Key Carrier WiFi Infographics

•

0 gefällt mir•647 views

Download our at-a-glance overview of the WBA's new Industry Report on Global Trends in Public Wi-Fi. Please feel free to distribute to the widest possible audience!

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Mehr von Wi-Fi 360

Mehr von Wi-Fi 360 (14)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Key Carrier WiFi Infographics

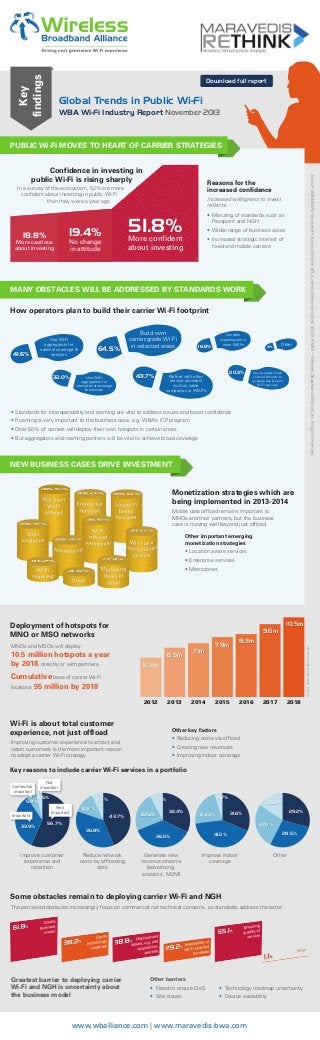

- 1. Key findings Download full report Global Trends in Public Wi-Fi WBA Wi-Fi Industry Report November 2013 PUBLIC Wi-Fi MOVES TO HEART OF CARRIER STRATEGIES Reasons for the increased confidence In a survey of the ecosystem, 52% are more confident about investing in public Wi-Fi than they were a year ago 18.8% More cautious about investing Increased willingness to invest reflects: • Maturing of standards such as Passpoint and NGH 51.8% 19.4% • Wider range of business cases More confident about investing No change in attitude • Increased strategic interest of fixed and mobile carriers MANY OBSTACLES WILL BE ADDRESSED BY STANDARDS WORK How operators plan to build their carrier Wi-Fi footprint 41.6% Use Wi-Fi aggregators for national coverage & services 32.0% 64.5% Use Wi-Fi aggregators for international coverage & services Build own carrier-grade Wi-Fi in selected areas 43.7% Consider acquiring one or more WISPs 16.8% 20.3% Partner with other service providers such as cable companies or WISPs 1.5% Other Use so-called crowd sourced hotspots to leverage free & open Wi-Fi services • Standards for interoperability and roaming are vital to address issues and boost confidence • Roaming is very important to the business case, e.g. WBA’s ICP program • Over 60% of carriers will deploy their own hotspots in certain areas • But aggregators and roaming partners will be vital to achieve broad coverage Source: WBA/MaRe ecosystem survey October 2013 unless otherwise stated. © 2013 WBA – Wireless Broadband Alliance Ltd. All rights reserved. Confidence in investing in public Wi-Fi is rising sharply NEW BUSINESS CASES DRIVE INVESTMENT Monetization strategies which are being implemented in 2013-2014 Mobile data offload remains important to MNOs and their partners, but the business case is moving well beyond just offload. Other important emerging monetization strategies • Location aware services • Enterprise services • Metrozones Deployment of hotspots for MNO or MSO networks 10.5m 9.6m 10.5 million hotspots a year by 2018, directly or with partners. 6.5m 8.3m 7.9m 7.1m Source: Maravedis-Rethink forecast MNOs and MSOs will deploy 5.2m Cumulative base of carrier Wi-Fi locations 55 million by 2018 2012 2013 2014 2015 2016 Wi-Fi is about total customer experience, not just offload 2018 Other key factors Improving customer experience to attract and retain customers is the most important reason to adopt a carrier Wi-Fi strategy. 2017 • Creating new revenues • Reducing costs via offload • Improving indoor coverage Key reasons to include carrier Wi-Fi services in a portfolio Somewhat important 5.9% Important 33.9% Not important 3.5% 6.9% Very important 4.7% 7.6% 12.6% 43.7% 23.5% 32.4% 15.3% 56.7% Improve customer experience and retention 29.2% 31.6% 22.2% 27.0% 36.8% Reduce network costs by offloading data 41.5% 36.5% Generate new revenue streams (advertising, analytics, M2M) Improve indoor coverage 28.5% Other Some obstacles remain to deploying carrier Wi-Fi and NGH The perceived obstacles increasingly focus on commercial not technical concerns, as standards address the latter. Greatest barrier to deploying carrier Wi-Fi and NGH is uncertainty about the business model Other barriers • Need to ensure QoS • Technology roadmap uncertainty • Site issues • Device availability www.wballiance.com | www.maravedis-bwa.com