1. InvestmentThesis

Company Overview

- RPXC cannot function unless it has control of a huge number of patents. The

company has acquired these patents through cash flow from operations since

2009, and shows no signs having to alter this pattern. With a Base Case of

cash flows from operations as 65% of revenues, RPXC can fund its acquisi-

tions and has positive growth cash balances through 2019—implying the com-

pany will be able to fund its core competency without raising capital in the near

future.

- Until September 30, 2014, RPX has spent a combined $890 Million to ac-

quire over 4900 patents. A deal with Rockstar was finalized in February 2015

and RPXC effectively doubled its patent assets—worth $1.8B. So long as RPX

increases the number of patents they own, they can increase the number of

companies they attract to subscribe to their services, which gives investors

what they seek: growth.

-Over 96% of RPXC’s revenues are subscription based, and over 90% of

those revenues are renewed each year. These two things allow management

to focus energy on growth through patent acquisitions, and also leads to ex-

tremely high cash flow from operations. Because of this the current price to

cash flow multiple is much lower than is justifiable indicating a deep value to

investors.

-The patent market is growing like weeds, annual litigation costs have tripled

since 2008. RPX brings efficiency and a good name to a broken and badly

branded market. Their network effect allows them to generate more than 2x

revenue per dollar of assets than competitors.

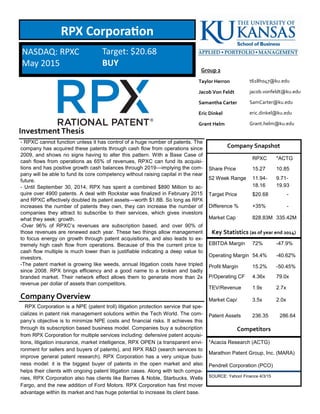

RPX Corporation

Company Snapshot

RPXC *ACTG

Share Price 15.27 10.85

52 Week Range 11.94-

18.16

9.71-

19.93

Target Price $20.68 -

Difference % +35% -

Market Cap 828.83M 335.42M

Key Statistics (as of year end 2014)

EBITDA Margin 72% -47.9%

Operating Margin 54.4% -40.62%

Profit Margin 15.2% -50.45%

P/Operating CF 4.36x 79.0x

TEV/Revenue 1.9x 2.7x

Market Cap/ 3.5x 2.0x

Patent Assets 236.35 286.64

Competitors

*Acacia Research (ACTG)

Marathon Patent Group, Inc. (MARA)

Pendrell Corporation (PCO)

SOURCE: Yahoo! Finance 4/3/15

NASDAQ: RPXC

May 2015

Target: $20.68

BUY

RPX Corporation is a NPE (patent troll) litigation protection service that spe-

cializes in patent risk management solutions within the Tech World. The com-

pany’s objective is to minimize NPE costs and financial risks. It achieves this

through its subscription based business model. Companies buy a subscription

from RPX Corporation for multiple services including: defensive patent acquisi-

tions, litigation insurance, market intelligence, RPX OPEN (a transparent envi-

ronment for sellers and buyers of patents), and RPX R&D (search services to

improve general patent research). RPX Corporation has a very unique busi-

ness model: it is the biggest buyer of patents in the open market and also

helps their clients with ongoing patent litigation cases. Along with tech compa-

nies, RPX Corporation also has clients like Barnes & Noble, Starbucks, Wells

Fargo, and the new addition of Ford Motors. RPX Corporation has first mover

advantage within its market and has huge potential to increase its client base.

t618h047@ku.edu

jacob.vonfeldt@ku.edu

SamCarter@ku.edu

eric.dinkel@ku.edu

Grant.helm@ku.edu

Taylor Herron

Jacob Von Feldt

Samantha Carter

Eric Dinkel

Grant Helm

Group 2

2. Page 2

May 2015 $20.68 BUY Group 2

Competitive Advantage through CAPEX

While RPXC’s business model and revenue growth de-

pends on new subscriptions and renewals, those sub-

scriptions will only keep rolling in if RPXC continues to

acquire new patents to expand its portfolio. More patents

equate to a larger client base, which is key to RPXC’s

subscription growth, stability, and more reoccurring reve-

nue. The industry of tech patent protection has high

growth potential—in 2013 there were approximately 2,500

tech companies sued by patent trolls1

. PPXC has high

probability to grab onto and take control of this market

given that it is the biggest buyer of patents in the open

market, and because the company also helps resolve pa-

tent troll litigation cases. RPXC is a one of a kind business

1 Investor Presentation 2014 3 RPX Corporation Website

2 Email from Boone

model, therefore the only company operating with this sort

of capacity2

. RPXC has first mover advantage in market

that houses over $12.2 billion in NPE litigation costs3

,

which grants a huge competitive advantage and an ex-

tremely wide moat. This moat is sustained because RPXC

holds an enormous amount of data, given the tech nature

of its business, which it uses to meet its clients’ needs—

many of which are big names. These names include Cis-

co, Toshiba, LinkedIn, and many more1

. More than 550

unique companies have been named in patent troll suits

just in Q1 of 2015; 500 of which are not yet clients of

RPXC and half of those experienced their first patent troll

suit. 75 of those 550 companies were sued more than

once, only half of which are current clients of RPXC2

.

In order to attract all of this client potential, RPXC has to

continue to acquire patents. With exception of its first

Base Case: 65% of Revenue

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Cash & Cash Equivilents 28.9 46.7 106.7 73.6 100.2 78.0 132.5 193.2 260.0 334.7 417.2

Cash from Operations 17.6 120.1 120.3 91.4 212.5 191.5 208.4 231.4 254.5 277.4 299.6

CapEx Requirement 38.5 72.1 101.2 87.4 127.1 137.0 147.7 164.5 179.8 194.9 209.5

Bear Case: 35% of Revenue

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Cash & Cash Equivilents 28.9 46.7 106.7 73.6 100.2 78.0 132.5 97.0 57.0 14.3 (31.2)

Cash from Operations 17.6 120.1 120.3 91.4 212.5 191.5 112.2 124.6 137.0 149.4 161.3

CapEx Requirement 38.5 72.1 101.2 87.4 127.1 137.0 147.7 164.5 179.8 194.9 209.5

Bull Case: 90% of Revenue

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Cash & Cash Equivilents 28.9 46.7 106.7 73.6 100.2 78.0 132.5 273.4 429.2 601.7 790.9

Cash from Operations 17.6 120.1 120.3 91.4 212.5 191.5 288.6 320.3 352.4 384.1 414.8

CapEx Requirement 38.5 72.1 101.2 87.4 127.1 137.0 147.7 164.5 179.8 194.9 209.5

year, RPXC has been able to fund its patent acquisitions

from its cash from operations. Historically, cash from oper-

ations as a percent of total revenues has been a fairly sig-

nificant, ranging anywhere from 46-127%, but more con-

sistently around 70% (see table 1). In a Base Case of

65% (table 2) and a Bull Case of 90% (table 4) of reve-

nues, cash from operations will be more than enough to

fund CAPEX needs for a conservatively growing client

base. In both of these cases, through 2019 the cash and

cash equivalent balance is still well within positive

growth—25% in the Base and 31% in in the Bull. In a very

unlikely Bear Case of a historically low (by more than

10%) 35% of revenues (table 3), cash alone will not be

able to fund RPXC’s CAPEX requirements for its growing

client base and the growth will become negative by 2016.

Depreciation and Amortization projections are the basis

of CAPEX projections. Historically, the two line up within

about $10 million of each other, CAPEX being on the

higher end. This is because depreciation and amortization

costs are associated with the acquisition of patents, which

is essentially how RPXC measures CAPEX. This means

that RPXC will likely not have to raise any capital in the

near future in order to fund the company’s business mod-

el. If the company does choose to raise capital, it can do it

through both equity and debt. It’s current debt level is 0%,

and has been since just slightly after it became public.

PRXC has enormous amount of leverage to work with if it

chooses to do so, or if cash from operations as a percent

of revenue fall more in line with the Bear Case.

Historic Operating Cash Flow as % of Revenue

2009 2010 2011 2012 2013 2014

Revenue 32.8 94.9 154.0 197.7 237.5 259.3

Cash Flow from Operating Activities 17.6 120.1 120.3 91.4 212.5 191.5

As % of Rev 54% 127% 78% 46% 89% 74%

Table 1

Table 2

Table 3

Table 4

3. Page 3

May 2015 $20.68 BUY Group 2

Cash Flows & Reoccurring RevenueRockstar Patents Purchase

On Tuesday December 23, 2014, RPX Corp announced

it would buy patents from the likes of Apple and other

Smartphone Tech firms. The sale is supposedly designed

to reduce the number of lawsuits over smartphone tech-

nology. The sale consists of over 4000 patents that are

owned by Rockstar Consortium and according to the man-

agement team at RPX, is the largest structured transac-

tion the company has ever been a part of. The deal, which

includes nearly over 35 other companies, is worth approxi-

mately $900 million.

Rockstar Consortium, was formed from the $4.5 Billion

purchase of about 6000 Nortel Network Corp Patents in

2011 following its bankruptcy. Rockstar also includes oth-

er Silicon Valley giants like Microsoft, Sony Erricson and

Blackberry. This is one of the first purchases of

Smartphone technology patents for RPX and the company

is hailing the deal as a “prototype” and that it hopes to fur-

ther promote innovation through their unique patent sys-

tem. John Amster, Chief Executive Officer of RPX Corp.

said that “Peace is breaking out,” after the deal was an-

nounced. “I Think people have started to realize that li-

censing, not litigation, is the best way to make use of pa-

tents, and this deal I a significant acknowledgement of that

reality.”

Cisco and Google are two of the companies who were

facing litigation from Rockstar so it’s easy to see why Cis-

co’s general counsel was pleased after the deal an-

nouncement; “With RPX acting as a clearing house and

deal manager, a global consortium of unprecedented

scale came together and reached a fair value for licensing

rights in a negotiated business transaction instead of a

courtroom. This is an approach and transaction that is

conducive for the entire industry.”

RPX received a transaction fee for its work, worth ap-

proximately $35 million and has been recognized on Q4

and Q1 revenues. As of September 30, 3024, RPX had

invested $890 Million to acquire approximately 4900 pa-

tent assets and rights, so completion of the deal with

Rockstar (which was finalized on February 3, 2015), effec-

tively doubled the patent assets that RPX has ownership

of, thereby doubling the amount of patents it can give out

to companies in return for subscription revenues. The ac-

quisition of these assets allows Rockstar to break into cell

technology patent industry, one of the busiest in terms of

litigation.

This will allow them to grow their client base substan-

tially. As large portion of RPX’s value is in their patent

“library”, this acquisition will make it increasingly more

valuable to subscribe to RPX patent litigation protection.

Not only will it attract new customers, but it will increase

the amount RPX can charge in each contract.

Due to the subscription business model of RPXC, much

of the company’s revenue is reoccurring in nature. For the

most recent fiscal year, subscription revenue consisted of

$251.4 Million of the total revenue of $259.3 Million. This

means that over the last year over 96% of RPXC Corpora-

tion’s revenue is subscrip-

tion based and therefore

reoccurring. In addition,

90% of the company’s rev-

enue is renewed every

year. It should also be not-

ed that the company gets

most of its revenue in a

single payment, and defers

the revenue evenly over

twelve months to comply

with GAAP. This makes

comparison from a quarter

to quarter perspective

much harder because if

they lost a client it would

not be apparent until the

following year.

The extremely high per-

cent of recurring revenue is im-

portant for any business, but es-

pecially a business like RPX. The

company’s success depends on them being able to go

acquire as many useful patents in order to gain new cli-

ents. One of the benefits of subscription revenue is that

you have the ability to focus on growth rather than focus-

ing on finding enough new or repeat business in order to

hit the same revenue numbers as last year. For example,

if RPX had $100 million in sales last year, they could know

with almost certainty that they could bring in $90 million

the next year, because of the 90% renewal rate. This

leaves management with the task of finding only $10 mil-

lion the next year in new sales, with everything over that

$10 million being growth on the previous revenues. The

reoccurring revenue model is key to RPX’s business be-

cause management can focus on what really matters to

their investors: growth.

Additionally, the reoccurring revenue model is essential

for great cash flows. As previously mentioned, cash flows

from operations (the core business) has since inception of

the company always been over 45%, and averaged over

65% of the total revenue. These cash flows are what we

as investors should be concerned with. Although cash

from operations are not quite the same as free cash flow

to the firm, it is still a good metric to look at. We as inves-

tors should understand that with a company like this, cash

*Chart from Investor Presentation

4. Page 4

May 2015 $20.68 BUY Group 2

Value as Defense Aggregator

flows should be a point of emphasis over earnings num-

bers. Currently RPX trades at over 20 times previous

earnings. This number is very misleading because of

RPX’s high amount of depreciation, currently around 40%

of revenues. This is expected with a patent company, but

because the earnings are being effected by the high

amount of non-cash depreciation, the earnings are being

artificially skewed. The actual cash earnings are much

higher. Right now, the company generates $3.53 per

share in cash flow from operations. They trade at 9.69 of

next years estimated free cash flows, and trade at only

4.36 times of the operating cash flows of last year’s earn-

ings. To get a sense of this high value, cash generating

giant Microsoft generates $3.94 per share in cash flow

from operations and trades at over 12.35 times the operat-

ing cash flow. Although this is a bit of an apples to orang-

es comparison, it still helps to show the great value this

company could be, especially in today’s high-priced mar-

ket.

Over the last 15 years, and more prolifically in the last 7,

the patent industry has shifted its approach from treating

intellectual property (IP) as a complicated legal entity to

treating patents as assets. This shifted has not only al-

tered this niche market, it has greatly affected the legal

and business practices of pretty much all companies doing

business in the United States. The change has created

four main types of patent companies. The most common

and influential companies are called non-practicing entities

(NPEs) and are more commonly referred to as “patent

trolls”. A subset of this category is offensive aggregators.

These companies buy or develop patents and then force

other companies who may possibly infringe on the IP to

buy a license to the patent. If the victim refuses, costly

litigation ensues. Some transactions jump straight to the

litigation face. There are also IP management companies,

who essentially consult with patent owners and how to

maximize revenues generated from their IP, which usually

ends in litigation.

The lack of an efficient market has created a hostile and

legally complex field which has a less than stellar reputa-

tion. The growing bad image of patent trolls has created a

huge market opportunity for RPXC. RPXC is considered a

defense aggregator, and they are the leader in this subcat-

egory. The company’s main services are patent defense

and RPX OPEN. RPXC buys patents on the open market,

then all of their subscribing customers collectively own

rights (with some exceptions) to the patent and can avoid

any infringement litigation. In 2013, 2500 companies faced

litigation. With only 204 customers in 2014, RPXC has a

high ceiling to grow into. Additionally, RPXC offers an

online market place for the buying and selling of patents in

an organized matter. Essentially the EBAY of patents, this

market creates a more efficient and friendly environment

for companies and patent owners to facilitate these trans-

actions. While the current trend is for transactions to occur

through litigation, RPXC hopes to shift trends and move

away from the bad name the industry has developed.

RPXC’s position as a defense aggregator, and more

importantly the largest defense aggregator, gives them a

number of huge competitive advantages. RPXC promises

to never use their patent ownership as a way to generate

litigation revenue. They have aligned their interests with

customers, making them a much better partner than the

alternative. This gives them superior likability and increas-

es the likelihood of subscription. Working as one entity in

the name of their collective customers, RPXC can reduce

inefficiencies. The company can provide one legal team

representing several of their customers in the event of liti-

gation, otherwise each company pays legal expenses and

the costs pile up. The biggest competitive advantage

RPXC has developed is via a network effect. Each cus-

Editors note: Disregards Rockstar Paten Acquisition due to time considerations

5. Page 5

May 2015 $20.68 BUY Group 2

tion is consistent as a percent of revenue, and because

CAPEX usually falls about $10M above Depreciation and

Amortization, CAPEX predications became more reliable.

Cash taxes are usually about $10M under reported in-

come tax expense and change in NWC is around -$25M,

which also increases accuracy of projections (see Appen-

dix B). With all these facts considered, the intrinsic per

share valuation price of RPXC is $20 (see Appendix B).

Because of the nature of predicting future numbers and

the lack of confidence in multiples, this method receives

70% weight in valuation (see Appendix E).

From a relative valuation standpoint, RPXC forces

some creativity. Huge Deprecation and Amortization

amount throw a wrench in EBITDA multiples and in an

industry where the focus needs to be elsewhere than

earning, earnings multiples are also funky. The metrics

developed for this report were MarketCap/PatentAssets

and TEV/Revenue.

RPXC is leading the world in patent acquisitions, which

is a key to the company’s ability to perform for its clients—

which makes a patent asset multiple important. It currently

trades at 3.5x, which is far above its competitors (.4x-2x).

Due to its size and influence within its market, RPXC right-

fully deserves higher multiples than its competition, but to

keep valuation conservative, the current market multiple

was used to deliver a share price of $17.39 (see Appendix

D), which is still a +14% premium when compared to the

current market price. This multiple is very indicative of a

company’s performance within this industry, so a 20%

weight was used in target price triangulation (see Appen-

dix E).

TEV/Revenue was used because it is more representa-

tive of the industry over all due to the fact that the focus is

on cash flows instead of the bottom line earnings to fund

operations. This was a straight forwards analysis, the in-

dustry ranged from 1.9x (RPXC) to 4.6x. Because of the

Rockstar acquisition and other revenue growth potential,

RPXC deserves a higher multiple than where it is currently

trading. 3.6x (see Appendix C) was used because it was

the industry average, so it delivers what we consider to be

conservative comparison given the completive edge

RPXC houses over its peers. This method gave a high

value of $29.12, which is far too inflated, thus only receiv-

ing 10% weight in target price triangulation (see Appendix

E).

When taking all three forms of valuation into considera-

tion, RPXC comes in at a buy recommendation with a

price of $20.68 a share—a 35% market premium. RPXC is

so undervalued because the market fails to see the im-

portance of continual patent acquisition—and RPXC’s ad-

vantage in this arena—and that the focus of valuation

needs to be placed on cash flows from operations rather

than earnings.

tomer gets access to a huge “library” of patents (over

10,000). Each new patent acquired benefits 204 custom-

ers, not just the owner of the patent. Each new subscriber

provides more capital for patent acquisitions. More patent

acquisitions make the “library” more valuable and encour-

ages more subscriptions. This builds rapidly, proliferating

their first mover and size advantages. While it makes

sense theoretically, it shows up in the financial statements

as well. For every dollar of patent assets on their books,

RPXC generates more than twice as much revenue than

their “patent troll” competitors. This financial advantage

will give them a huge advantage in patent acquisition.

More efficient sales generation allows them to buy more

patents adding to their network effect. These competitive

advantages, and RPXC’s alternative business model, give

them a huge leg up on their competitors. These justify

higher multiples in all relative valuation scenarios. The

company should be rewarded for its novel approach and

more importantly for its efficient use of the driving asset of

the industry.

Valuation & Recommendation

With company like RPXC, who’s business model is so

unique, intrinsic value is the bulk of valuation. Followed by

a Market Cap/Patent Assets ratio, and finally TEV/

Revenue. This metrics were chosen because traditional

metrics do not translate well for RPXC. EBITDA Margins

are huge because most of COGS is depreciation and

amortization expense, thereby throwing off EBITDA multi-

ples. P/E is also a poor multiple for RPXC cash flows are

emphasized over earnings.

In forecasting revenues, a revenue per company/client

was used as well as conservative growth estimate in the

total number of companies/clients (see Appendix A2). His-

torically this number for revenue/client has been con-

sistent around $1.40M, which was maintained for projec-

tions. RPXC has been adding clients in the range of 30-40

a year. Projected clients were kept at a conservative 25 for

2015-2018 and 24 in 2019. Not only do all of these projec-

tions fall under historical numbers, the Rockstar acquisi-

tion was also not factored into estimates—leading to over-

all conservative valuation, yet still landing with a buy rec-

ommendation.

RPXC came out as a strong buy because of a stellar Q1

2015, revenues were up by $11M from the previous quar-

ter because of the Rockstar acquisition. In the past, RPXC

has maintained very even quarters because of their dif-

fered revenue structure, and there is no reason to believe

that this will change going forward. However, Q2-Q4 reve-

nues are below the Q1 mark in order to project conserva-

tive numbers forward. Another key in delivering an accu-

rate DCF is CAPEX. Because Depreciation and Amortiza-