Red Eagle Mining - Morning Coffee July 26

•

1 gefällt mir•504 views

This document provides commentary and market data from Wednesday July 25, 2012, including: 1) Summaries of market index performance in Canada, the U.S., and globally along with commodity prices and currency exchange rates. 2) Discussion of earnings reports and developments from several Canadian and U.S. companies. 3) Technical indicators on trading volume and notable 52-week highs and lows for companies trading on the TSX, TSX Venture, NYSE, NASDAQ, and other exchanges.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Andere mochten auch

Andere mochten auch (8)

Ähnlich wie Red Eagle Mining - Morning Coffee July 26

Ähnlich wie Red Eagle Mining - Morning Coffee July 26 (20)

Mehr von Viral Network Inc

Mehr von Viral Network Inc (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Red Eagle Mining - Morning Coffee July 26

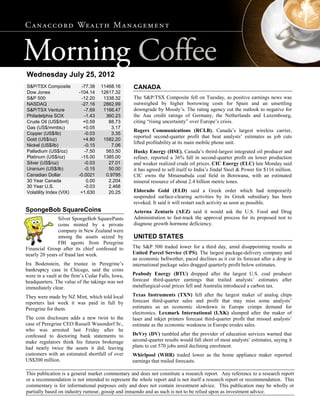

- 1. This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. Wednesday July 25, 2012 S&P/TSX Composite -77.38 11468.16 Dow Jones -104.14 12617.32 S&P 500 -12.20 1338.32 NASDAQ -27.16 2862.99 S&P/TSX Venture -7.69 1166.47 Philadelphia SOX -1.43 360.23 Crude Oil (US$/brrl) +0.59 88.73 Gas (US$/mmbtu) +0.05 3.17 Copper (US$/lb) -0.03 3.35 Gold (US$/oz) +4.80 1582.20 Nickel (US$/lb) -0.15 7.06 Palladium (US$/oz) -7.50 563.50 Platinum (US$/oz) -15.00 1385.00 Silver (US$/oz) -0.03 27.01 Uranium (US$/lb) -0.15 50.00 Canadian Dollar -0.0021 0.9795 30 Year Canada 0.00 2.204 30 Year U.S. -0.03 2.468 Volatility Index (VIX) +1.630 20.25 SpongeBob SquareCoins Silver SpongeBob SquarePants coins minted by a private company in New Zealand were among the assets seized by FBI agents from Peregrine Financial Group after its chief confessed to nearly 20 years of fraud last week. Ira Bodenstein, the trustee in Peregrine’s bankruptcy case in Chicago, said the coins were in a vault at the firm’s Cedar Falls, Iowa, headquarters. The value of the takings was not immediately clear. They were made by NZ Mint, which told local reporters last week it was paid in full by Peregrine for them. The coin disclosure adds a new twist to the case of Peregrine CEO Russell Wasendorf Sr., who was arrested last Friday after he confessed to doctoring bank statements to make regulators think his futures brokerage had nearly twice the assets it did, leaving customers with an estimated shortfall of over US$200 million. CANADA The S&P/TSX Composite fell on Tuesday, as positive earnings news was outweighed by higher borrowing costs for Spain and an unsettling downgrade by Moody’s. The rating agency cut the outlook to negative for the Aaa credit ratings of Germany, the Netherlands and Luxembourg, citing “rising uncertainty” over Europe’s crisis. Rogers Communications (RCI.B), Canada’s largest wireless carrier, reported second-quarter profit that beat analysts’ estimates as job cuts lifted profitability at its main mobile phone unit. Husky Energy (HSE), Canada’s thrird-largest integrated oil producer and refiner, reported a 36% fall in second-quarter profit on lower production and weaker realized crude oil prices. CIC Energy (ELC) late Monday said it has agreed to sell itself to India’s Jindal Steel & Power for $116 million. CIC owns the Mmamabula coal field in Botswana, with an estimated mineral resource of about 2.4 billion metric tones. Eldorado Gold (ELD) said a Greek order which had temporarily suspended surface-clearing activities by its Greek subsidiary has been revoked. It said it will restart such activity as soon as possible. Aeterna Zentaris (AEZ) said it would ask the U.S. Food and Drug Administration to fast-track the approval process for its proposed test to diagnose growth hormone deficiency. UNITED STATES The S&P 500 traded lower for a third day, amid disappointing results at United Parcel Service (UPS). The largest package-delivery company and an economic bellwether, paced declines as it cut its forecast after a drop in international package sales dragged quarterly profit below estimates. Peabody Energy (BTU) dropped after the largest U.S. coal producer forecast third-quarter earnings that trailed analysts’ estimates after metallurgical-coal prices fell and Australia introduced a carbon tax. Texas Instruments (TXN) fell after the largest maker of analog chips forecast third-quarter sales and profit that may miss some analysts’ estimates as an economic slowdown in Europe crimps demand for electronics. Lexmark International (LXK) slumped after the maker of laser and inkjet printers forecast third-quarter profit that missed analysts’ estimate as the economic weakness in Europe erodes sales. DeVry (DV) tumbled after the provider of education services warned that second-quarter results would fall short of most analysts’ estimates, saying it plans to cut 570 jobs amid declining enrolment. Whirlpool (WHR) traded lower as the home appliance maker reported earnings that trailed forecasts.

- 2. – Canadian and U.S. Comments for Wednesday July 25, 2012 2 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. ECON 101 CANADIAN Data Today: No scheduled releases. U.S. Data Today: This morning, New Home Sales (Jun) are expected to rise to 370K from 369K the previous month. ECON 201 In Canada, Retail Sales (May) increased by 0.3%, after losing 0.5% the previous month, while Retail Sales Less Autos (May) increased by 0.5%, after losing 0.3% previously. In the U.S., the Richmond Fed Manufacturing Index (Jul) fell to -17.0 points, after losing 3.0 points the previous month, while the House Price Index (May) increased by 0.8%, after gaining 0.7% before that. MARKET MOVERS Technical Indicators: TSX TSX VENTURE NYSE AMEX NASDAQ Advancing Issues 507 (36%) 302 (27%) 739 (23%) 406 (29%) 688 (27%) Declining Issues 722 (51%) 430 (38%) 2,358 (74%) 952 (68%) 1,772 (69%) Unchanged Issues 177 (13%) 399 (35%) 81 (3%) 32 (2%) 107 (4%) Total Issues 1,406 1,131 3,178 1,390 2,567 New Highs 15 9 107 57 15 New Lows 45 62 94 57 108 Up Volume (000s) 85,756 28,967 493,469 176,155 330,925 Down Volume (000s) 136,252 52,220 2,443,371 162,735 1,097,120 Unchanged Volume (000s) 7,123 26,122 21,212 2,745 23,270 Total Volume (000s) 2,291,310 1,073,088 29,580,526 3,416,356 14,513,147 Source: Yahoo! Finance Notable 52-Week Highs: ATCO Ltd. ACO.X $ 75.62 ATCO Ltd. ACO.Y $ 75.25 Acadian Timber Corp. ADN $ 12.40 Bombardier Inc. BBD.PR.C $ 24.89 Boardwalk REIT BEI.UN $ 65.03 Boralex Inc. BLX $ 9.30 Brookfield Canada Office Prop. BOX.UN $ 28.38 Canadian Wireless Trust CDW.UN $ 10.88 Canadian 50 Advantaged Pref. CPF.UN $ 28.00 Canadian Utilities CU.PR.D $ 26.22 Canadian Utilities CU.PR.E $ 25.88 Dollarama Inc. DOL $ 64.79 General Donlee Canada GDI $ 4.52 Global Dividend Fund GDP.UN $ 4.52 Cdn Premium Select IF HCS.UN $ 13.30 Hardwoods Distribution HWD $ 4.86 Industrial Alliance Ins & Fin IAG.PR.G $ 25.75 REIT INDEXPLUS Income Fund IDR.UN $ 11.97 InterRent REIT IIP.UN $ 4.94 Intertape Polymer Group ITP $ 8.53 Manulife Financial MFC.PR.I $ 25.20 Morguard North American REIT MRG.UN $ 12.00 Morguard Sunstone Real Estate MSN.UN $ 11.85 Northwest Healthcare Prop REIT NWH.UN $ 13.64 Cdn. Real Estate Investment REF.UN $ 43.19 First Asset Canadian REIT IF RIT.UN $ 12.51 RBC Target 2020 Corp. Bond ETF RQH $ 20.80 BMO Aggregate Bond Index ETF ZAG $ 16.12 BMO Mid Federal Bond Index ZFM $ 16.84 BMO Equal Weight REITs Index ZRE $ 20.93 Notable 52-Week Lows: Barrick Gold Corp. ABX $ 33.62 Alexco Resource AXR $ 3.96 Bloom Select IF BLB.UN $ 8.51 Ballard Power Systems BLD $ 1.08 Burcon NutraScience BU $ 5.21 Canaccord Financial CF $ 4.50 COGECO Inc. CGO $ 32.60 iShares Intl Fundamental Fund CIE $ 10.79

- 3. – Canadian and U.S. Comments for Wednesday July 25, 2012 3 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. iShares Japan Fundamental Fund CJP $ 6.32 iShares S&P/TSX Glb Mining Fd CMW $ 15.35 Forbes and Manhattan Coal FMC $ 0.82 Fortress Paper FTP $ 14.27 GMP Capital GMP $ 4.63 Hartco HCI $ 2.39 HBP S&P/TSX GlblBasMetBull+ETF HMU $ 6.20 IGM Financial IGM $ 38.17 Jaguar Mining JAG $ 0.64 Longview Oil LNV $ 6.65 First Asset Can-60 C. Call ETF LXF.A $ 7.60 Midas Gold MAX $ 1.94 Marengo Mining MRN $ 0.12 NovaCopper Inc. NCQ $ 1.80 NGEx Resources NGQ $ 1.54 Pan American Silver PAA $ 13.79 Prophecy Coal Corp. PCY $ 0.16 Pacific North West Capital PFN $ 0.06 Quest Rare Minerals Ltd. QRM $ 1.18 Resolute Forest Products RFP $ 9.67 Richmont Mines RIC $ 3.31 Revett Minerals Inc. RVM $ 3.10 St. Augustine Gold and Copper SAU $ 0.09 Walter Energy WLT $ 33.70 Wildcat Silver WS $ 0.71 Star Hedge Managers Corp. II XHG $ 5.09 iShares S&P/TSX Capped IT XIT $ 5.20 Exeter Resource Corp. XRC $ 1.25 Xtra-Gold Resources XTG $ 1.00 BMO S&P/TSX Base Metals E.T.F. ZMT $ 10.96 CANADIAN EQUITIES OF INTEREST Listed Alphabetically by Symbol Oil Integrateds & Refiners Would the Dark Knight put cheap gas in the Batmobile? Oil integrateds/refiners are set to report later this week. Equity Analysts have paired back expectations not only for the balance of 2012 but for 2013 as well. While bearish expectations seem to be the theme of late, Canaccord Genuity Portfolio Strategist Martin Roberge believes these projections could prove too bearish. Indeed, over the next few years, he believes refining margins should stay elevated due to robust oil output in the Midwest, transportation bottlenecks and growing foreign demand for U.S. oil products. Roberge points out that some of the reasons for wide refining margins (i.e., crack spreads) are well understood. Over the past three years, U.S. oil output from the Midwest has doubled to about 1M bbl/day which has created an unprecedented glut in crude inventories and contained WTI prices. At the same time, rising global oil demand from developing economies has allowed Brent prices to stay resilient in the $105-125 range. With refiners selling energy products in Brent markets, Midwest refiners have enjoyed very fat margins. As long as oil from the Midwest cannot flow fast enough to Gulf Coast refineries, which account for more than half the total U.S. refining capacity, the Brent/WTI spread should stay wide. Eventually, signs that bottlenecks abate should be reflected in lower oil carload volumes and rails’ pricing power. We are not there yet. Now, a less well understood cause for elevated crack spreads are very tight oil product inventories owing to rising demand from foreign markets. From its peak in early 2008, U.S. consumption of energy products has dropped 2.2M bbl/day to 18.7M. However, over the same period, the U.S. has gone from a net importer (2.3M bbl/day) to a net exporter (0.7M bbl/day) of oil products. As a result, total U.S. oil products consumed domestically and in foreign markets have reached new highs at 19.4M bbl/day. This explains why refinery capacity rates continue to increase. Importantly, petroleum products are final motor gasoline (46%), distillate fuel oil (20%), kerosene jet fuel (8%) and other “non power” fuels (26%). Roberge’s data shows that the U.S. is now a net exporter in all of these four categories with gasoline being the predominant product being exported to South American countries notably. So to sum it up, gasoline, distillate and kerosene inventories (74% of all products) oscillate near historical lows while demand keeps rising. Thus, unless foreign demand for U.S. oil products comes to a sudden halt, and inventories start to build, refining margins should stay elevated. Bottom line: Accumulate oil integrated/refiners’ shares during dips and stay overweight the group as refining margins are likely to stay high over the next year or two. Canaccord Genuity Oil & Gas Analyst Phil Skolnick has Suncor Energy (SU) as his favourite integrated. China PMI More cushion; where's the pushin'? China's HSBC Flash PMI, the earliest indicator of China's industrial activity, improved to 49.5 in July, compared to the actual figure of 48.2 in the previous month. Despite a positive move, the index has remained weak and stayed below the 50.0-mark for the ninth consecutive month. Credit Suisse Chief Economist for Non-Japan Asia Dong Tao, expects the official July manufacturing PMI, due to be released on August 1, to stay largely flat from 50.2 seen in June. Growth momentum remains challenged in China, but Dong believes the increased approval of infrastructure projects is likely to provide a cushion to the weak growth pace. The impact from infrastructure projects is not likely to be significant, in Dong's view, as the central government’s funding has its own limit, while local governments lack funding for their share of investments. Banks are

- 4. – Canadian and U.S. Comments for Wednesday July 25, 2012 4 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. only willing to lend to the top-tier local governments, and are more concerned about the underlying creditworthiness of the borrowers now. A swing factor for the economy remains the central government’s attitude towards the property sector. Dong believes the government would like to see stronger sales volume, but would be sensitive to seeing prices surge again. This is the reason why the Chinese government has maintained its harsh rhetoric on the sector. CIC Energy* (ELC : TSX : $1.77), Net Change: 0.20, % Change: 12.74%, Volume: 6,228,789 A Rick Nash-type of discount? CIC Energy entered into a binding merger agreement with India's Jindal Steel & Power. Under the terms of the agreement, ELC shareholders will receive $2.00 per share in cash, which values the total equity of the company at approximately $116.0 million. The Board recommends ELC shareholders accept the Jindal offer. The completion of the merger remains subject to the satisfaction of certain conditions, including, but not limited to, receipt of all requisite regulatory approvals in Botswana (including the receipt of certain approvals from the Minister of Minerals, Energy and Water Resources and under the Botswana Competition Act). The merger agreement provides for an outside date of October 9, 2012 for the completion of the transaction. Customary standstill undertakings not to solicit or invite alternative acquisition proposals and right to match covenants in favour of Jindal have been put into place. ELC has agreed to pay Jindal a termination fee of approximately C$3.5 million if the merger is not completed in certain circumstances. ELC will hold a special meeting of shareholders to consider and approve the merger. The meeting is scheduled to be held on or before August 28, 2012. ELC is focused on the advancement of the Mmamabula Energy Complex at the Mmamabula Coal Field in Botswana, Africa. Jindal Steel & Power is one of India's major steel producers with a significant presence in the mining, power generation and infrastructure sectors. On July 18, ELC confirmed that it is in advanced negotiations with Jindal regarding the possible acquisition of the company. On that day, ELC shares moved from $1.41 to $1.51. With ELC shares trading at a substantial discount to Jindal's $2.00 per share offer, the market is heavily discounting the chance the deal closes. Eldorado Gold* (ELD : TSX : $10.35), Net Change: 0.39, % Change: 3.92%, Volume: 1,769,390 If you're operating a chainsaw naked, you may not be the sharpest tool in the shed. Eldorado Gold caught a bid after announcing that the ban on tree cutting activities at its Skouries had been lifted. On June 29, 2012, the Suspension Committee of the Council of State, Greece’s highest administrative court, temporarily suspended tree cutting activities in the Halkidiki forest region, where the company operates the Stratoni silver-lead mine and is developing the Skouries and Olympias gold projects (officially announced on July 4, 2012). ELD has shown that it legally has the right to clear the surface and the Suspension Committee agreed. The suspension order has been revoked and surface clearing activities may resume (drilling activities on already cleared land had not been interrupted). The judges found that this investment is of particular benefit to the Greek economy," an official at the Council said. According to a Reuters article, the ruling, however, is temporary until the Council holds a full hearing on the case at a later point, according to the court official and another official close to the proceedings. Paul N. Wright, Chief Executive Officer of ELD, commented, "We are very pleased with the decision of the Council of State and will re-initiate our surface clearing activities in Halkidiki as soon as practically possible”. He adds, "Furthermore, we have full confidence in the integrity of our permits in Greece and in the judiciary, legislative, and executive institutions of the Hellenic Republic." A Bay Street analyst notes that this news is positive for the stock as Skouries is worth approximately 7% to his 5%/peak NAV (Skouries discounted at 10%). Of note, the stock lost approximately 7% on July 4 (versus flat performance for the group) and has lost an additional 19% since then (versus approximate 12% decline in the group). Gold Canyon* (GCU : TSX-V : $1.23), Net Change: -0.04, % Change: -3.15%, Volume: 110,300 Continues adding ounces. Gold Canyon Resources announced further positive assay results from its 2012 barge drilling program at its 100%-controlled Springpole Gold Project located 110 km northeast of the Red Lake Mining Camp, Ontario. Included in the most recent results was an intercept of 361 m of 1.08 g/t gold from Hole SP12-160. Commenting on the results, Dr. Quinton Hennigh, technical advisor to, and director of, Gold Canyon, stated, "Step-out drilling by barge early this summer indicated the Portage Zone continues to the 0-250 meter section. Given this encouragement, we decided to quickly infill drill this southeastern part of the deposit with the goal of adding ounces to our upcoming NI 43-101 compliant resource update. Results from recent drill holes in this area continue to provide strong encouragement that we can quickly grow the deposit." Currently, four drills mounted on barges continue to operate at Springpole, with nearly 31,500 m of diamond core drilling having been completed to date. In addition to an updated resource estimate, expected to be completed in Q4, 2012, work on a PEA of the Springpole deposit is on-going with a schedule completion in Q1 or Q2, 2013. Husky Energy* (HSE : TSX : $24.73), Net Change: -0.39, % Change: -1.55%, Volume: 512,673 The Dog Whisperer. Husky reported Q2/12 results, clean EPS of $0.45/share was ahead of Canaccord Genuity Oil & Gas

- 5. – Canadian and U.S. Comments for Wednesday July 25, 2012 5 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. Analyst Phil Skolnick's $0.29/share forecast and consensus average of $0.36/share. The reported $1.17 CFPS (diluted) also beat both the Street and Skolnick's $1.00 estimate. However, Q1/12 production of 281.9 MBOE/d was below both Skolnick's 293 MBOE/d estimate and the Street’s 289 MBOE/d. The EPS/CFPS beat was a result of better-than-expected netbacks in various areas, lower-than-estimated DD&A, and stronger-than-expected downstream earnings. HSE's 2012 production guidance was maintained at 290-315 MBOE/d. The company has also agreed with its principal shareholders that they will go back to receiving dividends in cash instead of shares, starting with this dividend payment. IMAX* (IMX : TSX : $23.46), Net Change: -0.43, % Change: -1.80%, Volume: 73,487 IMAX* (IMAX : NYSE : US$22.89), Net Change: -0.51, % Change: -2.16%, Volume: 899,681 Gotham's reckoning. The Dark Knight Rises posts $23.8 million on IMAX during opening weekend: IMAX released their box office estimates for the Dark Knight Rises and the numbers were very impressive and in Canaccord Genuity Media Analyst Aravinda Galappatthige’s opinion could not have been any higher given the screen count. Domestically the title generated $19 million in IMAX off 332 screens. This is 11.8% share of the total domestic gross for the title. The opening weekend (domestic) PSA (per screen average) was $57,200. This is ahead of even The Avengers opening weekend PSA of $56,000. The Avengers holds the record for the biggest opening weekend in history overall. Further, last year's Harry Potter finale generated a PSA of $55,500 domestically on IMAX. On the international front, the title generated $4.8 million in IMAX for a global total of $23.8 million. Internationally, it was released on 64 screens with another 89 due to open over the next several weeks. The international PSA was $75,000 well ahead of the $67,000 posted during the opening weekend of the Harry Potter finale. Galappatthige expects $130 million from The Dark Knight Rises for the full run in IMAX. Galappatthige is at the high end of expectations in this respect (Street estimates are $70-130 million). Martinrea International* (MRE : TSX : $8.06), Net Change: -0.03, % Change: -0.37%, Volume: 1,050,650 On cruise control or is the floor mat stuck again? Auto parts makers have produced good share price appreciation in 2012 on strong Q1/12 results and the road ahead appears all clear. Canaccord Genuity Auto Components Analyst David Tyerman expects EPS strength to continue in Q2/12 from the following factors: 1) Rebounding industry in North America. His forecast has been increased in this report. 2) Strong sales growth profiles for Martinrea and Linamar (LNR). 3) Margin expansion expected for LNR, MRE and Magna International (MG). Certainly, there are issues, including poor European prospects and LNR’s and MRE’s somewhat stretched financial leverage, but Tyerman believes the overall outlook for these companies remains good to very good. Valuations also remain attractive, with all three names trading at single-digit P/Es on his 2012 and 2013 forecasts. As we head in earnings season, Tyerman expects the EPS of MRE (Focus List pick) to surge 51.5% YOY in Q2/12, continuing the trend of the past couple of years. Drivers should include extremely strong sales growth (52.7%) and margin expansion (EBIT margin up 0.3% to 5.4%), partially offset by higher interest costs. He expects flat sequential EPS on relatively stable sales and margins. Longer-term his forecast outlook is also robust based on strong sales growth and margin expansion. Tyerman expects sales growth in coming years to be driven by rebounding industry sales and more recently from the July 2011 Honsel acquisition ($680 million annualized sales added) along with new business launches. Importantly, he expects that as the company launches its large backlog, it will generate margin expansion from increased capacity utilization. Also, he expects further margin improvements at Honsel, as MRE continues to chip away at improving profitability at the large Meschede, Germany operation. Note that Honsel is already nicely profitable. Given that sales growth plus margin expansion should translate into strong EPS growth, Tyerman continues to project substantial EPS growth over his forecast horizon from a combination of good CPV growth from backlog, moderately increasing industry production and significant margin expansion from better overhead absorption. He reiterated his bullish stance, noting that despite a very solid outlook, MRE trades at the low end of its historical EV/NTM EBITDA and P/E multiples. Nevsun Resources* (NSU : TSX : $3.17), Net Change: 0.22, % Change: 7.46%, Volume: 371,199 Positive confirmation. Shares of Nevsun jumped Tuesday after the gold producer released a new increased base metal NI 43- 101 compliant mineral resource and reserve estimate at its 60%-owned Bisha Mine in Eritrea. The update was highlighted by a 6% increase in contained copper and 38% increase in contained zinc, compared with the previous reserves estimate completed January 1, 2011. Management stated that the new estimate underscores the fact that the Bisha Mine is one of the highest grade open-pit base metals deposits in the world. Nevsun now intends to continue drilling while re-starting generative exploration in 2012 with the objective of further increasing reserves and extending the mine life at Bisha. The company expects base metals production at Bisha to commence in mid-2013 and continue until 2024. The mine has been producing gold since 2011 but, as previously disclosed, management currently expects Bisha to complete oxide gold production in the first quarter of 2013. Also on Tuesday, Nevsun reiterated its forecast for full-year 2012 gold production guidance of 240,000-260,000 ounces and noted

- 6. – Canadian and U.S. Comments for Wednesday July 25, 2012 6 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. that it intends to re-evaluate this guidance in August when reviewing the full quarter financial results with the added benefit of observing actual mining results for the month of July. Nexen* (NXY : TSX : $26.37), Net Change: 0.02, % Change: 0.08%, Volume: 17,706,186 She looks attractive, but is she? On Monday, China National Offshore Oil Corporation (CEO) entered into definitive agreement to acquire Nexen for US$15.1 billion, or US$27.50 per share in cash. According to Canaccord Genuity Oil & Gas Analyst Phil Skolnick, the current arb spread (~12% annualized at current intraday levels assuming the deal closes at the mid- point of Q4) looks attractive, but the key issue right now is whether or not the deal will be approved. Canadian Minister of Industry Christian Paradis, confirmed on Monday that the CEO and NXY transaction is subject to review under the Investment Canada Act. Skolnick sees a very good chance the deal closes given that NXY has a relatively small exposure to Canada (28% of its current production) and in light of CEO’s commitment to retain NXY’s management team and employees, establish Calgary as its North and Central American headquarters and list CEO on the TSX. However, there is risk that the government may not want to see the Chinese own 100% of the Long Lake project and ~16.26% of the Syncrude project, but Skolnick believes NXY’s board would have taken this into consideration before approving the deal. With respect to the U.S., Skolnick does not see any issues given this is mostly deepwater Gulf of Mexico prospects and NXY is only producing about 16 MBOE/d (or 8% of total corporate production), which is on the decline. One possible result, if needed, could be some asset sales to help satisfy regulators in both Canada and U.S. Rogers Communications* (RCI.B : TSX : $39.09), Net Change: 1.85, % Change: 4.97%, Volume: 3,141,644 Do It All In One Phone Call? Rogers reported Q2/12 margins and cash flow that exceeded Canaccord Genuity's estimates and consensus. At $3,106 million consolidated revenue was below Canaccord Genuity Telecommunication Analyst Davi Ghose's $3,131 million estimate and consensus of $3,145 million and up a modest 0.3%. However, adjusted EBITDA of $1,276 million easily beat Ghose's $1,211 million forecast and was above consensus of $1,255 million and up 2.6%, driven by a 4.6% increase in wireless EBITDA. Consequently, adjusted and diluted EPS of $0.91 beat Ghose's $0.82 estimate and consensus of $0.87 and was up from $0.85 in Q2/11. Finally as a result of very low capex and cash taxes, FCF of $633 million exceeded Ghose's $413 million forecast and consensus of $410 million and was up from $561 million in Q2/11. Capex of $458 million was well below Ghose's $525 million forecast and consensus of $534 million and was down 11.9% YoY, but this seems timing related as full- year capex guidance of $2,075-$2,175 million was reaffirmed. In addition, at only $23 million cash taxes were well below Ghose's $105 million forecast and consensus of $130 million, but up from only $3 million in Q2/11. RCI reaffirmed guidance, the company still expects 0-4% adjusted EBITDA growth in 2012. RCI must generate 1.4% YoY adjusted EBITDA growth in H2/12 to make the low end of full year guidance and 9.5% to make the high end. Key risks to Rogers meeting guidance include: 1) loss of high margin wireless roaming revenue; 2) continued subscriber pressure on the cable segment and 3) media pressures. In addition, in Ghose's view Rogers Wireless remains in a relatively weak strategic position due to the Bell (BCE)/TELUS (T) wireless network and roaming agreement. Finally, with rising cash taxes expected again in 2013 as per RCI’s release, FCF could be under pressure again in 2013 and the stock does not look particularly cheap. Nonetheless, Ghose expects RCI to benefit from the stronger than expected wireless and consolidated financials. Red Eagle Mining* (RD : TSX-V : $0.53), Net Change: 0.01, % Change: 1.92%, Volume: 50,700 Golden steps. Red Eagle Mining, which has had a successful summer so far thanks to a consistent flow of impressive assay results. announced another set of assay results from its 5,400-m Phase Two core drill program at the San Ramon gold system located within the Santa Rosa gold project in Colombia. Management highlighted that the new results show strong gold mineralisation over significant intervals, including Hole SR-060 which intersected 11.4 m of 16.04 g/t gold, including 2.0 m at 30.73 g/t gold and 3.5 m at 29.29 g/t gold. Hole SR-060 was collared 180 m to the west of Hole SR-053, which intercepted 7.0 m at 41.53 g/t gold and 480 m to the west of Hole SR-042 which intercepted 6.0 m at 31.85 g/t gold. Management also highlighted that Hole SR-060 intercepted high-grade mineralisation at a slightly shallower depth (~130-140 m) which will significantly enhance open pit evaluations. Assays have now been received for 20 holes with assays pending on 4 holes (SR-062 to SR-065) from Phase Two and 14 holes (SR-066 to SR-079) from Phase Three. Commenting on the results to date, Red Eagle's CEO, Ian Slater, said, "Our phase two drilling at San Ramon continues to deliver outstanding results. The significant increase in grade is encouraging as we move forward to resource and mining (open pit and underground) evaluations." Sprott Power* (SPZ : TSX : $0.97), Net Change: 0.01, % Change: 1.04%, Volume: 110,612 It's Uncle Buck! Sprott Power bucked the broader market's downtrend on solid Q2/12 results as new capacity entered service and another Bay Street analyst initiated coverage. The company generated 43.3 GWh, ahead of Canaccord Genuity Power

- 7. – Canadian and U.S. Comments for Wednesday July 25, 2012 7 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. Analyst Jared Alexander’s estimate of 36.1 GWh. Likewise, EBITDA for the quarter amounted to $2.2 million versus his estimate of $1.8 million and 73% above Q2/11 as operations commenced at the company’s Amherst wind farm during the quarter. The wind farm, which was completed on time and on budget during the second quarter, produced 9.5 GWh net to Sprott Power. Quarterly CFPS was $0.01/share, in line with estimates. The payout ratio, net of principal repayments, was 253% for the quarter. While high, this is not surprising given that Q2 and Q3 are seasonally weak quarters for the company. Alexander expects the payout ratio for the full year to improve to 106% (55% before expected debt repayments). For the full year, he continues to expect EBITDA to amount to $11.0 million for 2012, approximately 2.3 times the company’s 2011 performance. This growth is being driven by the recently completed Amherst wind farm and to a lesser extent the 2.3 MW Glace Bay expansion. Construction has commenced at Glace Bay and the company expects to complete the expansion late in the third quarter of this year. Longer term, Alexander expects EBITDA to more than double again by 2014 to $23.5 million. This increase is attributable to a full-year contribution from the Amherst wind farm as well as the Goulais project which is expected online towards the end of 2013. He continues to expect Sprott Power to generate $0.09/share of CFPS in both 2012 and 2013. After accounting for debt repayment, Alexander estimates the company will have a 2012 payout ratio of 106%. In 2013 the payout ratio is expected to improve to 87%. Alexander reiterated his bullish stance, noting that he believes that growth should drive an improving payout ratio which may fuel dividend increases. Talisman Energy* (TLM : TSX : $11.79), Net Change: -0.01, % Change: -0.08%, Volume: 6,858,828 I'm looking more attractive...today. Canaccord Genuity Oil & Gas Analyst Phil Skolnick upgraded Talisman on the back of Nexen (NXY) announcing it is being acquired by CNOOC for $15.1 billion, or US$27.50 per share, in an all-cash transaction. Skolnick believes it is a positive indicator of TLM’s ability to be acquired given its mixture of international assets (55% of production is outside of North America). Even though TLM does not have the same long-life oil sands assets that NXY has, SE Asia is a highlight, in his view, that could motivate a buyer of the company given it offers production growth (expecting 8% CAGR) + potentially rising gas prices. Further, Skolnick notes that TLM is currently undergoing another transformation. As he had pointed in an earlier report, TLM stated that it wants to do more than sell up to 50% of its North Sea interest, and it could potentially monetize longer dated assets that won’t cashflow for years in order to sharpen the focus of the company. While TLM indicated that now is not the time to do a corporate break-up (a la Encana (ECA)), he believes such divestiture talks naturally open up the door for discussions around an outright sale. TLM’s plans to sell to Sinopec (SNP) 49% of its North Sea asset could be a stepping stone, in his view, making TLM more acquirable as it leaves it with increased exposure to more desirable growth assets in Colombia, North America, and SE Asia and decreased exposure to the volatile North Sea production base. Bottom line, Skolnick believes either TLM fixes itself or he sees it being sold. Now of note, if it weren’t for the NXY acquisition, Skolnick says he would be less excited about what the North Sea sale means to TLM, but TLM trades at 4.3x 2013E DACF, and at a ~$11.2 billion market cap an acquirer can get ~409 MBOE/d of production added to itself. The NXY takeout metric of 5.8x 2013 DACF implies a 45% upside to TLM shares post the U.K. sale. He is raising his target price by 7% on re-rating associated with the NXY takeout. Skolnick does caution that risk to this thesis is that timing is everything, and falling oil prices can make it more of a net cash user, which would provide for some negative sentiment on the stock. That said, he believes that further negative sentiment associated with an operational upset could motivate a push to sell the company. U.S. EQUITIES OF INTEREST Listed Alphabetically by Symbol Apple (AAPL : NASDAQ : US$601.09), Net Change: -2.74, % Change: -0.45%, Volume: 14,801,521 iMissed. Apple reported its much-anticipated earnings after the close on Tuesday. For the third-quarter, the consumer electronics giant posted a profit of $9.32 per share on revenue of $35 billion, missing the Street’s expectations of $10.36 per share on $37.1 billion in sales. Wall Street expected Apple to ship 29 million iPhones during the June quarter — the figure investors were most anxious about — and actual iPhone shipments came in at just 26 million units. iPad channel sales totalled 17 million beating Street’s consensus for16 million units, and iPod family shipments slid in at 6.8 million units compared to analysts’ 5.9 million-unit consensus. Mac channel sales were expected to total 4.1 million units, and Apple reported shipping 4 million Mac computers in the third fiscal quarter. “We’re continuing to invest in the growth of our business and are pleased to be declaring a dividend of $2.65 per share,” said Peter Oppenheimer, Apple’s CFO. “Looking ahead to the fourth fiscal quarter, we expect revenue of about $34 billion and diluted earnings per share of about $7.65.”

- 8. – Canadian and U.S. Comments for Wednesday July 25, 2012 8 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. Baidu (BIDU : NASDAQ : US$114.54), Net Change: 7.44, % Change: 6.95%, Volume: 15,713,499 Did you? Baidu, China's largest search engine, reported better-than-expected second-quarter results as advertising revenues surged and customer base continued to increase. Net income climbed to 2.77 billion yuan ($434 million), or $1.24 per American Depositary Share. That exceeded the 2.5 billion yuan or $1.11 per ADS average of analysts’ estimates. Revenue rose 60% to 5.46 billion yuan ($858.8 million). Earlier last week, concerns that a weakening Chinese economy would hurt its big clients sent shares of Baidu tumbling to an 18-month low. However, the company's recent results, including its revenue outlook, underscored that business remained healthy for China's No.1 Internet search engine. Analysts said that being the biggest player in the sector had given Baidu more bargaining power with firms looking to advertise on its portal. For the third quarter, Baidu forecast a revenue between 6.25 billion yuan ($983 million) and 6.41 billion yuan ($1.01 billion), bracketing the average $993 million estimate from analysts. CEO Robin Li said that he expects a "hyper growth" in mobile users, but also said that the mobile Internet was still in a nascent stage. Li added, "We will maintain momentum by rolling out optimized sales processes and more advanced tools to help current and potential customers increase returns on their online marketing spend. We will also continue to actively explore the vast opportunities in China's fast-emerging mobile Internet and cloud sectors." Peabody Energy (BTU : NYSE : US$20.51), Net Change: -2.65, % Change: -11.44%, Volume: 19,841,613 It's Christmas in July, and I got another lump of coal! Shares of Peabody Energy were in the red Tuesday after the company’s Q2 results missed the mark and management provided disappointing guidance for Q3. Earnings came in at $0.51 per share versus the consensus forecast of $0.54 and Credit Suisse’s $0.52 estimate. Earnings in the quarter benefitted from lower than expected expenses, helping to offset weak results in Australia. Looking ahead, management forecast earnings of $0.20-0.45 per share while analysts were expecting $0.65 and Credit Suisse was looking for $0.83. The company’s Australian ops are expected to weigh on Q3 numbers with higher costs, lower overall pricing, a longwall move, the timing of export shipments and the introduction of a carbon tax being cited as reasons for weak results. Shares of Peabody have shed nearly 45% of their value this year as investors exit U.S. coal companies due to lower natural gas prices. Many power producers are shifting to gas as a cheaper source of power than coal, a move which analysts believe could be permanent. Coal demand remains strong in India and China, and Peabody is looking to expand in that area. It recently completed a $5 billion acquisition of Macarthur Coal to capitalize on strong Asian demand. Cisco Systems (CSCO : NASDAQ : US$15.08), Net Change: -0.99, % Change: -6.16%, Volume: 92,243,414 Proxy that! Cisco Systems confirmed plans to eliminate about 1,300 jobs, or 2% of the workforce, as it looks to streamline its business in the face of economic uncertainty. Credit Suisse believes the announcement speaks to both stronger than hoped for rev headwinds consistent with the macroecon climate. Separately, rival software maker VMware (VMW) announced it was buying computer networking specialist Nicira for nearly $1.3 billion. Credit Suisse believes VMW’s pending acquisition is a relatively more serious issue as the deal is meant to expand VMware's product line in the rapidly growing field of computer "virtualization." The idea coming out of some circles is that Nicira’s business model has been based on establishing one universal Ethernet switch and eliminating the proprietary switches like those made by CSCO and Juniper (JNPR). Credit Suisse believes the acquisition represents a long-term competitive threat to CSCO’s revenues and margins. However, in the near-term, CSCO has dramatically improved its competitive position, taking back share in its core enterprise switching and carrier routing businesses. Credit Suisse sees CSCO as well-positioned to benefit from improvement in end demand. Separately, CSCO’s $5bn acquisition of U.K. video service provider NDS has received approval from the European Commission (EC), after it ruled there was no potential for the deal to create an uncompetitive market. The deal will see CSCO incorporate the firm's technology into its own Videoscape product and help CSCO push into new emerging markets, such as India and China. DeVry (DV : NYSE : US$20.64), Net Change: -6.93, % Change: -25.13%, Volume: 10,595,202 Not VRY good grades. Shares of DeVry plunged after the for-profit education provider forecast downbeat results for its fiscal fourth quarter and said it plans to cut its workforce amid continued weakness in student enrollment. DeVry expects fourth- quarter adjusted earnings of $0.43-0.46 per share, on revenue of $500-510 million. Analysts on average were expecting earnings of $0.78 per share on revenue of $516.7 million. The company has been considered by industry watchers as one of the stronger school operators, thanks to its business, technology and health-care course offerings. Still, it hasn't been immune to the enrollment declines seen across the industry in the wake of tightened regulatory oversight of the for-profit education sector. Prospective students are also getting increasingly averse to the idea of taking out costly education loans, given the high unemployment rates, forcing colleges to spend more on scholarships and other incentives to lure new students. DeVry, which runs Keller Graduate School of Management, Chamberlain College of Nursing, Ross University and the Carrington Colleges

- 9. – Canadian and U.S. Comments for Wednesday July 25, 2012 9 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. Group, said it expects new enrollment to fall 15-17% at its DeVry University and 19-21% at Carrington Colleges. Also, DeVry plans to eliminate 570 jobs, in the fourth and the first quarter, and targets savings of at least $50 million in fiscal 2013. Netflix (NFLX : NASDAQ : US$80.30), Net Change: 0.36, % Change: 0.45%, Volume: 5,954,288 Change the channel, please. Netflix shares collapsed in after-hours trade, even as it reported better-than-expected earnings. The company beat on the bottom line, reporting earnings per share of $0.11 on revenue of $889 million. In comparison, the Street had a lower forecast of just $0.05 EPS on revenue of 889 million. Revenue improved some 13% to $889 million, roughly in line with estimates. Equally important were the subscriber numbers, investors were looking for 24.3 million domestic streaming subscribers, 9.1 million DVD subs, and 3.7 million subscribers from Canada, Latin America and the UK. However, Netflix didn’t quite get there. The company added only about 500,000 domestic subscribers during the period, below estimates that went as high as 800,000. The company reported it currently has 23.9 million domestic subscribers, 9.2 million DVD, and 3.6 million international. Netflix now projects it will end the third quarter with 24.9-25.7 million streaming subscribers. At that pace, the company says it would record third quarter sales of $890-911 million, which is in line with expectations for guidance of $907.5 million. Pfizer (PFE : NYSE : US$23.32), Net Change: -0.28, % Change: -1.19%, Volume: 32,273,491 Elan (ELN : NYSE : US$11.67), Net Change: -1.84, % Change: -13.62%, Volume: 19,721,048 Johnson & Johnson (JNJ : NYSE : US$67.28), Net Change: -0.83, % Change: -1.22%, Volume: 10,288,468 I just forgot what I was about to say. Pfizer, Johnson & Johnson, and Elan’s experimental Alzheimer’s disease treatment failed to prove effective in the first of four high-stakes late-stage trials in patients with mild to moderate forms of the memory-robbing disease. The drug failed to improve cognitive and life function, the primary goals of the trial. Instead, it appeared to have a dangerous side effect of edema (swelling in the brain), compared with patients taking placebos. The trial involved people who carry a variation of a gene called ApoE4 that makes them much more vulnerable to the disease. Its treatment, Bapineuzumab, is in a race with a similar product from Eli Lilly & Co. (LLY) to become the first therapy to target a cause for Alzheimer’s, rather than just its symptoms. Pfizer said it and its partner J&J would continue with three other late-stage trials of their medicine, based upon a review by independent safety monitors. Alzheimer’s is the most common form of dementia and the sixth leading cause of death in the U.S. An estimated 5 million Americans are believed to have the disease, and an estimated 36 million people worldwide are believed to have dementia, including Alzheimer’s disease, Pfizer said. On the news of the drug’s failure, U.S.-listed shares of Irish drugmaker, Elan, which has a longstanding financial interest in the drug plummeted the most of the three companies involved. Texas Instruments (TXN : NASDAQ : US$26.48), Net Change: -0.34, % Change: -1.27%, Volume: 10,847,544 I thought everything was bigger in Texas? Texas Instruments reported a 34% decline in its Q2 profit after Monday’s closing bell, saying an uncertain economic climate is leading to caution amongst its customers. Earnings came in at $0.38 per share on revenue of $3.335 billion (including a $0.06 impact to EPS from the acquisition of National Semiconductor) while analysts were looking for $0.41 on $3.347 billion and Canaccord Genuity Technology Analyst Bobby Burleson was expecting $0.35 on $3.35 billion. Management guided Q3 revenue below the consensus view, to $3.21-3.47 billion (a midpoint of $3.34 billion). This compared to consensus estimates of $3.54 billion and Burleson’s estimate of $3.61 billion. GAAP EPS is expected to range $0.34-0.42, including $0.07 impact from acquisition and restructuring charges. This compared to the consensus estimate of $0.50 (non-GAAP) and his $0.44 estimate. Burleson believes growth is likely to remain slow in the back half of the year due to a lack of seasonality for PCs and handsets, exacerbated by inventory growth for analog ICs in the Asian distribution channel exiting Q2 according to his checks. He remains neutral on shares of Texas Instruments and is lowering his target price to reflect for a reduced earnings outlook. Under Armour (UA : NYSE : US$52.71), Net Change: 4.33, % Change: 8.95%, Volume: 9,772,399 Sprinting ahead. Under Armour’s second quarter profit rose by 6.8% on strong sales growth across the board, offsetting rising marketing costs and management boosted its full-year outlook, sending shares higher on Tuesday. The company posted a profit of $6.7 million, or $0.06 per share in the quarter while analysts were expecting $0.05. Revenue increased by 27% to $369.5 million versus the $359 million analysts were looking for growth in the quarter was driven by 44% increase in footwear revenue, a key area for company growth as Under Armour continues to release new products. CEO Kevin Plank expects the growth to continue, saying the company is gaining momentum in footwear with its recently launch Spine running shoe and the Highlight football cleat. Its accessories and apparel divisions also posted double digit sales growth, helping revenue beat expectations. Looking ahead, management raised its full-year outlook. Sales growth is expected to be up 22-24% from 21-22%

- 10. – Canadian and U.S. Comments for Wednesday July 25, 2012 10 This publication is a general market commentary and does not constitute a research report. Any reference to a research report or a recommendation is not intended to represent the whole report and is not itself a research report or recommendation. This commentary is for informational purposes only and does not contain investment advice. This publication may be wholly or partially based on industry rumour, gossip and innuendo and as such is not to be relied upon as investment advice. previously, and EBIT growth is now expected to be 26-27% from 25-26%. Canaccord Genuity Consumer Products Analyst Camilo Lyon believes the full year guidance to be conservative given an improving gross margin and expense picture coupled with multiple growth drivers heading into the back half of the year. United Parcel Service (UPS : NYSE : US$74.01), Net Change: -3.94, % Change: -5.06%, Volume: 11,560,316 FedEx (FDX : NYSE : US$87.39), Net Change: -1.87, % Change: -2.09%, Volume: 3,413,841 Return to sender. United Parcel Service, the world’s largest package-delivery company, cut its full-year forecast after a drop in international package sales dragged quarterly profit below analysts’ estimates. The company lowered its full-year outlook to $4.50-4.70 a share, from its prior earnings estimate of $4.75-5.00 per share, and said customers are more concerned about the economy in the second half of the year. Profit of $1.15 a share in the second quarter trailed the average estimate from analysts of $1.17. Revenue rose to $13.35 billion from $13.19 billion a year ago, but fell shy of the $13.7 billion expected on average. Growth was slower than last quarter’s 4.4% expansion partly because of customers opting for less expensive shipment options. “Increasing uncertainty in the United States, continuing weakness in Asia exports and the debt crisis in Europe are impacting projections of economic expansion,” Scott Davis, UPS CEO, said in a statement. The revised full-year outlook would represent an increase of between 3% and 8% over 2011 adjusted results. UPS is viewed as an economic bellwether because of the volume of goods it handles. The value of packages that UPS moves in its trucks and planes is equivalent to about 6% of U.S. GDP and 2% of global GDP. The delivery company expects to close on its biggest takeover in its 105-year history in the fourth quarter, the purchase of Dutch company TNT Express. The company’s exposure to problems in Europe will increase with its purchase of TNT Express, which will make UPS the market leader in Europe and broaden its reach in Asian and Latin American markets. EU antitrust regulators last week said they were concerned about the combined company's high market share and broadened their investigation of UPS’s bid. Rival FedEx fell in sympathy. COFFEE BEANS – It must be one of the last frontiers for Olympics fever. The chief of Asia’s broadcasting union is in North Korea on Tuesday for talks on providing the country with TV and radio coverage of this year’s games. During the 2010 soccer World Cup in South Africa, North Korean state television aired unprecedented coverage of three matches as well as snippets from the opening ceremony but not the games played by wartime enemies South Korea and the U.S. (FoxNews.com) – A jaw-dropping moment really can make time appear to stand still, or at least slow down, new research suggests. Regular “awesome” experiences, like seeing the Grand Canyon or the Northern Lights, may also improve our mental health and make us nicer people, claim psychologists at Stanford University. The findings raise the prospect of “awe therapy” to overcome the stressful effects of fast-paced modern life. The new research found that by fixing the mind to the present moment, awe seems to slow down perceived time. (Reuters) THE LAST DROP: I’m going from a team having the most losses to a team with the most wins, so it’s been hard to maintain my excitement in that regard. – Ichiro Suzuki, through an interpreter, on being traded from the Seattle Mariners to the New York Yankees after 11 1/2 years * Canaccord Genuity and its affiliated companies may have a Corporate Finance or other relationship with the company and may trade in any of the Designated Investments mentioned herein either for their own account or the accounts of their customers, in good faith and in the normal course of market making. The authors have not received, and will not receive, compensation that is directly based upon or linked to one or more specific Corporate Finance activities, or to coverage contained in the Morning Coffee.