20240429 Calibre April 2024 Investor Presentation.pdf

Oei apr-15

1. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (20) 7208-1400 Fax: +44 (20) 7208-1401 ~ www.odey.com

Authorised and Regulated by the Financial Conduct Authority

■ The Fund returned -19.3% in April-15 against an MSCI Daily TR Net

Europe (€) return of +0.1%.

■ The Fund’s active exposure to the long USD had a significant impact

on performance (-11.6%), a considerable portion of which came from

the AUD/USD position.

■ The short equity book also had a negative impact (-7.0%) after

currency hedging. Positive contributions before currency hedging

came from Las Vegas Sands Corp. (+72bps), Kellogg Company

(+34bps) and Tupperware Brands Corp. (+27bps). These were

outweighed by negative contributions from a number of positions, the

worst of which were Seadrill Ltd (-55bps), BG Group Plc (-40bps) and

Coca-Cola HBC AG (-33bps).

■ After currency hedging the long equity book was flat for the month

(+0.1%). Positive contributions before currency hedging came from

positions such as Sky Plc (+31bps) and Hunter Douglas NV (+18bps).

These were canceled out by negative contributions from a number of

positions, the largest being LM Ericsson Telefon AB (-109bps), Alcatel

Lucent SA (-60bps) and Toyota Industries Corp. (-30bps).

■ Elsewhere our Australian government bond positions also

underperformed, contributing -0.9% to performance.

Source for above 3 tables: Internal unaudited figures. All

performance figures quoted are net of fees. Past performance

is not a reliable indicator of future performance.

Source for above table and chart: Quintillion Limited and

Bloomberg. Calculation on a NAV basis as at 30-Apr-15.

The data below refers to the € share class.

April was bloody. A portfolio built on global weakness coming out of China and

even embroiling the developed world, which had been successful since June of

last year was attacked on all sides. The Fund lost money on its Forex positions,

its emerging market short positions, its oil shorts and on top of that the telecoms

equipment providers had a shocking time. Some of the positions had become

crowded even if the thinking is still far away from the consensus. The book has

been cut, FX leverage has been reduced and in May, especially in the second half

of this month, the Fund is acting well.

Nobody likes being wrong. Nobody likes looking foolish. Nobody likes losing

money. In hindsight the tail wind that was the leveraged position in the US dollar

against Emerging Market currencies in particular, meant that I did not respond

quickly enough to the aggressive QE introduced by Draghi in December of last

year and the effects of the fall in the oil price two month earlier.

Essentially Draghi in December decided that a European economy with virtually

no growth and an equilibrium unemployment rate of 11.5%, which hid youth un-

employment of 25% and over employment of the over 60’s of 10%, was unac-

ceptable. By introducing negative interest rates he has successfully driven down

the exchange rate, forced banks to lend to generate any returns and in the process

driven assets sky high. His policies will create a bubble in asset prices but he has

decided it is a consequence worth putting up with. To be fair, his radical transfor-

mation of the political and economic direction of Europe has been strengthened

by employment law changes in Spain, which are freeing up the labour market

dramatically, and from June, changes to creditor protection in Italy, which will

give creditors possession of assets after two rather than nine years.

Fund size includes OEI Mac

Inception Date

Firm size ($m) 12,885.94

Strategy size ($m) 2,941.59

Fund Size (€m) 3,063.50

€ Class 785.47

$ Class 361.96

£ Class 300.36

£ B Class 170.44

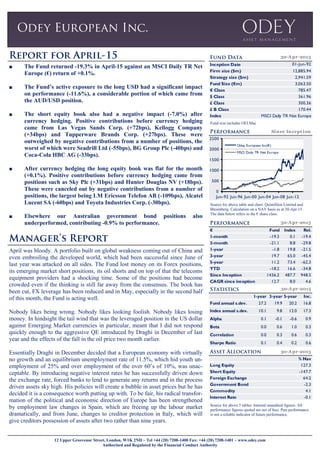

Index MSCI Daily TR Net Europe

30-Apr-2015

01-Jun-92

Since Inception

0

500

1000

1500

2000

2500

Jun-92 Jun-96 Jun-00 Jun-04 Jun-08 Jun-12

Odey European Inc(€)

MSCI Daily TR Net Europe

€ Fund Index Rel.

1-month -19.3 0.1 -19.4

3-month -21.1 8.8 -29.8

1-year -1.8 19.8 -21.5

3-year 19.7 65.0 -45.4

5-year 11.2 73.4 -62.3

YTD -18.2 16.6 -34.8

Since Inception 1436.2 487.7 948.5

CAGR since inception 12.7 8.0 4.6

30-Apr-2015

1-year 3-year 5-year Inc.

Fund annual s.dev. 27.2 19.9 20.2 16.8

Index annual s.dev. 10.1 9.8 12.0 17.3

Alpha 0.1 -0.1 -0.6 0.9

Beta 0.0 0.6 1.0 0.3

Correlation 0.0 0.3 0.6 0.3

Sharpe Ratio 0.1 0.4 0.2 0.6

30-Apr-2015

30-Apr-2015

% Nav

Long Equity 127.3

Short Equity -147.7

Foreign Exchange 64.2

Government Bond -2.3

Commodity 4.1

Interest Rate -0.1

2. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (20) 7208-1400 Fax: +44 (20) 7208-1401 ~ www.odey.com

Authorised and Regulated by the Financial Conduct Authority

European stockmarkets have been strong, driven by this quest for yield and for liquidity. By historic standards they possess

neither but this is a ‘Historic’ time itself. As we can see with the bull market in China, once a bubble forms it has an internal

logic of its own and it will grow until it has outgrown all of its surroundings. What is disconcerting to the stock-picker is that it

has little relevance to earnings growth and it certainly does not predict next year’s profits.

All of this has meant that the Fund is moving towards being net long equities. This bubble will end badly, but not yet. It only

began at the beginning of this year.

However it does mean that the US dollar, where they are hoping to end the QE experiment this year, has to remain the fa-

voured currency. Its rise was probably too quick and undoubtedly attracted too many followers, but here it looks interesting.

However it does not look a powerful enough bull market to be leveraged into.

As I have said for the last year, the risk to the world economy does not come from the developed world where, post 2008, debt

growth has been steady, but from out of the Emerging Markets. E.M. economies now represent 50% of the world’s GNP and

nearly 40% of the world’s debts. The world has been unable for thirty years now to get growth without debt growing even

faster. Operating assets are being asked to work harder to service ever increasing debts. Productivity growth has disappeared.

No wonder the pressure is still downwards on interest rates.

Economics, as I was taught, said nothing about the difference between two identical economies - one that had large debts and

one that was debt free. The one with large debts, paradoxically had the richer individuals and companies, and in an environ-

ment where credit remained freely available performed equally well. However, when faced with disruptive technologies or dis-

ruptive trade patterns the leveraged economy is forced not only to write off unwanted operating assets but the debts attached.

They have to be socialised through the economy. That day is coming, but April showed it is not now.

We are keen to be very open to our clients during difficult periods, so please do contact us if you need any further attribution or

explanation.

3. 12 Upper Grosvenor Street, London, W1K 2ND ~ Tel +44 (20) 7208-1400 Fax: +44 (20) 7208-1401 ~ www.odey.com

Authorised and Regulated by the Financial Conduct Authority

Internal unaudited figures. Internal unaudited figures

Internal unaudited figuresInternal unaudited figures

At 30-Apr-15

At 30-Apr-15

At 30-Apr-15 At 30-Apr-15

Comparative benchmark Primary: Cash, Secondary: MSCI Daily TR Net Europe (€)

Fund inception date 1 June, 1992

Fund type Cayman Long-Short OEIC

Listing Irish Stock Exchange

Base currency €

Share classes €, £ (A & B), $

Hedging Non-base currencies are unhedged

Dealing 1st

/15th

of each month based on funds received the previous day forward to 5pm Dublin time / COB 14th & month end

Front end fee Up to 5%

Annual management fee 1%

Performance fee 20% of the increase in the value per share of the fund between the

beginning and the end of the year. Fees crystalise annually. Losses carried forward.

Anti-dilution fee 0.5% NAV on subs/reds

Exit fee 1% if held <1yr

Min. investment €1,000,000 or £/$ equivalent

Dividends Reporting & accumulation

Price reporting Prices published daily in FT

ISIN €-KYG6708H1157 £A-KYG6708H1645, US$-KYG6708H1496 £B-KYG6708H1728

SEDOL €-3110423 £A-B00VSM0, US$-3110434 £B-B2RGGH3

At 30-Apr-15

At 30-Apr-15

At 30-Apr-15

Internal unaudited figures

Enquiries:

Sarah St. George

Tel: +44 20 7208-1432

Email: s.stgeorge@odey.com

US Clients - Tom Trowbridge

Tel: +1 (917) 538-7838

Email: t.trowbridge@odey.com

Crispin Odey

Portfolio Manager

Internal unaudited figures

-40

-30

-20

-10

0

10

20

30

Aerospace&Defense

Autos&Components

Banks&Finance

BusinessServices

Chemicals

CommercialServices

Construction

ConsumerDurable

Energy

Engr.&Manufacturing

Entertainment

EnvironmentalControl

Food,Bev&Tobacco

Healthcare

HouseholdGoods

Housewares

Index

Insurance

Leisure&Hotels

Media

Mining&Metals

Others

RealEstate

Retail

Software&Services

TechnologyHardware

Telecommunications

Textile&Apparel

Transport

Utilities

Long % of NAV

Short % of NAV

-60

-40

-20

0

20

40

60

Australia

Austria

Belgium

Canada

CaymanIslands

Denmark

Finland

France

Germany

HongKong

Hungary

Ireland

Italy

Japan

Jersey

Luxembourg

Netherlands

Norway

Portugal

SouthAfrica

Spain

Sweden

Switzerland

UK

US

Long % of NAV

Short % of NAV

-300

-200

-100

0

100

200

300

Mar-05 Jul-06 Nov-07 Mar-09 Jul-10 Nov-11 Mar-13 Jul-14

Long Equity Exposure Short Equity Exposure

Net Equity Exposure FX Exposure

Government Bond Exposure

Rank Security Strategy Notional Exposure (Ave %)

1 LM Ericsson Telefon AB Long 7.5

2 Alcatel-Lucent SA Long 4.1

3 Seadrill Ltd. Short 2.4

4 BG Group Plc Short 2.1

5 Saipem S.p.A. Short 2.8

Rank Security Strategy Notional Exposure (Ave %)

1 Las Vegas Sands Corp. Short 7.7

2 Kellogg Company Short 4.1

3 Sky Plc Long 11.3

4 Tupperware Brands Corp. Short 4.1

5 Sands China Ltd. Short 4.4

-37.3

-12.1 -10.4

-4.0

-0.2 -0.1

0.1 0.3 0.3

5.4

17.9

40.4

-50

-40

-30

-20

-10

0

10

20

30

40

50

GBP

AUD

JPY

RUB

NOK

SEK

CAD

CHF

HKD

KRW

EUR

USD

Rank Security Strategy Notional Exposure (%)

1 JPN 10Y Bond(Ose) Jun15 Short 30.7

2 ACGB 2 3/4 04/21/24 Long 29.0

3 Sky Long 11.1

4 Las Vegas Sands Short 7.6

5 Telefonaktiebolaget LM Ericsson Long 7.5

6 JPNK400 Index Fut Jun15 Long 6.7

7 Swatch Short 6.2

8 Intu Properties Short 5.9

9 Adidas Short 5.7

10 COTTON NO.2 FUTR Dec15 Long 5.5