Top Rated Pune Call Girls Pashan ⟟ 6297143586 ⟟ Call Me For Genuine Sex Serv...

Questions For Management And Directors, A Roadmap For Expansion And Growth

1. Fremont Michigan Insuracorp: High Quality Platform, Bargain Valuation

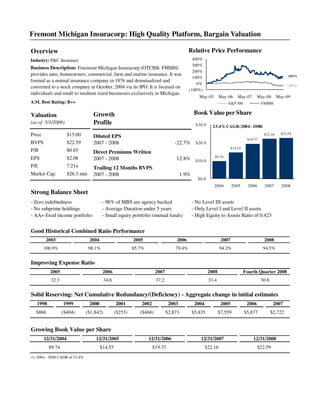

Overview Relative Price Performance

Industry: P&C Insurance 400%

300%

Business Description: Freemont Michigan Insuracorp (OTCBB: FMMH)

200%

provides auto, homeowners, commercial, farm and marine insurance. It was 109%

100%

formed as a mutual insurance company in 1876 and demutualized and

0% (24%)

converted to a stock company in October, 2004 via its IPO. It is focused on

(100%)

individuals and small to medium sized businesses exclusively in Michigan.

May-05 May-06 May-07 May-08 May-09

A.M. Best Rating: B++ S&P 500 FMMH

Valuation Growth Book Value per Share

(as of 5/1/2009) Profile $30.0 23.4% CAGR (2004 - 2008)

Price $15.00 Diluted EPS $22.16 $22.59

$19.37

BVPS $22.59 2007 - 2008 -22.7% $20.0

$14.55

P/B $0.65 Direct Premiums Written

EPS $2.08 $9.74

2007 - 2008 12.8% $10.0

P/E 7.21x Trailing 12 Months BVPS

Market Cap. $26.3 mm 2007 - 2008 1.9%

$0.0

2004 2005 2006 2007 2008

Strong Balance Sheet

- Zero indebtedness - 98% of MBS are agency backed - No Level III assets

- No subprime holdings - Average Duration under 5 years - Only Level I and Level II assets

- AA+ fixed income portfolio - Small equity portfolio (mutual funds) - High Equity to Assets Ratio of 0.423

Good Historical Combined Ratio Performance

2003 2004 2005 2006 2007 2008

100.9% 98.1% 85.7% 79.4% 94.3% 94.5%

Improving Expense Ratio

2005 2006 2007 2008 Fourth Quarter 2008

32.3 34.6 37.2 33.4 30.8

Solid Reserving: Net Cumulative Redundancy/(Deficiency) - Aggregate change in initial estimates

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

$866 ($404) ($1,842) ($253) ($468) $2,873 $5,835 $7,559 $5,877 $2,722

Growing Book Value per Share

12/31/2004 12/31/2005 12/31/2006 12/31/2007 12/31/2008

$9.74 $14.55 $19.37 $22.16 $22.59

(1) 2004 - 2008 CAGR of 23.4%.

3. Some Questions for Fremont's Management and Directors

It is highly important for management and directors to view core business issues from a variety of angles.

Hopefully, these questions will stimulate constructive solutions to serious business issues that face Fremont. Of

course, evidence of effective solutions will be concrete action which quantitatively improves results.

The Problem

Fremont's personal lines have gone from a 2006 gain of $4,129,003 to a 2008 loss of $806,725. Simultaneously,

net premiums earned in personal lines have grown tremendously. This growth has continued in the latest quarter

reported at an enormous rate.

An executive in the Michigan insurance industry has told me that this rate of premium growth in personal lines

(accompanied by losses) has few parallels among Fremont's peers and could easily become a mortal threat to

Fremont's financial health if it is not swiftly rectified.

What actions can management and directors take to assure shareholders that this development is of grave

concern to those tasked with maximizing shareholder value?

Why is management growing a line with profitability that has declined for years and has now gone negative?

If management and directors really understand that this is a grave problem, why haven't they stopped and indeed

contracted the growth in premiums in this line until the issue of losses has been shown to be successfully

remedied for at least two years?

I suggest that management and directors look at this from a shareholder perspective. As shareholders, would they

sit idly by as losses are allowed to mount in personal lines, whose premium growth has continued unabated as of

the latest quarter? Or would they demand a turnaround plan accompanied by concrete corrective action, whose

success is measured quantitatively in profit and loss in ensuing quarters/years?

Solutions

The Michigan Essential Insurance Act makes it very difficult for insurance companies to reduce premiums in

personal lines, but the company does have serious options.

I. Fremont should rank insurance agencies by historical loss performance (perhaps adjusted to reflect their

ranking in their geographic area). Then, Fremont should dispatch employees by telephone, and when

necessary, in person, to ask underperforming agencies to voluntarily cancel their contracts with the

company.

II. Fremont needs to promptly stop using credit scoring. It is a fine quantitative method. However, due to

the political environment, it hurts the company when it tries to raise rates. The use of credit scoring,

which Fremont is particularly known for, is like waving a red cape in front of an angry bull when it

comes to regulators. If the use of credit scoring keeps the company from getting its rates raised by

regulators, its success at predicting loss performance is a moot point.

III. Fremont needs to accept the inconvenient truth that the political environment in Michigan has become

hostile to the adequate pricing of personal lines. I understand that a Michigan-only identity is dearly held

by certain executives. However, Fremont's core value ought to be extending its great insurance services

to individuals and to businesses, regardless of where they live. The pursuit of shareholder value has now

made that mandatory.

Please don't imitate the ostrich, which tries to hide from danger by burying its head in the sand. Bravely confront

4. reality with Evidence-Based Management (EBM) and intelligent solutions.

Fremont needs to expand outside of Michigan. Indiana would be an excellent state for expansion. The regulatory

environment is rational, the economy is better than a state such as Ohio, and the weather environment is

mathematically modelable. There is competition from strong county mutuals. However, the company can win

against these. Fremont can never win against a Michigan regulator who has all the power and refuses to allow

the rate increases necessary for adequate pricing. You may protest that the regulators will allow adequate pricing,

but that argument has failed on the strength of overwhelming evidence to the contrary in the Governor' actions

s

and in the company' own results in personal lines.

s

A Practical Roadmap for Expansion

Fremont executives have told me that they are not sure how they would find the capital necessary to expand.

Here are some ideas:

I. First, Fremont already has excess capital. I believe Michigan law allows the company to pay a dividend

of up to 10% of statutory surplus to shareholders without any approval from the Michigan OFIR.

Statutory surplus stood at $33,169,00 in 2008 as of the company' latest 10-K. Fremont clearly has

s

excess capital. There would be more than enough money to acquire an insurance shell company in

Indiana. The practice is very common, inexpensive, and allows firms to quickly move into states without

many of the usual regulatory hurdles. There are investment banks which specialize in such transactions.

Large and small insurance companies alike do this often. It is a well-regarded method of expansion.

II. Fremont could easily do a sale-and-leaseback of its headquarters property to free up cash. It is owned

free and clear, with no mortgage indebtedness. What could be easier?

III. Obviously, as premiums decrease in Michigan personal lines, less capital will be needed to support

those operations. The capital can be freed up to be used more efficiently elsewhere (in another state) to

maximize shareholder value.

IV. The company could sell all or part of its Michigan book of business in personal lines. If this is

impossible due to its poor performance, the company could heavily reinsure the line and take steps

which would approach run-off, while staying within the bounds of the Michigan Essential Insurance Act.

I want to be clear, I have been the first to advocate a more efficient level of reinsurance for Fremont. However,

that is for lines which are economically viable, for which adequate pricing and performance can be obtained. If a

line has no future, do everything you can to minimize the pain and to expand in places where Fremont can make,

as opposed to lose, money.

Don'kid yourself, don'lose more money, and don'hope the line will come back. In insurance, “hope” is a four-

t t t

letter word for people who can'model risk.

t