Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie 3 pm3 c_2-%20estimating%20costs

Ähnlich wie 3 pm3 c_2-%20estimating%20costs (20)

Mehr von harwoodr

Mehr von harwoodr (13)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

3 pm3 c_2-%20estimating%20costs

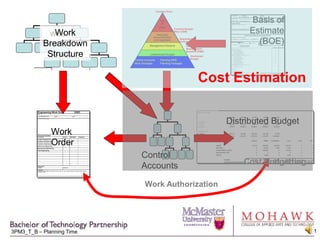

- 1. Cost Estimation Cost Budgetting Work Authorization

- 2. Cost Estimating The cost estimate is prepared as follows: The types of estimate required is determined from the RFP, RFQ or other requestor. The estimating method(s) appropriate to the type of estimate, the program phase and information available are selected. The estimating team is formed, briefed on the estimate requirements and statement of work. Estimates are prepared using a “Basis of Estimate” (BOE) Form, and collected by the “estimate manager” – usually the proposal manager before contract award, and project manager afterwards. Usually these estimates are expressed in a mixture of labour hours and dollars. The BOE forms are compiled, summarized, and submitted to the “Pricing” or “control accounting” function for the application of all additional Elements of Cost (EOC). If prepared for a proposal, “Profit” is applied to yield the proposal “priced estimate”. Otherwise, this forms the basis for the program budget.

- 3. Types of Cost Estimates

- 4. Estimating Methods Similar approaches as used for schedule estimating Expert judgment Analogous Parametric Probabilistic Estimates include both internal estimates and quotes from suppliers and sub-contractor Take care to subject external estimates to the same level of scrutiny as internal

- 5. Kicking off the Estimate Team Preparing an estimate is “a project within a project”, with the following steps: The “estimate manager” – possibly marketing or business development for proposal, project manager after contract award – performs an initial review of the required RFP/SOW. Depending on the level of estimate required and complexity of work, manager pulls together “estimating” team of “experts” Team performs review and estimates on BOE sheets, often supplemented by completion of a SOW compliance matrix for their aspects

- 6. Typical Basis-of-Estimate (BOE) Format 674-2435 Specific reference to proposal, contract or purchase order number WBS reference: estimates are usually done at the lowest level of WBS definition available at the time of the estimate Occasionally, BOE’s may be done by functional group rather than WBS in order to provide clear accountability for the estimate, however, this is not preferred Estimator’s certification, and approval by related functional management Assures “ownership” of estimates by those who will need to support them Summary of the work being estimated, as well as applicable specifications Estimate methods used Estimates by task, activity or deliverable, broken out into impacted functions Allows for use in early resource planning Allows follow-up comparison to actuals to assess estimate accuracy Estimate assumptions May be derived from the SOW/RFP compliance matrix, but should be on the BOE in order to provide a “standalone” reference

- 7. Turning the Estimate into a Contract Price The estimates developed on the various Basis of Estimate forms are collected and added together – this gives the total labour, material and other costs exclusively associated with completing the project (ie. the “Direct Costs”) However, when deciding what price to charge the customer, these costs must be supplemented by the other “Elements of Cost” “Indirect Costs” – the “cost of doing business” Profit – the “charge” for the “added value” delivered

- 9. Work conducted by dedicated program team

- 10. Material purchased to build program equipment and deliverables

- 11. Contract costs of sub-contracts performed for the program

- 12. Indirect: (applied by “Pricing” function)The “cost of doing business” for the business as a whole must be paid for by its “revenue generating” activities. This is done by calculating and applying “Overhead” rates to the Direct costs. Examples:

- 13. Total annual costs of secretarial, accounting, HS&E etc. staff divided by annual “direct” costs of all projects – rate applied against future project direct costs (eg. Add 50% to all direct labour hours)

- 14. Total material handling costs (labour, facilities, equipment) applied as an overhead to direct material costs

- 17. revise budget allocation and work authorization