Fixed exchange rate and flexible exchange rate.pptx

Avant Garde wealth Mgmt - Quarterly letter - 1303

1. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

Contents

The investment cycle – Impact on corporate profits, valuation, and consumption

Gold – End of a golden run or a golden opportunity?

Global health check – Disconnect between equities and the real economy

Portfolio positioning – Not much change

Stocks in the portfolio – Revisiting theses on sharp moves in prices

Portfolio performance – Subdued returns in a tough environment

Dear investor,

Confounding the bullish consensus at the end of 2012, equity markets proceeded to decline in the

Jan-Mar quarter. The large cap indices do not capture the full extent of the correction, with the mid

and small cap indices declining much more than their larger counterparts. For the full fiscal year

FY12-13 the return on the BSE500 Index was rather tepid at 4.8%. Today we revisit some of the

topics addressed in earlier letters to ascertain whether any assumptions or conclusions we have

drawn in the past should be modified based on what has transpired in the interim.

The length of this letter is primarily due to the large number of graphics included.

The investment cycle – Impact on corporate profits, valuation, and consumption

In our Q1 CY12 letter we had identified investment as an important driver of corporate profits.

Subsequently, in our Q2 CY12 letter we discussed the historical correlation between growth in

investment and growth in consumption. Let’s refer to some data on capital expenditures, courtesy

the excellent Engineering/Construction analyst team at Citigroup, which gives an indication of trends

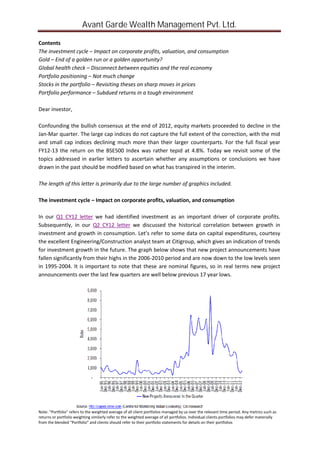

for investment growth in the future. The graph below shows that new project announcements have

fallen significantly from their highs in the 2006-2010 period and are now down to the low levels seen

in 1995-2004. It is important to note that these are nominal figures, so in real terms new project

announcements over the last few quarters are well below previous 17 year lows.

2. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

Not surprisingly, new project announcements are a leading indicator of future capital expenditure.

As the table and graphs below illustrate, the decline in new project announcements over the last

three years is suggesting up to a 50% decline in the capital expenditure run rate over the coming

years.

3. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

While the magnitude of decline suggested may seem startling it is not unprecedented. Referring to

the graph above showing YoY changes, after the decline in new project announcements in FY97-98

total capital expenditure proceeded to decline by a cumulative 46% over the next four years. To

compound the problem of a decline in new project announcements, the graphic below shows that

the percentage of projects under implementation that are stalled because of various reasons are at

an all time high.

Rather than try to pin down the exact magnitude of the expected decline in capital expenditure, for

our limited analytical purpose it is sufficient to conclude that the declining trend will persist and that

the annual declines could be as high as 20% over the next two years.

Recall the discussion on drivers of corporate profits in the Q1 CY12 letter. As a reminder, here is the

relevant identity, known as the Kalecki profits equation, along with the empirical data for the last

few years (all figures are as % of GDP):

Profits = Investment1

– Government savings –Foreign savings – Household Savings + Dividends

1

There is a very high correlation of ~0.95 between the “investment” figures and the historical capital expenditure data.

Investment includes capital formation by the household and non-corporate sector and is less volatile than corporate capex

Fiscal year Investment Govt savings

Foreign

savings

Household

savings

Dividends Profits

FY08 28.4% 4.1% -1.3% -22.9% 1.1% 9.4%

FY09 24.3% 8.4% -2.3% -23.8% 0.9% 7.4%

FY10 26.3% 9.4% -2.8% -25.8% 1.2% 8.4%

FY11 27.1% 7.4% -2.7% -24.9% 1.0% 7.9%

FY12 25.2% 8.0% -4.2% -22.9% 1.0% 7.2%

FY13 24.2% 7.5% -5.1% -21.0% 1.0% 6.6%

Source: RBI database

Note: Figures for FY13 are preliminary, based on the RBI survey

4. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

The data shows that profit margins (profits as % of GDP) have been declining more or less

consistently since FY08, which means that corporate profits have grown slower than nominal GDP.

Looking out over the coming 1-2 years, investment is likely to continue to decline using new project

announcements as a leading indicator. Government savings (federal and state deficit) will also likely

continue to decline given the focus on fiscal consolidation. There will be some relief from a lower

current account deficit (foreign savings) and perhaps from a further decline in household savings.

However, putting the pieces together it looks like the decline in profit margins is set to continue in

FY14 and possibly in FY15. If nominal GDP grows at 11-13% (5-6% real + 6-7% inflation) it seems safe

to conclude that corporate profit growth will at best be capped at 10%.

The low rate of profit growth should not come as a surprise to investors given the underlying trends

but unfortunately it does catch the consensus off-guard. Witness the significant downgrades to

consensus earnings estimates for the NIFTY Index for FY12-14. FY13 EPS estimates have been

downgraded by about 16% over the past two years2

. FY14 EPS estimates still build in 16% growth

over FY13 and are likely to continue to be revised downwards.

Stock markets can and often do move independent of the direction and magnitude change of

earnings in the short term. Since the December 2011 low the indexes have rallied by almost 30% in

the face of persistent earnings downgrades and low earnings growth.

Source: BSE India

2

This is the reason we prefer to look at trailing valuation metrics based on actual reported earnings versus consensus

forward estimates, which have significant scope for revision. In April 2011 the market may have looked attractive based on

consensus FY13 P/E of 13x, but in hindsight the valuation turned out to be closer to 16x FY13 P/E

10

15

20

25

30

35

40

0

12

24

36

48

60

72

84

96

108

120

132

144

156

168

180

192

204

216

228

240

252

264

276

288

300

312

324

336

348

360

372

384

396

408

420

432

444

456

468

480

492

504

516

528

540

552

564

576

588

600

612

624

636

648

660

672

684

696

708

720

732

744

756

768

780

792

Numberof Trading Days

Sensex Bear Markets P/E Progression(Trailing 12 month P/E)

Sep 94-Dec 96 Aug97-Nov 98 Feb 00-Apr 03 Jan 08-Mar 09 Nov 10-Present

Didthe bearmarketendhere?

5. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

The graph above is an updated version from our Q3 CY12 letter. At the time we had raised the

question of whether the bear market had ended in December 2011 and whether the indices were

now in a bull market, which is characterized by rising stock prices and rising P/E multiples. So far the

evidence seems inconclusive as the P/E multiple has been in a tight range of 16-18x since then,

which is unusual by historical standards. So it is reasonable to expect valuations to break out of this

band, either to the upside or to the downside, which will be the key short term driver of market

returns. Likelihood of poor earnings growth and continuing earnings downgrades suggest downside

to the P/E multiple. However, global liquidity and resulting buoyant asset markets provide an

argument for continuing support to P/E multiples and perhaps further upside. The jury is still out.

On the topic of correlation between growth in investment and consumption, the graph below is an

updated version from our Q2 CY12 letter. The sharp divergence in growth rates from FY08 to FY12

that we had highlighted has already begun to correct in FY13. Since the growth rate of investment is

likely to keep decelerating, using history as a guide the growth rate of consumption can be expected

to remain low in order to close the gap. Recent financials of many companies in the consumer

discretionary sector (autos and food and beverage for example) already reflect this growth

slowdown, which will probably persist for some more time.

Source: RBI

Gold – End of a golden run or a golden opportunity?

Gold is one of the largest positions in the portfolio and given the recent sharp decline in prices

deserves some detailed discussion. Gold declined by almost 14% in two days in April (although the

price has since moved up from the lows), apparently breaking through some key technical levels and

entering into a bear market (defined as a >20% fall in price from peak) as the price fell ~30% from

the recent September 2011 peak. Let’s evaluate the outlook for gold through three different lenses

(1) based on price action, (2) based on investor/human behaviour, and (3) based on fundamentals.

The dramatic fall in Gold price was the sharpest correction seen in the last 30 years. However, it is

not unprecedented for an asset class to suffer very sharp corrections and then go on to make new

highs. As the chart below shows, after increasing in price by 6x from January 1970 to December

0%

10%

20%

30%

40%

2%

7%

12%

17%

22%

Growth in consumption (3yr roll) (LHS) Growth in investment (3yr roll) (RHS)

6. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

1974, Gold fell almost 50% through August 1976 (during which time US stocks performed very well),

after which Gold proceeded to go up more than 8x before finally peaking at a price of $850 in

January 1980. As another example, Marc Faber of the Gloom, Boom, Doom report points out that

“global stock markets retreated between 40% and 50% in the October 1987 crash. But thereafter

they rose by another 10 to 20 times.” So purely from the perspective of price action, whether the

secular bull market3

in gold that started in 2001 at a price of ~$250 ended at the recent peak of

~$1900 reached in September 2011 will only be known for sure a few years from now with the

benefit of hindsight.

From a behavioural perspective, there are certain characteristics of investor behaviour that mark

bull market peaks and subsequent declines in any asset class, especially in the case of secular bull

markets. After the sharp two day price decline in Gold it has been widely reported in the media that

physical demand has gone up multi-fold across the globe. This is reflected in long waiting times and

significant premiums over the spot price for buyers who want to actually buy the metal. While the

demand surge in countries such as India and China is understandable given the cultural affinity to

gold, a similar trend in developed countries such as the US, UK, Canada, Japan, Australia was

unexpected. Historically, this is not the kind of behaviour exhibited following sharp price declines in

an ongoing bear market. The reason is that peaks in secular bull markets are characterized by

euphoria among the investor community about the asset in question, which leads to a significant rise

in ownership of that asset as a percentage of portfolios, usually using leverage. When the price

uptrend breaks down and there are significant price corrections investors are usually sellers (often

3

According to Wikipedia “a secular market trend is a long-term trend that lasts 5 to 25 years and consists of a series of

primary trends…a secular bull market consists of larger bull markets and smaller bear markets…In a secular bull market the

prevailing trend is "bullish" or upward-moving”

7. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

forced sellers given leverage) into the panic. While it can be argued that there was some element of

euphoria about Gold leading up to the September 2011 peak, it does not seem to reflect the kind of

wild optimism seen at peaks of past secular bull markets such as the Nasdaq in 2000, commodities in

2008, Gold in 1980, US stocks in 1929, etc. To conclude, investor behaviour following up to and since

the recent price high in September 2011 does not suggest that the secular bull market in Gold has

ended.

Coming to fundamentals, our investment thesis on gold has been premised on Gold being a store of

value in the face of unprecedented monetary easing by the world’s central banks. As a reminder, the

graph below (reproduced from our Q3 CY12 letter) demonstrates the correlation between the size of

central bank balance sheets and the price of gold. It is important to note that the correlation has not

necessarily held over short periods of time but has persisted over a period of years. For example,

from mid 2005 till early 2008 the increase in the price of Gold far exceeded the increase in balance

sheet size. Subsequently, from early 2008 till early 2009 the price of Gold was down slightly even as

central bank balance sheets expanded rapidly.

Note: Major central banks include Fed, ECB, BOE, PBOC, BOJ, SNB

Source: Bloomberg, Central Banks, World Gold Council

Since we laid out our bullish thesis for Gold in October 2012 the economic backdrop and actions of

policy makers have only strengthened the outlook for further monetary easing. The US Federal

Reserve has since announced QE3 and it seems likely that Janet Yellen will replace Ben Bernanke as

Chairman later this year. She is known to be a dove who supports and indeed argues for even more

quantitative easing. After the election of Shinzo Abe as prime minister, The Bank of Japan has

embarked on balance sheet expansion that overshadows even what the US has done relative to the

size of its economy. Mark Carney, the incoming governor of the Bank of England, has publicly argued

that the BoE can do more by way of monetary actions to support the economy. European Central

Bank President Mario Draghi recently stated that the southern European countries will be hurt by a

strong Euro and that “...among major central banks, the ECB has been the only bank that is not

expanding its balance sheet. But it will likely consider such a step.” The Swiss National Bank

continues to print money in order to prevent its exchange rate from appreciating. China remains the

only wild card, with lack of clarity on how its monetary policy will evolve.

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

-

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

Feb-02

May-02

Aug-02

Nov-02

Feb-03

May-03

Aug-03

Nov-03

Feb-04

May-04

Aug-04

Nov-04

Feb-05

May-05

Aug-05

Nov-05

Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

Nov-07

Feb-08

May-08

Aug-08

Nov-08

Feb-09

May-09

Aug-09

Nov-09

Feb-10

May-10

Aug-10

Nov-10

Feb-11

May-11

Aug-11

Nov-11

Feb-12

May-12

Aug-12

Total Assets for Major Central Banks (in USD billion) vs. Gold (USD/Oz)

Total Assets Gold

AssetCAGR= 14.5%

GoldCAGR= 17.5%

AssetCAGR= 18.3%

GoldCAGR= 20.8%

Sep'08(Lehman)

FedAssetCAGR(in USD):

Jan'95 - Sep'08 = 5.4%

Sep'08- Oct'12 = 31.8%

(Triggerpoint= Lehman)

ECBAsset CAGR(in EUR):

Jan'99 - Oct'11 = 9.8%

Oct'11 - Oct'12 = 34.6%

(Triggerpoint= Mario Draghi becomesChairman)

Assets Gold

8. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

It may be no coincidence that since the September 2011 peak in Gold price the combined central

bank balance sheets have only increased at a rate of 6.7% annualized through April 2013, which is

significantly lower than the rate of growth over the past decade. However, simple projections based

on the expected purchases by the Fed and BoJ, and assuming nominal expansion for the other

central banks, suggests that the combined balance sheets should once again grow in excess of 15%

in the coming twelve months, thus supporting the price of Gold.

There are many who question whether Gold is a store of value in the first place. Their primary line of

argument is that the Gold price has not always moved in line with CPI inflation over time. In

addition, the argument goes that an increase in the monetary base is actually not translating into

higher money supply and hence higher inflation due to falling velocity of money. This line of thinking

has gained ground recently as the price decline in Gold has occurred despite the expectations of

continued expansion in the global monetary base. The counterargument lies in how inflation is

defined and indeed how it is experienced. As articulated in our Q3 CY12 letter, “...gold benefits from

higher inflation and higher inflation expectations. Inflation, defined as increasing prices of goods and

services, has been relatively low over the past few years in developed economies. However, this

definition is narrow and misleading. Inflation is simply the reduction in the purchasing power of a

given quantity of money over time. Thought of in this manner increase in prices of assets is also

inflationary. Income is either spent on consumption or saved, which is essentially deferred

consumption. Savings are parked in assets. Higher asset prices lead to lower prospective returns from

those assets, which translates into a reduction in future purchasing power and is therefore

inflationary. So any increase in the quantity of money can lead to inflation either through higher

prices of goods and services or through higher asset prices.”

In the world of institutional investing the majority do not consider Gold to be an “asset class” and

thus not worthy of serious consideration. Investors who make the case for owning Gold are often

disparagingly referred to as Gold Bugs. The sharp rise in the price of Gold over the past decade has

forced discussion about its investment merits into the main stream. But most professional investors

have remained sceptics. This scepticism has come out in full force in the aftermath of the recent

crash in gold prices, with most major institutions calling for a bear market and lower prices ahead.

Our analysis of the fundamentals and our contrarian instincts tell us that despite or perhaps in spite

of the prevailing pessimism, this is the time to be a buyer in Gold and not a seller.

Global health check – Disconnect between equities and the real economy

Equity markets are buoyant globally and close to or at all time highs, with a few exceptions like

China. Movements in global markets are important for Indian equities as foreign equity inflows,

which have been running at all time highs, have arguably been a key driver of equity returns in the

face of poor domestic economic and corporate fundamentals. History has shown that equity returns

in India are closely correlated with movement in equity markets globally, which influence the level of

foreign inflows. In turn there is also some impact on the real economy through the channels of

exchange rates and capital availability.

9. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

The charts below highlight the increasing discrepancy between continuously rising equity prices and

underlying economic fundamentals. While most of the charts reference the US economy and equity

indexes, similar conclusions apply across many other countries.

Despite talk to the contrary, the outlook for the global economy continues to be very poor.

Source: JP Morgan Global Manufacturing and Services PMI; Markit Economics

Recent US macroeconomic data has been well below consensus expectations.

Source: Bloomberg; via Zerohedge.com

However, equity markets continue to make highs. The chart below is from a recent commentary by

fund manager John Hussman. He explains that “a declining line represents periods where economic

data and the S&P are becoming less correlated, or even moving inversely to each other. The most

10. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

recent correlation below -0.7 indicates that stocks and negative economic data are moving in almost

perfectly opposite directions.”

Source: www.hussmanfunds.com

The push higher in equity markets is accompanied by a high degree of complacency. We add a few

graphs to those we had shared in our Q4 CY12 letter in order to emphasize this point.

Source: Bloomberg; via Zerohedge.com

11. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

Source: Citigroup; via Zerohedge.com

Leverage is also at record highs.

Source: Bank of America Merrill Lynch; via Zerohedge.com

12. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

While the increasing disconnect between equity prices and economic fundamentals should be

apparent, it does not imply that a decline in equity prices is imminent as optimism about central

bank actions and the resulting liquidity may keep pushing asset prices higher for some more time.

However, it is inevitable that at some point either the actions of policy makers will begin to have

positive economic impact or else asset prices will begin to reflect the grim economic realities. The

former scenario does not seem very likely as of now. History shows that when investor consensus

veers around to the view that risk of downside in an asset class has been eliminated the risk of

capital loss from owning that asset class becomes very high.

Portfolio positioning – Not much change

The future is always uncertain and we are only willing to accept very limited risk of permanent

capital loss in the quest for returns. As a result our opportunity set has been very limited as it

continues to be difficult to find bargains that meet our criteria in the Indian equity markets. The low

portfolio turnover (18% in FY12-13) reflects this high threshold for putting money to work. When

markets are rallying it is tempting to participate by buying into stocks that have a positive near term

outlook even if the margin of safety is not very apparent. While such an approach may prove fruitful

occasionally we do not believe it is a prudent approach to compounding wealth as it entails high risk

of destroying capital. We would much rather wait for the fat pitches where we can identify a

mispriced stock with a high degree of conviction and make it a meaningful portfolio position.

As of quarter end March 2013 we were 55% net long (70% long, 15% short), with 30% of the

portfolio in cash and equivalents (the short positions are via futures).

We estimate that the long positions in aggregate have about 60% upside to their intrinsic value

under base assumptions. Even under stress scenarios the aggregate intrinsic value is marginally

higher than current prices, indicating limited risk of capital loss. For our short positions we estimate

intrinsic values 30-50% below current prices and believe that the stocks are trading at a premium to

even optimistic estimates of intrinsic value.

Stocks in the portfolio – Revisiting theses on sharp moves in prices

The portfolio composition remains similar as we added marginally to some existing positions on

price weakness and did not sell any shares. Piramal Enterprises and Gold remain the largest positions

in the portfolio, followed by SunTV. The other positions of roughly equivalent size are Manugraph,

Blue Star, Noida Toll Bridge, and Thangamayil Jewellery. DB Corp is a relatively small position in the

portfolio.

Manugraph’s stock price took a sharp hit during the quarter as a large shareholder decided to exit

their position. Since this came at a time when equity indices were declining and company financials

were weak, a large buyer only showed up at much lower prices. This is a risk one has to live with

when investing in small cap stocks that are not very liquid. However, our evaluation of the

company’s intrinsic value has not changed, which we estimate to be significantly more than current

market value. Even in a very bad year for business like FY13 the company will likely deliver a 11%+

13. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

post tax Return on Invested Capital and trades at 6.5x FY13 P/E and 0.5x FY13 P/B, with net cash

accounting for about 40% of market capitalization along with a 8% dividend yield. Earnings should

trend much higher in the coming years as demand for its product eventually picks up along with

capital spending by the newspaper companies, leading to the stock price moving up closer to its fair

value.

The stock price of Noida Toll Bridge is down about 25% from the interim peak reached in October

2012, yet the company’s fundamentals have only improved. Over the last two years the business

generated about Rs.65cr of free cash flow to equity on a current market capitalization of about

Rs.400cr. Political considerations have made the timing and magnitude of toll hikes uncertain but

historically the hikes have always come through, as with the recent 12% hike starting April 1st

2013.

Traffic on the flyway continues to grow as well. Given the monopolistic nature of the business there

is low volatility and high predictability of cash flows. So it is fairly easy to calculate the discounted

value of dividends that can be expected through the end of the asset’s concession period in 2029,

conservatively assuming no residual value from the guaranteed return clause in the concession

agreement. By our estimates the business is worth at least Rs.30/share and likely worth about

Rs.40/share, which is 50-100% above current market price. The key risks are a successful legal

challenge that amends the concession agreement or misallocation of cash flows by management.

Portfolio performance – Subdued returns in a tough environment

From inception in June 2011 till March 2013 the portfolio is up 11.7% while our benchmark, the

BSE500 index, is down 1.4%.

Note: During this period average cash balance is 50% and average net long position is 41%; Figures up to March 31, 2012 have been audited by KPMG

While our performance so far has been ahead of our benchmarks the absolute return remains low. It

is important to emphasize that returns are best measured over a bull-bear market cycle, and ideally

over multiple cycles. When making investment allocations we assume that we will be able to

maintain our positions through a bearish market phase if necessary, and it is important that as our

investors you maintain a similar view in order to allow for the decisions to bear fruit.

The returns you observe are a function of the decisions we take with regard to what securities we

choose to own and how we construct the portfolio. The sum total of these decisions is reflected in

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

Cumulativeportfolio returns vs. index

NAV (pre-fee) BSE500 Index

14. Avant Garde Wealth Management Pvt. Ltd.

Note: “Portfolio” refers to the weighted average of all client portfolios managed by us over the relevant time period. Any metrics such as

returns or portfolio weighting similarly refer to the weighted average of all portfolios. Individual clients portfolios may defer materially

from the blended “Portfolio” and clients should refer to their portfolio statements for details on their portfolios

portfolio returns over time. Our endeavour is to focus on making the decision making process as

robust as possible and the hope is that superior portfolio returns will follow as a result.

Gaurav Jalan

May 11, 2013