Call Girls In Noida 959961⊹3876 Independent Escort Service Noida

Hsbc correcion

1. 28 May 2010 Equity Strategy

Global abc

Global Research

EI – Equity Insights

A normal correction, not a new bear market

The recent correction is typical of year two of a bull market

as the first phase of growth ends

We still believe earnings growth will remain strong and

structural problems are not as bad as the market fears

Indiscriminate selling presents some attractive opportunities

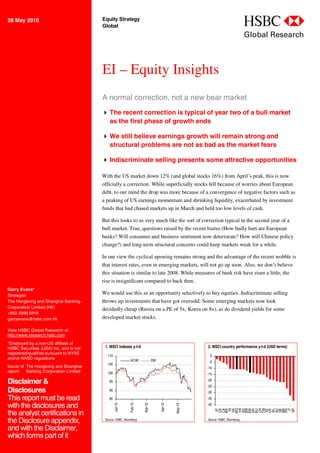

With the US market down 12% (and global stocks 16%) from April’s peak, this is now

officially a correction. While superficially stocks fell because of worries about European

debt, to our mind the drop was more because of a convergence of negative factors such as

a peaking of US earnings momentum and shrinking liquidity, exacerbated by investment

funds that had chased markets up in March and held too low levels of cash.

But this looks to us very much like the sort of correction typical in the second year of a

bull market. True, questions raised by the recent hiatus (How badly hurt are European

banks? Will consumer and business sentiment now deteriorate? How will Chinese policy

change?) and long-term structural concerns could keep markets weak for a while.

In our view the cyclical upswing remains strong and the advantage of the recent wobble is

that interest rates, even in emerging markets, will not go up soon. Also, we don’t believe

this situation is similar to late 2008. While measures of bank risk have risen a little, the

rise is insignificant compared to back then.

Garry Evans*

Strategist

We would use this as an opportunity selectively to buy equities. Indiscriminate selling

The Hongkong and Shanghai Banking throws up investments that have got oversold. Some emerging markets now look

Corporation Limited (HK) decidedly cheap (Russia on a PE of 5x, Korea on 8x), as do dividend yields for some

+852 2996 6916

garryevans@hsbc.com.hk developed market stocks.

View HSBC Global Research at:

http://www.research.hsbc.com

*Employed by a non-US affiliate of

HSBC Securities (USA) Inc, and is not 1. MSCI indexes y-t-d 2. MSCI country performance y-t-d (USD terms)

registered/qualified pursuant to NYSE

110 0

and/or NASD regulations ACWI EM -5

105

Issuer of The Hongkong and Shanghai -10

report: Banking Corporation Limited 100 -15

Disclaimer & 95 -20

-25

Disclosures 90

-30

This report must be read 85 -35

with the disclosures and

Jan-10

Feb-10

Mar-10

Apr-10

May-10

-40

HK

WO

IT

SW

TW

IN

CH

NL

JP

US

CA

MX

SA

UK

GE

SP

SG

EM

SZ

KR

RU

AU

BR

FR

the analyst certifications in

the Disclosure appendix, Source: HSBC, Bloomberg Source: HSBC, Bloomberg

and with the Disclaimer,

which forms part of it

2. Equity Strategy

Global abc

28 May 2010

What happened 3. ISM and ISM new orders – inventories

Before considering what might happen next, it is ISM New orders-inv ent (RHS, 3MMA)

65 30

essential to analyse thoroughly why equity 60

20

markets fell so sharply from mid-April. 55

50 10

While worries about Greek and other European

45 0

sovereign debt were the immediate cause, in our 40

view the decline was triggered rather by a -10

35

convergence of several negative factors. The 30 -20

decline was exacerbated by technical factors such 1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

as the positioning of institutional funds at the

Source: HSBC, Datastream

beginning of April.

Logically, this has to be the case. Greece is only Specifically, earnings momentum has

the 26th-largest economy in the world and its started to slow. Forecast earnings growth has

stock market comprises only 0.1% of MSCI been accelerating since mid-2009, but the first

World. How could worries about the sustainability signs are coming through of the momentum

of its debt cause global stocks to correct by 16%? peaking. This happened in Asia ex Japan at

the end of last year (see Chart 4) – one reason

The negative factors, besides European sovereign

why we went underweight the region. In the

risk, we are talking about include:

US and Europe, earnings momentum looks to

The end of the first phase of growth. Global have peaked in March. The Q1 US earnings

growth began to bottom early in 2009. The US season was extremely strong, with 11% y-o-y

manufacturing ISM, for example, troughed in revenue growth and 78% of S&P500

December 2008 and rose above 50 for the first companies beating forecasts at the bottom

time in August 2009 (Chart 3). Economists line. But, with expectations now somewhat

began to revise up 2010 US GDP forecasts higher than before, earnings can hardly go on

starting in June last year. But in most cycles, beating consensus forecasts at the same pace.

after an initial spurt, the acceleration of 4. Forecast earnings momentum*

growth inevitably slows. That is likely to

50% US AEJ

happen over the coming months. The lead

40%

indicator of the ISM – new orders minus 30%

inventories – for example (also shown in 20%

Chart 3) points to the headline ISM falling to 10%

52 over the next few months. That, don’t 0%

forget, still implies that business is expanding, -10% 00 02 04 06 08 10

but just at a slower pace. The same thing -20%

-30%

happened after the initial leg of the recovery in

-40%

1995 and 2005. Stock markets simply started

to discount this slowing of momentum. Source: HSBC, Datastream (*Change in the 12-month forward IBES EPS forecast over

the past six months)

2

3. Equity Strategy

Global abc

28 May 2010

Drying-up of liquidity. With the Fed’s members. Signs of this included Germany’s

purchases of securities over, the impact of unilateral ban on naked short-selling of

earlier liquidity injections wearing off, and the certain securities including government

money multiplier still low, money supply bonds, and clear disagreements within the

growth has slowed sharply in the US over the European Central Bank on its programme to

past few months. It is the same story in the rest purchase Eurozone government bonds.

of the developed economies, and even in Asia

Panic buying and selling

(Chinese M1 growth has fallen to 30% from

The degree of decline in stocks was also probably

39% over the past two months, for example).

exacerbated by how investors were positioned in

After such a strong liquidity-driven rally over

early April. Our conversations with fund managers

the past 12 months, that worries investors.

suggest that many were cautious in mid-February

5. US money supply growth (%, y-o-y) after the sharp decline in markets early in the year

25 and so missed the early part of the rally from

M1 M2 MZM February to April when MSCI World rose by 14%.

20

Many were forced to buy into the momentum –

15

rather against their better judgement given long-

10

term structural worries – towards the end of Q1.

5

That left them longer equities than they wanted to

0 be in early April, and Greece’s problems gave them

-5 85 89 93 97 01 05 09 a convenient excuse to take profits.

-10

6. Cash holdings of US mutual funds (% of total assets)

Source: HSBC, Bloomberg

7.0

6.5 All mutual funds

US bank regulation. The Senate version of the 6.0

regulatory reform bill came out at the last 5.5

minute much tougher on banks than initially 5.0

4.5

expected. Not only did it incorporate the full

4.0

“Volcker rule” (forcing banks to spin off prop

3.5

trading operations and sell stakes in hedge funds 3.0

and private equity funds), but it also obliges 98 99 00 01 02 03 04 05 06 07 08 09 10

banks to spin off their derivatives operations

Source: ICI

into separately capitalised units. How much of

this will survive when the bill is combined with

It is also clear that equity funds had very

the House’s version remains to be seen.

significantly lowered their cash holdings since

Confused messages out of Europe. While early 2009. Data for US mutual funds, for

there are genuine worries about the debt instance (Chart 6), shows they had cash equal

levels of some European countries, the only to 3.4% of assets at the end of March, lower

EUR750bn package put together by the even than at the peak of the 2003-7 bull market. In

European Union and IMF should have calmed April and May we suspect that cash holdings have

the markets. The main reason it did not was been built up significantly again.

the apparent disunity among Eurozone

3

4. Equity Strategy

Global abc

28 May 2010

And, as markets came down, we have seen signs of began right on cue after 410 days. There has been

institutions liquefying their funds as a precaution a wide variation, but on average the correction has

against redemptions. Understandable, given that in lasted 121 days. That would put the bottom this

the week ending 19 May, for example, equity time around August.

mutual funds globally saw outflows of USD12bn,

What happens next

according to EPFR data. Hedge funds, too, have

started to worry about a new wave of redemptions After such a sharp dislocation and rise in risk

and are also looking to raise cash levels to prepare aversion, there are obviously a large number of

against that eventuality. uncertainties. For example: how much will

European growth slow next year as a result of

Correction came right on cue

austerity programmes? How will consumer and

We have argued previously that the second year

business sentiment in Europe and the rest of the

of a bull market almost always sees a correction

world be affected by the falls in stock markets?

(which we would define as a 10-20% decline in

How big are the risks for European banks? Can the

US stocks, which equates to a decline of about 15-

US economic recovery remain resilient in the face

30% in higher-beta emerging markets).

of Europe’s problems? With Spain already seeing

The reason for this is that exactly the factors declining prices and US inflation slowing sharply,

described above start to kick in: the initial spurt of how big a worry is deflation? When do investors

growth peters out, and markets begin to wonder start to get nervous about sovereign risk in bigger

whether the recovery is sustainable. In every economies, such as the UK, the US or Japan?

recovery, there is also always a phase when the

It will take some time before it is clear what are

measures taken to end the recession (for example,

the answers to these questions. Moreover, how the

fiscal stimulus, rate cuts, bank rescues) are

situation with European government debt will pan

unwound. It is just that this time the magnitude of

out is also extremely hard to forecast with

the damage was that much bigger.

confidence. When and how will the EUR750bn

As shown in Table 7, the first correction in package be used? Will the ECB eventually move

S&P500 over the past 70 years came on average towards quantitative easing?

421 days after the bull market started. This time, it

7. US bull markets and initial correction

Started Ended Months Change % First correction Period until 1st Percent Length of

correction correction correction

(days) (days)

27-Jun-32 10-Mar-37 57 320% 7-Sep-32 72 -39% 176

28-Apr-42 30-May-46 50 158% 15-Jul-43 443 -11% 139

13-Jun-49 2-Aug-56 87 267% 13-Jun-50 365 -13% 34

22-Oct-57 12-Dec-61 50 86% None

26-Jun-62 9-Feb-66 44 80% 13-May-65 1052 -10% 46

7-Oct-66 29-Nov-68 26 48% None

26-May-70 11-Jan-73 32 74% 29-Apr-71 338 -14% 210

3-Oct-74 28-Nov-80 75 126% 15-Jul-75 285 -14% 64

12-Aug-82 25-Aug-87 61 229% 10-Oct-83 424 -14% 289

5-Dec-87 23-Mar-00 150 582% 3-Jan-90 760 -10% 27

9-Oct-02 9-Oct-07 61 101% 2-Dec-02 54 -14% 100

9-Mar-09 15 80% 23-Apr-10 410 -12% 27

Average 63 188% 421 -15% 121

Average (ex 1932-7) 64 175% 465 -12% 114

Source: HSBC, Bloomberg

4

5. Equity Strategy

Global abc

28 May 2010

The timeline for developments in China over the It is not clear that Europe’s travails will affect

next few months is equally hard to predict. Even US growth. As we have argued previously,

Premier Wen Jiabao admitted recently that “we for the next few quarters at least growth

are facing a few dilemmas in macro-adjustment”. should be boosted by (1) the remnants of last

Will the authorities continue to tighten policy to year’s USD787bn fiscal package, only 50%

prevent overheating, or has the economy begun to of which has so far been spent, (2) rebuilding

slow and therefore the authorities will need of inventories, which have increased only 1%

quickly to unwind policies to, for example, slow since the bottom last September despite

the rise in property prices? having been reduced by 14% during the

recession, (3) the ultra-low level of activity

This suggests that uncertainty is likely to continue

currently throughout the economy, as seen for

for a while and that stock markets will not

example in housing starts which, despite a

rebound strongly and investor confidence return

recent pick-up, are still 16% below the all-

until there is more clarity on some of these issues.

time low point of the past 50 years (Chart 9),

A correction, not a bear market (4) a modest rebound in capex, (5) short-term

Nonetheless, it still seems more likely to us that interest rates that are likely to remain close to

this will turn out to be a correction in a bull zero until the second half of next year.

market and not a new bear market. Some reasons:

9. US housing starts (SAAR)

8. US consumer expectations vs GDP consumption 3000

7 120 2500

6 110

5 100 2000

4

3 90 1500

2 80

1 70 1000

0 60

-1 500

1990

1993

1996

1999

2002

2005

2008

-2 50

-3 40 0

-4 30 63 68 73 78 83 88 93 98 03 08

GDP consumption (LHS) Consumer ex p

Source: HSBC, Bloomberg

Source: HSBC, Bloomberg

Corporate earnings growth is likely to remain

So far (at least), there are no signs that consumer strong. Companies, especially in the US, cut

or business confidence has been affected by the costs so drastically during the recession that

troubles in Europe. US consumer confidence, margins are likely to remain high for some

published on Tuesday and with data collected time to come. This means that only a small

up to 18 May, for example (Chart 8), surprised amount of top-line growth is sufficient to

on the upside (and is consistent with produce strong bottom-line numbers.

consumption growth of 2.5-3%). Even in Moreover, in many sectors, particularly

Europe, the German IFO survey published on retailing, companies that saw competitors go

21 May showed expectations higher than bust during the recession are enjoying

economists were forecasting. stronger pricing power.

5

6. Equity Strategy

Global abc

28 May 2010

Investors are already extremely bearish. Our recent drop in commodity prices. One of the

visits to fund managers recently, most notably negative factors for investing in emerging

in the US over the past two weeks, suggest markets – that they would almost all have to

there is a very strong consensus that Europe is raise rates in coming months – has disappeared,

a disaster-zone, with the Euro system likely to in our view.

collapse any time soon, and that the US’s

Things aren’t that bad

high and rising government debt/GDP ratio

It is also easy to exaggerate how much of a

means that it is only a matter of time before

negative impact the recent turmoil has had on

the US (and the UK and Germany) follow the

markets. While measures of bank risk have risen a

same path as Greece. Given this degree of

little, the rise is insignificant compared to the past

bearishness, we would argue that much of the

two years. The spread between three-month Libor

bad news is priced in.

and interest-rate swaps, for example (Chart 10),

How big are Europe’s problems really? While has risen to 29bps from a normal level of about

southern European countries clearly have a 8bps over the past six weeks. That represents an

problematical level of debt, and there are increase in risk aversion towards banks, but is

fundamental design flaws with the Euro, it is nowhere near that reached even in the summer of

wrong to underestimate the determination of 2007 when the credit crisis first started.

the European authorities to prop the system up.

10. Libor-OIS spread

They have done a lot already to at least

4.0

postpone the pain. The EUR110bn bailout

3.5

package for Greece should be enough to allow 3.0

it to fund itself until at least the end of 2011. 2.5

The EUR750bn general package and ECB 2.0

1.5

bond-buying scheme should ward off any

1.0

further immediate problems. On the positive 0.5

side, the whiff of crisis has pushed countries 0.0

Oct-06

Oct-07

Oct-08

Oct-09

Jan-06

Apr-06

Jul-06

Jan-07

Apr-07

Jul-07

Jan-08

Apr-08

Jul-08

Jan-09

Apr-09

Jul-09

Jan-10

Apr-10

such as Spain to begin to take the necessary

steps to make their economies more

competitive. The weakness of the Euro will Source: HSBC, Bloomberg

also help European exporters, such as

Germany. European growth is likely to slow The same is true of the Euro. We see many

next year, but the situation may not be anything headlines declaring that it has collapsed. While it

like as dire as investors have priced in. is true it has fallen by 19% against the dollar since

the peak in November last year, it is worth

The recent hiatus is likely to ward off remembering that this was almost an all-time high

premature monetary tightening. It seems for the currency. Look at the currency from a

unlikely that any major central bank will raise longer perspective (Chart 11), and it is still at the

rates over the next few quarters (and some, high end of the range it has traded in since its

such as Australia, which have already raised inception in 1999, and even well above the 30-

rates several times, may now be regretting that). year average of the theoretical Euro.

Notably, in emerging markets the risk of

inflation is likely to have receded with the

6

7. Equity Strategy

Global abc

28 May 2010

11. Trade-weighted Euro 12. Valuation data for major markets

130 Region 12M PE 2010 DY 10yGB

ACWI 11.3 2.7

120 Developed World 11.6 2.7

Emerging World 9.6 2.8

110 US 12.2 2.0 3.2

Canada 13.2 2.5 3.4

100 Brazil 9.1 3.4 12.6

Mexico 12.9 2.6 7.5

Europe 9.7 3.9

90

Europe ex UK 10.1 3.8

UK 9.0 4.1 3.6

80 France 9.9 4.1 2.9

81 83 85 87 89 91 93 95 97 99 01 03 05 07 09 Germany 10.4 3.4 2.7

Switzerland 11.1 3.3 1.5

Spain 8.2 6.4 4.1

Source: ECB Italy 9.1 4.5 3.9

Russia 5.1 2.3

Asia ex Japan 10.8 3.2

How to position yourself Japan 14.8 2.0 1.3

Australia 11.3 4.2 5.3

To us then, the mood of despondency is overdone. China 11.2 2.8 3.2

Korea 8.3 1.6 4.9

Most likely, what we have experienced over the Taiwan 11.5 4.3 1.4

past few weeks has been a normal second-year Hong Kong 13.9 3.4 2.5

India 14.8 1.2 7.4

stock market correction, exacerbated only by the Singapore 12.5 3.5 2.6

unprecedented nature of some of the long-term Source: HSBC, Datastream

structural imbalances in the global economy. That

suggests that, once the issues have been digested, Dividend yields are also starting to look attractive

the continuing cyclical rebound will represent and in some cases are above 10-year government

again an interesting time to buy equities. bond yields. Spain, for example, has a market

dividend yield of 6.4%, compared to government

An indiscriminate sell-off creates opportunities. We bonds yielding 4.1%. In Asia, Japan, Taiwan,

would already be looking to find countries, sectors Hong Kong and Singapore all offer higher DYs

and stocks where prices have fallen so low that than bond yields.

investors should be using this as an opportunity to

buy. In many cases, these will be investments that Among large-cap stocks, this is particularly the

have an attractive fundamental story but where case. Table 13, for example, shows stocks in the

valuations had run ahead of themselves. MSCI ACWI index with market cap greater than

USD10bn that have a forecast 2010 dividend yield

Consider country stock market valuations, for of 6% or higher and a dividend coverage ratio for

example (Table 12). Some markets are again this year of 1.5x or greater. It is notable how

offering extremely good value. Russia, for many blue-chip stocks, where one would think

example, is on a forward PE of 5x, Korea on 8x earnings should be well supported and where

and Brazil on 9x. dividend payout ratios are low, now offer highly

attractive dividend yields. In a low interest-rate

environment, these should look particularly

attractive to investors.

7

8. Equity Strategy

Global abc

28 May 2010

13. Large-cap stocks with dividend yield over 6%

Mkt cap DY (%) Cover

(USDbn) ratio (x)

AVIVA 11.8 8.8 2.3

BP 130.8 7.9 1.9

ZURICH FINANCIAL SVS. 28.6 7.8 1.8

ENEL 40.6 7.6 1.7

GAS NATURAL SDG 12.8 7.4 1.7

BANCO SANTANDER 82.3 7.1 1.9

ROYAL DUTCH SHELL 155.4 6.9 1.8

ENI 71.6 6.9 1.8

TURKCELL ILETISIM HZM. 11.1 6.7 1.7

VODAFONE GROUP 97.8 6.7 1.8

ENERGIAS DE PORTUGAL 10.7 6.6 1.7

FIRSTENERGY 10.5 6.5 1.6

RWE 36.1 6.5 1.9

E ON 58.0 6.4 1.8

BT GROUP 13.3 6.3 2.2

MOBL.TELSMS.OJSC SPN.ADR 18.6 6.3 1.7

TOTAL 106.5 6.2 1.9

CEZ 21.9 6.2 1.7

ELI LILLY 37.8 6.2 2.2

TELECOM ITALIA 14.9 6.2 2.0

SAMPO 'A' 11.2 6.1 1.8

AXA 34.5 6.1 2.5

CREDIT AGRICOLE 24.9 6.0 2.3

SK TELECOM 10.4 6.0 2.0

Source: HSBC, Datastream

8

9. Equity Strategy

Global abc

28 May 2010

Disclosure appendix

Analyst Certification

The following analyst(s), economist(s), and/or strategist(s) who is(are) primarily responsible for this report, certifies(y) that the

opinion(s) on the subject security(ies) or issuer(s) and/or any other views or forecasts expressed herein accurately reflect their

personal view(s) and that no part of their compensation was, is or will be directly or indirectly related to the specific

recommendation(s) or views contained in this research report: Garry Evans

Important disclosures

Stock ratings and basis for financial analysis

HSBC believes that investors utilise various disciplines and investment horizons when making investment decisions, which

depend largely on individual circumstances such as the investor's existing holdings, risk tolerance and other considerations.

Given these differences, HSBC has two principal aims in its equity research: 1) to identify long-term investment opportunities

based on particular themes or ideas that may affect the future earnings or cash flows of companies on a 12 month time horizon;

and 2) from time to time to identify short-term investment opportunities that are derived from fundamental, quantitative,

technical or event-driven techniques on a 0-3 month time horizon and which may differ from our long-term investment rating.

HSBC has assigned ratings for its long-term investment opportunities as described below.

This report addresses only the long-term investment opportunities of the companies referred to in the report. As and when

HSBC publishes a short-term trading idea the stocks to which these relate are identified on the website at

www.hsbcnet.com/research. Details of these short-term investment opportunities can be found under the Reports section of this

website.

HSBC believes an investor's decision to buy or sell a stock should depend on individual circumstances such as the investor's

existing holdings and other considerations. Different securities firms use a variety of ratings terms as well as different rating

systems to describe their recommendations. Investors should carefully read the definitions of the ratings used in each research

report. In addition, because research reports contain more complete information concerning the analysts' views, investors

should carefully read the entire research report and should not infer its contents from the rating. In any case, ratings should not

be used or relied on in isolation as investment advice.

Rating definitions for long-term investment opportunities

Stock ratings

HSBC assigns ratings to its stocks in this sector on the following basis:

For each stock we set a required rate of return calculated from the risk free rate for that stock's domestic, or as appropriate,

regional market and the relevant equity risk premium established by our strategy team. The price target for a stock represents

the value the analyst expects the stock to reach over our performance horizon. The performance horizon is 12 months. For a

stock to be classified as Overweight, the implied return must exceed the required return by at least 5 percentage points over the

next 12 months (or 10 percentage points for a stock classified as Volatile*). For a stock to be classified as Underweight, the

stock must be expected to underperform its required return by at least 5 percentage points over the next 12 months (or 10

percentage points for a stock classified as Volatile*). Stocks between these bands are classified as Neutral.

Our ratings are re-calibrated against these bands at the time of any 'material change' (initiation of coverage, change of volatility

status or change in price target). Notwithstanding this, and although ratings are subject to ongoing management review,

expected returns will be permitted to move outside the bands as a result of normal share price fluctuations without necessarily

triggering a rating change.

*A stock will be classified as volatile if its historical volatility has exceeded 40%, if the stock has been listed for less than 12

months (unless it is in an industry or sector where volatility is low) or if the analyst expects significant volatility. However,

9

10. Equity Strategy

Global abc

28 May 2010

stocks which we do not consider volatile may in fact also behave in such a way. Historical volatility is defined as the past

month's average of the daily 365-day moving average volatilities. In order to avoid misleadingly frequent changes in rating,

however, volatility has to move 2.5 percentage points past the 40% benchmark in either direction for a stock's status to change.

Rating distribution for long-term investment opportunities

As of 27 May 2010, the distribution of all ratings published is as follows:

Overweight (Buy) 50% (14% of these provided with Investment Banking Services)

Neutral (Hold) 37% (12% of these provided with Investment Banking Services)

Underweight (Sell) 13% (11% of these provided with Investment Banking Services)

Analysts, economists, and strategists are paid in part by reference to the profitability of HSBC which includes investment

banking revenues.

For disclosures in respect of any company mentioned in this report, please see the most recently published report on that

company available at www.hsbcnet.com/research.

* HSBC Legal Entities are listed in the Disclaimer below.

Additional disclosures

1 This report is dated as at 28 May 2010.

2 All market data included in this report are dated as at close 25 May 2010, unless otherwise indicated in the report.

3 HSBC has procedures in place to identify and manage any potential conflicts of interest that arise in connection with its

Research business. HSBC's analysts and its other staff who are involved in the preparation and dissemination of Research

operate and have a management reporting line independent of HSBC's Investment Banking business. Information Barrier

procedures are in place between the Investment Banking and Research businesses to ensure that any confidential and/or

price sensitive information is handled in an appropriate manner.

10

12. abc

Global Equity Strategy Research Team

Global Asia

Garry Evans Garry Evans

Global Head of Equity Strategy +852 2996 6916 garryevans@hsbc.com.hk

+852 2996 6916 garryevans@hsbc.com.hk

Leo Li

Europe +852 2996 6919 leofli@hsbc.com.hk

Robert Parkes Steven Sun

+44 20 7991 6716 robert.parkes@hsbcib.com +852 2822 4298 stevensun@hsbc.com.hk

CEEMEA Jacqueline Tse

+852 2996 6602 jacquelinetse@hsbc.com.hk

John Lomax

Vivek Misra

+44 20 7992 3712 john.lomax@hsbcib.com

+91 80 3001 3699 vivekmisra@hsbc.co.in

Wietse Nijenhuis

+44 20 7992 3680 wietse.nijenhuis@hsbcib.com