Social Media: Building Your Brand Audience

•

5 gefällt mir•1,069 views

This document summarizes findings from a survey of 1,000 connected consumers conducted by Razorfish in 2009. Some key findings include: - 65% of consumers report that a digital experience with a brand changed their opinion of that brand, and 97% say such an experience influenced a purchase. - Consumers are actively engaging with brands online through searching for brands, watching commercials on YouTube, reading corporate blogs, and posting reviews. - Contrary to conventional wisdom, consumers are open to brand advertising and engagement on social networks - 76% welcome ads on social networks, and 40% have friended a brand on Facebook or MySpace. - While consumers follow brands online, they may not be as passionate

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (19)

Ähnlich wie Social Media: Building Your Brand Audience

Ähnlich wie Social Media: Building Your Brand Audience (20)

Mehr von The Advertising Research Foundation

Mehr von The Advertising Research Foundation (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Social Media: Building Your Brand Audience

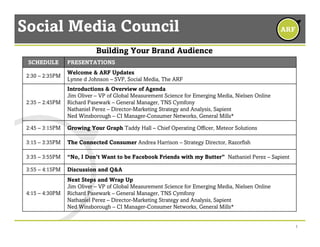

- 1. 1 Social Media Council Building Your Brand Audience Next Steps and Wrap Up Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills* 4:15 – 4:30PM Discussion and Q&A3:55 – 4:15PM “No, I Don’t Want to be Facebook Friends with my Butter” Nathaniel Perez – Sapient3:35 – 3:55PM The Connected Consumer Andrea Harrison – Strategy Director, Razorfish3:15 – 3:35PM Growing Your Graph Taddy Hall – Chief Operating Officer, Meteor Solutions2:45 – 3:15PM Introductions & Overview of Agenda Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills* 2:35 – 2:45PM Welcome & ARF Updates Lynne d Johnson – SVP, Social Media, The ARF 2:30 – 2:35PM PRESENTATIONSSCHEDULE

- 2. THURSDAY JANUARY 28, 2010 Bently Reserve, San Francisco Join us at our upcoming San Francisco event to learn how to use listening, evaluate listening applications, develop a listening strategy, integrate it into your existing research program, create an action plan and apply its learnings. Get answers to your questions on listening and develop an action plan that specifically addresses your business needs during this interactive day. Speakers include: » Jeremiah Owyang, digital media strategy superstar and blogger and Partner, Customer Strategy, Altimeter Group » Steve Patrizi, Vice President, Advertising Sales and Operations, LinkedIn » Doug Frisbie, National Social Media and Product Integration Manager, Toyota » Johanna Skilling, EVP, Director of Strategic Planning, Saatchi and Saatchi Wellness Putting Listening to Work 2010 ARF Industry Leader Forum TO FIND OUT MORE AND REGISTER www.TheARF.org/assets/ilf Upcoming ARF Events

- 3. Upcoming ARF Events Re:think 2010: The ARF Annual Convention + Expo MARCH 22-24, 2010 Marriott Marquis, New York City www.TheARF.org/assets/rethink-10 The ARF 2010 David Ogilvy Awards MARCH 23, 2010 Marriott Marquis, New York City Enter today! Submission deadline Ext January 11, 2010. www.TheARF.org/assets/ogilvy-10 The ARF 2010 Great Mind Awards MARCH 24, 2010 Marriott Marquis, New York City Nominate a colleague for a Great Mind Award today. www.TheARF.org/assets/great-mind-10

- 4. 4 Welcome & ARF Overview Lynne d Johnson SVP, Social Media The ARF

- 5. Discover valuable Knowledge Solutions Online and Off 5 PowerSearch A single search allows you to access nearly 60,000 documents, including: • ARF website • ARF conference papers, workshop papers, white papers, case studies, Ogilvy awards • Journal of Advertising Research • WARC database abstracts • Research and summaries of new and historical studies from 50 other sources: ARF member research companies, industry associations, and trusted non-member companies Morning Coffee Morning Coffee brings the web’s best news feeds, research, blogs and videos on advertising, marketing, media, consumers and culture to our members.

- 6. Social Media Council 6 Social media is becoming a critical part of progressive marketing thinking. With the rise of social media, the consumer has been able to drive the conversation with or without input from the brands. • Help companies understand how they can be the chief storytellers for their own brands within the midst of all of the noise and conversations. • Create appropriate metrics that can gauge the impact of marketing efforts in social media. • Develop a plan for research/insights to bring the voice of the human into the boardroom by “listening” to what is said in social media as part of a cohesive research program. • Have the ARF leverage social media with its membership and the marketing/media community to develop and demonstrate successful social media marketing principles. The Council will:

- 7. Social Media Council Co-Chairs 7 Jim Oliver VP of Global Measurement Science for Emerging Media, Nielsen Richard Pasewark General Manager, TNS Cymfony Nathaniel Perez Head of Community Intelligence, Sapient Interactive Ned Winsborough CI Manager, Consumer Networks, General Mills

- 8. 8 Building Your Brand Audience Next Steps and Wrap Up Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 4:15 – 4:30PM Discussion and Q&A3:55 – 4:15PM “No, I Don’t Want to be Facebook Friends with my Butter” Nathaniel Perez – Sapient3:35 – 3:55PM The Connected Consumer Andrea Harrison – Strategy Director, Razorfish3:15 – 3:35PM Growing Your Graph Taddy Hall – Chief Operating Officer, Meteor Solutions2:45 – 3:15PM Introductions & Overview of Agenda Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 2:35 – 2:45PM Welcome & ARF Updates Lynne d Johnson – SVP, Social Media, The ARF 2:30 – 2:35PM PRESENTATIONSSCHEDULE Social Media Council

- 10. Online Marketing Is Changing… 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 10 Build Site and Create ContentBuy Ads Tracking and Optimization Tracking and Optimization

- 11. Today It Has to Be Earned Paid Media (Ads) Owned Media Earned Media

- 12. A Big Opportunity 12/14/2009 www.meteorsolutions.com 12 Lots of Traffic •15-20% of Unique Visitors from “Earned” Links (source: Meteor Solutions) Valuable Visitors •1.5x – 4x Conversion Lift •Loyal Fans (source: Meteor Solutions, Razorfish) + ROI •Low Acquisition Costs •Engaged and Loyal Customers =

- 13. How to Monetize the Social Graph 4 Steps to Success: 1.Research – Listen and Map the DNA of Link Sharing and Influence 2.Connect with Fans and Advocates – Distribute Content and Energize the Base 3.Activate and Monetize – Increase Sharing, Engagement, and Action 4.Optimize – Improve Paid and Unpaid Activities 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 13

- 14. Lots of Help Figuring this Out 12/14/2009 www.meteorsolutions.com 14

- 15. Step 1: Research 12/14/2009 www.meteorsolutions.com 15

- 16. Revealing the Graph: The DNA of Social Media James Follows link to Palm.com and sees video James Shares Link to video Friends and Family Follow Link Friends Visit Landing Page to See Video & Offer Some buy and some pass it on… Assign unique IDs to each friend that clicks. Javascript on client assigns unique ID to James and the URL he shares Associate James with each visitor and identify sources of each (eg. Facebook) Track conversions and downstream word of mouth Buy!

- 17. Sharing PLUS Listening 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 17 Listening and Sentiment •Identify conversations and communities that drive most direct and indirect traffic and actions. •Track influencers and the earned media they generate. Third Party Listening Platform

- 18. Step 2: Connect with Fans and Advocates 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 18 Serious Fan Advocates Passionate about your brand, eager to share with others. Committed to the cause, eager to make a difference.

- 19. Create, Distribute…. and Energize 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 19

- 20. Syndicate and Publicize Relevant Content (even when it isn’t yours!) On Twitter – Post Links to Quality Fan Content – Follow Quality Followers – Re-Tweet Relevant Messages On Facebook – Friend Your Biggest Fans – Post Relevant Content and Links On Bookmarking Sites – Link to Quality Fan Content Through Delicious, Digg, etc. 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 20

- 21. How to Engage Your Fans and Advocates 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 21 •Recognition • Public Acknowledgement, Counters, Stars, Achievements •Rewards • Access, Special Content, Status •Sharing • Facebook Connect • Twitter API • Email • Sharing Widgets •Fun • Increasing Influence = More Recognition and “Richer” Rewards

- 22. The Multiplier Effect 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 22 100s 1,000,000s10,000s

- 23. Step 3: Activate and Monetize 12/14/2009 www.meteorsolutions.com 23 BUILDING BLOCKS OF SOCIAL PROMOTIONBUILDING BLOCKS OF SOCIAL PROMOTION LeaderboardsLeaderboardsSharing MapsSharing Maps Content Unlock Content Unlock Reward System Integration Reward System Integration Stimulate sharing to increase traffic: 20%-50% from sharing

- 24. 12/14/2009 Proprietary and Confidential. Patents Pending.

- 26. 12/14/2009 Proprietary and Confidential. Patents Pending. Share video with friends… and community earns right to watch the next video

- 27. Step 4: Optimize • Target influential sites/communities with immediate “call to action” • Increase paid media and seeding efforts on highest ROI placements 12/14/2009 www.meteorsolutions.com 27

- 28. Increase Advertising ROI on High Yield Sites

- 29. Take-Aways It’s not Magic…but it is different Social Media scales…and delivers Getting Started: Get to know your Social Graph: Track and Listen Engage and Activate Learn and Optimize 12/14/2009 CONFIDENTIAL www.meteorsolutions.com 29

- 30. Thank You! Questions? Give a Shout! Taddy Hall, COO Taddy@meteorsolutions.com c 917.612.6250 Sales: (866) 677-0604 12/14/2009 www.meteorsolutions.com 30

- 31. 31 Building Your Brand Audience Next Steps and Wrap Up Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 4:15 – 4:30PM Discussion and Q&A3:55 – 4:15PM “No, I Don’t Want to be Facebook Friends with my Butter” Nathaniel Perez – Sapient3:35 – 3:55PM The Connected Consumer Andrea Harrison – Strategy Director, Razorfish3:15 – 3:35PM Growing Your Graph Taddy Hall – Chief Operating Officer, Meteor Solutions2:45 – 3:15PM Introductions & Overview of Agenda Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 2:35 – 2:45PM Welcome & ARF Updates Lynne d Johnson – SVP, Social Media, The ARF 2:30 – 2:35PM PRESENTATIONSSCHEDULE Social Media Council

- 32. FEED: The 2009 Razorfish Digital Brand Experience Report Garrick Schmitt, Group Vice President, Experience Planning Email: garrick.schmitt@razorfish.com Twitter: @gschmitt

- 33. Conventional Wisdom Says Advertising Is Failing... 2

- 34. Page 3 © 2009 Razorfish. All rights reserved. 76% of people think companies lie in ads 77% trust companies less than they did last year 38% of people believe companies will do what is right 15% of people enjoy the ads as much as the programs 2008 Vizu Answers, 2009 Yankelovich, 2009 Edelman Trust Barometer, 2009 Edelman Trust Barometer, TGI, HT Spike Jones, Brains On Fire.

- 35. Worse? 83% Of Mad Men’s Time-Shifted Audience Fast Forwards Through The Commercials TIVO, September 25th, 2009

- 36. But It’s Not That Advertising Is Failing…It’s That Experiences Matter More Than Ever Before. 5

- 37. 6 HELLO

- 38. How Do Consumers Engage With Brands In An Increasingly Digital World?

- 39. 8 THE DETAILS

- 40. Meet The “Connected Consumer” In August 2009 Razorfish surveyed 1,000 U.S. “connected consumers”*: • Broadband access • Spent $150 online in the past six months (travel, Netflix, tickets, Amazon, etc.) • Visited a community site (MySpace, YouTube, Facebook, Yelp, etc.) • Consumed or created some form of digital media such as photos, videos, music or news WHAT IS YOUR AGE? WHICH OF THE FOLLOWING BEST DESCRIBES YOUR COMBINED HOUSEHOLD INCOME? 9 * This equates roughly to the U.S. broadband population which is about 200m based on the Pew Internet and American Life Project.

- 41. READ THIS

- 42. Yes, You Can Build A Brand Online. You Have No Choice Marketers have never thought of digital as a wonderful place to build a brand, but they should: • 65% of consumers have had a digital experience change their opinion about a brand • 97% of them report that experience influencing whether or not they purchased a product or service from that brand HAS AN EXPERIENCE YOU HAVE HAD ONLINE EVER CHANGED YOUR OPINION (EITHER POSITIVELY OR NEGATIVELY) ABOUT A BRAND OR THE PRODUCTS AND SERVICES IT OFFERS? HAS THAT EXPERIENCE INFLUENCED WHETHER OR NOT YOU PURCHASED A PRODUCT OR SERVICE FROM THE BRAND? 11

- 43. Actions Speak Louder Than Advertising Branded experience are the new advertising. And consumers are increasingly hungry for them, sometimes ravenously so: • 97% have searched for a brand online • 77% have watched a commercial on YouTube • 69% have read a corporate blog • 65% have played a branded, browser-based game. • 73% have posted a product or brand review on a site like Amazon, Facebook or Twitter PLEASE RATE THE FREQUENCY OF WHICH YOU DO THE FOLLOWING: 12

- 44. Brand Culture Or Fan Culture? Conventional wisdom holds that consumers don’t want brands encroaching on their social lives – but that’s just not true: • 76% of consumers welcomed brand advertising on social networks (FEED, 2008) • 40% of consumers “friended” a brand on Facebook and/or MySpace • 26% of consumers have “followed” a brand on Twitter HAVE YOU EVER “FRIENDED” A BRAND ON FACEBOOK OR MYSPACE? HAVE YOU EVER FOLLOWED A BRAND ON TWITTER? 13

- 45. The Outlet Malls Of Tomorrow? Facebook, MySpace & Twitter Marketers shouldn’t assume that consumers are as passionate about their brands as they are: Consumers don’t want a conversation with brands – they want deals. 14 • 44% of consumers who follow a brand on Twitter do so for deals • 37% of consumers who “friended” a brand on Facebook and/or MySpace do so for deals WHAT IS THE PRIMARY REASON YOU FOLLOW A BRAND ON TWITTER?

- 46. Bottom Line: Digital Brand Experiences Create Customers Digital is not simply an “awareness” or CRM play, it’s a customer-creation play. The overwhelming majority of consumers who engage with a brand online move from passive “receivers” to advocates almost instantly : 15 • 97% report increased brand awareness • 98% show increased consideration • 97% will more likely purchase a product • 96% may recommend the brand to their friends WHEN YOU HAVE PARTICIPATED IN A BRAND-SPONSORED CONTEST OR SWEEPSTAKES, DOES IT GENERALLY DO THE FOLLOWING:

- 48. Consumers Turning First, Foremost To Digital According to Forrester consumers now spend nearly as much time online as they do watching TV*. We found that their technical fluency is far greater than most believe: • 57% of consumers actively customize their homepages • 84% share links or bookmarks • 55% subscribe to RSS feeds • 33% get their news from Facebook • 20% get their news from Twitter PLEASE RATE THE FREQUENCY OF WHICH YOU DO THE FOLLOWING: 17 *Forrester 2009 North American Technographics Survey

- 49. Mobile Internet Service Use Skyrocketing Mobile Internet services are being consumed broadly. Majority of consumers own a smartphone and use it actively. 18 • 57% access the Internet from their phone • 50% have downloaded an app for their phone • 30% have interacted with an ad banner on their phone WHAT TYPE OF SMARTPHONE DO YOU HAVE?

- 50. Connected Consumers Are The New Mainstream 19 THE TECHNOLOGY ADOPTION CURVE

- 51. 20 BRAND CULTURE

- 52. Are Consumers Really In Control? Conventional wisdom says that every generation of consumer grows smarter, shrewder and more immune to marketing. But that’s not true – consumers are actively choosing to engage with brands, everywhere. • 40% have “friended” a brand on Facebook and/or MySpace • 26% have “followed” a brand on Twitter • 77% have watch an advert on YouTube • 69% have read a corporate blog post • 73% have posted a review of a brand on a site like Amazon or Yelp • 52% have blogged about brand’s product or service PLEASE RATE THE FREQUENCY OF WHICH YOU DO THE FOLLOWING: 21

- 53. Facebook And Twitter Creating Fan Culture For Brands After deals, the main reason consumers “friend” a brand? Because they *really* are a fan (or a customer, at least). Social media platforms are proving to be customer service platforms. • 33% friend a brand on Facebook/ MySpace because they are a customer • 24% follow a brand on Twitter because they are a current customer • 23% follow a brand on Twitter for “interesting or engaging” content, which shows promise for a new type of relationship WHEN YOU “FRIEND” A BRAND ON FACEBOOK OR MYSPACE, DOES IT GENERALLY DO THE FOLLOWING? WHEN YOU FOLLOW A BRAND ON TWITTER, DOES IT GENERALLY DO THE FOLLOWING? 22

- 54. Fans And The Future Of The Marketing Funnel Brand culture and fan culture are dramatically reshaping the traditional funnel as consumers leap from experience to advocacy (or the inverse) almost instantly. • 70% have participated in a brand- sponsored contest • 24% have produced content to participate in a contest • 26% have attended a brand sponsored event, such as Nike’s Human Race • 24% have downloaded a branded application for their mobile phone HAVE YOU EVER PARTICIPATED IN A BRAND-SPONSORED CONTEST OR SWEEPSTAKES? WHEN YOU HAVE PARTICIPATED IN A BRAND-SPONSORED CONTEST OR SWEEPSTAKES, DOES IT GENERALLY DO THE FOLLOWING? 23

- 55. Experiences Not Only Build Brands, They Make Or Break Them Amazon, Google, Facebook, Apple and Nike are all experiential brands that know consumer preference isn’t formed in reaction to a message, but to a series of experiences over time. There’s good reason. Of consumers who interact: • 97% report increased brand awareness • 98% show increased consideration • 97% will more likely purchase a product • 96% may recommend the brand to their friends 24

- 57. Getting To The Bottom Of Brand Engagement Everyone is chasing after a metric to define brand engagement. Millward Brown says “digital consumers” have 15% stronger relationships with brands. The Altimeter Group attempts to correlate social media activity to financial performance, citing Dell, Starbucks and eBay as leaders. We at Razorfish took a different tack: we simply wanted to know if there was any direct correlation between a consumer’s digital interaction with a brand and their likelihood to purchase a specific product or service. 26

- 58. Digital Experience Create Customers The answer was a resounding “yes”. Experiences have a much greater influence over brand affinity and consumer purchasing than even we anticipated: • 65% of consumers have had a digital experience change their opinion about a brand. • 97% of those report that experience influencing whether or not they purchased a product or service from that brand. • 64% of consumer report making a first purchase from a brand because of digital experience (e.g. website, banner, etc.) HAS AN EXPERIENCE YOU HAVE HAD ONLINE EVER CHANGED YOUR OPINION (EITHER POSITIVELY OR NEGATIVELY) ABOUT A BRAND OR THE PRODUCTS AND SERVICES IT OFFERS 27 HAS THAT EXPERIENCE INFLUENCED WHETHER OR NOT YOU PURCHASED A PRODUCT OR SERVICE FROM THE BRAND? HAVE YOU EVER MADE YOUR FIRST PURCHASE FROM A BRAND BECAUSE OF A DIGITAL EXPERIENCE (E.G., A WEB SITE, MICROSITE, MOBILE COUPON, EMAIL)?

- 59. Five Brands That Are Excelling In An Experience- Driven World…

- 60. 1. UNIQLO: Japanese Retailer Surprises And Delights Audiences With Every Interaction 29

- 61. 30 2. Red Bull: Pioneered Experiential Marketing With Subversive Events And Sponsorships

- 62. 31 3. Barbie: Reinvented An American Icon For The Pop Sugar Set And Broke Sales Records

- 63. 32 4. Nike: Human Race. Chalkbot. Nike Is Setting A New Standard For Experiential Marketing

- 64. 33 4. Virgin America: Brand Built By Breakthrough Experiences – And The Marketing Of Them

- 65. 34 34 5. Microsoft’s Bing: Accomplishing The Impossible By Putting Experience First And In Every Ad

- 66. Thank You Garrick Schmitt, Group Vice President, Experience Planning Email: garrick.schmitt@razorfish.com Twitter: @gschmitt

- 67. 32 Building Your Brand Audience Next Steps and Wrap Up Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 4:15 – 4:30PM Discussion and Q&A3:55 – 4:15PM “No, I Don’t Want to be Facebook Friends with my Butter” Nathaniel Perez – Sapient3:35 – 3:55PM The Connected Consumer Andrea Harrison – Strategy Director, Razorfish3:15 – 3:35PM Growing Your Graph Taddy Hall – Chief Operating Officer, Meteor Solutions2:45 – 3:15PM Introductions & Overview of Agenda Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 2:35 – 2:45PM Welcome & ARF Updates Lynne d Johnson – SVP, Social Media, The ARF 2:30 – 2:35PM PRESENTATIONSSCHEDULE Social Media Council

- 68. “No, I don’t want to be friends with my butter!” Re-setting the agenda for Social Media

- 69. Brand Friendships Changing Landscape Information Universe Building Better Social Experiences Case Study

- 70. Meet the most easily performed Facebook action.

- 71. Yet only 11% have “friended” a brand on Facebook.

- 72. And 41% of 18-24 say they don’t want to see profiles from brands on social networking sites.

- 73. Fan counts are misleading. 4 months 951 “likes” (0.02%) 318 comments (0.009%)

- 74. Engagement is dramatically growing. 138,000+ comments (1.7%) 71MM monthly active users

- 75. THINGS ARE CHANGING (US).

- 76. The World According to Google (or Eric Schmidt anyway...) •Five years from now the internet will be dominated by Chinese language content. •Today’s teenagers model how the web will work infive years – jumping from app to app to app seamlessly. •Five years is a factor of about 6 according to Moore’s Law, meaning that devices will be capable of far more by that time than they are today. •Within five years there will be broadband well above 100MB in performance – and distribution distinctions between TV, radio and the web will go away.

- 77. Media has fueled fundamental cultural shifts in what we find normal or acceptable about privacy.

- 78. Complete decentralization of social networks.

- 79. Real time information in search results on Google. Real time information in Google search results.

- 80. Expect Google’s Social Search to change the way we interact with search engines. Google’s Social Search to change the way we interact with search engines (and information).

- 81. Experiential conversation: fundamental shifts in the way we engage with each other. Experiential conversation: fundamental shifts in the way we engage with each other.

- 82. Media and consumer voice with few physical boundaries.

- 83. Content organization and filtering is becoming big business.

- 84. An information universe growing by the second. 724,311,510,618,248,992,017 Bytes of information created since 01.01.2009 – IDC OR 674,567,661,000+ GB OR 84B Full 8GB iPhones 23,952,000,000,000 Bytes of information created every second (roughly) IDC Digital Information Universe Study - 2009

- 85. An immense and ever-increasing wealth of knowledge is scattered about the world today; knowledge that would probably suffice to solve all the mighty difficulties of our age, but it is dispersed and unorganized. We need a sort of mental clearing house for the mind: a depot where knowledge and ideas are received, sorted, summarized, digested, clarified and compared.” H. G. Wells, 1938, The Brain: Organization of the Modern World “ An old problem with brand new proportions.

- 86. “Media defines us while we define media.” “We’ve shifted from media to mediated relationships.” “Connections were the constraint, we now have connections without constraints.” “The machine is (Changing) Us: YouTube and the politics of Authenticity”- Michael Wesch, Assistant Professor of Cultural Anthropology, Kansas State University. Breaking through the clutter. Three grounding principles

- 87. Shape the outcome, don’t prescribe it. Leave predictable outcomes behind. Turn insights into motives Relinquish control Brand/Consumer Research Online Anthropology Motives/Behavior Experience Media Engagement Connection DistributionCreation Community Earned Media Voice ConsumerBrand Control Media defines us while we define media.

- 88. Connectivity carries communication Brands should connect, not broadcast Move beyond static listening metrics (influence, motives) Understand influence and motives “in action” Social Media an unbound source of behavioral insights Create virtual focus groups Build connectivity through behavioral contexts you can associate with Create “mediated” experiences We’ve shifted from media to mediated relationships. Brand Consumers

- 89. Listen to your experiences Digital listening lets you understand how media has shaped you Perform discovery against your own conversation Behavior, influencers, motives, connectivity. Convergence of listening and analytics Cross-channel, cross-metrics analysis Source correlations (sales, CRM, web analytics, call-center, buzz) Advanced techniques (language, stochastic, etc.) Connections were the constraint, we now have connections without constraints.

- 90. Putting it all together. Queensland’s “Best Job in The World”

- 101. CreationCreation

- 103. CommunityCommunity

- 108. Why It Worked Bloggers in a hard economy, where a job could have a whole new meaning. Younger tech savvy, creative minded. Did not target travelers, but targeted advocates. Engagement motive: A reward that gets them to dream, creating an individual expression that promotes the brand. Experience motive: Self-expression, competition, prize, fame Influence “in action”: A travel story told by aspiring caretakers that spread the word to their circles. Shaping the outcome: one winner, public control, media shapes the brand Mediated experience: Queensland connected, without ever broadcasting. Leveraged the voice of the people and media. Listening: Clear opportunity to measure impact across metrics (from mere sentiment to visitors, tourism revenue, etc.)

- 109. THANK YOU! ANY QUESTIONS? Nathaniel Perez Director – Community Intelligence Twitter: @mahumbaba LinkedIn: http://www.linkedin.com/in/nathanielperez Email:nperez@sapient.com

- 110. 75 Building Your Brand Audience Next Steps and Wrap Up Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 4:15 – 4:30PM Discussion and Q&A3:55 – 4:15PM “No, I Don’t Want to be Facebook Friends with my Butter” Nathaniel Perez – Sapient3:35 – 3:55PM The Connected Consumer Andrea Harrison – Strategy Director, Razorfish3:15 – 3:35PM Growing Your Graph Taddy Hall – Chief Operating Officer, Meteor Solutions2:45 – 3:15PM Introductions & Overview of Agenda Jim Oliver – VP of Global Measurement Science for Emerging Media, Nielsen Online Richard Pasewark – General Manager, TNS Cymfony* Nathaniel Perez – Director-Marketing Strategy and Analysis, Sapient Ned Winsborough – CI Manager-Consumer Networks, General Mills 2:35 – 2:45PM Welcome & ARF Updates Lynne d Johnson – SVP, Social Media, The ARF 2:30 – 2:35PM PRESENTATIONSSCHEDULE Social Media Council

- 111. 76 Upcoming ARF Events Putting Listening to Work 2010 ARF Industry Leader Forum THURSDAY JANUARY 28, 2010 Bently Reserve, San Francisco Join us at our upcoming San Francisco event to learn how to use listening. Get answers to your questions on listening and develop an action plan that specifically addresses your business needs during this interactive day. Speakers include: » Jeremiah Owyang, Altimeter Group » Steve Patrizi, LinkedIn » Doug Frisbie, Toyota » Vishal Pandya, IBM » Johanna Skilling, Saatchi and Saatchi Wellness » Stephen Kim, Microsoft Advertising TO FIND OUT MORE AND REGISTER www.TheARF.org/assets/ilf

- 112. Next Social Media Council 77 TUESDAY FEBRUARY 2, 2010 ARF, New York TO FIND OUT MORE AND REGISTER www.TheARF.org/assets/social-media-council

- 113. Ogilvy Awards Submissions Deadline Extended January 11th – ogilvyawards@thearf.org Ad Effectiveness / January 21st All council schedules are in EDT format and in our ARF offices in NY unless otherwise noted. To register please visit http://www.thearf.org/channels/councils or email councils@thearf.org Upcoming Council Meetings and Announcements