The document provides information on calculating various financial ratios from a company's financial statements. It includes the formulas and calculations for ratios such as: gross profit ratio, net profit ratio, return on capital employed ratio, return on equity ratio, debt-to-equity ratio, current ratio, and inventory turnover ratio. It also defines key terms needed to compute the ratios, such as determining current assets, current liabilities, equity, assets, gross profit, net profit, and capital employed.

1. hapter: Sin

Financial Statement Analysis

6/2

Total asets tumover Net Sale

Avemge Total Asse

Significance:

ratio measures the efliciency with which a comnpany

u

uses its asscts to generate

the

sales

assets of t

total assets turnover, the larger will be the incone on cach dollar invested in the as r

The

business.

Example.

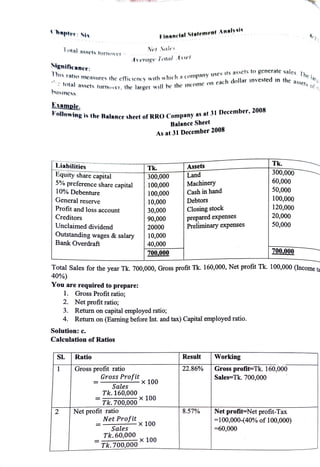

Follo

' s the Balance sheet ofRROCompany as at 31 December, 2008

Balance Sheet

As at 31 December 2008

Liabilities

Equity share capital

5% preference share capital

10% Debenture

Tk.

300,000

60,000

50,000

100,000

Assets

Tk

300,000

100,000

100,000

10,000

Land

Machinery

Cash in hand

General reserve Debtors

Closing stock

prepared expenses

Preliminary expenses

120,000

20,000

50,000

Profit and loss account 30,000

90,000

Creditors

Unclaimed dividend 20000

Outstanding wages &salary

Bank Overdraft

10,000

40,000

700.000 700.000

Total Sales for the year Tk. 700,000, Gross profit Tk. 160,000, Net profit Tk. 100,000 (ncome ta

40%)

You are required to prepare:

1. Gross Profitratio

2. Net profit ratio;

3. Return on capital employed ratio,

4. Return on (Earning before Int. and tax) Capital employed ratio.

Solution:c.

Calculation of Ratios

SI. Ratio Result Working

Gross profit ratio

Gross Profit

22.86%Gross profit=Tk. 160,000

Sales=Tk. 700,000

x 100

Sales

Tk.160,000

Tk.700,000

x 100

Net profit-Net profit-Tax

-100,000-(40% of 100,000)

=60,000

Net profit ratio 8.57%

Net Profit 10

x 100

Sales

Tk.60,000

x 100

Tk. 700,000

2. hapter: Sin Financinl Statement Analysis 6/23

Retum on Capitalemploycd ratio 12.29%Interest-interest of Debenture

Net profit after tax + interest

3

-

10% of 100,000

Capital employed 10,000

Capital employed=Total Asscts

Current liabilities-Fictitious Asscts

x 100

Tk.60,000 + Tk.10,000

x 100

Tk.490,000 =700,000-160,000-50,000

=4,90,000

Or, Capital employed=Total

liabilities-Current liabilities-|

Fictitious Assets

=700,000-160,000-50,000-490,000

Or, Capital employed=Share

capital+reserve&surplus-Long term

Liabilities-Factitious assets

=(300,000+100,000+(10,000+30,00

0) +100,000-50,000

=Tk. 490,000

Return on Earning before interest | 20.41% Net Profit before interest and tax

and Tax capital employed ratio=

Net profit before interest& tax

Capital employed

=Tk. 10,000

x 100

Tk.100,000

100

Tk.490,000

Activity Gama Company

Balance sheet

December 31, 2012

Assets

Current assets

Tk.10000000

1500000

2500000

Plant assets

Total assets

Liabilities and stock holders

Equity Tk.1000000

750000

Current liabilities

Long term liabilities

Total liabilities

Share holders equity

Total liabilities and stock holder equity

1750000

750000

2500000

Income statement data appear below:

Net sales

Tk. 3750000

40000

Interest expenses

The following account balances existed at December 31,

225000

2011 Tk. 2000000

Total assets 650000

Stockholdersequity

3. 6/24

Chapter: Six Financial Statement Analysis

The tax rate is 35 percent, industry norms as of December,

***

Industry

31 20122 are

standards

1.75

Debt/ equity ratio

Profit margin .12

0.15

Return on total assets 0.30

Return on stock holders equity 1.71

Total asset turnover

yanuate the following ratios for Gama Company as of December 31, 2012:

() Debt/equity ratio,

(i) Profit margin

ii) Return on total assets;

iv) Return on stock holders' equity

(v) Total asset turnover.

Classification ofRatio on the basis of Objective:

Ratio to Test Liquidity or Short Term Solvency: - Standard Rato

1CurrentRatio 2:1

1:1

2 | Liquid Ratio

1:1

WorkingCapitalRatio 8 Times

4 Inventory turnover ratio

4-6 Times

Accounts Receivable Turnover Ratio

4-6 Times

Accounts Payable Turnover Ratio

Cash to CurrentLiabilityRatio (Cash/CL) 0.25:1

2. Ratio to Test Capital Structure or Long TermSolvency:

Debt

Debt Bquity Ratio

2 Equity AssetsRatio

0.33:1

0.75:1

0.25:1

Liabilities Assets Ratio

Interest CoverageRatio

5 FixedAssets &Equity Ratio

6Capital Gearing Ratio 0.5:1

3. Ratio to Test Profitability:

20%-30%

Gross ProfitRatio

2 Net Profit Before Tax Ratio

3 Net ProfitAfterTaxRatio

Return on CapitalEmployed

Return before interest & Tax on Capital Employed

(10%-15%)

(5%-10%)

| (10%-15%6

(15%-20%)

|6 OperatingProf+it Ratio (OP/S)

Formula of Calculating Ratio:

SI. NameofRatio Formula of Ratio

Current Assets

CurrentLiabilities

Liquid Assets

Current ratio

22 Quick ratio

Current Liabilities

4. Chapter: Six

Financial Statement Analysis 6/25

3 Stock/Inventory Turnover ratio Cost of Goods Sold

Average Stock

GrossProfit

Net Sales

Net Profitafter Tax 10

Capital Employed

Net Credit Sales

4 Gross profit ratio

x 100

5 Return on capital employed )x 10

Accounts receivable turnover ratio

Average Receivable

Net Profit

Net profit ratio

x 100

Net Sales

External Liabilities

Debt equity ratio

Owner's Equity

Credit Purchase

9 Accounts payable turnover ratio

Average Payable

Sales

10 Capital turnover ratio

Capital Employed

Net Profit after Tax

11 Net profit ratio

x 100

Net Sales

Net Profit after Tax + Interest

Capital Employed

Credit Sales

12 Return on capital employed

x 100

13 Debtors turnover ratio

Average Debtors & B/R

Owner'sEquity

14 Owner's equity ratio

Fictitious Assets

Total Assets_

Owner's Equity

15 Equity-Asset ratio

Total Assets

External Liabilities

16 Liability -Assetratio

Total Assets

Necessary computation to calculate ratio:

1. Current Assets =

Cash in hand +Cash at Bank + Accounts Receivable +Bill Receivable +

Accrued Income +Short Term Investment + +Prepaid Expenses

Inventory

2. Current Liabilities =

Bank Overdraft + Accounts payable + Bill Payable +

Due/Outstanding

Expenses+Short Term Loan + Dividend Declared + Income Tax

3. Quick or Liquid Assets =

Current Assets-(Closing Inventory +

Prepaid Expenses)

4. Quick or Liquid Liabilities =

Current Liabilities

5. Working Capital =

Current Assets -

Current Liabilities

6. Internal Liabilities or Equity Fund =

Share Capital + Reserve & Surplus +Dividend declared

+Unclaimed Dividend - Fictitious Assets

7. External Liabilities =

Long Term Liabilities + Current Assets +

(Dividend Declared +

Unclaimed Dividend) - Fictitious Assets.

8. Gross Profit =

Net Sales Cost ofGoods Sold or Sales x %

9. Cost ofGoods Sold =

Sales- Gross profit or

(Opening Stock + Net Purchase + Direct Expenses

- Closing Stock)

10.

Operating Profit =

Gross Profit -

Operating Expenses

1. Net Profit Before Tax =

Gross Profit -

Operating Expenses Interest or, (Operating Profit-

Interest)

5. 6/26

Financial Statement Analysis

- - * * * * * *

Income 1ax or, N

Chapter: Six Intcrest

Operating Expenses

12. Net Profit after Tax -

Gross Profit

13. Capital Employed= Total Asscts (Less Fictitious Assets)

Current Liabilities

Or. Fixed Assets +Current Assets -

Current Liabilities

Or,Fixed Assets

Or. Share Capital + Reserve & Surphus + Long Term Debt -

Fictitious Asset

Or. Equity Fund + Long Term Liability

Profit Before Tax Inconme Tax

Working Capital

Check list for Ratio:

Measure of:

Broad Basic Computation

Ratios

Category

Liquidityand CashRatio

Eficiency

Adequacy of available

cash

Short-term debt paying

Cash plus cash equivalents

Current liabilities

Current assets

Current Ratio

ability

Immediate short-term

debtpaying ability

Eficiency

Current Liabilities

Quick assets

Quick Ratio

Current liabilities

Net sales of

Accounts

collection

Receivable Average accounts receivable

Turnover

Days

Uncollected

Days in year Liquidity of

Sales

receivables

Receivable turnover

Cost ofgoods sold Efficiency OT

Inventory Turnover

inventory

Average

inventory

Days in year Liquidity of inventory

Days

Inventory

Sales In

Inventoryturnover

Net sales Eficiency of assets in

generating revenues

Total Assets

Average Total assets

Total liabilities

Turnover

Debt financing (by

creditor) i.e. leverage

Equity financing (by

Solvency Debt Ratio*

Total Assets

Total equityy

Equity Ratio*

owner)

Total assets

Book value ofpledged assets Protection to secured

Pledged assets to

secured liabilities creditors

Book valueofsecuredliabilities

Income before interest and Ability to meet interest

payments (From the

viewofprofit)

Times interest

incometaxes

Interest expense

earned

Cash coverage Cash flows from operatingactivities Ability to meet interest

before interestandtaxes

Interest paid

payments (from the

view ofcash flows)

Ability to generate net

Profitability Profit margin ratio Net income

Net sales

Gross margin

income

Gross margin ratio

Net Sales

Net income -

preferred dividends

Ability to generate

gross margin

Overall profitability of

ROE

Average owners equity assets

ROA Net income

Return on Owner's

Average total assets investment

Financial Leverage|=|ROE-ROOA Eficiency of financial

6. Chapter: Six

Financial Statement Analvsis 6/27

percentage

leverage

Farnings per share Net income Preferred dividends Net ncome on each

Average no. of shares outstanding equity or common

ahares

Rook value per Owners' equity appicable Rook valhue of each

share to commonshares

No. of common shares outstanding

Cash flows from operating

equity share

Quality of income The of

extent

activities company's

by

earnings

Net income generated its

operation

Fixed assets Net sales Revenue generating

turnover

Average net fixed assets capacity by fixed

assets

Market Price canings rati0 Market price per common share Market value relative

to earninggs

EPS

Annual dividends per share

Dividend yicld ratio Cash return to each

common share

Market pricepershare

Sometimes, analyst use debt-equity ratio instead ofcalculating debt and equity ratio separately

The computation is as follows:

Debt-cquity ratio = Total debts/ Total equity capital

6.08 Summary of ratio's

| Profitability Formula

Gross profit

Sales

Gross profit: Revenue

Netprofit aftertax

Sales

Net profit after tax: Revenue

Profit beforeinterestandtax

Total assets-Current liabilities

Return on capital employed

Profit beforetax

Share capital + Reserves

Net profitaftertax

Non-current assets + Working capital

Return on share capital

Net profit after tax: Total assets

Solvency and efficiency ratio

Current ratio

Formula

Current assets

Current liabilities

Current assets-Inventory

Current liabilities

Acid test ratio

Revenue

Total assets-Current liabilities

Asset turnover

7. Chapter: Six Financial Statement Analysis

6/28

- - - -

lnventory turnover -**.

Cost of goodssold

Average inventory

Accounts receivable

Revenue

Accounts receivable days

365

Accounts payable days Accounts payabiex 365

Purchases

Shareholder ratios

Dividend yield

| Formula

Gross dividend pershare

Market price per share

Net profitaftertax-Dividend of prefshare

-

Earnings per share noof ordinary shares

Market price

Earnings per share

Price/earnings ratio

Capital structure Formula

Shareholder's funds

Total assets

Net worth: Total assets

Fixed assets

Shareholder's funds

Non-current assets: Networth

Non-current assets: Net worth + Fixed assets

Shareholder's funds +Long-term liabilities

Total liabilities

Total assets

long-term liabilities

Debt ratio

Prior chargecapital

Total capital

Prior chargecapital

Ordinary share capital and reserves

Total borrowing

Shareholder's funds

Capital gearing ratio

Debt: Equityratio

Borrowing: Net worth

Profit beforeinterestandtax

Interest charges

Interest cover

6.09 SuperTipsofthisChapter

Important Information to Answer the Creative Question:

1. Determinationtheamountof CurrentAssets:

Current Asset All assets under the heading of 'current assets' and loan and advance

expenses'in the assetsideofstatementoffinancial position.

Example

SI Taka

Particulars

Cash inhand

Bank balance/deposit

Stockgoods

Notes receivables

Accounts receivable

Shorttermloan

***

**

***

***

4

8. 6/29

Chapter: Six Pinancial Statement Analysis

- - - -

7 AdvanceExpense

Income reccivable/outstanding incomc

Total current assets

2. Determinationof Current Liability:

Current Liability = All liabilities under the head of 'current liabilities and other

provisions intheliabilitysideofstatementoffinancial position.

Example:

SIParticulars

Accounts payable

Notes payable

Bank overdraft

Shortterm loan

Outstanding expenses

Advance Income/Unearned revenue

Proposed dividend

Provision for incometax

Jnclaimed dividend

Taka

***

***

***

***

***

***

Total currentliabilities

*****

3. DeterminationofLiquid Asset:

Total LiquidAsset =

TotalCurrent Asset -ClosingStock-AdvanceExpenses

Example:

Particulars

|Total CurentAsset

(-)Closing Stock

() Advance Expenses

Total AmountofLiquid Asset

Taka

**

***

***

4. DeterminationofOwner'sEquity/Fund:

Owner's Equity = Share Capital + Reserve and Surplus - Expense not written off

(unadjusted

5. DeterminationofExternalLiability:

External Liability CurrentLiabilitiesandotherProvisions +Longterm Loans.

Example:

Particulars

Current Liabilities

(+) 10% Loan

20% Mortgage Loan etc.

External Liability

Taka

***

***

****

**

6. Determinationof TotalAssets:

Total Asset = Total of Asset side of Statement of Financial Position - Expenses not|

written offi(unadjusted

Example:

Particulars

Total Assets

Preliminary Expense

Taka

**

***

9. Chapter: Six

Financial Statement Analysis

Differed Advertisement

Underwriter's commission

Premium ofshare / dcbentur: ctc._

Amount of TotalAsset

***

***

7. Determinationof GrossProfit/Profit:

Gross Profit =

NetSales -

Cost ofGoodsSold

or, Gross Profit Sales x Percentage of Gross Profit (If the percentage/rate of profiton

sales is given)

or, Gross profit =

Cost of Goods Sold x Rate of Gross Profit (If rate of Gross Profit on

cost ofgoodssoldisgiven)

8. DeterminationofNetProfit:

Net Profit Gross Profit -

Operating Expense + Non-Operating

lncome- Non

Operating Expense

Example:

Particulars

Gross Profit

Taka

***

Operating Expenses ***

***

(+) Non-operatingIncome ***

***

( Non-operatingExpenses

AmountofNetProfit

9. Determinationof CostofGoodsSold:

Cost ofGoodsSold=NetSales-GrossProfit

Or, CostofGoodsSold =

OpeningStock+CostofPurchasedGoods-ClosingStock

Example:

Particulars

Net Sales

Taka

***

***

() Gross Profit

Cost ofGoodsSold

***

Or,

Particulars

Opening Stock

(+) NetPurchase

+) Wages

(+) CarryingCosts etc.

Closing Stock

Cost ofGoodsSold

Taka|

***

***

*** |

***

***)

***

10.DeterminationofInvested Capital:

Invested Capital =

Equity Fund + Long Term Loan

Or, Invested Capital =

Total Asset-Current Liability

Example:

Particulars

Equity Fund

(+) Long term Loan

Amount ofInvestedCapital

Taka

**

***

10. Chapter: Six

Financial Statement Analysis 6/31

- a - - - ~

Or,

Particulars

Net Asscts (Total Asset -

Expense not written off)

(-)CurrentLiability

Cost ofGoodsSold

Taka

**

11. Determinationof AverageStock:

Average Stock =PenngStock +ClosingStock

Example:

Value of opening stock Tk. 52,000 and Closing Stock TK. 44,000.

52000+44000

Average Stock =

Tk. 48,00o

12. Determinationof Working / Current Capital:

Working/ CurrentCapital =

CurrentAsset-CurrentLiability

Example:

Particulars Taka

Total Current Asset ***

(Total CurrentLiability

Amount ofworkingcapital:

13.Determination of FixedCost Fund:

Fixed Cost Fund =

PreferredShare Capital+Long Term Loan

***

Example:

Particulars

Preferred Share Capital

(+) 10% Debenture

Amount ofFixed CostFund:

Taka

***

***

14.DeterminationofNetProfitbeforeTaxandInterest:

Net Profit before Tax and Interest= Net Profit afterDeducting Tax + Interest Expense

(Interest ofLoan)+IncomeTaxExpense

Example:

Particulars

Net Profit after Deducting Tax

(+) 10% Debenture

(+) Income Tax Expense

Amountof NetProfitbeforeTaxandInterest:

Taka |

***

***