2013.06.18 Time Series Analysis Workshop ..Applications in Physiology, Climate Change and Finance, part 3

•

6 gefällt mir•1,846 views

Professor Dimitris Kugiumtzis, Aristotle University of Thessaloniki, Greece, presented this workshop on nonlinear analysis of time series as part of the Summer School on Modern Statisitical Analysis and Computational Methods hosted by the Social Sciences Compuing Hub at the Whitaker Institute, NUI Galway on 17th-19th June 2013.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Andere mochten auch (12)

Ähnlich wie 2013.06.18 Time Series Analysis Workshop ..Applications in Physiology, Climate Change and Finance, part 3

Ähnlich wie 2013.06.18 Time Series Analysis Workshop ..Applications in Physiology, Climate Change and Finance, part 3 (20)

Mehr von NUI Galway

Mehr von NUI Galway (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

2013.06.18 Time Series Analysis Workshop ..Applications in Physiology, Climate Change and Finance, part 3

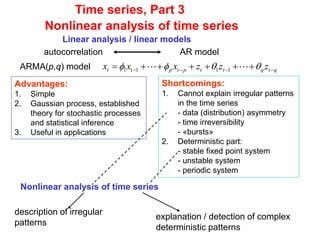

- 1. Nonlinear analysis of time series ARMA(p,q) model qtqttptptt zzzxxx 1111 Linear analysis / linear models Advantages: 1. Simple 2. Gaussian process, established theory for stochastic processes and statistical inference 3. Useful in applications Shortcomings: 1. Cannot explain irregular patterns in the time series - data (distribution) asymmetry - time irreversibility - «bursts» 2. Deterministic part: - stable fixed point system - unstable system - periodic system autocorrelation AR model description of irregular patterns explanation / detection of complex deterministic patterns Time series, Part 3 Nonlinear analysis of time series

- 3. ),,,,( 21 tptttt XXXfX A general nonlinear model tptttt XXXfX ),,,( 21 additive noise p ptttt 'XXX ,,, 211 X p f : f ?

- 4. tptpttt XXXX 2211 Linear AR model Generalizations / extensions of the ΑR model p ,,, 21 constant (linear ΑR) random coefficients - RCA - BL constant (linear ΑR, ARMA) function of Xt - ARCH - GARCH piecewise models - SETAR - Markovian )1()1( 2 )1( 1 ,,, p )2()2( 2 )2( 1 ,,, p )()( 2 )( 1 ,,, l p ll

- 5. Self-excited threshold autoregressive models (SETAR) ll rrrr ,,,, 110 lrrr 10 lRRR 21 lirrR iii ,,1],,( 1 p Partition of selection of a lag d, partition of for dtX t j pt j pt j t j t XXXX )()( 2 )( 21 )( 1 jdt RX SETAR when

- 6. )1,0(~ 0αν4.00.1 0αν6.00.2 11 11 t ttt ttt t XX XX X Example for SETAR -5 0 5 -3 -2 -1 0 1 2 3 4 x(t-1) x(t) (xt-1 ,xt ) for a SETAR model

- 7. AR models with probabilistic selection of threshold Exponential autoregressive models (EAR) tt j t j t XXX 2 )( 21 )( 1 1με2 με1 j tt j t j t XXX 2 )( 21 )( 1 AR models with periodic coefficients 12όταν2 2όταν1 kt kt j 1 )1( 1 0)1( 2 0)2( 1 2 )2( 2 Example

- 8. Markov chain driven AR models ljJt ,,2,1 The selection of the threshold is determined by a Markov chain )|( 1 iJjJP tt Transition matrix Example tt J t XX t 1 )( 9.0)1( 9.0)2( 8.02.0 9.01.0 )|( 1 iJjJP tt =

- 9. Piecewise polynomial models tptttt XXXfX ),,,( 21 1 2( , , , )t m t t t p tX p X X X polynomial of order p and degree m Example 2 1 1 1 1(1 )t t t t tX aX X aX aX logistic map1a aa /)1( Two fixed points: 0 and Fractional autoregressive models tq j j tj p j j tj t Xbb Xaa X 1 10 1 10 10 qp 0pa 0qb Example Fraction of two polynomials

- 10. random coefficients autoregressive models (RCA) 1 ttt XX AR(1) with multiplicative errors p i titiit XtBbX 1 )( RCA ib constant )(tBb iii )(,),(),( 21 tBtBtB p independent of t tXrandom with mean 0 Example titit XtBX )(1.0 )9.0,0(~ 2 tB

- 11. Bilinear models (BL) BL of order 1: ttttt XbaXX 11 p i titiit XtAaX 1 )( s k ktjki btA 1 )( )(tAa iii coefficients ts XXts const, tss ,- If linear w.r.t. “Bilinear” because: ts Xts const, tsXs ,- If linear w.r.t.

- 12. AR models with conditional heteroscedasticity tX ~ ARCH ~ BL 2 tX ARCH ttt VX 22 11 ptptt XXV 0 0i Model of multiplicative noise ),0(~ 2 t GARCH q i iti p i itit VXV 11 2 0i ttt VX 0 0i

- 13. Analysis with nonlinear models 1. Model selection 2. Parameter estimation - maximum likelihood method - method of ordinary least squares 3. Diagnostic checking uncorrelated following normal distribution rgm m 2)(ˆ|ln2)(AIC xθx Μ candidate models, m = 1,...,M errors (rediduals):

- 14. Real world time series mechanics physiology geophysics economics

- 15. Nonlinear time series analysis and dynamical systems Time series 1 2, , , nx x x Assumption: : trajectory of the dynamical systemd ts 0s : state vector at time 0 dd : t f system function t : continuous or discrete time For time series we assume underlying systems to be dissipative Trajectory in d attractor d :h observation function ( )t tx h sobservation : 0( )t t s f sNonlinear dynamical system

- 16. Attractor: ● stable fixed (equilibrium) point ● finite set of equilibrium points ● limit cycle ● torus ● strange attractor self similarity - fractals chaossensitivity to initial conditions can be derived by a linear system cannot be derived by a linear system

- 17. Nonlinear dynamical systems, maps (discrete time) si = 1 – 1.4 si-1 2 + 0.3si-2 chaotic map Hénon 2 1 1 1 6 4.0exp9.01 k kk s i iss chaotic map Ikeda si = a si-1(1 - si-1) periodic a=3.52 chaotic a=4 Logistic map

- 18. Nonlinear dynamical systems, flows (continuous time) s3 s1 s2 s1, s2 , s3Lorenz system: 2133 31212 121 )( sscss sssbss ssas 3 8 2810 cba sampling time τs

- 19. Noise in the time series ( )t tx h s 0( )t t s f s noise ( )t t tx h w s observational noise noise Observation Dynamical system 0( )t t tf s s dynamic (system) noise tw : white noise, uncorrelated to andtx ts t : white noise, uncorrelated to us tu

- 20. Noise: dynamic (system) ε observational (measurement) w si = a si-1(1 - si-1) xi = si + wi, wi ~ N(0,s) logistic map si = a si-1(1 - si-1) + εi , εi ~ N(0,s2) xi = si chaotic periodic

- 21. Scatter diagrams in 2 and 3 dimensions d=1 d=3d=2

- 22. d=1 d=3d=2 0 50 100 150 200 250 300 0 50 100 150 200 time index i x(i) annual sunspots 1700-1996 0 50 100 150 200 0 50 100 150 200 x(i) x(i-1) sunspots 0 50 100 150 200 0 50 100 150 200 0 50 100 150 200 x(i-1) sunspots x(i) x(i-2) 0 50 100 150 200 250 300 0 100 200 300 400 500 time index i x(i) square of AR(9) 0 100 200 300 400 500 0 100 200 300 400 500 x(i) x(i-1) Square of AR(9) 0 200 400 600 0 200 400 600 0 100 200 300 400 500 x(i-1) Square of AR(9) x(i) x(i-2) 50 100 150 200 250 0 500 1000 1500 2000 time index i x(i) square of z-lorenz 0 500 1000 1500 2000 0 500 1000 1500 2000 x(i) x(i-1) square of z-lorenz 0 500 1000 1500 2000 0 500 1000 1500 2000 0 500 1000 1500 2000 x(i-1) square of z-lorenz x(i) x(i-2) Scatter diagrams in 2 and 3 dimensions

- 23. - Other topics: - Hypothesis testing for linearity / nonlinearity - Control system evolution - Synchronization - … - State space reconstruction in order to observe the complexity / stochasticity / structure of the system - Estimation of characteristics of the system / attractor measuring the complexity / dimension of the system - Modeling / Prediction Use nonlinear models to improve predictions Topics in the analysis of time series and dynamical systems

- 24. xi = [xi , xi-t ,…, xi-(m-1)t ] Method of delays Parameters embedding dimension m delay time t time window length tw tw = (m-1)t We assume that the studied system is deterministic State space reconstruction initial state space M is 1is )(1 ii sfs x R observed quantity xi = h(si ) h Embedding ? 1ix ix )(1 ii xFx Rm reconstructed state space xi = F(si )Φ condition: 12 Dm

- 25. m=2 τ=1 s(i)= 1 – 1.4 s(i-1)2 + 0.3s(i-2) or s1 (i)= 1 – 1.4 s1(i-1)2 + s2(i-1) s2 (i)= 0.3 s1(i-1) Method of delays Example: Hénon map xi= s1 (i) projection m=3 τ=1 m=2 τ=2 m=3 τ=2 self-intersections

- 26. τ =10 xi= s1 (i) projection τ=1 Method of delays, m=3 3213 21312 211 )( cssss sbssss ssas a=10, b=28, c=8/3 Example: Lorenz system optimal τ ? τ =5 τ =20

- 27. • From the autocorrelation r(τ) (measures linear correlation) τ r(τ) =1/e ή τ r(τ) =0 Estimation of τ )()( ),( log),(),( , ypxp yxp yxpYXI YX XY yx XY )(),( t t IYXI xYxX ii • From the mutual information I(τ) (measures linear and nonlinear correlation) τ first local minimum I(τ)

- 28. • Close points on the attractor are: - either real neighboring points due to system dynamics - or false neighboring points due to self-intersections and insufficiently low m Method of false nearest neighbors (FNN) Estimation of m Optimal m ? R R2 • Takens theorem: … but D is unknown 12 Dm • At a larger m where there are no self-intersections all false neighboring points will be resolved as they will no longer be close • The optimal m’ is the one for which there are no longer any false nearest neighbors as the dimension increases by one from m’ to m’+1. • Too small m self-intersection in the attractor • Too large m “curse of dimensionality”

- 29. An example of estimating m by the method FNN The estimation of m with the method FNN depends on: - the delay τ - noise x-Lorenz without noise 2 4 6 8 10 0 5 10 15 20 25 30 35 40 m %FNN FNN, x-lorenz, no-noise t=2 t=5 t=10 t=20 x-Lorenz + 10% noise 2 4 6 8 10 0 5 10 15 20 25 30 35 40 m %FNN FNN, x-lorenz 10% noise t=2 t=5 t=10 t=20

- 30. • Dimension 1. Euclidean 2. Topologic 3. Fractal (correlation, information, box counting, …) • Lyapunov exponents (largest, the whole spectrum) • Entropy Estimation of nonlinear characteristics Nonlinear characteristics (invariant measures)

- 31. The correlation dimension ν characterizes the fractal structure of the attractor (self-similarity at different scales) using the density of the points of the attractor in the reconstructed state space The basic idea is that the probability of two points being closer than a distance r Correlation dimension ν rji xx changes w.r.t. r as a power of r i : number of points lying in a sphere with radius r and center ix i i jx r x x scaling law rxi ~ ν integer the attractor is a regular geometric object ν non-integer attractor is a fractal holds for 0r N xi xi

- 32. xi xi rrC )(Scaling law for small r Convergence of ν(m) for m sufficiently large Estimation dlog ( ) dlog C r r for a range of r If ν small and non-integer and the system is deterministic small dimension and fractal (chaotic) structure Estimation of the correlation dimension ν Correlation sum N i N ij jr NN rC 1 1)1( 2 )( xxi Nii ,,1, xreconstructiontime series , 1, , ( 1)ix i N m t Estimation of xi 0 when 0 ( ) 1 when 0 x x x Heaviside function

- 33. x-Lorenz + 10% observational noise, τ=2 x-Lorenz + 10% observational noise, τ=10 log C(r) vs log r local slope vs log r ν vs m x-Lorenz without noise, τ=2

- 34. The estimation of ν is affected by the following factors: - correlation time wji - selection of τ and m - noise - time series length

- 35. -2 -1.5 -1 -0.5 0 0.5 -5 -4 -3 -2 -1 0 logr logC(r) m=1 m=10 () -2 -1.5 -1 -0.5 0 0.5 0 1 2 3 4 5 log r localslope m=1 m=10 () 0 2 4 6 8 10 0 1 2 3 4 5 m () n=924 Hénon -2 -1.5 -1 -0.5 0 0.5 -5 -4 -3 -2 -1 0 logr logC(r) m=1 m=10 () -2 -1.5 -1 -0.5 0 0.5 0 1 2 3 4 5 log r localslope m=1 m=10 () 0 2 4 6 8 10 0 1 2 3 4 5 m (t) Hénon + 10% white noise -4 -3.5 -3 -2.5 -2 -1.5 -1 -5 -4 -3 -2 -1 0 logr logC(r) m=1 m=10 () -4 -3.5 -3 -2.5 -2 -1.5 -1 0 2 4 6 8 10 log r localslope m=1 m=10 () 0 2 4 6 8 10 0 2 4 6 8 10 m () Returns of ASE index 1/1/2005 – 20/9/2005 -4 -3.5 -3 -2.5 -2 -1.5 -1 -5 -4 -3 -2 -1 0 logr logC(r) m=1 m=10 () -4 -3.5 -3 -2.5 -2 -1.5 -1 0 2 4 6 8 10 log r localslope m=1 m=10 () 0 2 4 6 8 10 0 2 4 6 8 10 m () white noise

- 36. The Lyapunov exponents measure the average rate of divergence and convergence of the trajectories on the attractor at the directions of the local state space Lyapunov spectrum: m ...21 λi > 0 divergence λi < 0 convergence λi = 0 direction of flow If λ1 > 0 and the system is deterministic chaos Lyapunov exponents Dissipative system : m i i 1 0

- 37. xi xi’ xi+t xi’+t d0 dt Largest Lyapunov exponent λ1 Initial distance d0= xi - xi’ of two nearby trajectories is expected to increase exponentially with time If t t e 1 0 λ1 is the largest Lyapunov exponent N j j jt Nt 1 ,0 , 1 ln 1 Computation: After time t: dt= xi+t - xi’+t

- 38. Example: x-Lorenz without noise with 10%-noise The estimation of λ1 depends on : τ, m, noise

- 39. The true system generating the time series: )(1 ii sfs Prediction models 2 1, 1 1, 2, 2, 1 1, 1 1.4 0.3 i i i i i s s s s s Hénon map 1 1, 2, 1, 1( , ) f i i is s s 2 1, 2, 2, 1( , ) f i i is s s 1i if s s

- 40. The true system generating the time series: unknown)(1 ii sfs The problem of modeling and prediction of time series: given x1, x2, … xi , to estimate / predict xi+1 State space reconstruction with the method of delays: xi = [xi, xi-t …, xi-(m-1)t] Prediction models The reconstructed system from the time series: estimation?)(1 ii xFx The function that is relevant to time series prediction: )(1 ii xFx )(1 ii Fx x mm :F m F : 1 1( , )i i ix F x x m = 2, τ = 1

- 41. • Semi-local models, e.g. neural networks the form of function F is derived as a weighted sum of local basic functions Nonlinear prediction models • Global models, e.g. polynomials function F bears the same analytic expression for the whole domain • Local models, e.g. the local linear model function F is defined differently at each point of the reconstructed state space

- 42. Prediction using similar segments of the time series Prediction at time i+T from the mappings Τ step ahead of “similar” segments from the past of the time series

- 43. Local prediction models Implementation of the idea of “similar” segments: time series segments reconstructed points },...,,{ )()2()1( Kiii xxxThe nearest neighboring points to xi: Prediction of xi+T from the mappings of the neighbors: },...,,{ )()2()1( TKiTiTi xxx Zeroth order prediction: TiiTi xTxx )1()(ˆ Average prediction: K j Tjii x K Tx 1 )( 1 )(

- 44. Local linear prediction We assume that for the neighbor of xi the local linear model is valid : i mimii miiiii 'a xaxaxaa xxxFFx xa x 0 )1(210 )1(1 ),,,()( tt tt xi(1)+T = a0 + a’ xi(1) xi(2)+T = a0 + a’ xi(2) xi(K)+T = a0 + a’ xi(K) The model holds for )()2()1( ,...,, Kiii xxx K j mjimjiji aaa xaxaax m 1 2 )1()()(101)( ,,, )(min 10 t Estimation of parameters (method of ordinary least squares) maaa ,,, 10

- 45. Estimation of prediction error We split the time series in two parts: 1 11 2, 1, , , , ,N N Nx x x x x learning set test set 1 1 ˆ ˆ, ,N Nx xpredictions ˆi T i T i Te x x prediction error N i i TN Nt TtTt xx N xx NTN T 1 2 1 2 1 1 ˆ 1 )(NRMSE 1 statistic for prediction error ( )ix T

- 46. Example: x-Lorenz • local linear prediction model (LLP) Prediction with: • local average prediction model (LAP) 11,5,1 Kmt without noise with 10%-noise

- 47. 0 2 4 6 8 10 0.7 0.8 0.9 1 1.1 m nrmse(m) () AR LAM(K=15) LLM(K=15) Prediction error (nrmse) for the last 30 quarters annual- quarter growth rate of GNP of USE in the period 1947 – 1991 164 166 168 170 172 174 176 -0.01 -0.005 0 0.005 0.01 0.015 0.02 () real AR(3) LAM(m=5,K=15) LLM(m=5,K=15) Predictions starting at the first quarter of 1989 with prediction horizon being the last 6 years Prediction with - linear model, AR - local average model, LAM - local linear model, LLM

- 48. Prediction starting at 20/9/2005 and prediction horizon is up to 16 days ahead ASE index in the period 1/1/2002 – 20/9/2005 Predict index with - linear model, AR - local average model, LAM returns 1 1 t t t t x x y x 18 25 02 09 16 -0.015 -0.01 -0.005 0 0.005 0.01 0.015 day returnsofindex () general index returns y n (T), AR(7) y n (T), LAM(m=7,K=20) index 18 25 02 09 16 3200 3250 3300 3350 3400 3450 day closeindex () general index xn (T), AR(7) xn (T), LAM(m=7,K=20)

- 49. One step ahead prediction in the period 21/9/2005 – 12/10/2005 ASE index in the period 1/1/2002 – 20/9/2005 Predict index with - linear model, AR - local average model, LAM returns 1 1 t t t t x x y x 18 25 02 09 16 -0.015 -0.01 -0.005 0 0.005 0.01 0.015 day indexreturn () general index y n (1) AR(7) y n (1) LAM(m=7,K=20) index 18 25 02 09 16 3200 3250 3300 3350 3400 3450 day closeindex () general index xn (1) AR(7) xn (1) LAM(m=7,K=20)