports from Africa are as expected char- China disbursed USD 29.6 billion in export credit

acterised by a disproportionate share of oil and minerals. globally

China’s trade with Africa has as a result been very lucra- • Natural resources-backed lines of credit, or the ‘Angola

tive for resource-rich African countries, and these African Mode’, where China’s Exim Bank uses natural resource

commodity suppliers have become crucial suppliers for exports or preferential access to them as collateral for

China. South Africa is China’s only African trade partner from infrastructure projects and as a means to repay loans

which it imports substantial amounts of products that are • Mixed credits, where financing packages combine

not resources, while China’s leading suppliers of oil (Angola), concessional and market rate loans, such as a mixture

Manganese (South Africa), chromium (South Africa), cobalt of FDI and export credit3

(the DRC), and platinum (South Africa) are all African.

Laying down a methodology: The Angola Mode

China's annual flow of Outbound Foreign Direct Investment

(OFDI) to Africa in recent years is still far in arrears of the US, As China’s engagement with Africa has deepened during the

France and the UK (see chart above, right). In 2009, China’s last decade, its deals on the continent came to broadly fit a

OFDI stock in Africa reached USD 9.3 billion, still marginally mould. As a country that recently emerged from civil war yet

behind that of Switzerland, the Netherlands and far behind that is rich in natural resources and sorely in need of infra-

the US, France and the UK (which has the most invested stock structural renewal, Angola has become one of the biggest

in Africa, namely USD 61.4 billion). Chinese investment in recipients of Chinese financing for infrastructure projects in

Africa reflects a similar predilection for resource-rich coun- Africa, one of China’s largest trading partners on the conti-

tries as is the case with trade, and in 2009 a full 76% of Chinese nent, and a major source of its oil. In 2004 Angola signed a

FDI in Africa was concentrated in resource-rich countries. In deal with China that would become emblematic of China’s

2009, the main sectors for Chinese OFDI stock in Africa were ‘infrastructure for resources’ relationship with Africa.

mining (30%), manufacturing (22%), and construction (16%).

Angola received a USD 2 billion loan from a Chinese policy

Yet while Chinese levels of OFDI in Africa still lag far behind bank, China EximBank, for the development of infrastructure,

those of Western countries, China and other emerging part- including electricity generation, telecom expansion, railway

ners are following new paths of investing in Africa. Europe rehabilitation and water. As part of the repayment terms for

and North America have typically relied on FDI and Official the loan, Angola agreed to supply China with 10,000 barrels

Development Assistance (ODA) in Africa, but emerging of oil per day. In a pattern that would be repeated frequently

powers such as China are adopting a more holistic approach afterwards, a Chinese construction/engineering company

to broaden their economic relationship with Africa that was awarded contracts for the infrastructure projects, while

combines trade and investment with development coop- rights for extracting natural resources was afforded to a

eration. Thus while developing partners such as China, Chinese oil company.

India, South Korea and Brazil are not only engaging with

African countries that Western countries have avoided in the 3 Deborah Brautigam, author of ‘The Dragon’s Gift,’ has put China’s total

past, they are also increasingly using alternative financing purely concessional loans, zero-interest loans and grant commitments to

methods. China in particular uses the following financing Africa at USD 2.1 billion in 2009, while she estimated China’s preferential

export credit commitments to Africa for 2007-09 at around USD 2 billion

methods in Africa2: and non-concessional finance at around USD 5 billion annually. In sum, all

2 For more detail see ‘African Economic Outlook 2011’, ADB, OECD, UNDP, China’s alternative financial flows to Africa reached an annual average com-

UNECA, 2011, p. 112. mitment of USD 7.1 billion over 2007-09.

The Beijing Axis 7

8. The China Analyst Features 专题

International Contract Revenue in Africa, China's and Rest Chinese contractors have become highly competitive

of World's Share (USD mn, 2001-09) bidders for publicly tendered infrastructure projects. A 2007

2001 7.4% 92.6% survey of 35 Chinese construction companies active in Africa

found that around 50% of Chinese projects in Africa were

2002 9.9% 90.1% actually won via an international bidding process. The extent

China of Chinese contractors success in Africa is illustrated in the

2003 11.8% 88.2%

fact that in 2001 China’s share of contract revenue in Africa

2004 14.7% 85.3% Rest of World was a mere 7.4%, yet by 2009 this had climbed to 36.6% (see

chart to the left), making it the dominant player, far ahead of

2005 21.4% 78.6% Italy with 15% in second place and France with 10% in third.

2006 28.4% 71.6% Africa is now China’s largest market in terms of contract

revenue with 41.1%, even more than Asia with 36%. Similar

2007 26.9% 73.1%

to Chinese trade and investment in Africa, the revenue of

2008 42.4% 57.6%

Chinese contractors is highly concentrated in a few resource-

rich countries. In 2009, the leading six countries (Algeria,

2009 36.6% 63.4% Angola, Sudan, Nigeria, Libya and Ethiopia), mostly oil and

gas-related economies, accounted for USD 18.1 billion or 71%

0 10,000 20,000 30,000 40,000 50,000 60,000

Source: ENR; The Beijing Axis Analysis

of China’s total revenue (see chart opposite page).

Repaying loans for infrastructure development with natural Chinese contractors in Africa have been most successful in

resources is not a new concept. The first reported example of civil infrastructure projects such as transport and construc-

such a deal involving China in Africa was actually not 2004 in tion. As stated above, around 50% of Chinese contractors

Angola, but 2001 in the DRC when China provided USD 280 in Africa seem to prefer international bids, yet around 40%

million for dam construction and received loan payments were accounted for by grants, concessional loan projects and

in oil. After 2004, however, such deals became more widely other mechanisms in which the Chinese government play a

used by China in Africa, and also expanded to other resources strong role. The case of Angola, where Chinese commercial,

such as bauxite, chromium, and iron ore. It should be noted, investment and contracting activity has been vigorous for

however, that the Angola mode is not the only mode of almost a decade now, can be held up as an example of the

engagement for Chinese companies in Africa, yet they are progression of Chinese contracting over time. The establish-

common in countries such as Angola, the DRC and Sudan ment of Angola’s first loan agreement with China Exim Bank

who have only recently emerged from conflict and instability. in March 2004 facilitated the entry of China’s large SOEs into

Angola, and in the time since dozens of Chinese contractors

The process of concluding Angola Mode deals is typically have established operations there.4

borne out of intergovernmental agreements that deter-

mine the purpose, amount, maturity and interest rate of the Although Chinese contractors typically still focus more on

loan, followed by the signing of a loan agreement – often the lower value added part of the construction value chain,

concessional in nature – between China Exim Bank and the their ability to undertake construction projects at cheaper

borrower. The capital is then disbursed in tranches in terms prices have made them very competitive and, in the case

of project completion, and paid directly to Chinese contrac- of Angola, have broken the monopoly of Portuguese and

tors in China, which are selected by Exim Bank and China’s Brazilian contractors. Due to the volume of their needs and

Ministry of Commerce and sanctioned by the beneficiary the lack of quality products available for sourcing locally,

government. With such a methodology in place, the main Chinese contractors bring most of their workers and mate-

Chinese actors in Africa are rials from China (although in Angola some Chinese compa-

• Lending agencies: China’s policy banks, China Exim nies have in the last few years begun to set up local factories

Bank and China Development Bank through the to produce some industrial inputs). After a few years, mostly

China-Africa Development (CAD) Fund private Chinese companies also began entering Angola,

• Extractors and builders: Large state-owned enter- largely to subcontract from the larger companies and to set

prises and some private ones operating in the extrac- up a procurement chain for providing equipment and mate-

tive and construction/engineering industries rials from China.

• Other business people: Small to medium-sized

Chinese businesses and individual entrepreneurs that Windows of opportunity: Africa’s new business landscape

may appear subsequently

China is engaging with Africa like no other country has ever

Getting their hands dirty: Chinese contractors in Africa done before, and in the fundamental exchange of Africa’s

resources for Chinese-built infrastructure, China is making

Collectively, these actors are re-shaping Africa’s business

4 For an assessment of the various estimates provided for the number

landscape, yet none are doing so more obviously than China’s of Chinese state-owned and private companies in Angola, see L Corkin,

construction and engineering contractors. Having originally ‘Chinese Construction Companies in Angola: A Local Linkages Perspective,’

relied solely on Chinese government-financed projects, p. 17.

8 The Beijing Axis

9. Features

Features 专题 The China Analyst

a significant contribution to addressing a lasting struc- Leading Countries for Chinese Contractor Revenue in Africa

tural bottleneck in Africa. The ‘infrastructure for resources’ and Number of Chinese Contractors in Country (USD mn, 2009)

22

deals it concludes in Africa are unique in the way they lock 6,000

African countries into using their resources for infrastruc-

ture – revenue never actually comes in, obviating the need 17

5,000

for taxation. China is transcending conventional patterns of

engagement of straightforward FDI and ODI, and has instead

fashioned an elaborate system where a strong government 4,000

role and alternative financing methods can overcome risk,

and the leveraging of China’s own booming construction

industry can see Chinese contractors building much-needed 3,000

civil infrastructure as well as value-adding processing indus-

17

tries such as refineries and petro-chemical complexes in 2,000

14 12

Africa.

15

China is a strong player in Africa both in upstream activi- 1,000 8 6

7 9

ties such as exploration and extraction, as well as in down-

stream activities such as processing. China's demand for 1 1 5 4

0

oil and minerals has created a new level of competition for Algeria Angola Sudan Nigeria Libya Ethiopia Congo(B) Egypt DRC Botswana

Africa’s resources, and has contributed to higher prices, to Source: China Statistical Yearbook 2010; The Beijing Axis Analysis

the benefit of Africa. In countries such as the DRC and Angola

where previous failed construction booms have formed part more time in Africa they will become more aware of their

of protracted instability, China has undertaken projects own shortcomings and more receptive to the value offered

where many other investors have regarded the risk as being by foreign companies with the right knowledge and experi-

too high. The sustainability and flexibility of China’s contem- ence. For such foreign companies, the challenge will be to

porary engagement in Africa, moreover, should contribute utilise these opportunities in the right industries, at the right

significantly to Africa’s current construction boom not being time. China’s increased business in Africa has also created

as forlorn as the previous one, and that would make it a true demand for services essential to doing in business in Africa,

new era for Africa. providing new opportunities for banks, law firms, and various

other service providers.

This is not to say that the impact of China in Africa is flawless,

yet this should not be the expectation for something that is These are but a few examples of how China’s ‘infrastructure

not an exercise in altruism. Chinese projects in Africa are in for resources’ engagement is creating new business opportu-

essence turnkey projects, in theory fulfilled by contractors nities for foreign firms in Africa. Yet perhaps the best oppor-

who then sign off on the engagement, and hence the extent tunity of all is the fact that Africa itself is changing. As China’s

of the true lasting value add on the ground in Africa is some- activities in Africa increases, Africa is gradually transforming

times brought into question by some observers, especially itself from a perennial backwater to a new source of growth

since China exports a significant share of its labour to Africa. with diversifying economies, expanding consumer markets,

Yet this could be changing, as we have seen, as Chinese and working infrastructure – making Africa open for business

companies seek to establish local manufacturing capabilities like never before.

on the continent, in addition to establishing several special

economic zones and other forms of skills transfer. Barry van Wyk, Senior Consultant

barryvanwyk@thebeijingaxis.com

The strong role played by government-to-government inter-

action in Chinese deals in Africa has in practice often meant

that many of Africa’s mineral rights are sold in closed deals

and not in public auctions. Yet the increasing number of

Chinese extractive companies and construction/engineering

contractors in Africa has opened up a vast new opportunity

landscape for foreign companies on the continent, both

in terms of potential partnership and new clientele. Thus

in areas where Chinese companies are still comparatively

less adept, such as consulting and industrial design, many

opportunities for partnerships are now open to foreign firms.

Chinese firms in Africa still lack a deep understanding of local

business as well as cultural and regulatory issues, and here

again foreign companies with experience in Africa can profit.

Foreign companies could also explore joint bids with Chinese

companies for construction projects. As Chinese firms spend

The Beijing Axis 9

10. The China Analyst Features 专题

China and Latin America: Untapped Sources of Added

Value

Bilateral trade between China and Latin America has increased ten-fold in the last decade, preparing

the way for a massive wave of Chinese investment in the region in 2010. While both bilateral trade and

investment are expected to increase further in the coming years, questions remain on how balanced

and sustainable the relationship will be. This article argues that both regions are set to enter a new stage

of their relationship that will be characterised by increasing Chinese investments in more value added

industries and eventually higher value added exports from Latin America. By Javier Cuñat

O

nly ten years ago, upon China’s entry into the World imports and 2% of its total exports (see charts below). Ten

Trade Organisation (WTO), China was the world’s years later, trade between China and LatAm amounted to

seventh-largest economy, growing at 7.3% y-o-y and USD 179.3 billion, a tenfold increase, with LatAm accounting

accounting for just over a tenth of global economic growth. In for 6.5% of China’s total imports and 5.6% of its total exports;

2010, with a global financial crisis still persistent in the United and China accounting for 12.3% of LatAm’s total imports and

States (US) and Europe, China became the world’s second- 12.9% of LatAm’s total exports.

largest economy, growing at 9.6% (H1 2011) and contrib-

uting one-third to total world GDP growth. The emergence Overall, China is not only more important to LatAm today than

of China as a global economic power has greatly benefited ten years ago and vice versa, but the two regions are progres-

the global economy. In China’s phenomenal rise, one thing sively becoming more dependent on each other as important

is clear: as China grows, other countries benefit. As China’s sources of growth compared to other regions, exemplified by

exported-oriented economy keeps churning out increasingly the free trade agreements China has signed in recent years with

higher value added goods, other countries can now purchase Chile, Peru and Costa Rica. This trend became more evident

previously unattainable products at competitive prices. during the most recent financial crisis, during which China’s

stimulus package and unrelenting demand for commodities

Yet this trend has also to varying degrees presented the helped LatAm’s exports to China counterbalance a decrease

regions and countries within China’s trade, investment and in demand from the US and Europe. For its part China found

geopolitical radar with a number of challenges. Antidumping the perfect partner to serve its own demand, diversifying

and protectionist measures in the US and Europe, labour and its sources of fuel and metals needed to power and build its

community issues in Africa, and territorial disputes in Asia economy during the financial crisis and into the future.

are just some examples. Latin America (LatAm), with its own

particularities, is no exception. According to the Economic Commission for LatAm and the

Caribbean (ECLAC), China today ranks among LatAm’s top

The relationship trading partners, particularly in countries such as Brazil, Chile,

Peru and Argentina, where China accounts for 15%, 24%,

When China entered the WTO, annual trade between China 16% and 9%, respectively, of each country’s total exports.

and LatAm amounted to USD 14.4 billion, with LatAm What's more, China is now the largest importer of goods and

accounting for 2.7% of China’s total imports and 2.9% of its services from Brazil and Chile, and the second-largest from

total exports; and China accounting for 2.3 % of LatAm’s total Peru, Argentina and Cuba. However, these exports remain

China's Trade with LatAm and the Caribbean (USD bn, China's Trade with LatAm and the Caribbean (%, 2001-10)

2001-10)

100 14% China as % of LatAm Exports

China as % of LatAm Imports

Exports 12%

80 LatAm as % of China Exports

Imports 10% LatAm as % of China Imports

60

8%

6%

40

4%

20

2%

0 0

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Source: UN Comtrade; The Beijing Axis Analysis Source: UN Comtrade; The Beijing Axis Analysis

10 The Beijing Axis

11. Features

Features 专题 The China Analyst

concentrated in raw materials such as copper, iron ore, and A survey by the China-Brazil Business Council (CBBC) revealed

soybeans, which account for nearly 60% of total exports. that 93% of Chinese investments in Brazil in 2010 were under-

Similarly, China’s exports to LatAm are mainly electronic taken by state-owned companies, while 6% were undertaken

items, autoparts, equipment and machinery, and textiles. by companies belonging to provinces, and 1% by private

companies. The survey also found that Chinese investments

Indeed, the trade relationship between China and LatAm in 2010 totalled USD 12.6 billion (slightly higher than ECLAC’s

is essentially built on the exchange of natural resources for figures), 82% of which involved mergers and acquisitions.

manufactured goods or low value for high value added prod- Sinopec made the largest investment when it acquired a 40%

ucts. While this makes a lot of sense from the countries' factor stake in the Brazilian operations of Repsol-YPF for USD 7.1

endowment and comparative advantage point of view, it also billion (see table on next page). Of China's total investment

presents great challenges for LatAm manufacturers who have commitments in 2010, 95% were concentrated in the areas

seen Chinese exports progressively replace their market shares of oil and gas, agribusiness, mining, and ironworks. However,

at home, in other LatAm markets, and especially in the US. this trend appears to shifting in 2011, with announced Chinese

investments in LatAm and the Caribbean thus far amounting

Regarding investment, China's FDI stock in LatAm breached to USD 7.13 billion (see chart below), with a stronger focus on

USD 41 billion at the end of 2009, accounting for up to 18% higher value added industries.

of total Chinese FDI stock in the world. LatAm's investment

stock in China, on the other hand, dwarfs that number, hitting If the figures from 2010 and the announced figures of H1

USD 112.6 billion in 2008, or roughly 14% of the total foreign 2011 are any indication, they show that China is becoming

capital absorbed by China. A closer look into the GDP figures increasingly entrenched throughout the region, possibly

for both regions illustrates that current levels of Chinese FDI marking the start of a new phase of economic relations

in LatAm and the Caribbean are comparatively low. In addi- between China and LatAm which features stronger trade

tion, they are mostly concentrated in tax havens such as the links that are accompanied by growing investment in not

Cayman Islands and British Virgin Islands, which accounted only natural resources, but also manufacturing, infrastruc-

for 96.7% of all Chinese FDI into LatAm between 2003 and ture and services. As examples, Huawei, ZTE and Lenovo are

2009. Excluding the two tax havens, LatAm only received becoming prominent investors in the telecommunications

about USD 126 million in Chinese FDI, or less than 1% of the and electronics sectors, and BYD, Chery and Geely are leading

annual total. Overall, there is Chinese under-investment in all the charge in the auto industry.

sectors but especially in higher value added industries.

The fundamental challenges facing the China-LatAm relation-

2010 - Breakthrough ship are two-fold. Firstly, how to increase and diversify Chinese

FDI in the region beyond raw materials to more value added

In 2010, with an estimated investment of USD 15.25 billion, industries; and secondly how to improve trade by means of

China's investment in LatAm was more than twice the amount exporting more value added LatAm goods. Both challenges, as

it invested in the region in the period 2006–09, namely USD they unfold, will present substantial opportunities for both sides.

7 billion. China's 9% share of FDI in the region now makes

it the third-largest foreign investor in LatAm, trailing only Forever imbalanced? Unlikely

the US and the Netherlands, which accounted for 17% and

13%, respectively (see chart below). By country, the main Over the long term, the greatest opportunity but also chal-

destinations for Chinese FDI were Brazil, Argentina and Peru, lenge facing Chinese companies in LatAm is successful inte-

all of which have established strong trade links with China. gration with the host economies. The model it is presently

Brazil, China’s BRICS counterpart in the region, was by far the utilising in a number of countries, characterised by the acqui-

biggest benefactor of this investment wave, with USD 9.6 sition of natural resource assets, the extraction and low value

billion in Chinese FDI in 2010. added exports ‘back to China’, and under-developed commu-

nity relations, has both a limited political and business shelf

Origin of FDI in LatAm and the Caribbean* (%, 2006-10) China's LatAm FDI Destinations by Country* (%, 2010-Q3 2011)

USD 864.17 bn USD 112.63 bn USD 15.25 bn USD 7.13 bn

100% 100

8% 10% Latin America

Others Colombia

80% 80

30% 28% Caribbean Costa Rica

Financial

Mexico

Centres

60

60% 7% Ecuador

10% Netherlands

5% Peru

13% China

4% 40

40% 2% Argentina

10% 9% UK

4% Brazil

5% 3% Japan

4% 20

20% Spain

25%

17% Canada

0

0% 2010 Q1-Q3 2011

US

2006-2009 2010 *Note: Data for 2010 is confirmed investments; data for 2011 is announced investments.

Source: ECLAC; The Beijing Axis Analysis Source: ECLAC; The Beijing Axis Analysis

The Beijing Axis 11

12. The China Analyst Features 专题

Major Announced Chinese Foreign Direct Investments in LatAm (2010-11) highlighted deals denote those in non-resources sectors

Year Month Investor Status USD mn Partner/target Sector Subsector Country

2010 Jan Honbridge Holdings Concluded 400 Sul-Americana de Metals Metals Iron ore Brazil

2010 Feb Sany Heavy Industry Ongoing 200 Build a manufacturing plant Manufacturing Heavy machinery Brazil

2010 Mar East China Mineral Concluded 1,200 Itaminas Metals Iron ore Brazil

Expl. & Develop.

2010 Mar CNOOC Concluded 3,100 Bridas Energy Oil Argentina

2010 Mar State Grid Ongoing 1,050 Quadra Mining Metals Copper Chile

2010 Apr WISCO Concluded 4,700 A JV steel mill Metals Steel Brazil

2010 May State Grid Concluded 1,720 Cobra, Elecnor and Isolux Power Power grid Brazil

2010 May Sinochem Concluded 3,070 Peregrino Field Energy Oil Brazil

2010 Aug Tongling Nonferrous & Planning 3,000 A copper mine Metals Copper Ecuador

China Railway Construction

2010 Sep Chery Ongoing 400 n/a Transport Auto Brazil

2010 Oct Sinopec Ongoing 7,190 Repsol/YPF Energy Oil Brazil

2011 Jan CR Zongshen Concluded 80 Kasinski Transport Motorcycle Brazil

2011 Mar Chongqing Grain Group Concluded 2,400 n/a Agriculture Soybeans Brazil

2011 Apr Lenovo Ongoing 900 Positivo Electronics PC Brazil

2011 Apr Huawei Ongoing 363 Build a plant Telecom Mobile phone, tablet PC Brazil

2011 Apr ZTE Concluded 200 Build a plant Telecom Tablet PC Brazil

2011 May Chongqing Polycomp Concluded 60 Owens Corning Plant Material Fiber glass Brazil

International Corp.

2011 May XCMG Concluded 200 n/a Manufacturing Heavy machinery Brazil

2011 May Geely Concluded 10 Nordex Transport Auto Uruguay

2011 Jun China CNR Corp Ongoing 127 T’Trans Transport Train Brazil

2011 Jun Qingshan Mining Ongoing 3 JDC Mining Co Metals Gold, silver & copper Mexico

2011 Jun TCL Ongoing 21 Radio Victoria Fueguina Telecom Mobile Argentina

2011 Jul BOMCO Concluded n/a BRCP, Asperbras Energy Petroleum equipment Brazil

2011 Aug ICBC Ongoing 600 Standard Bank Argentina Finance Banking Argentina

2011 Aug Midea Group Ongoing 223 Carrier Corporation Manufacturing Home appliances Argentina,

of UTC Group Brazil, Chile

2011 Sep Taiyuan Steel, CITIC Ongoing 1,950 CBMM Metals Niobium Brazil

Group and Baosteel

Total for Q1-Q3 2011 7,137

Source: China Global Investment Tracker, Heritage Foundation, Carta da China No 56 June 2010, China-Brazil Business Council; Observatario Iberoamericano de Asia - Pacifico

and press releases. Note highlighted deals denote those in non-resources sectors.

life. While benefits of both existing and proposed Chinese construction equipment manufacturers, decided to put down

investments are real, trade tensions from the LatAm side are roots in the region by investing USD 200 million in a manu-

emerging and creating contradictions for both parties. We facturing plant in the Brazilian state of Sao Paulo. One year

saw a good example of this at the beginning of 2011, when later, XCMG, its closest Chinese competitor, followed in its

the Brazilian Finance Minister called for a revaluation of the footsteps. We have seen similar examples in the automobile

renminbi following a massive USD 15 billion flow of Chinese industry in Mexico, where Chinese automakers Zhongxing,

investments into Brazil during 2010. Geely and Changan, through a partnership with Mexico’s

Autopark, have all announced plans to establish auto-making

More importantly, LatAm now more than ever represents an facilities. China’s ZTE has started manufacturing smartphones

opportunity for Chinese manufacturers to enlarge their global in Argentina together with local white goods manufacturer

footprints and market shares, especially in markets where BGH and has also announced it will start producing tablet

their international competitors have a significant presence. computers in Brazil. The list goes on in a number of high-

Aware of China’s price advantages, constantly improving value-added industries (see table above). Leading Chinese

technology standards and overall positive macroeconomic companies are looking at a number of LatAm countries as

outlook for the LatAm region (recently revised by the World key launchpads from which to market their products not only

Bank to 4.6% growth for 2010), Chinese manufacturing in other LatAm markets but also in North American markets.

companies are realising that an export-oriented develop-

ment strategy towards LatAm without a footprint is a dead- According to ECLAC, 90% of China's confirmed investment

end game. Various factors, i.e. consolidated market shares at in LatAm has targeted the extraction of natural resources.

home, the need to better understand their customers in the Looking into China’s upgraded endowment factors over

region, and strong balance sheets built on export revenue the years, the scale, nature and international ambitions of

with low production costs, have laid the foundation for its domestic champions together with recent Chinese OFDI

capital investments to grow and deepen in the years to come. figures in the region, one can expect an increasing number

of Chinese manufacturing companies to invest in high value

In February 2010, Sany Heavy Industry, one of China’s largest added industries in the region. While investments in oil,

12 The Beijing Axis

13. Features

Features 专题 The China Analyst

gas and mineral resources will remain at the top of Beijing’s challenge but probably one of the best opportunities for the

agenda, less value added Chinese investments in LatAm region’s export diversification ambitions.

going forward would not make much sense from a global

supply chain point of view. If trade relations continue to Cross-border opportunities for LatAm's exporters do not

unfold as they have in the last decade, Chinese manufacturers only exist in the natural resources side of Chinese demand

and infrastructure developers will need to integrate LatAm but also in food, beverages, agribusiness, leather and fabrics,

in their supply chains in the long run as much as LatAm is plastics, chemicals, pharmaceuticals, machinery and elec-

willing to. So expect this trend to intensify. tronics, among other sectors. While market entry strategies

may vary greatly - from organic to inorganic growth, from

Over the long term, the greatest opportunity but also chal- JV partnerships to wholly foreign owned enterprises, from

lenge facing LatAm companies seeking to compete in China export development to assembling and/or manufacturing,

is to diversify their exports towards more value added prod- from partnering with a local distributor(s) to developing

ucts. While a significant number of LatAm’s manufactured one's own distribution channels – one thing is clear: ignoring

exports compete with products China itself produces, one the Chinese consumption market is neither possible nor wise

should not forget that China is the world’s second-largest if one aims to remain competitive over the long term.

importer of manufactured goods. So from a sectoral and

product perspective, the challenge is not that there is no Final word

market for LatAm's manufactured goods in China, but rather

identifying what the specific products with the greatest If 2010 meant anything for China-LatAm trade and invest-

potential are and how to market them effectively. ment relationship, it was change. We are leaving behind a

stage in the relationship characterised by booming bilateral

The Chinese market is more complex than any other market trade, few investments and strong unbalances, and entering

of comparable size, and therefore requires an on-the-ground, a new stage characterised by the utilisation of new sources

customised and dedicated strategic approach. Even though of added value. This stage will not only be characterised by

China is a large market for a number of products, entering the trade but also by increasing Chinese investments in more

Chinese market is not an easy task and profits are usually the value added industries and eventually higher value added

result of a long-term investment in understanding the Chinese exports from LatAm. If this happens, and we think it will, the

culture, the specifics of your market and network building. exchange of natural resources for manufactured goods will

Just as one cannot ignore that the emergence of Chinese prove to be not the trend itself but the catalyst and continu-

manufacturing companies is disrupting domestic competition ation of a bigger trend. Both regions are set to take steps

in a number of industries in LatAm, and increasingly in more towards a more balanced, sustainable, value added and

capital and technological-intensive products, one cannot mutually beneficial relationship. While Chinese OFDI figures

ignore that the Chinese marketplace represents a tremendous for 2010 and H1 2011 provide some hints, it is still uncertain

opportunity for international companies. China ranks among which countries, sectors and companies will be the protago-

the world's largest consumers and importers of power gener- nists in the coming decade.

ating equipment, aircraft and parts, computers and industrial

machinery, agricultural products, consumer and luxury goods How do LatAm companies look at China and how do Chinese

among a large spectrum of sectors and products. companies look at LatAm? While the challenges involved in

business transactions are complex, a change in perception

Brazilian aircraft company Embraer, along with Mexican will be key as old perceptions have on many occasions been

bread maker Bimbo, are just two examples of successful as unbalanced as the trade and investment relationship.

LatAm ventures in the Chinese market. Embraer, which China should not be perceived as a neo-colonial power as

opened its first office in Beijing in 2000, continued with the much as LatAm is no one’s backyard. The first, and most prob-

construction of a spare parts distribution centre at Beijing ably the biggest, barriers that LatAm companies face when

International Airport, and the signing of a joint venture with engaging with China are not that different than what the

Aviation Industry Corporation of China in 2003. Embraer Chinese face when engaging with LatAm. These are culture,

has delivered more than 70 aircraft in China and has already language, protocol, and lack of information, and they impact

achieved a 52% share of China’s market for aircraft with up how we understand the opportunities and challenges.

to 120 seats in 2009. With two plants in China, Bimbo is a

pioneer in marketing packaged baked goods in China, espe- Working out the information deficits and bringing the market

cially in Beijing and Tianjin, and is expanding to other cities. realities to the corporate landscape in China and LatAm will

further assist and facilitate mutually beneficial and more

Despite such precedents, LatAm’s business presence in China value added trade and investment. Government bodies,

is still mainly dominated by the so-called multilatinas, with a industry associations, chambers of commerce, corporate

strong component coming from the natural resources sector, players and service providers must work in that direction.

while LatAm's small and medium-sized enterprises lag behind

their counterparts in terms of presence and market penetra- The rules are changing but the game is just beginning.

tion. As LatAm becomes increasingly integrated with China,

bringing the region’s small and medium-sized enterprises to Javier Cuñat, General Manager: Beijing Axis Strategy

the Chinese market not only represents a major competitive javiercunat@thebeijingaxis.com

The Beijing Axis 13

14. The China Analyst Features 专题

Rising Stars: China’s Emerging Construction Machinery

Manufacturers

Buoyed by increasing demand, especially in emerging markets, China's construction machinery players

have been actively enhancing their international reach and catching up with their foreign counterparts.

China’s three leading companies in this sector are XCMG, Sany, and Zoomlion, and this article outlines

the different strategies adopted by these rising stars and their global expansion plans. By Ankit Khaitan

S

tarting from a mere USD 1 billion worth of sales in 1999, Global Market Share of Construction Machinery Industry in

China’s construction machinery industry saw a decade Terms of Sales Volume (2002 vs. 2009)

of high growth with sales reaching USD 60 billion in North

Europe Japan Others

China America

2010. This phenomenal growth in demand was fuelled by

rapid growth in both the developed coastal areas of China 100

and more recently, inland areas. In developed areas, the

16%

genesis of growth was local governments’ expansion of small

29%

cities, while in inland China it was a growing market for infra- 80 10%

structure and housing. Currently, for every 1% increase in the

urbanisation rate, 13 million people move from rural areas to 4%

cities, but this number still lags far behind that of developed

60 28% 13%

countries and the global average. The Chinese government

has set a clear target of achieving an urbanisation rate of 60%

by 2020, indicating that China still has a long way to go in

22%

this regard. 40

28%

Another key demand driver for construction machinery is

the strong growth in fixed asset investments spurred mostly 20

by downstream segments, including infrastructure and 32%

property investments. For instance, social housing, though 18%

comparatively smaller investments, is significant in construc-

tion project volume and substantially increases the need for 0

2002 2009

equipment. Additionally, demand from foreign markets has Source: CCMA; Off-Highway Research

also grown, allowing China’s construction machinery exports

to experience rapid growth in recent years. Together, these comprehensive production lines. In contrast, Zoomlion

factors have bolstered the development of the construction is China’s second-largest, and the world’s tenth-largest,

machinery industry in China, making it the world’s fastest- construction machinery manufacturer. It emerged out

growing and third-largest market and catapulting the three of Changsha Construction Machinery Research Institute,

largest players onto the world stage. a leading state-owned research institution focusing on

construction machinery, effectively affording it a strong

Beginnings competitive advantage.

According to a report by Off-Highway Research (a consul- Consolidation and government support

tancy specialising in the research and analysis of interna-

tional construction), China’s share of the global construc- Though the industry in China is highly fragmented with over

tion machinery market jumped from 18% in 2002 to 32% 900 companies vying for market share, a majority of them

in 2009 in terms of sales volume (see chart above, right). only manufacture components or engage in sub-assembly

China’s three leading pioneers in this regard are Sany Heavy due to the hefty upfront financial investments that are

Industry, Zoomlion and XCMG, which have emerged as the required. In addition, intense competition between both

three dominant manufacturers that together account for domestic and foreign participants as well as rising demand

about 30% of the market in China, larger than the top three for improved and advanced technology have forced small

foreign companies active in China (see chart on next page). operators to either be acquired by more established players

Indeed, these three are now ranked in the top ten in terms of or simply exit the game.

sales revenue globally.

In fact, the large in-house companies have supplemented

Out of these, Sany and XCMG only started operating in the organic growth and scaled up rapidly through consolida-

early 1990s but quickly transformed themselves from being tion. In the past decade, Sany has acquired assets from its

single product machinery companies to ones that boast parent company to expand its capabilities while Zoomlion

14 The Beijing Axis

15. Features

Features 专题 The China Analyst

Approximate Market Share of China's Construction balanced between its two largest segments, concrete and

Machinery Industry (2010) crane machinery, contributing 43% and 34% to total revenue,

Caterpillar Volvo XCMG Zoomlion respectively, in 2010 (see chart on next page).

Komatsu Hitachi XGMA Other Chinese Sany leads the local market for truck mounted concrete

Kobelco Sany Heavy Other Foreign pumps and full hydraulic rollers; its production of pump

trucks is one of the best in the world. Compared to Zoomlion,

it is less diverse and its most important segment, concrete,

10% 9% alone contributes more than 60% of its total sales revenue.

7% Nonetheless, after Sany acquired the excavator and truck

5% crane businesses from its parent, its level of business diver-

4% sification started closing in on Zoomlion’s, with product

32% 1% categories expanding to include concrete machinery, road

11%

construction machinery, excavator, pile driving machinery,

hoisting machinery and port machinery.

8%

3%

11%

XCMG is the world’s largest manufacturer of truck cranes,

Source: CCMA which account for most of its total revenue. The comprehen-

sive line of products it offers includes construction mobile

has targeted third parties to scale up its product offerings. cranes, crawler cranes, wheel loaders, concrete boom pumps,

For example, Zoomlion acquired Hunan Puyuan Construction piling rigs, aerial fire trucks, asphalt pavers and cold milling

Machinery's truck crane business and Zhongbiao’s environ- machines.

mental and sanitation machinery business in 2003.

Over the years, Chinese companies in various industries have

This consolidation is being further encouraged by the successfully moved up the value chain by offering a wide

government, who is actively promoting consolidation in range of products and the construction machinery industry

the industry to avoid disorderly competition among local is no different. Foreign companies have historically served

manufacturers. Furthermore, equipment manufacturing is the Chinese excavator market by leveraging their strong

one of the seven strategic emerging industries identified in expertise and precision quality. Yet according to CCMA data,

the 12th Five Year Plan that the government will focus on so Chinese companies now control one-third of the global exca-

as to foster the development of a sound market environment; vator market, up from 22% in 2006. Such strategic moves

hence consolidation will be an ongoing trend in the industry have undeniably boosted their overall competitiveness and

going forward. Chinese construction machinery manufac- allowed them to capture market share from their foreign

turers are also afforded tax breaks and other incentives from competitors in China and in other emerging markets.

local Chinese governments, enabling them to take a long

term view of the market rather than just focusing on short Going global – M&A and partnership

term profits.

The global presence of US-based Caterpillar and Japan's

It is worth noting that foreign enterprises have had little Komatsu has been strong for decades as they began

opportunity to compete against local competitors in this expanding abroad early on when growth in their domestic

consolidation drive due to regulatory restrictions, and have markets slowed with urbanisation reaching a saturation

been unable to acquire majority stakes in joint ventures with point. Following a similar strategy, Zoomlion, Sany and

domestic firms. This has allowed local rivals to gather market XCMG have been encouraged to expand into foreign markets

share from foreign companies and at the same time narrow because of their solid positions in the Chinese market, world-

the capability and quality gap by integrating independent class products, sustainable low cost advantage and China’s

enterprises’ abilities via strategic acquisitions. Moreover, expansive infrastructure projects. Sany in particular has led

foreign enterprises have simply not been able to increase domestic equipment manufacturers in overseas expansion.

production fast enough to meet rising demand, diluting their

market shares. However, the three differ in their overseas expansion strat-

egies. Zoomlion focuses on a direct M&A route to expand,

Different specialisations integrating its costs and scaling its position in China while

leveraging its target’s distribution network and technical

The product portfolios of China’s three largest industry players capacities. CIFA, a global manufacturer based in Italy, was a

mostly overlap, yet there is diversity in their product offerings very strategic acquisition for Zoomlion that strengthened the

and this unique characteristic defines some of the dynamics latter's R&D capabilities and helped increase its global market

in the industry. Zoomlion has the world's most diverse range share. In contrast, Sany has preferred to expand by building

of products including concrete machinery, tower cranes, its own plants in foreign countries. For instance, Sany recently

road and earthmoving machinery, environmental sanitation built research and development centres in Brazil (2010) and

machinery, and bulk material transportation equipment. Germany (2009) as part of an ambitious international expan-

Despite such a diversified portfolio, revenue sources are sion plan. Also, it is the first Chinese construction machinery

The Beijing Axis 15

16. The China Analyst Features 专题

XCMG, Sany, Zoomlion Revenue Mix Comparison (%, H1 and enter the top five global construction machinery compa-

2010) nies. For its part, Sany plans to scale up rapidly to achieve

Concrete Excavators

Mechanical these numbers as soon as 2012. To accomplish this, Sany is

Machinery Scrapers building plants in overseas markets with great potential such

Environmental as Indonesia, North African countries and South Africa, a stra-

Crane Machinery Machinery Compaction

tegic step that will open new channels to market its prod-

Road and Piling ucts. Zoomlion is following similar tactics and expanding

Machinery Others

quickly to acquire brands, technology and distribution

100 6% channels, with a keen focus on emerging markets. Similarly,

7% 9%

4% XCMG recently announced the acquisition of two European

12% 3% suppliers, marking its first international acquisitions aimed

20% 3%

80

12% at boosting its value chain and extending its technological

10% capabilities in key component production.

60 12% 37%

China’s three leading construction machinery manufacturers

seem well placed to achieve these goals, yet each of them still

40 have much potential to improve their technology. To be sure,

69% to enhance their competitive position, Chinese machinery

manufacturers are constantly upgrading their technological

20 52% 44% capabilities and focusing on technical innovation, but they

still have some ground to cover before they start taking on

the world leaders. That said, these firms have demonstrated

0 a remarkable ability to incorporate technology and quickly

XCMG Sany Zoomlion

Source: CCMA; Bloomberg adapt. As a case in point, Sany invented the first 66-metre

truck-mounted concrete pump in the world.

player to set up factories in India and the US, where it recently

opened a USD 60 million assembly plant which in August Chinese construction machinery manufacturers are set to

2011 started assembling trucks mounted with concrete- become some of the largest beneficiaries of the infrastruc-

pumping equipment. XCMG, China's largest construction ture boom in emerging markets where competitive prices are

machinery maker, has opted to cooperate with foreign capital key, and with improving technology and evolving interna-

and foster close partnerships with overseas dealers. The tional expansion plans, the likes of XCMG, Sany and Zoomlion

group has already established close cooperation with nearly are gearing up for bigger challenges.

100 dealers who help sell its products all over the world, but

most notably in emerging markets such as Indonesia, Brazil Ankit Khaitan, Consultant

and Russia. ankitkhaitan@thebeijingaxis.com

Among these key differences, there is one commonality

that exists in the internationalisation strategy of all three of

China’s major machinery manufacturers - they have been

aggressively marketing their product overseas though new

distributing channels with a core focus on emerging markets,

namely Brazil, Russia, India and Africa. Emerging markets are

sweet spots for these companies because it is difficult to

access developed US and European markets where dominant

and established players, such as Caterpillar, emphasise their

value-added after sales services. Emerging markets, on the

other hand, are more price sensitive, and prices of machinery

equipment from Chinese manufactures are typically 15-20%

below foreign competitors, providing buyers in emerging

markets with a considerable overall cost saving. Another

important reason is that, like China, these countries are

experiencing a similar urbanisation process and are conse-

quently investing a lot towards infrastructure improvement,

providing Chinese enterprises a potential market to tap into.

Reaching higher: The years ahead

XCMG, Zoomlion and Sany have revealed their sales targets

for the 12th Five Year Plan period (2011-15). XCMG and

Zoomlion aim to achieve USD 20 billion each in sales by 2015

16 The Beijing Axis

17. CHINAAFRICA

BUSINESS FORUM 2011

SAVE THE DATE | 20 OCT

8.00 am - 7.00 pm

Thursday, 20 October 2011

Gallagher Estate, South Africa

This one day Business Forum will bring together key business

leaders, industry specialists, project managers and others to

explore the exciting current dynamic of the China - Africa rela-

tionship.

For enquiries call +27 11 463 9184 or email Candice at

candice@siyenza.za.com or fax your request to +27 11 463 8432.

Organiser: Sponsor:

Siyenza Management (Pty) Ltd The Beijing Axis Ltd

info@siyenza.com www.thebeijingaxis.com

18. The China Analyst Features 专题

The New Scramble For Africa: Emerging Powers on the

Emerging Continent

The BRICS of China, India, Brazil, Russia and South Africa – and China in particular – are at the forefront

of a new scramble for projects and deals in Africa. Each one brings to the continent its own distinct busi-

ness nous, yet collectively the BRICS are instrumental in transforming Africa’s business fortunes. Leaving

aside China’s dominant position in Africa, this article focuses on the activities of the other BRICS nations

on the continent. By guest contributor Charlie Pistorius

T

he global balance of power is shifting into the hands BRICS Trade Profile (As a % of Country Total, 2009)

of the rapidly industrialising emerging growth giants, 60

especially the BRICS block of economies: Brazil, Russia,

India, China and South Africa. The BRICs (excluding South 50

Africa as the smallest strategic member) are today fuelling Africa

the global recovery with their huge demand requirements, 40 Developed

Economies

high growth multiples and vast deployment of capital.

Explosive population growth and rapid urbanisation in 30 Emerging Economies

these economies have engendered a vital demand for food South, East

and energy security, and an urgent need for capital stock 20 & Southeast Asia

build-up, in particular transport, power, communication and Latin America

housing infrastructure. In Africa the emerging BRICS have 10

latched onto China’s coattails in seeking commercial favour

0

and opportunity, although each with their own individual China India Brazil Russia SA BRICS

modus operandi and business methodology. Yet they all have Source: UNCTAD Statistical Yearbook 2010

the same purpose, namely to secure a foothold in Africa’s

vast and rich resource offerings. But the story is not merely is impressive. Between 2000 to year-end 2009, India origi-

one described by an exchange of outgoing raw materials in nated the majority of deals, 812 in all; China managed 450;

return for inbound capital, tools and cheap final products. As Russian firms undertook 436 deals; South Africa at least 237;

the floodgates for broader and more ingrained partnerships and Brazil 190. For the year 2010 up to the end of May 2011,

are opening, so too will Africa’s story change in its balance of China led the way by undertaking 195 new deals, followed

trade and investment. by India with 183, Russia 102, Brazil 51, and South Africa 40,

according to UNCTAD’s World Investment Report (2011).

The BRICS 'Way'

The trade relationship between the emerging economies

The large BRICS economies (as well as other emerging players and Africa is, however, the one that best defines the scale

such as South Korea and Turkey), all have the same compara- of their overall commitment and interest on the continent.

tive advantage in their outward engagement: they are able Collective bilateral trade between the BRICS and Africa for

to access large pools of finance and cash reserves (mostly instance ballooned from a mere USD 24.3 billion in 2000

through state incentives and subsidised support), and they to USD 193.4 billion in 2010 - though China's share of USD

also uphold a version of the Developmental State Model that 123.3 billion alone makes up 64% of the total. Of Africa’s total

encourages a statist approach to business - explicit in the trade volume with the world, the BRICS collectively account

case of China - that enables private enterprise and mercan- for an impressive 22%, which hardly measured 10% in 2000.

tile commerce, rather than perpetuating poor management Shockingly however, South Africa’s intra-Africa trade only

approaches which translates into an unproductive utilisation measured 2.3% of Africa’s global total in 2009, dropping to

of strategic assets. 1.5% in 2010 (see chart on next page).

As a bloc, the BRICS' global outward FDI stock build-up Brazil: Not only Lusophone specialists

increased substantially from USD 134 billion in 2000 to over

USD 1,085 billion in 2010 – only a small smattering of this To date Brazil’s multinational firms have mostly been involved

was, however, destined for Africa (roughly 2.7%). Developed in Africa’s construction and upstream exploration and

economies still provide the largest vested interest of capital energy production. The likes of Petrobras, which is one of

stock in Africa – roughly 40% originates from the European the global oil and gas leaders with 2009 revenues of over

economies. Since 2000, the majority of BRICS outward invest- USD 118 billion, has staked increasing claims in Africa, espe-

ments in Africa has been in cross-border M&A. Considered cially in Nigeria, Senegal and Angola, while also maintaining

purely by this measure, the number of BRICS engagements exploration activity in Mozambique and Tanzania. Brazilian

18 The Beijing Axis