Q4 2012 Houston Medical Office Market Research Report

•

1 gefällt mir•214 views

Empfohlen

Weitere ähnliche Inhalte

Andere mochten auch

Ähnlich wie Q4 2012 Houston Medical Office Market Research Report

Ähnlich wie Q4 2012 Houston Medical Office Market Research Report (20)

Mehr von Colliers International | Houston

Mehr von Colliers International | Houston (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Q4 2012 Houston Medical Office Market Research Report

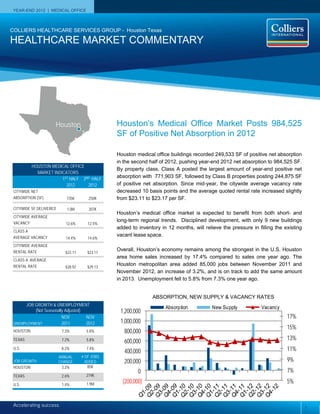

- 1. COLLIERS INTERNATIONAL | HOUSTON MEDICAL OFFICE | 2ND QUARTER 2010 YEAR-END 2012 | MEDICAL OFFICE Accelerating success. HOUSTON MEDICAL OFFICE MARKET INDICATORS 1ST HALF 2012 2ND HALF 2012 CITYWIDE NET ABSORPTION (SF) 735K 250K CITYWIDE SF DELIVERED 1.0M 207K CITYWIDE AVERAGE VACANCY 12.6% 12.5% CLASS A AVERAGE VACANCY 14.4% 14.6% CITYWIDE AVERAGE RENTAL RATE $23.11 $23.17 CLASS A AVERAGE RENTAL RATE $28.92 $29.13 COLLIERS HEALTHCARE SERVICES GROUP - Houston Texas HEALTHCARE MARKET COMMENTARY Houston’s Medical Office Market Posts 984,525 SF of Positive Net Absorption in 2012 Houston medical office buildings recorded 249,533 SF of positive net absorption in the second half of 2012, pushing year-end 2012 net absorption to 984,525 SF. By property class, Class A posted the largest amount of year-end positive net absorption with 771,903 SF, followed by Class B properties posting 244,875 SF of positive net absorption. Since mid-year, the citywide average vacancy rate decreased 10 basis points and the average quoted rental rate increased slightly from $23.11 to $23.17 per SF. Houston’s medical office market is expected to benefit from both short- and long-term regional trends. Disciplined development, with only 9 new buildings added to inventory in 12 months, will relieve the pressure in filling the existing vacant lease space. Overall, Houston’s economy remains among the strongest in the U.S. Houston area home sales increased by 17.4% compared to sales one year ago. The Houston metropolitan area added 85,000 jobs between November 2011 and November 2012, an increase of 3.2%, and is on track to add the same amount in 2013. Unemployment fell to 5.8% from 7.3% one year ago. 5% 7% 9% 11% 13% 15% 17% (200,000) 0 200,000 400,000 600,000 800,000 1,000,000 1,200,000 Absorption New Supply Vacancy ABSORPTION, NEW SUPPLY & VACANCY RATES Houston UNEMPLOYMENT NOV 2011 NOV 2012 HOUSTON 7.3% 5.8% TEXAS 7.2% 5.8% U.S. 8.2% 7.4% JOB GROWTH ANNUAL CHANGE # OF JOBS ADDED HOUSTON 3.2% 85K TEXAS 2.6% 274K U.S. 1.4% 1.9M JOB GROWTH & UNEMPLOYMENT (Not Seasonally Adjusted) 1

- 2. MEDICAL OFFICE & HEALTHCARE MARKET COMMENTARY | YEAR-END 2012 | COLLIERS INTERNATIONAL HOUSTON TEXAS COLLIERS INTERNATIONAL | P. Vacancy & Availability Houston’s medical office occupancy increased slightly during the second half of 2012 with the citywide average vacancy rate decreasing by 10 basis points (bps) to 12.5% from 12.6%. By property class, Class B vacancy rates posted the largest decrease during the second half of 2012, 50 bps to 11.5% from 12.0% in 2Q 2012. Class A vacancy rates increased 20 bps to 14.6 % from 14.4%, while Class C vacancy rates increased 30 bps to 12.1% from 12.1%mid-year. Sublease space has not had a significant impact on current vacancy rates, remaining below 1.0% of total vacant space over five years. Of the 3.4M SF of vacant space on the market at year-end 2012, only 61,180 SF was sublease space. Disciplined medical office development activity has helped prevent major upheavals in current occupancy levels. There were only seven (7) new buildings (152,108 SF) added to the market during 2011 and just nine (9) buildings (1.26M SF) delivered in 2012. The largest project completed within the past two years was the University of Texas MD Anderson Cancer Center Administration Building located at 7007 Bertner Avenue in the Texas Medical Center (895,600 SF owner occupied). Presently, only one medical office building is under construction, The 30,000 SF College Park Medical Plaza located at 3117 College Park Dr. in The Woodlands. The project is 23% pre-leased and is scheduled to deliver June 2013. Absorption & Demand Houston medical office buildings recorded 249,533 SF of positive net absorption in the second half of 2012, pushing year-end 2012 net absorption to 984,525 SF. By property class, Class A posted the largest amount of year-end positive net absorption with 771,903 SF, followed by Class B properties posting 244,875 SF of positive net absorption. In contrast, Class C posted 32,253 SF of negative net absorption. Rental Rates Quoted full-service rental rates for all medical office property classes averaged $23.17/SF in 4Q 2012, an increase from the $23.00/SF in mid- year. Medical office building landlords continued to offer lease concessions including free rent and generous tenant improvement packages to attract and retain credit worthy tenants. By property class, on a bi-annual basis, the average Class A rental rate of $29.13 per SF increased from $28.92 per SF, Class B increased to $22.57 from $22.43 per SF, and the average Class C rate increased from $22.43 to $22.57 per square foot. MEDICAL OFFICE CLASS A & B VACANCY VS. RENTS $0.00 $5.00 $10.00 $15.00 $20.00 $25.00 $30.00 $35.00 8% 10% 12% 14% 16% 18% 20% Q1- 10 Q2- 10 Q3- 10 Q4- 10 Q1- 11 Q2- 11 Q3- 11 Q4- 11 Q1- 12 Q2- 12 Q3- 12 Q4- 12 Class A Vacancy Class B Vacancy Class A Rents Class B Rents Class A 7,611,919 28.2% Class B 14,239,726 54.9% Class C 5,006,935 18.6% Class A Class B Class C (100,000) 0 100,000 200,000 300,000 400,000 500,000 600,000 700,000 Q1-10 Q2-10 Q3-10 Q4-10 Q1-11 Q2-11 Q3-11 Q4-11 Q1-12 Q2-12 Q3-12 Q4-12 Class A Class B Class C MEDICAL OFFICE NET ABSORPTION BY CLASS MEDICAL OFFICE EXISTING INVENTORY BY CLASS 2

- 3. MEDICAL OFFICE & HEALTHCARE MARKET COMMENTARY | YEAR-END 2012 | COLLIERS INTERNATIONAL HOUSTON TEXAS COLLIERS INTERNATIONAL | P. Sales Activity Transaction activity remained solid during 2012, with 57 properties changing hands. According to CoStar Comps, Houston medical sales transactions had a total dollar volume of $170M, averaging $223 per SF with a 7.4% capitalization rate. Many of the transactions were multi- property sales, however, there were several significant single property transactions that occurred. The 27,760 SF 8515 Fannin MOB in the South Main/Medical Center submarket was purchased by The Link Group, Inc. in September 2012. The 80,740 SF 1111 Augusta MOB in the San Felipe/Voss submarket was purchased by Sentinel Real Estate Corporation for $21.4M or $265 per SF. The property was built in 1977 and was renovated in 2004.. The 29,313 SF, Kingsland Medical Plaza located at 777 S Fry Rd. in the Katy Freeway West submarket was purchased by Finesa Real Estate Group for $4.3M or $147 per SF. Investcorp JV Griffin Partners purchased the Offices at Pin Oak Park, a 504,700 SF, five-building portfolio from McCord Development for $78.7M or $156 per SF. The property is located in the Bellaire submarket and was 90% occupied at the time of sale. Leasing Activity Houston’s 2012 medical office leasing activity reached 823,000 SF. By property class, Class B product led the market with 464,000 SF leased, followed by Class A at 271,000 SF, then Class C at 88,000 SF. Although the majority of new leases signed in the second half of the year were in the 1,000 - 5,000 SF range, there were a few larger lease transactions. One of the larger transactions was Physician Endoscopy Center’s lease renewal of 14,080 SF at 3030 S Gessner Rd. in the Westchase submarket. Additional lease transactions include: DermSurgery Associates, PA renewed its lease of 14,000 SF in Greenpark I in the South Main/Medical Center submarket; Legacy Community Health Center leased 3,700 SF at 8300 Homestead Rd. in the Northeast Near submarket; Woodlands Gynocology & Aesthetics leased 3,000 SF Medical Arts Center II in The Woodlands submarket. Source: Costar Group; Real Capital Analytics RBA: 27,760 SF Built: 1994 Buyer: The Link Group, Inc. Seller: Treeline Partners Ltd Sale Date: Sep 2012 RBA: 80,740 SF Built: 1977/2004 Buyer: Sentinel Real Estate Corp Seller: Healthcare Realty Trust Inc. Sale Date: Aug 2012 Sale Price: $21.4M Cap Rate: 6.81% RBA: 29,313 SF Built: 1994 Buyer: Finesa Real Estate Group Seller: Norvin Partners Sale Date: Dec 2012 Sale Price: $4.3M Kingsland Medical Plaza 777 S Fry Rd Katy Freeway West Submarket 8515 Fannin Street1 South Main/Medical Center Submarket SALES TRANSACTIONS 1111 Augusta Drive San Felipe/Voss Submarket 1Colliers International Houston Transaction Cordes Medical Building 2655 Cordes Drive E Fort Bend Co/Sugar Land Submarket RBA: 8,531 SF Built: 2005 Buyer: Scuben Cordes, LLC Seller: Jag At Cordes LLC Sale Date: Nov 2012 Sale Price: $2.3M Cap Rate: 8.25% 3

- 4. MEDICAL OFFICE & HEALTHCARE MARKET COMMENTARY | YEAR-END 2012 | COLLIERS INTERNATIONAL HOUSTON TEXAS COLLIERS INTERNATIONAL | P. The Texas Medical Center (TMC) – the world’s largest medical center – represents one of Houston’s major economic drivers and core industries with an estimated regional annual economic impact of $14 billion. TMC is also one of Houston’s largest employers with 92,500 employees, including physicians, scientists, researchers and other advanced degree professionals in the life sciences. The internationally-renowned, 1,300-acre TMC is the world’s largest medical complex with 52 member institutions, including leading medical, academic and research institutions, all of which are non-profit and dedicated to the highest standards of research, education and patient and preventive care. Member institutions include 13 hospitals and two specialized patient facilities, as well as 19 renowned academic and research institutions virtually covering all health-related careers – including two medical schools, four nursing schools, as well as schools of dentistry, public health, and pharmacy – and 15 support services organizations. Over 69,000 students – including more than 7,000 international students – are affiliated with TMC, including high school, college and health profession graduate programs. More than 7.1 million patients visited in 2011, including approximately 16,000 international patient visits. TMC Patient Care Institutions The University of Texas M.D. Anderson Cancer Center Texas Children’s Hospital Memorial Hermann Hospital System The Methodist Hospital St. Luke’s Episcopal Hospital Lyndon B. Johnson General Hospital Quentin Mease Community Hospital Ben Taub General Hospital The Institute for Rehabilitation and Research The Hospice at the Texas Medical Center Texas Heart Institute Shriners Hospitals for Children – Houston Veterans Affairs Medical Center in Houston In addition to the medical facilities and institutions of higher learning, TMC is also home to more than 280 professional buildings. Overall, the complex covers over 18 miles of public and private streets and roadways, with 45.5M SF of existing patient, education, and research space. TMC has continued to grow and expand over the past several decades with the majority of growth occurring in the past ten years. The Center is located in the 110-acre University of Texas Research Park, a joint effort between the University of Texas Health Science Center, M.D. Anderson and General Electric Healthcare. In terms of future growth, TMC approved $7.1 billion in building and infrastructure investments between 2008 and 2012, with annual research expenditures estimated at $1 billion. TMC Academic and Research Institutions Texas Children’s Hospital Neurological Research Institute Baylor College of Medicine The University of Texas Health Science Center at Houston The University of Texas M.D. Anderson Cancer Center University of Houston College of Pharmacy Rice University Texas A&M University Health Science Center Prairie View A&M University College of Nursing Texas Woman’s University Institute of Health Sciences Texas Southern University College of Pharmacy and Health Sciences Harris County Psychiatric Center Houston Academy of Medicine TEXAS MEDICAL CENTER The University of Texas M.D. Anderson Cancer Center ranked #1 in U.S. News & World Reports “Americas Best Hospitals” for cancer care. 4

- 5. MEDICAL OFFICE & HEALTHCARE MARKET COMMENTARY | YEAR-END 2012 | COLLIERS INTERNATIONAL HOUSTON TEXAS COLLIERS INTERNATIONAL | P. HOUSTON AREA HOSPITAL LOCATIONS 5

- 6. MEDICAL OFFICE & HEALTHCARE MARKET COMMENTARY | YEAR-END 2012 | COLLIERS INTERNATIONAL HOUSTON TEXAS COLLIERS INTERNATIONAL | P. Accelerating success. COLLIERS INTERNATIONAL | HOUSTON 1300 Post Oak Boulevard Suite 200 Houston, Texas 77056 Main +1 713 222 2111 LISA R. BRIDGES Director of Market Research Houston Direct +1 713 830 2125 Fax +1 713 830 2118 lisa.bridges@colliers.com 6 The Colliers Advantage Enterprising Culture Colliers International is a leader in global real estate services, defined by our spirit of enterprise. Through a culture of service excellence and a shared sense of initiative, we integrate the resources of real estate specialists worldwide to accelerate the success of our partners. When you choose to work with Colliers, you choose to work with the best. In addition to being highly skilled experts in their field, our people are passionate about what they do. And they know we are invested in their success just as much as we are in our clients’ success. This is evident throughout our platform—from Colliers University, our proprietary education and professional development platform, to our client engagement strategy that encourages cross-functional service integration, to our culture of caring. We connect through a shared set of values that shape a collaborative environment throughout our organization that is unsurpassed in the industry. That’s why we attract top recruits and have one of the highest retention rates in the industry. Colliers International has also been recognized as one of the “best places to work” by top business organizations in many of our markets across the globe. Colliers International offers a comprehensive portfolio of real estate services to occupiers, owners and investors on a local, regional, national and international basis.