2020 Mid-Year | Texas Seniors Housing | Research & Forecast Report

•

0 gefällt mir•82 views

Texas Seniors Housing still a sound investment amid COVID-19

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Mehr von Colliers International | Houston

Mehr von Colliers International | Houston (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

2020 Mid-Year | Texas Seniors Housing | Research & Forecast Report

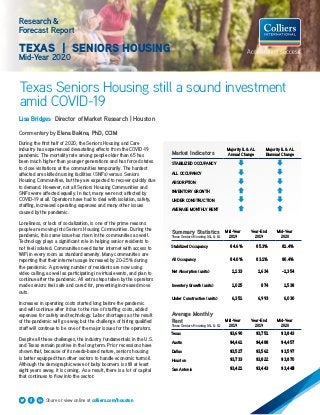

- 1. Research & Forecast Report TEXAS | SENIORS HOUSING Mid-Year 2020 Texas Seniors Housing still a sound investment amid COVID-19 Lisa Bridges Director of Market Research | Houston Commentary by Elena Bakina, PhD, CCIM During the first half of 2020, the Seniors Housing and Care industry has experienced devastating effects from the COVID-19 pandemic. The mortality rate among people older than 65 has been much higher than younger generations and has forced states to close visitations at the communities temporarily. The hardest affected are skilled nursing facilities (SNFs) versus Seniors Housing Communities, but they are expected to recover quickly due to demand. However, not all Seniors Housing Communities and SNFs were affected equally. In fact, many were not affected by COVID-19 at all. Operators have had to deal with isolation, safety, staffing, increased operating expenses and many other issues caused by the pandemic. Loneliness, or lack of socialization, is one of the prime reasons people are moving into Seniors Housing Communities. During the pandemic, this same issue has risen in the communities as well. Technology plays a significant role in helping senior residents to not feel isolated. Communities need faster internet with access to WiFi in every room as standard amenity. Many communities are reporting that their internet usage increased by 20-25% during the pandemic. A growing number of residents are now using video calling, as well as participating in virtual events, and plan to continue after the pandemic. All extra steps taken by the operators made seniors feel safe and cared for, preventing increased move outs. Increases in operating costs started long before the pandemic and will continue after it due to the rise of staffing costs, added expenses for safety and technology. Labor shortages as the result of the pandemic will go away, but the challenge of hiring qualified staff will continue to be one of the major issues for the operators. Despite all these challenges, the industry fundamentals in the U.S. and Texas remain positive in the long term. Prior recessions have shown that, because of its needs-based nature, seniors housing is better equipped than other sectors to handle economic turmoil. Although the demographic wave of baby boomers is still at least eight years away, it is coming. As a result, there is a lot of capital that continues to flow into the sector. Summary Statistics Texas Seniors Housing (AL & IL) Mid-Year 2019 Year-End 2019 Mid-Year 2020 Stabilized Occupancy 84.6% 85.3% 81.4% All Occupancy 84.0% 83.1% 80.4% Net Absorption (units) 1,133 1,634 -1,354 Inventory Growth (units) 1,025 874 1,538 Under Construction (units) 6,351 6,993 6,030 Average Monthly Rent Texas Seniors Housing (AL & IL) Mid-Year 2019 Year-End 2019 Mid-Year 2020 Texas $3,690 $3,751 $3,843 Austin $4,461 $4,488 $4,457 Dallas $3,527 $3,562 $3,597 Houston $3,733 $3,822 $3,870 San Antonio 8$3,421 $3,443 $3,443 Share or view online at colliers.com/houston Market Indicators Majority IL & AL Annual Change Majority IL & AL Biannual Change STABILIZED OCCUPANCY ALL OCCUPANCY ABSORPTION INVENTORY GROWTH UNDER CONSTRUCTION AVERAGE MONTHLY RENT

- 2. 22 Texas Research & Forecast Report | Mid-Year 2020 | Seniors Housing & Care | Colliers International2 Demographics Overview The U.S. Census reports that seniors represent 10% of Texas’ population and that 25% of them are living alone. Approximately 25% of seniors 60 and older received food stamps in the last year. Further, the census reports that about 10,000 baby boomers turn 65 every day and that trend will continue over the next 15 years, increasing the need for seniors housing. 2019 U.S. Census data shows that seven of the nation’s fifteen fastest growing cities are located in Texas and the state is the third fastest-growing state in the country in terms of percentage gain of housing units (11.3%) and first in terms of the largest numeric increase (1.1 million). The oldest baby boomers are in their mid-seventies now and this category of seniors help drive today’s IL development boom. In the past, the 75+ population has been entering IL communities in large numbers, but that’s not the case anymore. Seniors are staying active longer, and industry players are now running feasibility analyses on the 80+ population. It’s difficult to predict when we will see a large number of Baby Boomers start renting IL and AL communities. Advances in healthcare and technology may push this process beyond 2025. Supply and Demand The National Investment Center for Seniors Housing and Care (NIC) reported a decrease in the number of units absorbed on a net basis in the primary U.S. markets during the first half of 2020. Annual absorption was -0.2%, 310 basis points lower than in Q1 2020 and up 300 basis points from a year ago. NIC also reported a decrease in the number of units absorbed in Texas during the first half of 2020, -1,605 units; however, on a biannual basis there were 283 seniors housing units absorbed. The highest demand on an annual basis was in the Houston metro where 285 units were absorbed, followed by Dallas (145 units). In contrast, both Austin and San Antonio recorded negative net absorption over the year of 30 and 320 units, respectively. In Houston, inventory grew by 574 units and in Dallas by 155 units. Austin and San Antonio both recorded negative growth in the first half of 2020, shrinking by -114 units by -36 units, respectively. Major metros in Texas reported seniors housing occupancy rates decreased during the first half of 2020. All of the major markets recorded a decrease in occupancy between Q4 2019 and Q2 2020. 76.0% 78.0% 80.0% 82.0% 84.0% 86.0% 88.0% -2,000 -1,500 -1,000 -500 0 500 1,000 1,500 Texas Major Metros - Senior Housing (Majority AL & IL) Absorption Inventory Growth Stabilized Occupancy Occupancy 64.0% 66.0% 68.0% 70.0% 72.0% 74.0% 76.0% -3,500 -3,000 -2,500 -2,000 -1,500 -1,000 -500 0 500 Texas Major Metros - Majority NC Absorption Inventory Growth Stabilized Occupancy Occupancy Supply and Demand Trends Market No. of Properties No. of Units Stabilized Occupancy Absorption Inventory Growth Units Under Construction Avg. Monthly Rent ALL MARKETS 494 60,944 69.7% -2,864 34 446 $7,129 AUSTIN 52 6,363 74.5% -307 -114 0 $7,350 DALLAS 217 27,307 67.1% -1,358 -47 322 $7,137 HOUSTON 138 17,199 67.4% -724 179 124 $7,442 SAN ANTONIO 87 10,075 69.7% -475 16 0 $6,588 Mid-Year 2020 Nursing Care Statistical Summary Market No. of Properties No. of Units Stabilized Occupancy Absorption Inventory Growth Units Under Construction Avg. Monthly Rent ALL MARKETS 643 74,018 81.4% -1354 1,538 6,030 $3,843 AUSTIN 87 9,684 80.7% -129 408 1,079 $4,457 DALLAS 302 33,873 84.4% -569 592 2,216 $3,597 HOUSTON 175 20,886 78.5% -363 574 2,349 $3,870 SAN ANTONIO 79 9,575 81.8% -293 -36 386 $3,448 Mid-Year 2020 Senior Housing Market Statistical Summary - Includes IL and AL Majority Seniors Housing Statistical Summary

- 3. 3 Houston Research & Forecast Report | Mid-Year 2020 | Seniors Housing & Care | Colliers International33 Rent Trends Seniors Housings annual rent growth rate continued to increase in 2020 in all Texas metros, growing 1.3% over the year. IL and AL Majority average monthly rent rose 0.6% in Austin, 1.6% in Dallas, 1.4% in Houston and 1.0% in San Antonio between Q2 2019 and Q2 2020. The Texas average monthly rental rate for seniors housing is $3,843. Nursing care trends are not as healthy as seniors housing trends. Inventory growth for Texas fell by -0.2% on an annual basis. Annual absorption declined by -6.9% and the occupancy rate declined over the year by 490 basis points from 73.6% to 68.6%. At the end of the second quarter of 2020, the Texas nursing care average asking monthly rental rate of $7,129 was 5.4% higher than the average rental rate in the second quarter of 2019. Investment Activity The 2020 Emerging Trends in Real Estate report by Price Waterhouse Cooper (PwC) continues to rank Seniors Housing among top subsectors for investment and development. Private equity returns for Seniors Housing properties continues to outpace those of other real estate sectors except for industrial. For the past seven years, Seniors Housing has been ranked number one among all types of Apartment Investments. This year’s report ranked it second after moderate/workforce apartments. The average cap rate for Seniors Housing properties in Texas has decreased to 5.84% at the end of Q2 2020, marginally below the national average of 5.9%. The average cap rate for SNFs in the U.S. saw a sharp decline from its highest point of 12.2% in Q4 2018 and reached a historical low 8.6% in Q2 2020. Despite market uncertainty, the limited supply of new acquisitions and historically low-interest rates fuel buyers’ competition and, consequently, push cap rates down. On the other hand, many buyers have a difficult time securing financing. Lenders are looking for buyers to have strong financials and more equity upfront. Texas Seniors Housing Buyer Composition Sales Activity - (SH and NC) Source: Real Capital Analytics Mid-Year 2020 NO. OF PROPERTIES: 22 TOTAL SALES VOLUME: 360.3M AVERAGE $ PER UNIT: $136,276 AVERAGE CAP RATE: 5.84% Texas Seniors Housing Sales Volume 60,000 80,000 100,000 120,000 140,000 160,000 180,000 200,000 U.S. Texas Texas Seniors Housing Price Per Unit 0 500,000,000 1,000,000,000 1,500,000,000 2,000,000,000 2,500,000,000 3,000,000,000 Rolling 4-Quarter Volume Quarterly Volume ` 8.2% 39.8% 25.7% 24.6% 35.8% 1.0% 62.9% 25.2% 35.9% 29.5% 23.1% 18.2% 26.7% 32.3% 25.7% 44.9% 38.7% 80.8% 1.0% 2.7% 12.5% 1.1% 1.0% 2.4% 2015 2016 2017 2018 2019 2020 YTD Cross-Border Institutional REIT/Listed Private User/Other

- 4. 4 North American Research & Forecast Report | 2014 | Office Market Outlook | Colliers International Copyright © 2015 Colliers International. The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report. Colliers International | Market 000 Address, Suite # 000 Address, Suite # +1 000 000 0000 colliers.com/<<market>> 4 North American Research & Forecast Report | 2014 | Office Market Outlook | Colliers International Copyright © 2020 Colliers International. The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report. Colliers International | Houston 1233 West Loop South, Suite 900 Houston, Texas 77027 +1 713 222 2111 colliers.com/houston Construction Costs Senior living construction costs have been on the rise in the U.S., including Texas, as a result of labor shortages and the rising prices of building materials. Developers have seen hard costs increase anywhere between 7-10% annually. According to The Weitz Company’s national construction data, mid-level assisted living projects development costs range from $194 to $249 per square foot, while mid-level independent living projects range from $168 to $198 per square foot. In Texas, construction costs are still lower than the national average. The highest construction costs among Texas major metros are in Houston where mid-level assisted living projects range from $168 to $268 per square foot, while mid-level independent living projects range from $146 to $221 per square foot. 2020 (Per Gross Square Foot) Low High Low High Low High Low High Low High Low High Low High Low High Independent Living $140 $165 $159 $213 $143 $169 $162 $218 $146 $221 $165 $221 $140 $165 $158 $212 Cottages $112 $131 $154 $192 $114 $134 $158 $196 $116 $200 $161 $200 $111 $130 $154 $191 Assisted Living $162 $208 $218 $258 $166 $213 $223 $264 $168 $268 $227 $268 $161 $207 $217 $257 Skilled Nursing $186 $218 $236 $301 $190 $223 $242 $308 $194 $313 $246 $313 $185 $217 $235 $300 IL Commons $228 $289 $299 $367 $233 $295 $306 $375 $237 $381 $311 $381 $227 $288 $297 $365 Under Buildling Parking $80 $109 $110 $140 $82 $111 $113 $143 $83 $146 $115 $146 $80 $108 $110 $140 Sitework Source: The Weitz Company High-LevelHigh-Level Mid-Level High-Level Mid-Level Austin Dallas Excluded Excluded Senior Living Construction Costs Excluded Excluded Excluded Excluded Excluded Excluded Houston San Antonio Mid-Level High-Level Mid-Level Year-End Senior Housing Under Construction (The list below is a selection from different markets and is not a complete list of all properties currently under construction.) PROPERTY NAME MARKET PROPERTY TYPE IL UNITS AL UNITS NC BEDS OPERATOR ANTICIPATED OPEN DATE Greyrock Seniors at Circle C Ranch Austin Freestanding 152 0 0 Greyrock Sniors LP January 2021 Grand Living at Georgetown Austin Combined 100 80 0 Ryan Companies June 2021 Ariel Pointe Senior Living Dallas Combined 120 85 0 Civitas Senior Living August 2021 Wilshire by Abby Senior Living Dallas Combined 135 90 120 Abby Develoopment July 2021 Vineyard Pearland Houston Combined 130 69 0 Valeo Senior, LLC September 2021 Grand Living at Riverstone Houston Freestanding 100 80 0 Ryan Companies October 2021 The Blake at new Braunfels San Antonio Combined 0 112 0 Blake Managment Group, LifeCare Properties LLC December 2020 The Brooks of Cibolo San Antonio Combined 156 78 0 Civitas Senior Living August 2020 Under Construction According to NIC MAP, our Seniors Housing data source, there were 4,605 Majority IL units under construction in Texas primary markets in Q2 2020, followed by 1,425 Majority AL and 446 Majority NC units. Dallas and Houston continued to have high volumes of the Seniors Housing construction. Houston had 2,473 units under construction in Q2 2020, the third-highest in the U.S. Dallas’s construction volume (2,138 units) is fifth in the country. Senior population growth and an abundance of debt capital spur these new developments. FOR MORE INFORMATION Lisa Bridges CPRC Director of Market Research | Houston +1 713 830 2125 lisa.bridges@colliers.com CONTRIBUTOR Elena Bakina PhD, CCIM Senior Vice President | Houston +1 713 830 4008 elena.bakina@colliers.com

- 5. Our philosophy revolves around the fact that the best possible results come from linking our global enterprise with local advisors who understand your business, your market, and how to integrate real estate into a successful business strategy. C O L L I E R S I N T E R N A T I O N A L G L O B A L L O C A T I O N S COMMERCIAL REAL ESTATE SECTORS REPRESENTED OFFICE INDUSTRIAL LAND RETAIL HEALTHCARE MULTIFAMILY HOTEL $129BTRANSACTION VALUE 2BSF UNDER MANAGEMENT $3.5BIN REVENUE 443OFFICES 18,700PROFESSIONALS 430ACCREDITED MEMBERS 68COUNTRIES SIOR ADVANTAGE Colliers International (NASDAQ, TSX: CIGI) is a leading real estate professional services and investment management company. With operations in 68 countries, our more than 15,000 enterprising professionals work collaboratively to provide expert advice to maximize the value of property for real estate occupiers, owners and investors. For more than 25 years, our experienced leadership, owning approximately 40% of our equity, has delivered compound annual investment returns of almost 20% for shareholders. In 2019, corporate revenues were more than $3.0 billion ($3.5 billion including affiliates), with $33 billion of assets under management in our investment management segment. Learn more about how we accelerate success at corporate.colliers.com, Twitter @Colliers or LinkedIn. Colliers professionals think differently, share great ideas and offer thoughtful and innovative advice to accelerate the success of its clients. Colliers has been ranked among the top 100 global outsourcing firms by the International Association of Outsourcing Professionals for 13 consecutive years, more than any other real estate services firm. Colliers is ranked the number one property manager in the world by Commercial Property Executive for two years in a row. PROPERTY POSITIONING & MARKETING REAL ESTATEINVESTMENT VALUATION& ADVISORY CORPORATE SOLUTIONS MANAGEMENT REALESTATE REPRESENTATION LANDLORD REPRESENTATION TENANT LOCA TION INTELLIGENCE MA RKET RESEARCH& CAPITAL MARKETS PROJECT MANAGEMENT COLLIERS SPECIALIZATIONS and REAL ESTATE SERVICE REPRESENTATION DATACENTERS HE ALTHCARE HOTELS & HOSPITALITY SERVICES IND USTRIAL LAND HOUSING&MULTIFAMILY SER VICES MARINA, LEISURE & GOLF COURSE OFFICE RETAIL SPECIALPURPOSE