Empfohlen

Weitere ähnliche Inhalte

Ähnlich wie Residual

Ähnlich wie Residual (20)

Mehr von iipmff2

Mehr von iipmff2 (20)

Residual

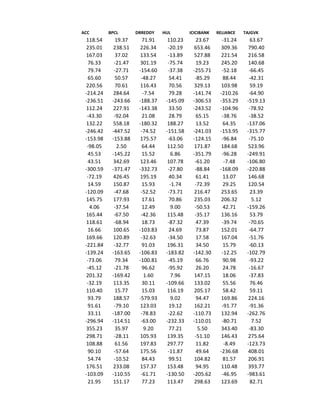

- 1. ACC BPCL DRREDDY HUL ICICIBANK RELIANCE TAJGVK 118.54 19.37 71.91 110.23 23.67 -31.24 63.67 235.01 238.51 226.34 -20.19 653.46 309.36 790.40 167.03 37.02 133.54 -13.89 527.88 221.54 216.58 76.33 -21.47 301.19 -75.74 19.23 245.20 140.68 79.74 -27.71 -154.60 -37.38 -255.71 -52.18 -66.45 65.60 50.57 -48.27 54.41 -85.29 88.44 -42.31 220.56 70.61 116.43 70.56 329.13 103.98 59.19 -214.24 284.64 -7.54 79.28 -141.74 -210.26 -64.90 -236.51 -243.66 -188.37 -145.09 -306.53 -353.29 -519.13 112.24 227.91 -143.38 33.50 -243.52 -104.96 -78.92 -43.30 -92.04 21.08 28.79 65.15 -38.76 -38.52 132.22 558.18 -180.32 188.27 13.52 64.35 -137.06 -246.42 -447.52 -74.52 -151.58 -241.03 -153.95 -315.77 -153.98 -153.88 175.57 -63.06 -124.15 -96.84 -75.10 -98.05 2.50 64.44 112.50 171.87 184.68 523.96 45.53 -145.22 15.52 6.86 -351.79 -96.28 -249.91 43.51 342.69 123.46 107.78 -61.20 -7.48 -106.80 -300.59 -371.47 -332.73 -27.80 -88.84 -168.09 -220.88 -72.19 426.45 195.19 40.34 61.41 13.07 146.68 14.59 150.87 15.93 -1.74 -72.39 29.25 120.54 -120.09 -47.68 -52.52 -73.71 216.47 253.65 23.39 145.75 177.93 17.61 70.86 235.03 206.32 5.12 4.06 -37.54 12.49 9.00 -50.53 42.71 -159.26 165.44 -67.50 -42.36 115.48 -35.17 136.16 53.79 118.61 -68.94 18.73 -87.32 47.39 -39.74 -70.65 16.66 100.65 -103.83 24.69 73.87 152.01 -64.77 169.66 120.89 -32.63 -34.50 17.58 167.04 -51.76 -221.84 -32.77 91.03 196.31 34.50 15.79 -60.13 -139.24 -163.65 -106.83 -183.82 -142.30 -12.25 -102.79 -73.06 79.34 -100.81 -45.19 66.76 90.98 -93.22 -45.12 -21.78 96.62 -95.92 26.20 24.78 -16.67 201.32 -169.42 1.60 7.96 147.15 18.06 -37.83 -32.19 113.35 30.11 -109.66 133.02 55.56 76.46 110.40 15.77 15.03 116.19 205.17 58.42 59.11 93.79 188.57 -579.93 9.02 94.47 169.86 224.16 91.61 -79.10 123.03 19.12 162.21 -91.77 -91.36 33.11 -187.00 -78.83 -22.62 -110.73 132.94 -262.76 -296.94 -114.51 -63.00 -232.33 -110.01 -80.71 7.52 355.23 35.97 9.20 77.21 5.50 343.40 -83.30 298.71 -28.11 105.93 139.35 -51.10 146.43 275.64 108.88 61.56 197.83 297.77 11.82 -8.49 -123.73 90.10 -57.64 175.56 -11.87 49.64 -236.68 408.01 54.74 -10.52 84.43 99.51 104.82 81.57 206.91 176.51 233.08 157.37 153.48 94.95 110.48 393.77 -103.09 -110.55 -61.71 -130.50 -205.62 -46.95 -983.61 21.95 151.17 77.23 113.47 298.63 123.69 82.71

- 2. 133.83 -22.91 -53.10 -8.28 -118.21 27.38 376.50 160.59 -2.29 133.64 19.02 306.38 113.55 62.71 9.24 -72.16 47.27 174.24 103.15 241.23 51.99 53.58 152.83 164.86 49.73 107.01 15.79 127.32 0.17 -23.25 -165.43 50.93 -100.36 -39.56 125.65 -22.69 -209.34 31.40 -100.80 37.49 -22.00 -19.10 34.26 9.46 -26.32 -118.27 66.50 53.99 -2.94 66.09 -89.89 -178.75 137.24 -33.77 -3.15 125.95 216.20 202.65 105.61 -9.96 111.61 38.64 73.76 143.24 161.68 70.44 190.38 163.32 -27.44 443.60 -48.94 -17.25 22.87 -5.74 53.66 26.07 321.88 -9.58 0.17 55.08 143.57 73.17 106.59 59.65 148.97 16.10 -87.08 -44.37 10.32 -32.52 354.10 -12.14 -29.71 41.24 -103.69 112.88 165.48 208.35 25.56 236.93 -93.80 -84.56 73.44 -0.42 -50.70 -184.43 -443.10 -99.67 -36.94 -322.29 -220.31 -203.36 119.93 -21.78 -129.44 -101.81 75.73 -25.87 139.50 -20.61 49.81 -257.73 -134.87 112.27 -36.02 -123.36 17.62 -11.37 -135.08 -89.09 -98.02 -12.52 7.22 51.20 37.70 -25.90 -97.14 -1.62 -25.77 -101.24 97.77 309.09 149.59 176.38 217.59 211.40 205.16 74.88 50.81 75.64 26.84 15.06 1.48 401.72 57.52 -77.89 155.91 -61.39 249.39 115.32 468.86 -51.12 122.56 -97.88 -11.96 165.61 129.07 -34.04 112.43 316.03 3.61 105.89 154.95 143.50 36.88 194.14 -85.91 60.25 -49.58 71.93 121.88 308.77 178.50 75.62 272.31 156.29 106.13 105.69 364.13 135.32 188.79 25.51 111.21 166.41 105.59 21.00 -66.71 49.20 -57.10 -34.78 -113.05 -15.75 165.58 -121.83 -9.92 54.70 -148.80 -124.98 -67.79 -207.53 95.83 198.75 -36.32 -12.62 -4.80 85.95 59.26 -162.45 -136.53 6.94 -69.68 80.28 -92.23 -45.61 9.52 163.65 216.54 70.26 66.24 41.89 12.97 279.01 8.56 110.54 86.17 -15.57 101.24 -26.76 -42.25 120.70 -197.49 -86.24 -46.19 34.64 11.37 -3.04 -448.91 -79.89 -90.65 -27.58 11.98 -59.46 48.36 -69.33 64.74 111.36 25.60 54.76 -117.07 -197.17 109.32 -123.74 -138.31 25.27 -111.58 -14.46 60.30 49.80 -6.25 50.19 -4.77 26.87 -50.77 3.18 -147.80 -58.66 -101.93 272.70 -64.02 0.00 -19.95 -130.94 -100.81 -120.72 -108.96 -87.71 -184.54 -69.29 188.73 43.31 -112.76 -10.56 -29.43 29.00 21.38 378.68 165.32 152.38 459.29 30.99 -55.33 67.77 158.66 2.21 -13.19 23.00 -23.91 17.42 -129.72 15.63 -33.16 72.79 -147.18 67.25 0.00 331.00 92.39 -105.64 -25.70 -5.91 167.69 19.67 85.51 105.35 -501.56 44.92 500.42 -46.26 21.02

- 3. -36.99 -95.27 12.47 -64.18 -388.68 -179.53 40.34 -96.45 -75.42 58.10 -11.14 -189.60 -28.98 21.05 24.61 -11.81 61.05 89.97 -16.91 -161.68 16.00 -25.38 -44.26 175.27 45.16 -145.30 -72.80 98.08 -75.00 0.92 301.98 -71.01 -101.29 174.48 0.00 174.07 21.93 -119.93 -48.44 -48.94 -144.94 23.53 -323.44 105.65 -74.44 -54.59 -72.55 -71.14 0.00 -11.36 164.73 24.68 132.24 191.57 92.04 206.90

- 4. TATAMOTORSNifty 186.49 37.21 458.00 336.79 422.63 179.94 249.16 111.72 -2.81 -46.40 -76.57 -34.21 201.17 88.88 -231.08 -54.27 -608.37 -316.92 -262.94 -120.77 109.74 7.49 -63.51 86.84 -311.93 -204.40 -160.36 -68.71 80.55 109.34 -133.05 -112.34 1.54 20.10 -68.66 -195.71 15.48 78.26 -40.22 -28.04 -29.42 210.13 128.51 149.83 4.03 -17.18 52.28 58.51 -135.77 6.29 6.31 61.03 38.81 83.64 -83.41 24.43 -130.75 -99.17 -29.71 35.19 135.62 3.61 -26.96 67.43 -47.28 52.07 22.49 61.34 167.86 103.35 -79.71 5.75 10.35 22.33 -206.19 -164.12 25.37 54.68 170.03 127.95 182.51 29.43 101.10 69.61 210.72 83.39 213.05 142.37 -139.82 -106.30 189.32 109.07

- 5. -48.53 37.55 156.40 49.55 -21.06 76.48 56.74 116.72 -0.58 -78.49 -156.95 -38.57 -67.68 26.62 -2.02 -13.21 53.72 74.56 192.49 115.44 40.17 28.46 38.86 83.65 -92.18 -0.40 135.05 100.98 44.51 17.79 -268.50 -208.79 -33.22 16.39 -54.24 -18.93 -26.63 -6.27 181.44 -44.69 127.77 196.50 109.11 45.77 261.70 117.54 112.72 53.56 292.96 172.74 168.75 54.70 184.16 151.79 166.77 93.46 -37.78 -54.16 -55.16 -96.14 74.61 24.82 -57.99 -56.68 -55.32 49.54 202.69 124.55 111.93 -14.64 -61.08 -56.34 117.07 64.70 -218.53 -112.20 339.88 33.83 -74.36 -61.63 29.52 -47.86 -130.69 -13.13 156.90 74.37 302.85 18.53 -52.30 -9.11 277.36 117.60 273.71 76.23

- 6. -102.52 -159.32 81.47 -21.36 159.62 -37.96 -289.60 -61.65 105.56 45.48 189.28 -23.99 -438.48 -180.44 114.32 -17.76

- 7. Beta 0.883421 Rj Rm Alpha Estimated Rj^ Residual S. No. ACC Nifty 1 118.54 37.21 10.05 42.92 75.63 2 235.01 336.79 307.58 -72.56 3 167.03 179.94 169.01 -1.99 4 76.33 111.72 108.74 -32.42 5 79.74 -46.40 -30.94 110.68 6 65.60 -34.21 -20.17 85.78 7 220.56 88.88 88.56 132.00 8 -214.24 -54.27 -37.90 -176.34 9 -236.51 -316.92 -269.93 33.42 10 112.24 -120.77 -96.65 208.89 11 -43.30 7.49 16.66 -59.96 12 132.22 86.84 86.76 45.46 13 -246.42 -204.40 -170.53 -75.90 14 -153.98 -68.71 -50.66 -103.33 15 -98.05 109.34 106.64 -204.69 16 45.53 -112.34 -89.20 134.73 17 43.51 20.10 27.80 15.71 18 -300.59 -195.71 -162.85 -137.74 19 -72.19 78.26 79.19 -151.38 20 14.59 -28.04 -14.73 29.32 21 -120.09 210.13 195.68 -315.77 22 145.75 149.83 142.40 3.34 23 4.06 -17.18 -5.13 9.19 24 165.44 58.51 61.73 103.71 25 118.61 6.29 15.60 103.01 26 16.66 61.03 63.96 -47.30 27 169.66 83.64 83.93 85.72 28 -221.84 24.43 31.63 -253.47 29 -139.24 -99.17 -77.56 -61.68 30 -73.06 35.19 41.13 -114.19 31 -45.12 3.61 13.24 -58.36 32 201.32 67.43 69.62 131.71 33 -32.19 52.07 56.04 -88.23 34 110.40 61.34 64.23 46.17 35 93.79 103.35 101.34 -7.55 36 91.61 5.75 15.13 76.48 37 33.11 22.33 29.77 3.34 38 -296.94 -164.12 -134.94 -162.00 39 355.23 54.68 58.35 296.88 40 298.71 127.95 123.08 175.62 41 108.88 29.43 36.04 72.84 42 90.10 69.61 71.54 18.55 43 54.74 83.39 83.71 -28.97 44 176.51 142.37 135.82 40.69

- 8. 45 -103.09 -106.30 -83.87 -19.22 46 21.95 109.07 106.40 -84.45 47 133.83 37.55 43.22 90.61 48 160.59 49.55 53.82 106.77 49 9.24 76.48 77.61 -68.37 50 53.58 116.72 113.16 -59.58 51 0.17 -78.49 -59.29 59.46 52 -22.69 -38.57 -24.03 1.33 53 34.26 26.62 33.57 0.69 54 66.09 -13.21 -1.62 67.71 55 216.20 74.56 75.91 140.29 56 143.24 115.44 112.03 31.21 57 -48.94 28.46 35.19 -84.13 58 -9.58 83.65 83.95 -93.52 59 148.97 -0.40 9.69 139.28 60 -12.14 100.98 99.26 -111.40 61 25.56 17.79 25.77 -0.20 62 -184.43 -208.79 -174.40 -10.03 63 119.93 16.39 24.52 95.40 64 -20.61 -18.93 -6.68 -13.93 65 17.62 -6.27 4.51 13.11 66 51.20 -44.69 -29.43 80.64 67 97.77 196.50 183.64 -85.87 68 74.88 45.77 50.48 24.39 69 57.52 117.54 113.88 -56.36 70 -51.12 53.56 57.36 -108.48 71 112.43 172.74 162.65 -50.21 72 194.14 54.70 58.37 135.77 73 178.50 151.79 144.14 34.36 74 135.32 93.46 92.61 42.71 75 -66.71 -54.16 -37.80 -28.91 76 -121.83 -96.14 -74.89 -46.94 77 95.83 24.82 31.97 63.86 78 -162.45 -56.68 -40.03 -122.42 79 9.52 49.54 53.81 -44.28 80 279.01 124.55 120.08 158.93 81 -42.25 -14.64 -2.89 -39.36 82 -3.04 -56.34 -39.73 36.69 83 48.36 64.70 67.20 -18.84 84 -197.17 -112.20 -89.07 -108.10 85 60.30 33.83 39.93 20.37 86 3.18 -61.63 -44.40 47.58 87 -19.95 -47.86 -32.23 12.29 88 -69.29 -13.13 -1.56 -67.73 89 21.38 74.37 75.75 -54.37 90 67.77 18.53 26.41 41.36 91 -129.72 -9.11 2.00 -131.72

- 9. 92 331.00 117.60 113.94 217.06 93 85.51 76.23 77.39 8.12 94 -36.99 -159.32 -130.70 93.71 95 -96.45 -21.36 -8.83 -87.62 96 24.61 -37.96 -23.49 48.10 97 -25.38 -61.65 -44.42 19.04 98 -75.00 45.48 50.23 -125.23 99 174.07 -23.99 -11.14 185.21 100 -323.44 -180.44 -149.35 -174.09 101 -11.36 -17.76 -5.64 -5.72 Mean 26.45 18.57 Residual 10668.89

- 10. Beta 0.87247 Rj Rm Alpha Estimated Rj^ Residual S. No. BPCL Nifty 1 19.36733 37.21 9.28 41.74 -22.38 2 238.5141 336.79 303.12 -64.61 3 37.01635 179.94 166.28 -129.26 4 -21.4677 111.72 106.75 -128.22 5 -27.7076 -46.40 -31.20 3.49 6 50.57166 -34.21 -20.56 71.14 7 70.60811 88.88 86.82 -16.21 8 284.6395 -54.27 -38.07 322.71 9 -243.664 -316.92 -267.23 23.56 10 227.9108 -120.77 -96.09 324.00 11 -92.0403 7.49 15.82 -107.86 12 558.1769 86.84 85.04 473.13 13 -447.52 -204.40 -169.06 -278.47 14 -153.884 -68.71 -50.67 -103.21 15 2.496634 109.34 104.68 -102.18 16 -145.224 -112.34 -88.73 -56.49 17 342.6912 20.10 26.82 315.88 18 -371.469 -195.71 -161.47 -210.00 19 426.4527 78.26 77.56 348.89 20 150.8741 -28.04 -15.19 166.06 21 -47.6777 210.13 192.62 -240.29 22 177.9277 149.83 140.00 37.93 23 -37.535 -17.18 -5.71 -31.82 24 -67.4989 58.51 60.33 -127.83 25 -68.9369 6.29 14.76 -83.70 26 100.6452 61.03 62.53 38.12 27 120.8918 83.64 82.25 38.64 28 -32.7711 24.43 30.59 -63.37 29 -163.651 -99.17 -77.24 -86.41 30 79.33738 35.19 39.98 39.36 31 -21.7833 3.61 12.43 -34.21 32 -169.419 67.43 68.11 -237.53 33 113.3497 52.07 54.71 58.64 34 15.76545 61.34 62.79 -47.03 35 188.5742 103.35 99.45 89.13 36 -79.1031 5.75 14.30 -93.40 37 -187.003 22.33 28.76 -215.77 38 -114.507 -164.12 -133.91 19.40 39 35.97461 54.68 56.99 -21.01 40 -28.1056 127.95 120.92 -149.02 41 61.55703 29.43 34.96 26.60 42 -57.6353 69.61 70.01 -127.65 43 -10.5239 83.39 82.03 -92.56 44 233.0794 142.37 133.50 99.58

- 11. 45 -110.546 -106.30 -83.47 -27.08 46 151.168 109.07 104.44 46.73 47 -22.9133 37.55 42.04 -64.95 48 -2.28696 49.55 52.51 -54.80 49 -72.1597 76.48 76.01 -148.17 50 152.8343 116.72 111.11 41.72 51 -23.2532 -78.49 -59.20 35.95 52 -209.341 -38.57 -24.37 -184.97 53 9.462163 26.62 32.51 -23.05 54 -89.8857 -13.21 -2.24 -87.64 55 202.647 74.56 74.33 128.32 56 161.6751 115.44 110.00 51.68 57 -17.2502 28.46 34.11 -51.36 58 0.170819 83.65 82.26 -82.09 59 16.09925 -0.40 8.93 7.17 60 -29.713 100.98 97.38 -127.10 61 236.9272 17.79 24.81 212.12 62 -443.099 -208.79 -172.88 -270.22 63 -21.784 16.39 23.58 -45.36 64 49.80984 -18.93 -7.24 57.05 65 -11.3658 -6.27 3.81 -15.18 66 37.69982 -44.69 -29.71 67.41 67 309.0884 196.50 180.72 128.37 68 50.8149 45.77 49.22 1.60 69 -77.8881 117.54 111.83 -189.71 70 122.5555 53.56 56.01 66.54 71 316.0288 172.74 159.99 156.04 72 -85.9103 54.70 57.01 -142.92 73 75.61705 151.79 141.71 -66.09 74 188.7903 93.46 90.82 97.97 75 49.20027 -54.16 -37.97 87.17 76 -9.91957 -96.14 -74.60 64.68 77 198.75 24.82 30.94 167.81 78 -136.534 -56.68 -40.17 -96.36 79 163.6507 49.54 52.50 111.15 80 8.557845 124.55 117.95 -109.39 81 120.6977 -14.64 -3.49 124.19 82 -448.908 -56.34 -39.88 -409.03 83 -69.3297 64.70 65.73 -135.06 84 109.3154 -112.20 -88.61 197.92 85 49.79544 33.83 38.79 11.00 86 -147.796 -61.63 -44.49 -103.30 87 -130.939 -47.86 -32.48 -98.46 88 188.7284 -13.13 -2.18 190.91 89 378.684 74.37 74.17 304.52 90 158.6569 18.53 25.44 133.21 91 15.62583 -9.11 1.33 14.29

- 12. 92 92.38695 117.60 111.89 -19.50 93 105.3549 76.23 75.79 29.57 94 -95.2709 -159.32 -129.72 34.45 95 -75.423 -21.36 -9.36 -66.06 96 -11.8085 -37.96 -23.84 12.03 97 -44.2623 -61.65 -44.51 0.24 98 0.92284 45.48 48.96 -48.04 99 21.92639 -23.99 -11.65 33.57 100 105.6518 -180.44 -148.14 253.80 101 164.7287 -17.76 -6.21 170.94 Mean 25.48 18.57 Residual 21191.53

- 13. Beta 0.543533 Rj Rm Alpha Estimated Rj^ Residual S. No. DRREDDY Nifty 1 71.90734 37.21 -8.21 12.01 59.89 2 226.3424 336.79 174.85 51.50 3 133.5373 179.94 89.59 43.94 4 301.1867 111.72 52.51 248.67 5 -154.602 -46.40 -33.43 -121.17 6 -48.2663 -34.21 -26.80 -21.46 7 116.4326 88.88 40.10 76.34 8 -7.53664 -54.27 -37.71 30.17 9 -188.371 -316.92 -180.47 -7.90 10 -143.383 -120.77 -73.85 -69.53 11 21.08407 7.49 -4.14 25.22 12 -180.322 86.84 38.99 -219.31 13 -74.5222 -204.40 -119.31 44.79 14 175.5698 -68.71 -45.56 221.13 15 64.43975 109.34 51.22 13.22 16 15.52167 -112.34 -69.27 84.79 17 123.4577 20.10 2.71 120.74 18 -332.732 -195.71 -114.59 -218.15 19 195.1893 78.26 34.33 160.86 20 15.92664 -28.04 -23.45 39.38 21 -52.519 210.13 106.00 -158.52 22 17.60712 149.83 73.22 -55.62 23 12.49113 -17.18 -17.55 30.04 24 -42.3583 58.51 23.59 -65.95 25 18.72827 6.29 -4.80 23.52 26 -103.832 61.03 24.96 -128.79 27 -32.6262 83.64 37.25 -69.87 28 91.03265 24.43 5.07 85.97 29 -106.83 -99.17 -62.11 -44.72 30 -100.814 35.19 10.91 -111.73 31 96.62338 3.61 -6.25 102.87 32 1.600534 67.43 28.44 -26.84 33 30.10664 52.07 20.09 10.02 34 15.03426 61.34 25.13 -10.09 35 -579.935 103.35 47.96 -627.90 36 123.0332 5.75 -5.08 128.12 37 -78.8299 22.33 3.93 -82.76 38 -63.0036 -164.12 -97.41 34.41 39 9.202195 54.68 21.51 -12.31 40 105.9337 127.95 61.34 44.60 41 197.8328 29.43 7.78 190.05 42 175.5559 69.61 29.63 145.93 43 84.43399 83.39 37.11 47.32 44 157.371 142.37 69.17 88.20

- 14. 45 -61.7119 -106.30 -65.99 4.28 46 77.23069 109.07 51.07 26.16 47 -53.1024 37.55 12.20 -65.30 48 133.6431 49.55 18.72 114.92 49 47.26821 76.48 33.36 13.91 50 164.8647 116.72 55.23 109.63 51 -165.433 -78.49 -50.87 -114.56 52 31.40358 -38.57 -29.17 60.58 53 -26.3154 26.62 6.26 -32.57 54 -178.748 -13.21 -15.39 -163.36 55 105.6139 74.56 32.31 73.30 56 70.4426 115.44 54.53 15.91 57 22.87032 28.46 7.26 15.61 58 55.07555 83.65 37.26 17.82 59 -87.0789 -0.40 -8.43 -78.65 60 41.23852 100.98 46.68 -5.44 61 -93.7959 17.79 1.46 -95.26 62 -99.6721 -208.79 -121.69 22.02 63 -129.44 16.39 0.70 -130.14 64 -257.727 -18.93 -18.50 -239.23 65 -135.083 -6.27 -11.62 -123.47 66 -25.9044 -44.69 -32.50 6.60 67 149.5868 196.50 98.59 50.99 68 75.64312 45.77 16.67 58.97 69 155.9127 117.54 55.67 100.24 70 -97.8773 53.56 20.90 -118.78 71 3.605016 172.74 85.68 -82.07 72 60.24691 54.70 21.52 38.73 73 272.3142 151.79 74.29 198.02 74 25.50705 93.46 42.59 -17.08 75 -57.0992 -54.16 -37.65 -19.45 76 54.70417 -96.14 -60.47 115.17 77 -36.3174 24.82 5.28 -41.60 78 6.944908 -56.68 -39.02 45.96 79 216.5408 49.54 18.71 197.83 80 110.5388 124.55 59.49 51.05 81 -197.495 -14.64 -16.17 -181.33 82 -79.8881 -56.34 -38.84 -41.05 83 64.74057 64.70 26.95 37.79 84 -123.744 -112.20 -69.19 -54.55 85 -6.24967 33.83 10.17 -16.42 86 -58.6611 -61.63 -41.71 -16.95 87 -100.811 -47.86 -34.22 -66.59 88 43.3069 -13.13 -15.35 58.66 89 165.325 74.37 32.21 133.11 90 2.20839 18.53 1.86 0.35 91 -33.1579 -9.11 -13.16 -20.00

- 15. 92 -105.635 117.60 55.71 -161.35 93 -501.556 76.23 33.22 -534.78 94 12.46507 -159.32 -94.81 107.27 95 58.09831 -21.36 -19.82 77.92 96 61.05427 -37.96 -28.85 89.90 97 175.2718 -61.65 -41.72 216.99 98 301.9807 45.48 16.51 285.47 99 -119.928 -23.99 -21.25 -98.68 100 -74.4351 -180.44 -106.28 31.85 101 24.67617 -17.76 -17.86 42.54 Mean 1.88 18.57 Residual 17384.13

- 16. Beta 0.472294 Rj Rm Alpha Estimated Rj^ Residual S. No. HUL Nifty 1 110.2253 37.21 -2.32 15.26 94.97 2 -20.1917 336.79 156.75 -176.94 3 -13.8947 179.94 82.67 -96.57 4 -75.7396 111.72 50.45 -126.19 5 -37.3782 -46.40 -24.23 -13.15 6 54.4147 -34.21 -18.47 72.89 7 70.55838 88.88 39.66 30.90 8 79.27847 -54.27 -27.95 107.22 9 -145.094 -316.92 -152.00 6.90 10 33.49633 -120.77 -59.35 92.85 11 28.79199 7.49 1.22 27.57 12 188.2694 86.84 38.70 149.57 13 -151.582 -204.40 -98.85 -52.73 14 -63.0569 -68.71 -34.77 -28.29 15 112.5 109.34 49.33 63.17 16 6.857143 -112.34 -55.37 62.23 17 107.7844 20.10 7.18 100.61 18 -27.796 -195.71 -94.75 66.95 19 40.33857 78.26 34.65 5.69 20 -1.73871 -28.04 -15.56 13.82 21 -73.7081 210.13 96.93 -170.64 22 70.85934 149.83 68.45 2.41 23 8.996372 -17.18 -10.43 19.43 24 115.4825 58.51 25.32 90.16 25 -87.3156 6.29 0.65 -87.97 26 24.6864 61.03 26.51 -1.82 27 -34.5029 83.64 37.19 -71.69 28 196.3141 24.43 9.22 187.09 29 -183.818 -99.17 -49.15 -134.66 30 -45.1941 35.19 14.30 -59.50 31 -95.9184 3.61 -0.61 -95.31 32 7.960625 67.43 29.53 -21.57 33 -109.664 52.07 22.28 -131.94 34 116.1868 61.34 26.65 89.53 35 9.024495 103.35 46.49 -37.47 36 19.12246 5.75 0.40 18.72 37 -22.6173 22.33 8.23 -30.85 38 -232.332 -164.12 -79.83 -152.51 39 77.20588 54.68 23.51 53.69 40 139.3517 127.95 58.12 81.24 41 297.7721 29.43 11.58 286.19 42 -11.8661 69.61 30.56 -42.43 43 99.50577 83.39 37.07 62.44 44 153.4841 142.37 64.93 88.56

- 17. 45 -130.5 -106.30 -52.52 -77.98 46 113.4743 109.07 49.20 64.28 47 -8.28083 37.55 15.42 -23.70 48 19.01859 49.55 21.09 -2.07 49 174.2408 76.48 33.81 140.43 50 49.72737 116.72 52.81 -3.08 51 50.92838 -78.49 -39.39 90.31 52 -100.798 -38.57 -20.53 -80.27 53 -118.273 26.62 10.26 -128.53 54 137.2385 -13.21 -8.55 145.79 55 -9.95851 74.56 32.90 -42.86 56 190.3846 115.44 52.21 138.18 57 -5.74163 28.46 11.13 -16.87 58 143.5714 83.65 37.19 106.38 59 -44.368 -0.40 -2.51 -41.86 60 -103.692 100.98 45.38 -149.07 61 -84.5564 17.79 6.09 -90.65 62 -36.9427 -208.79 -100.92 63.98 63 -101.813 16.39 5.43 -107.24 64 -134.866 -18.93 -11.26 -123.61 65 -89.0899 -6.27 -5.27 -83.82 66 -97.1387 -44.69 -23.42 -73.72 67 176.3815 196.50 90.49 85.89 68 26.84256 45.77 19.30 7.54 69 -61.3878 117.54 53.20 -114.58 70 -11.9612 53.56 22.98 -34.94 71 105.8927 172.74 79.27 26.63 72 -49.5784 54.70 23.52 -73.10 73 156.2897 151.79 69.37 86.92 74 111.2114 93.46 41.83 69.38 75 -34.7826 -54.16 -27.90 -6.89 76 -148.804 -96.14 -47.72 -101.08 77 -12.6205 24.82 9.41 -22.03 78 -69.6753 -56.68 -29.09 -40.59 79 70.25925 49.54 21.08 49.18 80 86.16922 124.55 56.51 29.66 81 -86.2359 -14.64 -9.23 -77.01 82 -90.651 -56.34 -28.93 -61.73 83 111.3583 64.70 28.24 83.12 84 -138.306 -112.20 -55.30 -83.00 85 50.18888 33.83 13.66 36.53 86 -101.926 -61.63 -31.42 -70.50 87 -120.72 -47.86 -24.92 -95.80 88 -112.757 -13.13 -8.52 -104.24 89 152.381 74.37 32.81 119.57 90 -13.1868 18.53 6.43 -19.62 91 72.78782 -9.11 -6.62 79.40

- 18. 92 -25.6983 117.60 53.23 -78.93 93 44.91669 76.23 33.69 11.23 94 -64.1829 -159.32 -77.56 13.38 95 -11.1413 -21.36 -12.41 1.26 96 89.97079 -37.96 -20.25 110.22 97 45.16292 -61.65 -31.43 76.59 98 -71.0076 45.48 19.17 -90.17 99 -48.4379 -23.99 -13.64 -34.79 100 -54.5929 -180.44 -87.53 32.94 101 132.2378 -17.76 -10.70 142.94 Mean 6.46 18.57 Residual 7877.60

- 19. Beta 1.286323 Rj Rm Alpha Estimated Rj^ Residual S. No. ICICIBANK Nifty 1 23.67088 37.21 7.44 55.30 -31.63 2 653.4641 336.79 440.66 212.80 3 527.8846 179.94 238.91 288.98 4 19.2337 111.72 151.15 -131.92 5 -255.712 -46.40 -52.24 -203.47 6 -85.2935 -34.21 -36.56 -48.73 7 329.1341 88.88 121.76 207.37 8 -141.743 -54.27 -62.37 -79.37 9 -306.526 -316.92 -400.23 93.70 10 -243.518 -120.77 -147.91 -95.61 11 65.14985 7.49 17.08 48.07 12 13.51952 86.84 119.14 -105.62 13 -241.035 -204.40 -255.49 14.45 14 -124.147 -68.71 -80.95 -43.20 15 171.8742 109.34 148.09 23.79 16 -351.787 -112.34 -137.06 -214.72 17 -61.2031 20.10 33.29 -94.50 18 -88.8351 -195.71 -244.31 155.47 19 61.4053 78.26 108.11 -46.71 20 -72.3895 -28.04 -28.63 -43.76 21 216.4721 210.13 277.74 -61.27 22 235.0293 149.83 200.16 34.87 23 -50.5256 -17.18 -14.66 -35.86 24 -35.1667 58.51 82.70 -117.87 25 47.39161 6.29 15.52 31.87 26 73.86961 61.03 85.94 -12.07 27 17.57778 83.64 115.02 -97.45 28 34.50271 24.43 38.87 -4.36 29 -142.302 -99.17 -120.12 -22.18 30 66.76388 35.19 52.70 14.06 31 26.20207 3.61 12.08 14.12 32 147.1531 67.43 94.18 52.97 33 133.0189 52.07 74.42 58.60 34 205.172 61.34 86.34 118.83 35 94.46601 103.35 140.38 -45.91 36 162.2054 5.75 14.84 147.36 37 -110.735 22.33 36.17 -146.90 38 -110.013 -164.12 -203.67 93.65 39 5.500382 54.68 77.78 -72.28 40 -51.1012 127.95 172.03 -223.13 41 11.81781 29.43 45.30 -33.48 42 49.63678 69.61 96.98 -47.35 43 104.823 83.39 114.70 -9.88 44 94.94585 142.37 190.58 -95.63

- 20. 45 -205.617 -106.30 -129.30 -76.32 46 298.6301 109.07 147.74 150.89 47 -118.215 37.55 55.74 -173.95 48 306.377 49.55 71.18 235.19 49 103.1501 76.48 105.82 -2.67 50 107.0149 116.72 157.58 -50.56 51 -100.356 -78.49 -93.52 -6.83 52 37.49015 -38.57 -42.17 79.66 53 66.50042 26.62 41.69 24.81 54 -33.7687 -13.21 -9.55 -24.22 55 111.6115 74.56 103.34 8.27 56 163.3172 115.44 155.93 7.38 57 53.65939 28.46 44.05 9.61 58 73.16531 83.65 115.04 -41.88 59 10.31776 -0.40 6.92 3.40 60 112.8834 100.98 137.34 -24.45 61 73.4375 17.79 30.33 43.11 62 -322.286 -208.79 -261.13 -61.16 63 75.73405 16.39 28.52 47.21 64 112.2716 -18.93 -16.91 129.18 65 -98.0173 -6.27 -0.62 -97.40 66 -1.62464 -44.69 -50.04 48.42 67 217.593 196.50 260.21 -42.61 68 15.06073 45.77 66.32 -51.26 69 249.3888 117.54 158.63 90.76 70 165.6093 53.56 76.34 89.27 71 154.9482 172.74 229.64 -74.69 72 71.92807 54.70 77.80 -5.88 73 106.1254 151.79 202.69 -96.56 74 166.4053 93.46 127.66 38.74 75 -113.047 -54.16 -62.23 -50.82 76 -124.983 -96.14 -116.23 -8.75 77 -4.8032 24.82 39.37 -44.17 78 80.2847 -56.68 -65.47 145.75 79 66.24108 49.54 71.16 -4.92 80 -15.5671 124.55 167.66 -183.22 81 -46.1867 -14.64 -11.39 -34.80 82 -27.5766 -56.34 -65.04 37.46 83 25.60455 64.70 90.66 -65.06 84 25.27233 -112.20 -136.88 162.15 85 -4.77396 33.83 50.95 -55.72 86 272.7031 -61.63 -71.84 344.54 87 -108.959 -47.86 -54.12 -54.84 88 -10.56 -13.13 -9.45 -1.11 89 459.292 74.37 103.11 356.19 90 22.99887 18.53 31.27 -8.27 91 -147.181 -9.11 -4.28 -142.90

- 21. 92 -5.90551 117.60 158.72 -164.62 93 500.4184 76.23 105.49 394.93 94 -388.685 -159.32 -197.49 -191.19 95 -189.599 -21.36 -20.04 -169.56 96 -16.908 -37.96 -41.39 24.49 97 -145.304 -61.65 -71.86 -73.44 98 -101.291 45.48 65.95 -167.24 99 -48.9426 -23.99 -23.41 -25.53 100 -72.5518 -180.44 -224.66 152.11 101 191.5734 -17.76 -15.40 206.98 Mean 31.33 18.57 Residual 14455.43

- 22. Beta 0.96551 Rj Rm Alpha Estimated Rj^ Residual S. No. RELIANCE Nifty 1 -31.2426 37.21 9.09 45.01 -76.26 2 309.3592 336.79 334.27 -24.91 3 221.5445 179.94 182.83 38.72 4 245.2036 111.72 116.96 128.25 5 -52.1759 -46.40 -35.71 -16.47 6 88.43642 -34.21 -23.94 112.37 7 103.9799 88.88 94.90 9.08 8 -210.258 -54.27 -43.31 -166.95 9 -353.287 -316.92 -296.90 -56.38 10 -104.962 -120.77 -107.52 2.55 11 -38.7588 7.49 16.32 -55.08 12 64.34861 86.84 92.93 -28.58 13 -153.95 -204.40 -188.26 34.31 14 -96.8445 -68.71 -57.25 -39.59 15 184.6765 109.34 114.66 70.02 16 -96.2796 -112.34 -99.38 3.10 17 -7.47912 20.10 28.49 -35.97 18 -168.092 -195.71 -179.87 11.78 19 13.06612 78.26 84.65 -71.59 20 29.24779 -28.04 -17.99 47.24 21 253.6498 210.13 211.98 41.67 22 206.3236 149.83 153.75 52.58 23 42.71455 -17.18 -7.50 50.22 24 136.1559 58.51 65.58 70.58 25 -39.743 6.29 15.16 -54.90 26 152.0131 61.03 68.01 84.00 27 167.0437 83.64 89.84 77.20 28 15.79298 24.43 32.68 -16.88 29 -12.2507 -99.17 -86.66 74.41 30 90.98138 35.19 43.06 47.92 31 24.78203 3.61 12.58 12.21 32 18.05873 67.43 74.20 -56.14 33 55.55793 52.07 59.36 -3.80 34 58.42395 61.34 68.31 -9.89 35 169.8611 103.35 108.87 60.99 36 -91.7677 5.75 14.64 -106.41 37 132.9351 22.33 30.65 102.29 38 -80.7078 -164.12 -149.37 68.66 39 343.396 54.68 61.89 281.51 40 146.4344 127.95 132.63 13.80 41 -8.48858 29.43 37.50 -45.99 42 -236.681 69.61 76.30 -312.98 43 81.56599 83.39 89.60 -8.03 44 110.4787 142.37 146.55 -36.07

- 23. 45 -46.9536 -106.30 -93.55 46.60 46 123.6864 109.07 114.40 9.29 47 27.38324 37.55 45.34 -17.96 48 113.5476 49.55 56.93 56.61 49 241.2336 76.48 82.93 158.30 50 15.79396 116.72 121.78 -105.99 51 -39.5568 -78.49 -66.70 27.14 52 -22.0045 -38.57 -28.15 6.15 53 53.99211 26.62 34.79 19.20 54 -3.14784 -13.21 -3.66 0.52 55 38.6423 74.56 81.07 -42.43 56 -27.4402 115.44 120.55 -147.99 57 26.06681 28.46 36.57 -10.50 58 106.591 83.65 89.86 16.73 59 -32.522 -0.40 8.70 -41.22 60 165.4835 100.98 106.59 58.89 61 -0.4188 17.79 26.27 -26.69 62 -220.306 -208.79 -192.50 -27.81 63 -25.8712 16.39 24.91 -50.78 64 -36.0195 -18.93 -9.19 -26.83 65 -12.5234 -6.27 3.04 -15.56 66 -25.7659 -44.69 -34.06 8.29 67 211.3951 196.50 198.81 12.58 68 1.480111 45.77 53.28 -51.80 69 115.3222 117.54 122.57 -7.25 70 129.0741 53.56 60.80 68.27 71 143.5038 172.74 175.87 -32.36 72 121.8837 54.70 61.90 59.98 73 105.6932 151.79 155.64 -49.95 74 105.593 93.46 99.33 6.26 75 -15.7497 -54.16 -43.20 27.45 76 -67.7863 -96.14 -83.74 15.95 77 85.94801 24.82 33.05 52.89 78 -92.2302 -56.68 -45.64 -46.59 79 41.88954 49.54 56.92 -15.03 80 101.2429 124.55 129.35 -28.10 81 34.64445 -14.64 -5.05 39.69 82 11.97652 -56.34 -45.31 57.29 83 54.75752 64.70 71.56 -16.80 84 -111.581 -112.20 -99.24 -12.34 85 26.86907 33.83 41.75 -14.88 86 -64.0201 -61.63 -50.42 -13.60 87 -87.7123 -47.86 -37.12 -50.59 88 -29.4299 -13.13 -3.59 -25.84 89 30.98967 74.37 80.90 -49.91 90 -23.9059 18.53 26.98 -50.88 91 67.25297 -9.11 0.29 66.96

- 24. 92 167.6887 117.60 122.64 45.05 93 -46.2585 76.23 82.69 -128.95 94 -179.528 -159.32 -144.73 -34.79 95 -28.9791 -21.36 -11.54 -17.44 96 -161.682 -37.96 -27.57 -134.12 97 -72.8014 -61.65 -50.43 -22.37 98 174.4818 45.48 53.00 121.48 99 -144.936 -23.99 -14.07 -130.87 100 -71.1422 -180.44 -165.12 93.98 101 92.04368 -17.76 -8.06 100.10 Mean 27.02 18.57 Residual 5465.65

- 25. Beta 1.284755 Rj Rm Alpha Estimated Rj^ Residual S. No. TAJGVK Nifty 1 63.66559 37.21 10.71 58.51 5.15 2 790.4 336.79 443.40 347.00 3 216.5792 179.94 241.89 -25.31 4 140.68 111.72 154.24 -13.56 5 -66.4452 -46.40 -48.90 -17.55 6 -42.3077 -34.21 -33.24 -9.07 7 59.19283 88.88 124.89 -65.70 8 -64.8993 -54.27 -59.01 -5.88 9 -519.134 -316.92 -396.46 -122.67 10 -78.9207 -120.77 -144.45 65.53 11 -38.5201 7.49 20.33 -58.85 12 -137.06 86.84 122.28 -259.34 13 -315.767 -204.40 -251.90 -63.87 14 -75.0999 -68.71 -77.57 2.47 15 523.9598 109.34 151.19 372.77 16 -249.905 -112.34 -133.62 -116.29 17 -106.795 20.10 36.53 -143.33 18 -220.884 -195.71 -240.73 19.85 19 146.6835 78.26 111.26 35.42 20 120.5422 -28.04 -25.32 145.86 21 23.38767 210.13 280.68 -257.29 22 5.124555 149.83 203.20 -198.07 23 -159.259 -17.18 -11.37 -147.89 24 53.7891 58.51 85.88 -32.09 25 -70.6525 6.29 18.78 -89.44 26 -64.7717 61.03 89.12 -153.89 27 -51.7582 83.64 118.16 -169.92 28 -60.1253 24.43 42.10 -102.22 29 -102.792 -99.17 -116.70 13.91 30 -93.2218 35.19 55.91 -149.14 31 -16.6667 3.61 15.35 -32.01 32 -37.831 67.43 97.34 -135.18 33 76.45875 52.07 77.60 -1.14 34 59.1133 61.34 89.51 -30.40 35 224.1648 103.35 143.48 80.68 36 -91.358 5.75 18.10 -109.46 37 -262.756 22.33 39.40 -302.15 38 7.519709 -164.12 -200.14 207.66 39 -83.2957 54.68 80.96 -164.26 40 275.6419 127.95 175.10 100.54 41 -123.734 29.43 48.52 -172.25 42 408.0067 69.61 100.14 307.86 43 206.91 83.39 117.84 89.07 44 393.7662 142.37 193.62 200.14

- 26. 45 -983.607 -106.30 -125.87 -857.74 46 82.71028 109.07 150.84 -68.13 47 376.4964 37.55 58.95 317.55 48 62.70619 49.55 74.37 -11.67 49 51.99182 76.48 108.97 -56.98 50 127.3163 116.72 160.67 -33.35 51 125.6471 -78.49 -90.13 215.78 52 -19.1027 -38.57 -38.84 19.74 53 -2.945 26.62 44.91 -47.86 54 125.9531 -13.21 -6.26 132.21 55 73.7555 74.56 106.49 -32.74 56 443.5993 115.44 159.02 284.58 57 321.8824 28.46 47.27 274.61 58 59.64804 83.65 118.18 -58.53 59 354.0984 -0.40 10.19 343.91 60 208.3529 100.98 140.45 67.91 61 -50.6966 17.79 33.57 -84.27 62 -203.359 -208.79 -257.53 54.17 63 139.5 16.39 31.76 107.74 64 -123.364 -18.93 -13.61 -109.75 65 7.22076 -6.27 2.66 4.56 66 -101.24 -44.69 -46.70 -54.54 67 205.1613 196.50 263.17 -58.00 68 401.7223 45.77 69.52 332.21 69 468.8623 117.54 161.71 307.15 70 -34.0364 53.56 79.52 -113.56 71 36.88156 172.74 232.63 -195.75 72 308.7653 54.70 80.99 227.78 73 364.1278 151.79 205.72 158.41 74 21 93.46 130.79 -109.79 75 165.5761 -54.16 -58.87 224.45 76 -207.529 -96.14 -112.81 -94.72 77 59.25926 24.82 42.60 16.66 78 -45.6057 -56.68 -62.11 16.51 79 12.96519 49.54 74.35 -61.38 80 -26.7606 124.55 170.73 -197.49 81 11.37441 -14.64 -8.10 19.47 82 -59.4595 -56.34 -61.68 2.22 83 -117.073 64.70 93.83 -210.90 84 -14.4578 -112.20 -133.43 118.98 85 -50.7692 33.83 54.17 -104.94 86 0.00001 -61.63 -68.47 68.47 87 -184.54 -47.86 -50.78 -133.76 88 29 -13.13 -6.17 35.17 89 -55.3259 74.37 106.26 -161.58 90 17.41935 18.53 34.51 -17.09 91 0.00001 -9.11 -0.99 0.99

- 27. 92 19.67213 117.60 161.80 -142.13 93 21.01751 76.23 108.64 -87.62 94 40.34483 -159.32 -193.97 234.32 95 21.05263 -21.36 -16.74 37.79 96 16 -37.96 -38.07 54.07 97 98.07692 -61.65 -68.50 166.57 98 0.00001 45.48 69.14 -69.14 99 23.52941 -23.99 -20.11 43.64 100 0.00001 -180.44 -221.11 221.11 101 206.8966 -17.76 -12.11 219.00 Mean 34.57 18.57 Residual 30430.53

- 28. Beta 1.329434 Rj Rm Alpha Estimated Rj^ Residual S. No. TATAMOTORS Nifty 1 186.4925 37.21 5.30 54.77 131.72 2 457.9984 336.79 453.05 4.95 3 422.629 179.94 244.53 178.10 4 249.1628 111.72 153.83 95.33 5 -2.80655 -46.40 -56.38 53.57 6 -76.5718 -34.21 -40.17 -36.40 7 201.1687 88.88 123.46 77.71 8 -231.082 -54.27 -66.84 -164.24 9 -608.375 -316.92 -416.02 -192.35 10 -262.943 -120.77 -155.25 -107.69 11 109.7398 7.49 15.26 94.48 12 -63.5137 86.84 120.75 -184.26 13 -311.933 -204.40 -266.44 -45.50 14 -160.361 -68.71 -86.04 -74.32 15 80.55243 109.34 150.67 -70.11 16 -133.048 -112.34 -144.04 11.00 17 1.54407 20.10 32.02 -30.48 18 -68.6615 -195.71 -254.88 186.22 19 15.48229 78.26 109.35 -93.87 20 -40.219 -28.04 -31.98 -8.24 21 -29.4246 210.13 284.66 -314.09 22 128.5073 149.83 204.49 -75.98 23 4.032027 -17.18 -17.54 21.57 24 52.2829 58.51 83.09 -30.80 25 -135.768 6.29 13.66 -149.43 26 6.305288 61.03 86.44 -80.13 27 38.80802 83.64 116.49 -77.68 28 -83.4143 24.43 37.78 -121.20 29 -130.753 -99.17 -126.54 -4.22 30 -29.7135 35.19 52.08 -81.79 31 135.6238 3.61 10.10 125.52 32 -26.9647 67.43 94.95 -121.92 33 -47.2786 52.07 74.52 -121.80 34 22.48626 61.34 86.85 -64.36 35 167.8593 103.35 142.70 25.16 36 -79.7132 5.75 12.95 -92.67 37 10.35467 22.33 34.99 -24.64 38 -206.19 -164.12 -212.88 6.69 39 25.36889 54.68 78.00 -52.63 40 170.0319 127.95 175.41 -5.38 41 182.5111 29.43 44.43 138.08 42 101.1019 69.61 97.85 3.25 43 210.7233 83.39 116.16 94.56 44 213.0508 142.37 194.58 18.47

- 29. 45 -139.822 -106.30 -136.02 -3.80 46 189.3163 109.07 150.31 39.01 47 -48.534 37.55 55.22 -103.75 48 156.3991 49.55 71.18 85.22 49 -21.0599 76.48 106.98 -128.04 50 56.73519 116.72 160.48 -103.74 51 -0.58013 -78.49 -99.04 98.46 52 -156.949 -38.57 -45.97 -110.98 53 -67.6844 26.62 40.70 -108.38 54 -2.0188 -13.21 -12.26 10.24 55 53.72208 74.56 104.42 -50.70 56 192.4895 115.44 158.77 33.72 57 40.17359 28.46 43.14 -2.97 58 38.86329 83.65 116.51 -77.65 59 -92.1768 -0.40 4.77 -96.94 60 135.0513 100.98 139.55 -4.50 61 44.50504 17.79 28.96 15.54 62 -268.501 -208.79 -272.26 3.76 63 -33.2201 16.39 27.09 -60.31 64 -54.24 -18.93 -19.86 -34.38 65 -26.6334 -6.27 -3.03 -23.61 66 181.4401 -44.69 -54.10 235.54 67 127.7689 196.50 266.54 -138.77 68 109.1055 45.77 66.16 42.95 69 261.7011 117.54 161.56 100.14 70 112.7202 53.56 76.51 36.21 71 292.9615 172.74 234.95 58.02 72 168.7453 54.70 78.03 90.72 73 184.1584 151.79 207.10 -22.94 74 166.7662 93.46 129.56 37.21 75 -37.7771 -54.16 -66.70 28.92 76 -55.164 -96.14 -122.51 67.35 77 74.60938 24.82 38.30 36.31 78 -57.9926 -56.68 -70.05 12.06 79 -55.3191 49.54 71.16 -126.48 80 202.6943 124.55 170.89 31.81 81 111.9335 -14.64 -14.16 126.09 82 -61.0753 -56.34 -69.60 8.53 83 117.0732 64.70 91.32 25.76 84 -218.533 -112.20 -143.85 -74.68 85 339.8844 33.83 50.27 289.61 86 -74.361 -61.63 -76.63 2.27 87 29.52381 -47.86 -58.32 87.85 88 -130.693 -13.13 -12.16 -118.54 89 156.8972 74.37 104.18 52.72 90 302.8543 18.53 29.93 272.92 91 -52.2989 -9.11 -6.81 -45.49

- 30. 92 277.3585 117.60 161.65 115.71 93 273.7147 76.23 106.64 167.07 94 -102.517 -159.32 -206.50 103.98 95 81.471 -21.36 -23.10 104.57 96 159.6154 -37.96 -45.17 204.78 97 -289.605 -61.65 -76.65 -212.95 98 105.5556 45.48 65.77 39.78 99 189.2802 -23.99 -26.58 215.86 100 -438.484 -180.44 -234.57 -203.91 101 114.3161 -17.76 -18.31 132.62 Mean 29.99 18.57 Residual 11921.58

- 31. Residual Std Dev Stock Beta Varience Return Portflio Wt β2xWj2 σεj2xWj2 2 Stocks σεj ACC 0.883421 10668.89 135.54 68.62 0.14 0.016233 221.9146 BPCL 0.87247 21191.53 169.42 69.24 0.05 0.002024 56.33488 DRREDDY 0.543533 17384.13 142.48 66.78 0.21 0.013031 766.7829 HUL 0.472294 7877.60 100.39 58.08 0.36 0.029557 1043.826 ICICIBANK 1.286323 14455.43 175.45 78.18 0.07 0.008689 75.911 RELIANCE 0.96551 5465.65 121.10 61.51 0.16 0.023189 135.9595 TAJGVK 1.284755 30430.53 216.15 44.17 0.00 0 0 TATAMOTORS 1.329434 11921.58 171.36 82.90 0.00 0 0 Nifty 99.34 52.72 0.092722 2300.729 47.96591 Return R 64.00 Beta βP 0.70396158 2 σM Mkt Varience 99.34 2 σεp Unsystematic Risk 2300.72872 Portfolio σ2 Var P 2309.939659

- 32. Risk Free (Rf) 5.00 σM2 99.34 Excess Return Unsystemati Return (Ri) Beta Ri-Rf to Beta(Ri- Rank c Risk Rf)/Beta ACC 10668.89 68.62 0.88 63.62 72.02 4 BPCL 21191.53 69.24 0.87 64.24 73.63 3 DRREDDY 17384.13 66.78 0.54 61.78 113.66 1 HUL 7877.60 58.08 0.47 53.08 112.39 2 ICICIBANK 14455.43 78.18 1.29 73.18 56.89 7 RELIANCE 5465.65 61.51 0.97 56.51 58.53 6 TAJGVK 30430.53 44.17 1.28 39.17 30.49 8 TATAMOTORS 11921.58 82.90 1.33 77.90 58.59 5 Excess Return Unsystemati (Ri-Rf) *Beta Rank Stock c Risk Return (Ri) Beta Ri-Rf to Beta(Ri- / Var Rf)/Beta 1 DRREDDY 17384.13 66.77835 0.543533 61.77835 113.6607 0.001932 2 HUL 7877.602 58.08119 0.472294 53.08119 112.3901 0.003182 3 BPCL 21191.53 69.24014 0.87247 64.24014 73.63021 0.002645 4 ACC 10668.89 68.62255 0.883421 63.62255 72.0184 0.005268 5 TATAMOTORS 11921.58 82.89746 1.329434 77.89746 58.59447 0.008687 6 RELIANCE 5465.648 61.50791 0.96551 56.50791 58.52648 0.009982 7 ICICIBANK 14455.43 78.17501 1.286323 73.17501 56.88696 0.006512 8 TAJGVK 30430.53 44.16712 1.284755 39.16712 30.48607 0.001654 0.039861 Return R 67.7085 Beta βP 0.931681 Mkt Varience σM2 99.34 2 Unsystematic Risk σεp 1476.296 Portfolio Var σP2 1490.799

- 33. mkt var*cell J14/(1+mkt (Beta/residual var)*{(Ri- Ci= var*cell K14 Zi= Rf)/Beta-C*)} Optimum value of Ci for which all securities used in the calculation Where C* = of Ci have excess return-to-beta above Ci Note In cell J14 and K14 the sum is till the securities which is last used not the whole series (i=1 to i). Eg, if we are calculating for ACC, then sum will be till ACC from DrReddy, i.e. from Rank 1 to Rank 4 only, not till Rank 8 Weights Weights of the securities will be calculated by Z value of that security divided by Total Z value. And the Total Z value will be till the CutOff C, i.e. C*, Z not to be calculated for the Securities which do not have there C less than their Excess return over Beta ∑{(Ri-Rf) Weights 2 2 2 2 Beta^2/ Var ∑{Beta^2/ Var} Ci Zi β xWj σεj xWj *Beta / Var} Alloted 1.69941E-05 0.001932 1.69941E-05 0.191556 0.003548 8.63% 0.002202 129.5649 2.8316E-05 0.005114 4.53101E-05 0.505742 0.006708 16.32% 0.005943 209.8952 3.59202E-05 0.007759 8.12303E-05 0.764581 0.003 7.30% 0.004057 112.9319 7.31503E-05 0.013027 0.000154381 1.274538 0.005858 14.25% 0.015858 216.7834 0.000148252 0.021714 0.000302632 2.094059 0.006301 15.33% 0.041547 280.2434 0.000170558 0.031696 0.00047319 3.007268 0.009808 23.87% 0.053096 311.3087 0.000114464 0.038207 0.000587654 3.586127 0.004743 11.54% 0.022041 192.5617 5.42414E-05 0.039861 0.000641896 3.722383 0.00113 2.75% 0.001248 23.00677 0.000641896 0.041094 100%