Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Andere mochten auch (19)

Ähnlich wie Enron

Ähnlich wie Enron (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Enron

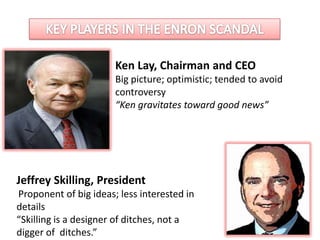

- 1. Ken Lay, Chairman and CEO Big picture; optimistic; tended to avoid controversy “Ken gravitates toward good news” Jeffrey Skilling, President Proponent of big ideas; less interested in details “Skilling is a designer of ditches, not a digger of ditches.”

- 2. David Duncan, Chief Auditor His job was to check accounts. He was an Andersen employee for 20 years, who was in charge of the Enron account since 1997. Andrew Fastow, CFO Ambitious; unwilling to let the rules get in the way “I don’t know that he ever had a moral compass”

- 3. Sherron Watkins Vice President She is considered by many to be the whistleblower who helped to uncover the Enron scandal in 2001. Richard Causey Enron's former chief accounting officer, Causey handled Enron audits for Arthur Andersen LLP before joining Enron.

- 5. WHAT WENT WRONG In Enron The Enron deception was practicing the accounting fraud by creating the SPS (Special Purpose Entity) which exchange the debt and failing investment into sales revenue in financial statement. This Fraud is done by the cooperation of Enron CFO, few of Enron people and Andersen’s chief auditor for Enron

- 6. WHAT WENT WRONG In Arthur Andersen Public Accountant As an organization of public accountant Arthur Andersen violated the regulation of the Public Accountant practices because Andersen was not only as the internal auditor but also as the external auditor of Enron.

- 7. 1993-2001: Enron also used complex & dubious accounting schemes • to reduce Enron’s tax payments; • to inflate Enron’s income and profits; • to inflate Enron’s stock price and credit rating; • to hide losses in off-balance-sheet subsidiaries; • to engineer off-balance-sheet schemes to funnel money to themselves, friends, and family; • to fraudulently misrepresent Enron’s financial condition in public reports.

- 8. Accounting Scheme Enron’s rapid growth in late 1990s involved large capital investments not expected to generate significant cash flow in short term. Maintaining Enron’s credit ratings at an investment grade (e.g., BBB- or higher by S&P) was vital to Enron’s energy trading business. One perceived solution: Create partnerships structured as special purpose entities (SPEs) that could borrow from outside investors without having to be consolidated into Enron’s balance sheet. SPE 3% Rule: No consolidation needed if at least 3% of SPE total capital was owned independently of Enron.

- 9. Accounting Scheme Enron’s creation of over 3000 partnerships started about 1993 when it teamed with Calpers (California Public Retirement System) to create JEDI (Joint Energy Development Investments) fund. Enron initially thought of these partnerships as temporary solutions for temporary cash flow problems. Enron later used SPE partnerships under 3% rule to hide bad bets it had made on speculative assets by selling these assets to the partnerships in return for IOUs backed by Enron stock as collateral! (over $1 billion by 2002)

- 10. Accounting Scheme • In Nov 1997, Calpers wants to cash out of JEDI. • To keep JEDI afloat, Enron needs new 3% partner. • It creates another partnership Chewco (named for the Star Wars character Chewbacca) to buy out Calpers’ stake in JEDI for $383 million. • Enron plans to back short-term loans to Chewco to permit it to buy out Calper’s stake for $383 million. • Chewco needs $383 million to give Calpers • It gets….. — $240 mil loan from Barclay’s bank guaranteed by Enron — $132 mil credit from JEDI (whose only asset is Enron stock) •Chewco still must get 3% of $383 million (about $11.5 million) from some outside source to avoid inclusion of JEDI’s debt on Enron’s books (SEC filing, 1997).

- 11. Accounting Scheme Chewco Capital Structure: Outside 3% $125,000 from William Dodson & Michael Kopper (an aide to Enron CFO Fastow) $11.4 mil loans from Big River and Little River (two new companies formed by Enron expressly for this purpose who get a loan from Barclay’s Bank)

- 12. Conclusion • With the fall of Enron due to the accounting fraud, many began to question the accounting practices corporations throughout the United States. • The fall of Enron lead to the dissolution of the accounting firm Arthur Anderson. Which at the time was one of the “Big Five” accounting firms. • Following the collapse of Enron the Sarbanes-Oxley Act was passed on July 2002. The act established the Public Company Accounting Oversight Board to oversee the auditors of public companies and to protect the interst of investors. • In November 2004 Enron emerged from its bankrupsy and on September 2006 they sold Prisma Energy International Inc. their last buisness. • As of 2007 Enron chenged it name to Enron Creditors Recovery Corporation. 2011-11-02 12