Pine Flash Note: Monetary Policy – walking on thin ice

1. Pine Flash Note: Monetary Policy – walking on thin ice

January 15, 2013

We revised our CPI inflation (IPCA) forecast from 5.10% to 5.60% in 2013. Despite the marked

deterioration in the inflation outlook, we believe this level of IPCA does not change the

strategy of maintaining the Selic rate at 7.25% until the end of the year in a context of

limited recovery. It is worth noting that our estimate of real GDP growth in 2013 is 2.6%

below the median of market forecasts (3.20%, according to the latest Boletim Focus) and the

more pessimistic potential GDP growth estimates.

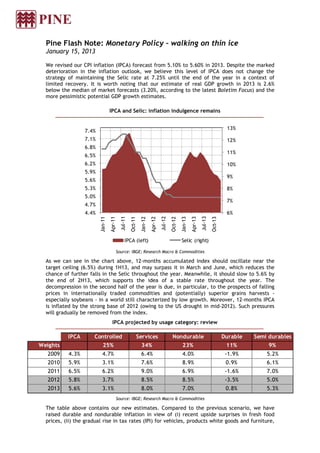

IPCA and Selic: inflation indulgence remains

13%

7.4%

7.1% 12%

6.8%

11%

6.5%

6.2% 10%

5.9%

9%

5.6%

5.3% 8%

5.0%

7%

4.7%

4.4% 6%

Jul-11

Jul-12

Jul-13

Apr-11

Apr-12

Apr-13

Jan-11

Oct-11

Jan-12

Oct-12

Jan-13

Oct-13

IPCA (left) Selic (right)

Source: IBGE; Research Macro & Commodities

As we can see in the chart above, 12-months accumulated index should oscillate near the

target ceiling (6.5%) during 1H13, and may surpass it in March and June, which reduces the

chance of further falls in the Selic throughout the year. Meanwhile, it should slow to 5.6% by

the end of 2H13, which supports the idea of a stable rate throughout the year. The

decompression in the second half of the year is due, in particular, to the prospects of falling

prices in internationally traded commodities and (potentially) superior grains harvests -

especially soybeans - in a world still characterized by low growth. Moreover, 12-months IPCA

is inflated by the strong base of 2012 (owing to the US drought in mid-2012). Such pressures

will gradually be removed from the index.

IPCA projected by usage category: review

IPCA Controlled Services Nondurable Durable Semi durables

Weights 25% 34% 23% 11% 9%

2009 4.3% 4.7% 6.4% 4.0% -1.9% 5.2%

2010 5.9% 3.1% 7.6% 8.9% 0.9% 6.1%

2011 6.5% 6.2% 9.0% 6.9% -1.6% 7.0%

2012 5.8% 3.7% 8.5% 8.5% -3.5% 5.0%

2013 5.6% 3.1% 8.0% 7.0% 0.8% 5.3%

Source: IBGE; Research Macro & Commodities

The table above contains our new estimates. Compared to the previous scenario, we have

raised durable and nondurable inflation in view of (i) recent upside surprises in fresh food

prices, (ii) the gradual rise in tax rates (IPI) for vehicles, products white goods and furniture,

2. according to the government schedule, and (iii) the historically high diffusion index inside

IPCA throughout 2H12 (despite being statistically irrelevant for predicting future inflation

signals derived only by shocks and/or one-time events).

Therefore, the main risk to our forecast stands in the (high) volatility in food prices (in the

table above, it is embedded in the non-durable goods group). In this sense, we also simulated

a price change exceeding our forecast of 7.0% in line with its inflation in 2012 (8.5%). In this

case, the estimated IPCA would rise from 5.6% to 5.9%. Similarly, an abrupt BRL devaluation -

near 2.2/US$ for example – would also lead the IPCA in late 2013 to a most pessimistic level,

close to 6.0%. That is why we conclude the BCB would intervene, (if necessary) to keep the

BRL between 2.0/US$ and 2.08/US$.

Finally, we note that our projections (a) already include a reduction of only 11% in consumer

electricity prices - versus the government target of nearly 17% - that should reduce controlled

price inflation from 3.7% in 2012 to 3.1%, (b) do not take into account a possible

readjustment in gasoline and diesel prices. The magnitude and timing (if it occurs indeed) are

obviously political decisions. In addition, considering there is little headroom for "more

inflation", it is highly likely the government adopts new measures to offset its effects over

consumer prices, either via tax reductions (PIS-COFINS) or via increased blending of ethanol in

gasoline.

Marco Antonio Maciel Marco Antonio Caruso

Chief economist Economist

Pine Pine

3. Disclaimer

This report has been prepared by PINE Research Macro/Commodities, a research department of Banco Pine S.A., PINE Securities USA LLC

(“PINE”), a broker-dealer registered with the U.S. Securities and Exchange Commission and a member of the Financial Industry Regulatory

Authority and the Securities Investor Protection Corporation, is distributing this report in the United States. PINE assumes responsibility for

this research for purposes of U.S. law. Any U.S. person receiving this report and wishing to effect any transaction in a security discussed in

this report should do so with PINE at +1-646-398-6900, 645 Madison Avenue, New York, NY 10022.

Banco Pine refers to PINE, as well as Banco Pine S.A. and PINE Investimentos.

This report is for distribution only under such circumstances as may be permitted by applicable law. This report is not directed at you if PINE

is prohibited or restricted by any legislation or regulation in any jurisdiction from making it available to you. You should satisfy yourself

before reading it that PINE is permitted to provide research material concerning investments to you under relevant legislation and regulations.

Nothing in this report constitutes a representation that any investment strategy or recommendation contained herein is suitable or

appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. It is published solely for

information purposes, it does not constitute an advertisement and is not to be construed as a solicitation, offer, invitation or inducement to

buy or sell any securities or related financial instruments in any jurisdiction. Prices in this report are believed to be reliable as of the date on

which this report was issued and are derived from one or more of the following: (i) sources as expressly specified alongside the relevant data;

(ii) the quoted price on the main regulated market for the security in question; (iii) other public sources believed to be reliable; or (iv) PINE's

proprietary data or data available to Banco Pine. All other information herein is believed to be reliable as of the date on which this report

was issued and has been obtained from public sources believed to be reliable. No representation or warranty, either express or implied, is

provided in relation to the accuracy, completeness or reliability of the information contained herein, except with respect to information

concerning PINE, its subsidiaries and affiliates, nor is it intended to be a complete statement or summary of the securities, markets or

developments referred to in the report. In all cases, investors should conduct their own investigation and analysis of such information before

taking or omitting to take any action in relation to securities or markets that are analyzed in this report.

As of the end of the month immediately preceding the date of publication of this report, neither Banco Pine nor any its affiliates beneficially

own 1% or more of any class of common equity securities of the companies analyzed in this report. In addition, neither Banco Pine nor its

affiliates: (a) have managed or co-managed a public offering of securities for the companies; (b) have received compensation for investment

banking services from the companies in the past 12 months; or (c) expect to receive or intends to seek compensation for investment banking

services from the companies within the next three months. Pine Research issues its views pursuant to relevant factors necessary to

recommend an investment decision and independently of any instructions that Investimentos might have from any covered company with

which it has a business relationship. The recommendations given by the Pine Corporate Research with respect to the shares covered by its

analysts respond exclusively to the analysis of the merits and the market conditions in which the publicly-traded companies operate.

Banco Pine does not undertake that investors will obtain profits, nor will it share with investors any investment profits nor accept any liability

for any investment losses. Investments involve risks and investors should exercise prudence in making their investment decisions. Banco Pine

accepts no fiduciary duties to recipients of this report and in communicating this report is not acting in a fiduciary capacity. The report

should not be regarded by recipients as a substitute for the exercise of their own judgment. Opinions, estimates, and projections expressed

herein constitute the current judgment of the analyst responsible for the substance of this report as of the date in which was issued and are

therefore subject to change without notice and may differ or be contrary to opinions expressed by other business areas or groups of Banco

Pine as a result of using different assumptions and criteria. Any such opinions, estimates, and projections must not be construed as a

representation that the matters referred to therein will occur. Prices and availability of financial instruments are indicative only and subject

to change without notice.

Research will initiate, update and cease coverage solely at the discretion of Pine Research. The analysis contained herein is based on

numerous assumptions. Different assumptions could result in materially different results. The analyst(s) responsible for the preparation of this

report may interact with trading desk personnel, sales personnel and other constituencies for the purpose of gathering, synthesizing and

interpreting market information. Banco Pine is under no obligation to update or keep current the information contained herein, except when

terminating coverage of the companies discussed in the report. Banco Pine relies on information barriers to control the flow of information

contained in one or more areas within Banco Pine, into other areas, units, groups or affiliates of Banco Pine. The compensation of the analyst

who prepared this report is determined by research management and senior management (not including investment banking). Analyst

compensation is not based on investment banking revenues, however, compensation may relate to the revenues of Banco Pine as a whole, of

which investment banking, sales and trading are a part.

The securities described herein may not be eligible for sale in all jurisdictions or to certain categories of investors. Options, derivative

products and futures are not suitable for all investors, and trading in these instruments is considered risky. Mortgage and asset-backed

securities may involve a high degree of risk and may be highly volatile in response to fluctuations in interest rates and other market

conditions. Past performance is not necessarily indicative of future results. If a financial instrument is denominated in a currency other than

an investor’s currency, a change in rates of exchange may adversely affect the value or price of or the income derived from any security or

related instrument mentioned in this report, and the reader of this report assumes any currency risk.

This report does not take into account the investment objectives, financial situation or particular needs of any particular investor. Investors

should obtain independent financial advice based on their own particular circumstances before making an investment decision on the basis of

the information contained herein. For investment advice, trade execution or other enquiries, clients should contact their local sales

representative. Neither Banco Pine nor any of its affiliates, nor any of their respective directors, employees or agents, accepts any liability

for any loss or damage arising out of the use of all or any part of this report.

Any prices stated in this report are for information purposes only and do not represent valuations for individual securities or other

instruments. There is no representation that any transaction can or could have been effected at those prices and any prices do not necessarily

reflect Banco Pine’s internal books and records or theoretical model-based valuations and may be based on certain assumptions. Different

assumptions, by Banco Pine or any other source, may yield substantially different results.

This report may not be reproduced or redistributed to any other person, in whole or in part, for any purpose, without the prior written

consent of Banco Pine, and Banco Pine accepts no liability whatsoever for the actions of third parties in this respect.

Additional information relating to the financial instruments discussed in this report is available upon request.

Regulation A-C Certifications

The analyst responsible for the production of this report hereby certifies that the views expressed herein accurately and exclusively reflect his

or her personal views and opinions about any and all of the issuers or securities analyzed in this report and were prepared independently and

autonomously.