1. Dear Investor,

Our interest in Bajaj Finserv emerges from the hugely undervalued Insurance Operations of the

company. With over 70% of its profits and value coming from Insurance Operations, it is one of the few

stocks to play for the growth in the Insurance Industry. At the current Market price, the Insurance

operations of the company are available at a valuation of 6500 Crs after adjusting for the company's

stake in Bajaj Finance (after 20% Holding Discount) and other Balance sheet items. This is extremely

cheap for a 74% stake in two of the most efficient Insurance companies in India.

Conservative and Capital Efficient Underwriting Operations :-

- Bajaj Allianz General Insurance Company (BAGIC)

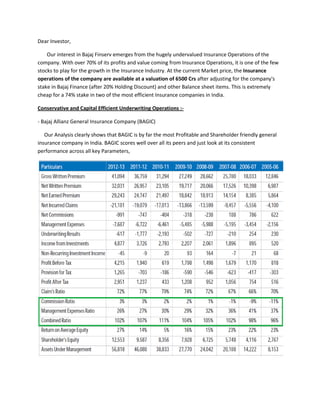

Our Analysis clearly shows that BAGIC is by far the most Profitable and Shareholder friendly general

insurance company in India. BAGIC scores well over all its peers and just look at its consistent

performance across all key Parameters,

2. BAGIC has in fact stated generating underwriting Profits (last Quarter Underwriting Profit of 56 Cr)

from this year. Its Combined ratios are well under 100% compared with the Industry average of around

110%, that shows the Quality of its operations. Underwriting Profits literally means that the company

has a negative cost on the capital which are classified as liabilities and BAGIC is getting paid for using

Customers money. The free Float generated from such Underwriting is helping the company achieve

ROE's of over 26%. BAGIC also has the best Gross Written Premium/ Share Holders equity which is

almost double the Industry average which points to the Capital efficiency of its operations and

sustainability of such high ROE's.

Disciplined Underwriting and large Low Cost Floats :-

- Bajaj Allianz Life Insurance Company (BALIC)

BALIC is by far the largest value creator for Bajaj Finserv. The Life Insurance subsidiary has till now

received Shareholders Equity of just around 1211 Cr - You can compare it with the last year's profit of

about 1000 Cr and the company's Net worth of 4400 Cr to understand the brilliant performance of the

company since inception. Life Insurance business allows the company to receive Long Tail floats and

when these can be generated at a low cost, there is huge profits available as shown in BALIC. Life

Insurance companies will continue to have strong Cash Inflows when they grow, considering the back

ended nature of outflow. With the huge growth opportunity in India expected to unfold over the next

decade, BALIC can continue to add on its AUM from the existing 32000 Cr.

While BALIC may not generate underwriting Profit, its Average Claims ratio (78%), Expenses Ratio

(19%), Investment Income and Employee productivity are among the best in the Industry. The best part

about BALIC has been its conservative underwriting during phases of extreme competition. Despite this

leading to erosion in Market Share and overall Fund size, BALIC has been able to focus on disciplined

underwriting which will keep it in good stead going forward.

The entire Life Insurance industry has gone through significant stress over the last few years with

huge shifts in Product Portfolios and other Regulatory changes. While the shift towards Traditional

products will reduce Fee Income, in the long term they would be compensated by a steady float. We

believe that the Industry would start growing from this year and should be able to clock over 15% CAGR

for the next 3-5 years. BALIC with its Solvency ratios of around 710% against mandated 150% is well

positioned to ride this growth. This huge CAR would be levered in the growth phase and thus can help

the company to improve its ROE's significantly. BALIC can almost triple its underwriting without any new

addition of Equity.

Highly Efficient Insurance Operations to provide Value and Growth :-

There are several global examples of Efficient and Disciplined Insurance companies which have had

strong compounded growth for decades and created strong Value for its Shareholders. While Bajaj

3. Finserv doesn't have a real competitive advantage like the Distribution network of Banks (or) an unique

low cost model of GEICO, a disciplined Underwriting process and Cost conscious operations has helped it

to compound its Book steadily.

In a Capital deficient country like India, Insurance companies which are able to generate large

Capital at relatively lower cost should do extremely well. Bajaj Finserv between its Insurance operations

manages about 37000 Cr of Capital which is generated at a cost lower than Banks, leading to strong

Investment income. During the ensuing growth phase, company would continue to add more AUM and

can generate very high returns on Incremental Equity.

Insurance continues to be an extremely under penetrated product in India and it would be one of

the fastest growing Financial product going forward. While the Life Insurance industry has gone through

a turmoil, we believe that the recent changes have set up a strong base for the Long Term growth.

Efficient Private Insurers have been consistently increasing their Market shares against a bloated public

sector. This trend can continue for many more years like in the Banking sector.

When we look at Bajaj's Insurance operations from a Banking analogy, we are seeing a Bank with

the lowest cost of funds, has an adequate provisioning and strong Risk underwriting which is leading to

best in Industry NIM's and ROA's. All these makes us believe that, Bajaj's Insurance division can

effectively double its Book every 4 years and can continue its compounding for many more years.

Value can be Suppressed for an extended Time period :

An elongated period of Suppressed value is the biggest risk to the stock that holds back several

Investors. With the management not keen on unlocking value through Dividends (or) listings, only a

consistently strong performance will help re-rate the stock. While the company is just a holding

company for the group's Financial divisions, it's still being viewed by Investors like its peer - Bajaj

Holdings & Investment which is a diversified Holding and investment company of the promoters.

Almost every Financial company with a wide range of Assets is a holding company in that sense, from

Sundaram Finance, Reliance Capital, Birla Nuvo to Max India. There is no Insurance company in India

which is not present within a Holding company structure, including that of the Insurance companies

promoted by banks. Nevertheless this continues to be a significant risk and Management's thoughts on

this needs to be ascertained using better.

Conclusion :

There are very few Analysts tracking the company and there has been severe neglect of the stock

among Investors. While the current depressed environment in the Insurance sector has largely led to the

neglect of this stock - once the Insurance industry comes into focus with a few Listings, the company

would be re-rated substantially. It is this neglect that is allowing Investors to buy the Shares at such

cheap valuations.

4. Management's quality of execution can be seen in all its business divisions, from the rapid scale up

the operations of its Consumer Finance subsidiary to the Efficient underwriting at its Insurance

subsidiaries. We believe that the current valuations discounts a large part of the Uncertainties and the

risks involved, thereby providing significant upsides in case of positive surprises.

The stock currently quotes at a Price/ Earnings of less than 6X and a Price to Book of less than 1.3X,

for a company which can consistently generate ROE's of over 20%. The Book itself is substantially

undervalued in our view and to buy the stock near its Book value is a good bargain.

We are clearly not expecting a sharp Rerating or a rapid close in the Price-Value gap, as we

understand the inherent limitations of its Holding structure. But even if the share price follows its

earnings growth - we should be able to get a 20% compounded returns over the next 3-5 years. Any

other form of value unlocking (Bank License, Insurance subsidiary listing etc) or Market recognition that

would lead to a reduction in the Price - Value gap would be an added bonus.

Regards,

[Gokul Raj. P, Director - HBJ Capital]

You can mail us at gokul@hbjcapital.com (or) Call us at 09994577745 for more queries.