Financial accounting questions

•

2 gefällt mir•1,953 views

These are financial accounting questions for students to revise and get homework answers to

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Financial accounting questions

Ähnlich wie Financial accounting questions (20)

Mehr von allhomeworktutors

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Financial accounting questions

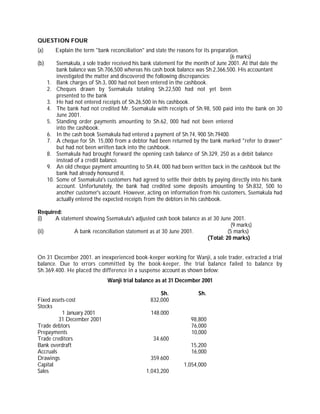

- 1. QUESTION FOUR (a) Explain the term "bank reconciliation" and state the reasons for its preparation. (6 marks) (b) Ssemakula, a sole trader received his bank statement for the month of June 2001. At that date the bank balance was Sh.706,500 whereas his cash book balance was Sh.2,366,500. His accountant investigated the matter and discovered the following discrepancies: 1. Bank charges of Sh.3, 000 had not been entered in the cashbook. 2. Cheques drawn by Ssemakula totaling Sh.22,500 had not yet been presented to the bank 3. He had not entered receipts of Sh.26,500 in his cashbook. 4. The bank had not credited Mr. Ssemakula with receipts of Sh.98, 500 paid into the bank on 30 June 2001. 5. Standing order payments amounting to Sh.62, 000 had not been entered into the cashbook. 6. In the cash book Ssemakula had entered a payment of Sh.74, 900 Sh.79400. 7. A cheque for Sh. 15,000 from a debtor had been returned by the bank marked "refer to drawer" but had not been written back into the cashbook. 8. Ssemakula had brought forward the opening cash balance of Sh.329, 250 as a debit balance instead of a credit balance. 9. An old cheque payment amounting to Sh.44, 000 had been written back in the cashbook but the bank had already honoured it. 10. Some of Ssemakula's customers had agreed to settle their debts by paying directly into his bank account. Unfortunately, the bank had credited some deposits amounting to Sh.832, 500 to another customer's account. However, acting on information from his customers, Ssemakula had actually entered the expected receipts from the debtors in his cashbook. Required: (i) A statement showing Ssemakula's adjusted cash book balance as at 30 June 2001. (9 marks) (ii) A bank reconciliation statement as at 30 June 2001. (5 marks) (Total: 20 marks) On 31 December 2001. an inexperienced book-keeper working for Wanji, a sole trader, extracted a trial balance. Due to errors committed by the book-keeper, the trial balance failed to balance by Sh.369.400. He placed the difference in a suspense account as shown below: Wanji trial balance as at 31 December 2001 Sh. Sh. Fixed assets-cost 832,000 Stocks 1 January 2001 148.000 31 December 2001 98,800 Trade debtors 76,000 Prepayments 10,000 Trade creditors 34.600 Bank overdraft 15,200 Accruals 16,000 Drawings 359.600 Capital 1,054,000 Sales 1,043,200

- 2. Provision for depreciation 166,400 Purchases 733.000 Operating expenses 126.000 Provision for doubtful debts 3,800 Discounts received 5,000 Discounts allowed 5,800 Suspense account 369.400 2,548 400 248 400 Investigations carried out after preparing the above trial balance detected the following errors: 1. The total of the sales day book for December 2001 was overcast by Sh.25,700. 2. On 2 July 2001 the business purchased office equipment for Sh.40.000. These were debited to purchases account. 3. Depreciation on the equipment is at the rate of 10% per annum on cost and based on the period (months) of usage in the year. 4. A payment to a creditor by cheque of Sh.8.500 was erroneously credited to the creditor's account. 5. A payment of Sh.4.500 for telephone expenses was debited to telephone account as Sh.5.400. 6. An amount of Sh.15.000 received from a debtor was not posted to the debtor's account from the cash book. 7. An amount of discounts received of Sh.2.500 was debited to discounts allowed account. 8. Purchases day book for October 2001 was undercast by Sh.28,000. 9. Assume the business had reported a net profit of Sh.85,800 before adjusting for the above errors. Required: (a) The adjusted trial balance and the correct balance of the suspense account (6 marks) (b) Journal entries to correct the errors (Narrations not required) (6 marks) (c) Suspense account starting with the balance determined in the adjusted trial balance in (a)above. (4 marks) (d) The adjusted net profit for the year. (4 marks) (Total: 20 marks) QUESTION TWO The following information has been extracted from the accounts of Madaraka Investments Ltd. for the year ended 31 December 2001. Comparable figures for the previous year are also shown. Profit statement for the year ended 31 December 2001 2000 Sh. `000' Sh'000' Sales 115,200 72.000 Cost of goods sold 70800 42,000 Gross profit 44,400 30,000 Less: Trading expenses 19 800 16,200 24,600 13,800 Less: Debenture interest 900 900 Net profit before taxation 23,700 12,900 Less: Corporation tax 11 520 5.760 Net profit after taxation 12.180 7.140 Less: Ordinary share dividend 6.300 4,500 Undistributed profit for the year 5,880 2,640

- 3. Balance sheet as at 31 December 2001 2000 Sh.'000' Sh.'000' Sh.'000' Sh.'000' Assets employed: Fixed assets at cost 44.400 33.600 Depreciation 9000 7,200 35,400 26,400 Current assets: Stock 19,800 14,400 Debtors 12,600 9.000 Cash - 32 400 2,880 26,280 67.800 52.680 Less: Current liabilities Creditors 7,200 5.220 Taxation 11,520 5,760 Proposed dividends 6,300 4,500 Bank overdraft 2,340 27,360 - 15.480 Net assets 40 440 3 7,.200 Financed by: Ordinary share capital Authorised, issued and fully paid (Sh.25 per share) 18,000 18,000 Undistributed profits 16 080 10,200 34,080 28.200 Long-tern loan: 6 360 9.000 10% debentures (secured) 40 440 37 200 Required: (a) Calculate six accounting ratios for both 2000 and 2001 that would help in assessing the profitability and liquidity positions of Madaraka Investments Ltd. (12 marks) (b) Comment on Madaraka Investment's liquidity position. (4 marks) (c) Comment on Madaraka Investment's profitability position. (4 marks) (Total: 20 marks) QUESTION THREE Kyamba, Onyango and Wakil were partners in a manufacturing and retail business and shared profits and losses in the ratio 2:2:1 respectively. Given below is the balance sheet of the partnership as at 31 March 2001:

- 4. Balance sheet as at 31 March 2001 Assets Sh. Sh. Non-current assets: Fixed assets 465,000 Current assets: Stocks 294,000 Debtors 209,000 503,000 968 000 Capital and liabilities: Capital accounts: Kyamba 160,000 Onyango 140,000 Wakil 200 000 500,000 Current accounts: Kyamba 65,300 Onyango 49.000 Wakil 53.000 167,300 667,300 Current liabilities: Bank overdraft 48,700 Trade creditors 252,000 300,700 968 000 Additional information: 1. On 1 April 2001. Wakil retired from the partnership and was to start a business as a sole trader while Kyamba and Onyango continued in partnership. On retirement of Wakil, the manufacturing business was transferred to hum while Kyamba and Onyango continued with the retail business. 2. The assets and liabilities transferred to Wakil were as follows: Net book value Transfer value Sh. Sh. Fixed assets 260,000 306,000 Stocks 166,000 157,000 Debtors 172,000 165,000 Creditors 156,000 156,000 Wakil obtained a loan from a commercial bank and paid into the partnership the net amount due from him. On retirement of Wakil from the partnership, goodwill was valued at Sh.200, 000 but was not to be maintained in the books of the partnership of Kyamba and Onyango. After retirement of Wakil on 1 April 2001. Kyamba and Onyango agreed on the following terms and details of the new partnership:

- 5. Kyamba and Onyango to introduce additional capital of Sh.48,000 and Sh.68,000 respectively. Each partner was entitled to interest on capital at 10% per annum with effect from 1 April 2001 and the balance of the profits was to be shared equally after allowing for annual salaries of Sh.72,000 to Kyamba and Sh.60,000 to Onyango. 5. The profit of the new partnership before interest on capitals and partners' salaries was Sh.240, 000 for the year ended 31 March 2002. 6. The profits made by the new partnership increased stocks by Sh.100.000; debtors by Sh.90.000 and bank balance by Sh.50, 000. 7. Drawings by the partners in the year were Kyamba Sh.85, 000 and OnyanSh go.70,000. Required: (a) Profit and loss and appropriation account for the year ended 31 March 2002. (4 marks) (b) Capital accounts for the year ended 31 March 2002. (4 marks) (c) Current accounts for the year ended 31 March 2002. (8 marks) (d) Balance sheet of the new partnership as at 31 March 2002. (4 marks) (Total: 20 marks) QUESTIONFOUR (a) State the reasons for maintaining control accounts. (4 marks) (b) The following information has been extracted from the books of Mutero Traders Limited for the month of April 2002. Balances as at I April 2002: Sh. Sales ledger - Debit balances 838,000 - Credit balances 184,000 Purchases ledger -Debit balances 196.000 - Credit balances 598.000 Transactions during the month: Sales on credit 8,784.000 Purchases on credit 7.849.000 Returns inwards 248,000 Returns outwards 179,000 Cheques received from trade debtors 2.968.000 Cash paid to trade creditors 4,674.000 Cheques paid to trade creditors 1.393.000 Bad debts written-off 139.000 Discounts allowed to trade debtors 162.000 Discounts received from trade creditors 231.000 Credit sales off-set against credit purchases 356.000 Credit purchase of a motor vehicle posted in the purchases ledger 598.000 Dishonoured cheques from trade debtors 193,000 Cash received to replace dishonoured cheques from trade debtor 106.000 An invoice to trade debtors of Sh.174,000 posted as 147.000 Balances as at 30 April 2002:

- 6. Sales ledger credit balances 123.000 Purchases ledger debit balances 177,000 Required: The sales ledger and purchases ledger control accounts for the month ended 30 April 2002. (16 marks) (Total: 20 marks) QUESTIONFIVE (a) Distinguish between each of the following pairs of terms: (i) Receipts and revenue. (4 marks) (ii) Balance sheet and statement of affairs. (4 marks) (iii) Cash basis of accounting and accrual basis of accounting. (4 marks) (iv)Materiality and substance over form. (4 marks) (b) What conflicts may exist in the application of the fundamental accounting concepts? (4 marks) (Total: 20 marks) These are really great accounting questions and you can find the answers to these and other homework questions at http://allhomeworktutors.com/ See a list of homework questions provided with answers by expert tutors at http://allhomeworktutors.com/homework-answers where you can start registering for free at http://allhomeworktutors.com/users/sign_up and all you need to say is do my homework