Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (16)

Ähnlich wie Bank of baroda_q4_fy10

Ähnlich wie Bank of baroda_q4_fy10 (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Bank of baroda_q4_fy10

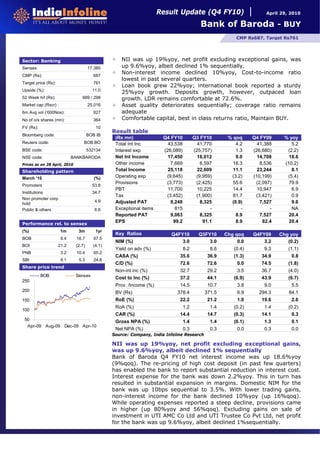

- 1. Result Update (Q4 FY10) April 29, 2010 Bank of Baroda - BUY CMP Rs687, Target Rs761 Sector: Banking NII was up 19%yoy, net profit excluding exceptional gains, was Sensex: 17,380 up 9.6%yoy, albeit declined 1% sequentially. Non-interest income declined 10%yoy, Cost-to-income ratio CMP (Rs): 687 lowest in past several quarters. Target price (Rs): 761 Loan book grew 22%yoy; international book reported a sturdy Upside (%): 11.0 25%yoy growth. Deposits growth, however, outpaced loan 52 Week h/l (Rs): 689 / 298 growth. LDR remains comfortable at 72.6%. Market cap (Rscr) : 25,016 Asset quality deteriorates sequentially; coverage ratio remains 6m Avg vol (‘000Nos): 927 adequate No of o/s shares (mn): 364 Comfortable capital, best in class returns ratio, Maintain BUY. FV (Rs): 10 Result table Bloomberg code: BOB IB (Rs mn) Q4 FY10 Q3 FY10 % qoq Q4 FY09 % yoy Reuters code: BOB.BO Total Int Inc 43,538 41,770 4.2 41,388 5.2 BSE code: 532134 Interest exp (26,089) (25,757) 1.3 (26,680) (2.2) NSE code: BANKBARODA Net Int Income 17,450 16,012 9.0 14,708 18.6 Prices as on 28 April, 2010 Other income 7,669 6,597 16.3 8,536 (10.2) Shareholding pattern Total Income 25,118 22,609 11.1 23,244 8.1 March '10 (%) Operating exp (9,645) (9,959) (3.2) (10,199) (5.4) Provisions (3,773) (2,425) 55.6 (2,097) 79.9 Promoters 53.8 PBT 11,700 10,225 14.4 10,947 6.9 Institutions 34.7 Tax (3,452) (1,900) 81.7 (3,421) 0.9 Non promoter corp 4.9 Adjusted PAT 8,248 8,325 (0.9) 7,527 9.6 hold Public & others 6.6 Exceptional items 815 - - - NA Reported PAT 9,063 8,325 8.9 7,527 20.4 Performance rel. to sensex EPS 99.2 91.1 8.9 82.4 20.4 (%) 1m 3m 1yr Key Ratios Q4FY10 Q3FY10 Chg qoq Q4FY09 Chg yoy BOB 9.4 16.7 67.5 NIM (%) 3.0 3.0 0.0 3.2 (0.2) BOI 21.2 (2.7) (4.1) Yield on adv (%) 8.2 8.6 (0.4) 9.3 (1.1) PNB 3.2 10.4 65.2 CASA (%) 35.6 36.9 (1.3) 34.9 0.8 SBI 9.1 5.3 24.6 C/D (%) 72.6 72.6 0.0 74.5 (1.8) Share price trend Non-int inc (%) 32.7 29.2 3.5 36.7 (4.0) BOB Sensex Cost to Inc (%) 37.2 44.1 (6.9) 43.9 (6.7) 250 Prov. /Income (%) 14.5 10.7 3.8 9.0 5.5 200 BV (Rs) 378.4 371.5 6.9 294.3 84.1 150 RoE (%) 22.2 21.2 1.0 19.6 2.6 RoA (%) 1.2 1.4 (0.2) 1.4 (0.2) 100 CAR (%) 14.4 14.7 (0.3) 14.1 0.3 50 Gross NPA (%) 1.4 1.4 (0.1) 1.3 0.1 Apr-09 Aug-09 Dec-09 Apr-10 Net NPA (%) 0.3 0.3 0.0 0.3 0.0 Source: Company, India Infoline Research NII was up 19%yoy, net profit excluding exceptional gains, was up 9.6%yoy, albeit declined 1% sequentially Bank of Baroda Q4 FY10 net interest income was up 18.6%yoy (9%qoq). The re-pricing of high cost deposit (in past few quarters) has enabled the bank to report substantial reduction in interest cost. Interest expense for the bank was down 2.2%yoy. This in turn has resulted in substantial expansion in margins. Domestic NIM for the bank was up 10bps sequential to 3.5%. With lower trading gains, non-interest income for the bank declined 10%yoy (up 16%qoq). While operating expenses reported a steep decline, provisions came in higher (up 80%yoy and 56%qoq). Excluding gains on sale of investment in UTI AMC Co Ltd and UTI Trustee Co Pvt Ltd, net profit for the bank was up 9.6%yoy, albeit declined 1%sequentially.

- 2. Bank of Baroda – (Q4 FY10) Non-interest income declined 10%yoy, Cost-to-income ratio lowest in past several quarters Bank of Baroda reported a steep 10%yoy decline in its non-interest income. While fee income grew at a modest pace 8%yoy growth rate, the bank reported 58%yoy decline in trading income. The recovery mechanism adopted in the recent times enabled the bank to report 43%yoy rise in recovery from previous write-offs. We expect the bank to witness 16%CAGR in non-interest income over FY10-12E. For the quarter ended Q4 FY10, the bank reported substantial decline in its operating cost. Operating expenses were down 5%yoy and 3%qoq. This is commendable as the bank added over 178 branches and 136 ATM’s during the year. Of this, over 50branches and 77 ATM’s were added during the quarter. Cost-to-income ratio for the bank at 38.4% is the lowest in past several quarters. Loan book grew 22%yoy; international book reported a sturdy 25%yoy growth. As against the system credit growth of 16.7%yoy as at March 2010, the bank reported a healthy 22%yoy growth in its loan book. Even on a sequential basis, the loan book was up 12%. This growth in loan book was led by sturdy 25%yoy (8%qoq) rise in international loans. The share of international loans in total loan book has now increased to 24.8% as against 24.2% as at end FY09. We expect the share to remain at current levels in coming period as margin on this book has remained low at 1.4%. On the other hand, domestic book, too reported a healthy 21%yoy (13.5%qoq) growth. Amongst the domestic book, retail loan book was up 23.5%yoy, SME (excluding retail) was up 28%yoy. While the proportion of retail book in total book stood at 18.2%, the proportion of home loans in total domestic book stands at 7.8%. The agriculture book was up 29%yoy, largely due to year-end phenomenon. Gross NPA on agriculture portfolio has remained at elevated levels of 3.3% as against 1.7% as at FY09. We expect the bank to witness 22% CAGR in loans over FY10-12E. Deposit growth outpaces loan growth; international deposit grew 36%yoy; CASA deposits, too reported a healthy 25%yoy rise. The bank reported a healthy 25.3%yoy (12.1%qoq) rise in deposit growth. The C/D ratio for the bank remained at comfortable levels of 73%. The re-pricing of high cost-of-deposits during the past few quarters had enabled the bank to report substantial reduction in cost-of-deposits. Domestic cost-of- deposits have declined from 6.5% as at end FY09 to 5.6% as at end FY10 (down ~80bps), albeit rose sequentially. Given the rising interest scenario, interest cost is set to rise. International deposits grew 36%yoy (14% sequentially). CASA deposits, on the other hand reported 25%yoy (7.6%qoq) growth. CASA ratio for the bank now stands at 35.6%. Asset quality deteriorates sequentially; coverage ratio remains adequate Gross NPL for the bank were up 6.2%qoq (30.3%yoy) to Rs24bn or 1.36% of total loans. Net NPL too grew 33.5%yoy (23.5%qoq) to Rs6bn or 0.34% of total loans. Interestingly, Gross and Net NPA on international book has remained low at 0.47% and 0.11% respectively. We however remain comfortable with bank’s asset quality and expect minimal accretion in coming quarters. Credit cost for the bank too rose to 6bps as at end FY10. We have factored in 9% CAGR in loan loss provision over FY10-12E. The bank restructured Rs4.6bn of loans during the quarters, taking the total loan restructured to Rs51bn. This, however, remains minimal when compared with peers. Provision coverage ratio for the bank has remained comfortable at 74.9% levels. Comfortable capital, best in class returns ratio, Maintain BUY. The bank remains adequately capitalized with CAR at 14.4% an Tier I ratio at 9.3%. It has raised over Rs9bn of Tier I capital (innovative perpetual bond) and Rs10bn of Tier II bond since the beginning of the year. In a recent interview, the bank management had indicated a comfortable CAR of 13-13.5% Returns ratio for the bank remains amongst the best with RoE at 23.7% and RoA of 1.2% as at end FY10. We continue to like the bank and expect it to command premium valuation as against its peers on expectations of higher loan growth, better returns ratio and minimal concerns over asset quality. We have raised our FY11 and FY12 net profit estimates by 6% and 13% respectively. The bank has outperformed its peers and Sensex over the past three-six months and currently trades at cheap valuation of 1.2x FY12 PB. We expect the valuations to re-rate further and have assigned a 1.4x FY12 PB multiple to arrive at a fair value of Rs761. Maintain BUY. Result Update 2

- 3. Bank of Baroda – (Q4 FY10) Peer comparison (Q4 FY10) Key Ratios BoB Corp Bank NIM (%) 2.5 3.0 CASA (%) 28.6 35.6 C/D (%) 68.2 72.6 Non-interest income (%) 42.6 30.5 Cost to Income (%) 40.3 38.4 BV (Rs) 402.6 378.4 RoE (%) 20.3 22.2 RoA (%) 1.3 1.2 CAR (%) 15.4 14.4 Gross NPA (%) 1.0 1.4 Net NPA (%) 0.3 0.3 Source: Companies, India Infoline Research Financial summary Y/e 31 Mar (Rs m) FY09 FY10A FY11E FY12E Total operating income 78,811 87,458 109,036 134,176 yoy growth (%) 32.2 11.0 24.7 23.1 Operating profit (pre-provisions) 43,050 49,353 61,414 75,095 Net profit 22,272 30,583 32,650 40,122 yoy growth (%) 55.1 37.3 6.8 22.9 EPS (Rs) 60.9 83.7 89.3 109.8 BVPS (Rs) 282 397 470 564 P/E (x) 11.3 8.2 7.7 6.2 P/BV (x) 2.4 1.7 1.5 1.2 ROE (%) 22.3 23.7 19.9 20.7 ROA (%) 1.1 1.2 1.1 1.1 Dividend yield (%) 1.3 2.2 2.2 2.2 CAR (%) 14.1 14.4 13.0 12.3 Tier I (%) 8.5 9.3 9.0 8.8 Source: Company, India Infoline Research Result Update 3

- 4. Bank of Baroda – (Q4 FY10) NIM improved by 10bps sequentially CASA deposits grew 7.6%qoq and 25%yoy 3.3 (%) 40.0 (%) 3.1 38.0 2.9 36.0 2.7 34.0 2.5 32.0 2.3 30.0 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Source: Company, India Infoline Research Asset quality remains comfortable Adequately capitalised GNPL NNPL NPL coverage (RHS) 15.0 (%) 3.0 (%) 84.0 (%) 2.5 82.0 14.0 2.0 80.0 13.0 1.5 78.0 1.0 76.0 12.0 0.5 74.0 0.0 72.0 11.0 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Source: Company, India Infoline Research Trend in loans and deposits growth (Q-o-Q) Share of international loans and deposits in total book. Loans Deposits Loans Deposits 27.0 20.0 (%) (%) 15.0 25.0 10.0 23.0 5.0 21.0 - 19.0 (5.0) (10.0) 17.0 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Q1 FY08 Q2 FY08 Q3 FY08 Q4 FY08 Q1 FY09 Q2 FY09 Q3 FY09 Q4 FY09 Q1 FY10 Q2 FY10 Q3 FY10 Q4 FY10 Source: Company, India Infoline Research. Result Update 4

- 5. Recommendation parameters for fundamental reports: Buy – Absolute return of over +10% Market Performer – Absolute return between -10% to +10% Sell – Absolute return below -10% Published in 2010. © India Infoline Ltd 2010 This report is for the personal information of the authorised recipient and is not for public distribution and should not be reproduced or redistributed without prior permission. The information provided in the document is from publicly available data and other sources, which we believe, are reliable. Efforts are made to try and ensure accuracy of data however, India Infoline and/or any of its affiliates and/or employees shall not be liable for loss or damage that may arise from use of this document. India Infoline and/or any of its affiliates and/or employees may or may not hold positions in any of the securities mentioned in the document. The report also includes analysis and views expressed by our research team. The report is purely for information purposes and does not construe to be investment recommendation/advice or an offer or solicitation of an offer to buy/sell any securities. The opinions expressed are our current opinions as of the date appearing in the material and may be subject to change from time to time without notice. Investors should not solely rely on the information contained in this document and must make investment decisions based on their own investment objectives, risk profile and financial position. The recipients of this material should take their own professional advice before acting on this information. India Infoline and/or its affiliate companies may deal in the securities mentioned herein as a broker or for any other transaction as a Market Maker, Investment Advisor, etc. to the issuer company or its connected persons. India Infoline Ltd. One India Bull Center, Jupiter Mill Compound, 841, Senapati Bapat Marg, Nr, Elphinstone Road, Lower Parel (W), Mumbai 400 013. For Research related queries, write to: Amar Ambani at amar@indiainfoline.com or research@indiainfoline.com For Sales and Account related information, write to customer care: info@5pmail.com or call on 91-22 4007 1000