Indian #e commerce industry is it attractive for business or consumer by Alvis Lazarus

•

1 gefällt mir•1,213 views

A scholarly article depicting a multi-dimensional perspective of e-commerce in India - Indian #e commerce industry is it attractive for business or consumer by Alvis Lazarus.

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie Indian #e commerce industry is it attractive for business or consumer by Alvis Lazarus

Ähnlich wie Indian #e commerce industry is it attractive for business or consumer by Alvis Lazarus (20)

Mehr von World Trade Center Pune - India

Mehr von World Trade Center Pune - India (9)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

Indian #e commerce industry is it attractive for business or consumer by Alvis Lazarus

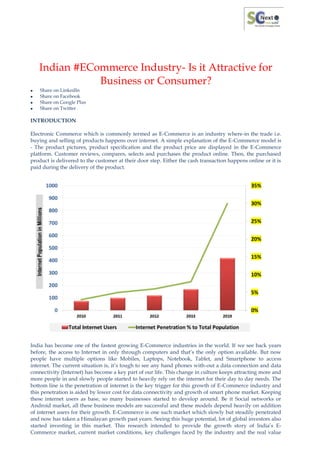

- 1. Indian #ECommerce Industry- Is it Attractive for Business or Consumer? Share on LinkedIn Share on Facebook Share on Google Plus Share on Twitter INTRODUCTION Electronic Commerce which is commonly termed as E-Commerce is an industry where-in the trade i.e. buying and selling of products happens over internet. A simple explanation of the E-Commerce model is - The product pictures, product specification and the product price are displayed in the E-Commerce platform. Customer reviews, compares, selects and purchases the product online. Then, the purchased product is delivered to the customer at their door step. Either the cash transaction happens online or it is paid during the delivery of the product. India has become one of the fastest growing E-Commerce industries in the world. If we see back years before, the access to Internet in only through computers and that‟s the only option available. But now people have multiple options like Mobiles, Laptops, Notebook, Tablet, and Smartphone to access internet. The current situation is, it‟s tough to see any hand phones with-out a data connection and data connectivity (Internet) has become a key part of our life. This change in culture keeps attracting more and more people in and slowly people started to heavily rely on the internet for their day to day needs. The bottom line is the penetration of internet is the key trigger for this growth of E-Commerce industry and this penetration is aided by lower cost for data connectivity and growth of smart phone market. Keeping these internet users as base, so many businesses started to develop around. Be it Social networks or Android market, all these business models are successful and these models depend heavily on addition of internet users for their growth. E-Commerce is one such market which slowly but steadily penetrated and now has taken a Himalayan growth past years. Seeing this huge potential, lot of global investors also started investing in this market. This research intended to provide the growth story of India‟s E- Commerce market, current market conditions, key challenges faced by the industry and the real value

- 2. proposition for the business and the consumers. This research paper also focuses on the Online Retailing segment within the E-Commerce Industry when trying to evaluate the attractiveness of this industry from business and consumer standpoint. There are multiple channels of distribution available in India and currently E-Commerce is one among them. And, E-Commerce is seen as highly convenient model since it saves time in purchasing a product. HYPOTHESIS The research idea is to get insight into E-Commerce Industry to establish - Growth story of E-Commerce Industry in India Is the Indian E-Commerce Industry attractive for Business or Consumers? With tremendous growth potential in the coming years and good availability of funds are seen as positive for Business (B2C E-Commerce Players) and on other hand, multiple selection options and easy of shopping are the positives for the Consumers (Online Buyers). For whom is this Industry more attractive? RESEARCH SCOPE The scope of this paper is to research on the current E-Commerce Industry in India. This research has two sections to it. Section-1 captures the growth story of the E-Commerce Industry, Current Market share, Growth potential, Supply Chain Model etc. Then, this paper discuss Further, the paper focuses on the growth story of E-Commerce from year 2000, Current Market share, Growth Trend, Major Players in the Industry, Penetration by Categories, volumes etc. Section-2 evaluates the booming B2C E-Commerce (Retail) from Business and Consumer standpoint to conclude whether the current E-Commerce Industry is attractive for the Business or the Consumer. GROWTH STORY OF E-COMMERCE INDUSTRY IN INDIA Electronic Commerce (E-Commerce) is a platform in which buying and selling of goods is done and for this internet is needed. Based on the Buyer and Seller, there are 3 types of E-Commerce: C2C (Consumer to Consumer): C2C transactions happen between customers. The E-Commerce players provide the platform and the processes, through which the transaction takes place. A commission on the transaction value will be the gain for the E-Commerce player. Example of C2C businesses are – Online auction (E-Bay), Online Classifieds, Online Real estate (Commonfloor.com, Magicbricks.com, and 99acres.com). B2B (Business to Business): B2B are the transactions between businesses. Examples of this model are – Indiamart.com, TradeIndia.com, and Sulekha.com. B2C (Business to Consumer): B2C is the most common form of E-Commerce in which a variety of goods are available. Few categories to name are Electronics, Apparels, White goods, Footwear, Stationery, and services like Online Travel Booking and Online Matrimonial websites. Few key players at different categories of B2C are Flipkart, Snapdeal, Amazon, Cleartrip, Expedia, Ibibo, IRCTC, MakeMyTrip, Yatra, Jabong, Myntra, Yepme, Zovi, FabFurnish, PepperFry, UrbanLadder, Zansaar, BigBasket, EkStop, LocalBanya and ZopNow. Main Flows in E-Commerce: There are 4 key flows in E-Commerce and they are (1) Product Flow, (2) Cash Flow, (3) Information Flow, and (4) Reverse Product Flow.

- 3. Product Flow: This is the movement of the goods from the suppliers till the customers. Logistics players play a key role in moving products through this chain. Cash Flow: Cash flow is from the customers back to Suppliers through the multiple stake-holders in the E-Commerce model i.e. from Customer to E-Commerce players and Supplier through intermediaries. Information Flow: This information flow happens in both the directions and a key flow which is vital for the proper functioning of the end to end activities in the E-Commerce model. Reverse Product Flow: This specifically means the product returns and damages which has to be picked from the customer and returned to the supplier through the E-Commerce player. Birth of E-Commerce in India If we go back and analyze the birth of E-Commerce in India, the start of dot com companies started in the mid-1990s and B2B E-Commerce portals are introduced by 1996. Less awareness, meagre Internet penetration and no confidence in online payment systems were reasons for E-Commerce not gaining momentum. Second wave of E-Commerce started way back in the year 2000 through some small online shopping web platforms. The IT crisis of 2000 caused all these initiatives to be turned down and there were no major activities happened in the E-Commerce space for next 5 years. From year 2005, the real growth of E- Commerce has kicked off and the first category to penetrate well is the „Online Travel‟. At 2006, online travel booking is enabled by the entry of LCC (Low Cost Carriers) in airline industry and selling of tickets through the Online Travel Agents (OTA). By this same time, the e-ticketing had been already started by Indian Railways. Year 2007 marked the start of multiple online retailers and e-tailing is leveraged to provide a differentiated service and enhance customer experience. Group Buying started in the year 2010 and Social commerce is used as a medium to reach out to customers. Current E-Commerce Market in India & Key Players From the year 2010, E-Commerce has seen a tremendous growth which is aided by the growing internet penetration. With a staggering CAGR of 34.58% from 2009 to 2012, the Industry has expanded from USD 2.5 Billion to USD 16 Billion in a matter of four years from 2009 to 2013 (Source: www.dazeinfo.com).

- 4. According to a survey by ASSCHOM, E-Commerce grew at an enormous 88% in 2013 to USD 16 Billion and expected to reach USD 56 Billion by 2023. It is more appropriate to name the key players in each of the segment since most of the them are niche players in various segments like books, consumer electronics, fashion, apparel, furniture, grocery, deals etc. Hence, it is more meaningful to explain the current trend and key players segment wise. Out of the total E-Commerce pie – Online travel contributes for 70% and specifically E-Tailing (Online Retail) contributes for 16%. The estimated current market share of E-Commerce (Online Retail) is INR 12,000 Crore and the key players and market leaders are specific to each segment. Multi category segment is the largest in the online retail industry and currently attracting most of the investments and the top players in the market place in multi category segment are Flipkart, Snap-deal and Amazon. Travel sector, which is estimated at around 8 Billion USD accounts for around 70% of the overall Indian E-Commerce market in 2013 (Source: IAMAI). In the travel sector the key players are Clear trip, Expedia, Ibibo, IRCTC, Make My Trip and Yatra. This travel segment is also seeing some signs of consolidation. In Fashion and Lifestyle category the major players are Jabong, Myntra, Yepme and Zovi. In Furniture, FabFurnish, PepperFry, UrbanLadder and Zansaar are the key players. Furniture is expected to become the third largest segment after Electronics and Fashion. This segment is expected to grow almost 4-5 times this year. Market place player, Snapdeal has already launched furniture and Flipkart & Amazon may start Furniture soon and they are currently exploring. In Grocery segment, the major players are BigBasket, EkStop, LocalBanya and ZopNow. Grocery market potential is expected to be around 400 Billion USD and that would pose all attributes to become the largest sector. Though the number of transactions is very healthy, the major challenge in this sector is „Managing Inventory‟ and „Logistics‟. Capital Funds One another key factor fuelling the E-Commerce growth in India is the Venture Capital Funds. There are hundreds of Venture capitalists currently operating in India but out of them the top 7 have the cream of investments, they are Accel Partners, Helion Ventures, Nexus Ventures, Tiger Global, Kalaari Capital, IDG Ventures, and SAIF. According to Venture Intelligence and a report from Economic times, these seven VCs account for 222 of the 414 investments or 54% of the deals that have materialized in the ecommerce space since 2007. Accel Partners is the leader, with 54 investments out of the total. It is followed by Helion Ventures, Nexus Ventures and Tiger Global, respectively.

- 5. These capital risk funds have a major stake in the growth of India E-Commerce Industry. With Flipkart‟s recent one billion dollar fund raising and Amazon allocating two billion dollars of funds for investment at Amazon India, Indian E-Commerce industry is all set to pose like a war field. These VC also demands key part in the decision making. For example, Accel and Tiger who has a stake of 40% in both Flipkart and Myntra, would have obviously triggered their merger. These kind-of happening is not new. As we remember Flipkart acquired Letsbuy.com and Myntra acquired Exclusively.in; what is common in these is, these companies have common investors and hold a good stake in the companies. E-Commerce Supply Chain model Under the E-Commerce supply chain model, the types of business models, Customer touch points, Supply chain model are explained below: Business Model - There are two different business models in E-Commerce – (1) Buy & Sell and (2) Market place. In Marketplace, products from multiple vendors are displayed in the online platform (Website) and the products could be from Brand, Shops or even Individual person. The marketplace provider takes care of the marketing and attracting customers, ensuring track of transactions and the user interface, whereas the vendor who is displaying his product will take care of availability of product and shipping. Marketplace provider takes a percentage of the sale as his revenue from the vendor. Marketplace doesn‟t hold any physical inventory and thereby avoiding holding costs. Hence, Marketplace can offer a wide variety of products but the major concern for this model is the real time data and information flow between vendor and market place systems and product quality. In Buy and Sell model, the products are purchased by the E-Commerce organization and stocked at their warehouses. Those procured products are displayed on the website and once the customer purchases the product, the product is delivered to the customer at his/her doorstep. In this model, huge inventory holding cost is a major setback but the benefit is the product can be delivered quickly to the customer and also highest level of customer experience can be provided since the E-Commerce provider manages and accountable for the delivery and quality of the product. Customer Touch Points - In E-Commerce there are 5 main customer touch points. They are Marketing, Front End, Payment, Customer Service and Product Delivery. All these 5 main touch points are so critical since they impact the Customer experience and Satisfaction.

- 6. First and most important touch point is the marketing. E-Commerce depends heavily on marketing. Way back in 2010-11, the Ad spends of E-Commerce companies are INR 10 Lakhs which has grown taller to reach INR 25-75 Crores in 2014 (Source: Economic Times). On an average, online retailers spend 10-15% of annual revenue on advertising and marketing. The current trend in E-Commerce industry is personal and digital marketing and with growing importance of marketing, E-Commerce companies are also hiring marketing firms like Lowe and Partners, Scarecrow Communications and Happy Creative Services to steer their marketing campaigns. "It's mainly in countries like India that online brands need to use traditional media to propagate the use of the online service, especially if the larger pie of the consumers is not necessarily online," said Kartik Iyer, CEO at Happy Creative Services. (Source: Economic Times). Front end to the customer is the „Website‟ which is the face of the organization and a critical tool to attract more customers. Search engine optimization and web maintenance directly impact the traffic to the website and the click to conversion rate of customers. User interface, web design, catalogue and content management are the key things to ensure a seamless user interface and experience. Payment processing is another customer touch point where the customer pays the product cost through the payment processing gateway. There are basically two types of payments – Online payments or Cash on Delivery. Online payment is made upfront when the product is purchased and before the product is delivered. In Cash on delivery, the payment is done when the product is delivered to the customer and another model which is almost similar to this is the Card on delivery model where the payment is made through card during the delivery of product. Customer Service plays a role right from order till delivery of the product. Customer service team takes calls to clarify on product specification or related information, it also updates the status of the order when asked by customer, and it also supports the customer on post sale clarifications, product returns and any other concerns. The final and most critical touch point with the customer is the last mile delivery where the company customer associate (CA) or Field executive (FE) will carry the product and deliver the product to the customer. This touch point is so important since the entire brand name of the organization relies on CA/FE‟s communication, attitude and behaviour when he is at the customer‟s place. E-Commerce Supply Chain A basic supply chain model for the Buy and Sell online business is shown in the schematic diagram below.

- 7. The Sales and Operations planning (S&OP) team of the E-Commerce organization does the Demand and Supply planning. This planning takes into account the forecast from the category teams and the available and planned capacity from the Operations planning team. Based on the S&OP, the purchase orders are released to the Vendors/Suppliers/Brand/Manufacturers. Basis the schedule, the products are delivered at the Warehouses or Distribution centre of the E-Commerce organization. From there, the products are distributed as per plan and need. The customer uses the web to view and select the product he/she needs from the E-Commerce organization‟s website and purchases the product. Once the customer has ordered the product, the order reaches the nearest warehouse. The orders are consolidated based on a pre-defined cut off which depends on the service levels committed to the customer and based on the optimum performance of the operations. Consolidated orders are picked, packed, labelled and invoiced. The products are delivered to the customer at their door step and that is called the „Last Mile Delivery‟. There are a lot of ways the Last Mile delivery is planned and few time slot based deliveries are explained below: Scheduled delivery In scheduled delivery, Customers can select any specific date for delivery within a specified time period after placing an order. For example, Flipkart offers a window of 7 days within which customer can select a delivery date. Same-day / Next-day delivery If customers do not prefer a scheduled delivery, they can opt for SDD (Same Day Delivery) or NDD (Next Day Delivery). E-Commerce players offer this option for most tier 1 and tier 2 cities. Though it is the most preferred option of the customer and they need the ordered products immediately, this needs a well-coordinated logistics planning and execution. To achieve optimum logistics cost in this model, substantial volumes are needed every day on all the lanes where this SDD/NDD options are offered. Slotted Delivery Customer can pick a preferred delivery slot and the slot timing can vary from 2-4 hours. BigBasket.com offers 2 hours slot and offers around 4 slots in a day. After the order is placed by the customer, they display the available slots for the same day and the next day for the customer to choose from. Open Box Delivery One of the major challenges faced by the E-Commerce players is „Product Returns‟. These returns could not be questioned or argued with customer since the product is not seen during delivery and it can badly impact the customer experience and may end up in losing market share. Around 30-40% of the return reasons are product damages and the solution to this is „Open Delivery‟. In this model, the product is unpacked and displayed to the customer. Also the customer signatory would be received in an online form using a tab or a hard copy of a form. This can be a valid proof and means to solve most of the post- sale issues coming out of product damages. Though „Open Box Delivery‟ is not going to solve all the issues, it will certainly solve most of them. For example, a customer who signed off on a form after receiving his brand new laptop as open delivery can‟t come back and complain that the laptop screen is fully broken. Another great advantage of this model is – Any genuine intact shortages or damages found out during Open Box Delivery, can be taken back in the same delivery vehicle avoiding extra reverse logistics cost and we can avoid customer waiting time significantly since the replacement product can be initiated immediately. Open Box Delivery will increase your delivery time a bit and may negatively impact the number of deliveries per vehicle/trip. Currently, this model is not used by any E-Commerce players but definitely this is in pipeline. Plug and Play The final model is the „Plug and Play‟. As the name implies, the product is plugged and played during the forward flow itself. This would not only sort out the product damage claim during post sales but also ensures that the product is in working condition during the time of delivery. Though it sounds great, effective implementation of this is a big challenge. The reason is – this model expects the field executives (FE) to actually set up a product and shows it working condition which demands high quality people and training for the FE(s). Hence, Plug and Play has to be evaluated sector-wise and can be switched-on on segments where it will be effective. Even this model is not in practice but we can experience them soon.

- 8. IS THE E-Commerce Industry attractive for Business or Consumers? Attractiveness of the E-Commerce industry is analysed through Porter‟s 5-Forcse model (Competition within Industry, Threat of new entrants, Threat of substitutes, Bargaining power of suppliers and Bargaining power of customers), SWOT (Strength, Weakness, Opportunity and Threat) analysis, Challenges faced by the business, Consumer value proposition and the issues faced by the customer. Porter’s 5-Forces Model for E-Commerce Using Porter‟s 5 Forces model, the current E-Commerce industry is analysed for the rivalry within the industry, threat of new entrants, threat of substitute products, bargaining power of suppliers and the bargaining power of buyers. Threat of New Entrants: Current E-Commerce industry has a lot of potential for growth for all the players. With E-Commerce industry estimated to reach 56 Billion USD by 2023 there is wealth of opportunities for lot of new players to gain market share and expand their business. There are no entry barriers for starting up a new E-Commerce business and all you need is well managed platform to showcase your products, swift operations team to deliver product quickly and a customer service team to excel in customer satisfaction. In addition, the initial capital investment needed for starting an E- Commerce business is very less and for most of the start-ups with around 100 SKUs (Stock Keeping Unit), the capital needed us well within INR 10 Lakhs. With 51% of FDI allowed in multi brand retail for market place, there is lot of funding options for the new players when they look for expansion. All these factors pose a huge threat of new entrants to the current E-Commerce Industry. Threat of Substitutes: In the E-Commerce industry, that too specifically in the Market place, there are a lot of options and varieties available for the same product with less differentiation. Since there are a lot of suppliers competing in the same space, pricing plays a vital role in gaining more market share. With no switching cost for the buyers, the current E-Commerce industry has a huge threat from substitute products. Bargaining power of Suppliers: For the manufacturers, E-Commerce is one among multiple channels for selling the product to the customers. The bigger manufacturers who are already having a good brick and mortar presence can easily forward integrate to start the online retail channel also on their own.

- 9. Bargaining power of Customers: With E-Commerce industry in full expansion mode, there are a lot of campaigns, policies and processes to gain and retain customers. Customers have access to pricing information across different E-Commerce players. With no product differentiation there is no switching cost. Cash on delivery, Easy returns, Cheap price, Exchange offers and Same day delivery etc. – all these are initiatives towards gaining more and more customers. With more intense completion in this E- Commerce industry, Customers have good bargaining power. Rivalry within Industry: With high threat of new entrants and no entry barriers, the competition in the E-Commerce industry is so intense and getting more intense day by day. Business have to come up with new initiatives every often and spend more in marketing to be in the competition. With high chances of forward integration on few segments by large manufacturers/suppliers and the competition from the traditional brick and mortar business fuelled the competition still more. SWOT Analysis Business Challenges Though the current E-Commerce industry is seeing explosive growth and showing tremendous potential, it is facing a lot of business challenges also. Key challenges currently faced by this industry and the challenges ahead for the E-Commerce industry is described below. Cash On Delivery (COD) As we all know, change is the most sensitive thing to handle and change management is the most critical lever for success. Even online shopping is not an exemption and they have to manage „Big Change‟ of the move from „Brick and Mortar‟ (Touch and Feel) model to Online Model. This huge change is managed by a key driver named the Cash on Delivery (COD) Model. COD model ensures the customer that their hard earned money is safe and demands payment only after product delivery. Currently COD is accounted for 60% to 70% of online retail sales (Source: study by Internet and Mobile Association of India and audit firm KPMG). This huge dependency on cash-on-delivery model is proving to be so costly for the E- Commerce players who offer this mode of payment. This huge percentage of COD transactions clearly

- 10. shows that the growing E-Commerce customer base is not proportional with the adoption of payments through credit or debit cards. Also, this COD model has a negative hit on the bottom-line in multiple ways. “The COD payment transactions add about 3% additional costs to the E-Commerce firm," said Ashish Jhalani, founder of e- Tailing India. This additional cost can climb up-to even 25-30% when the product is returned by the customer. Typically as a cost per delivery, COD transactions incur an additional expense of INR 35-65 for every transaction involving cash on delivery and it is as high as INR 100 in cases of returns in COD model (Source: Study by market research arm of Avendus Capital). To implement COD model, lot of effort is needed and most E-Commerce companies have spent years putting the processes deal with these issues. But, COD model is not a business friendly model for the very reason it involves cash handling. This increases the cost and also increases the cash receiving cycle by 10-14 days. Most E-Commerce companies have currently restricted the value of goods that can be bought on COD model. For example, Flipkart has kept the limit at about INR 50,000. In addition, the maximum percentage of customer returns is from cash on delivery model. Having said all these, current E-Commerce players are relying on COD model for penetrating into market and there are struggling to remove or replace with other options. Profitability of the Industry We have discussed much about the booming E-Commerce sector and the potential growth we can expect in the coming years. But the other side of this story is – „No E-Commerce players are profitable‟. Most of the E-Commerce players are working out ways to be profitable in next 2 years but that is going to be a tough ride since this current industry is primarily driven by customer value proposition and specially the product cost. In fiscal 2013, Snapdeal posted losses of Rs 120.1 crore and reported losses of Rs 81.2 crore in fiscal 2012 (Source: Company's financials filed at the Registrar of Companies). Flipkart India reported a loss of Rs 281.7 crore before extraordinary items and tax in fiscal 2013, according to documents filed with the MCA, compared with a Rs 109.9 crore loss in fiscal 2012. (Source: Ministry of corporate affairs' (MCA) website). Even if we look at Amazon founded way back in 1994, is never been profitable till now. The general belief is that E-Commerce has become a successful distribution channel. That is too early to conclude keeping in mind that online retail is just <1% of the total retail sales and the logistics model is not scalable when E-Commerce companies tries to become profitable. Channel Conflicts As the E-Commerce has seen explosive growth and as more products move through the E-Commerce channel, conflict arises between the traditional Brick and Mortar model and the E-Commerce model. The root of this conflict is pretty straightforward – Online channel is capturing market by offering the lowest price and they are quite able to do that because Online Channel chops off all the intermediate channel partners like the distributors, stockiest etc. and most of the E-Commerce players are having enough funds in the pocket and their prime focus is to expand the market and not the profitability. This product pricing can‟t be matched by the traditional Brick and Mortar players and this is the reason for the conflict.

- 11. Due to this, the big handed traditional players put tremendous pressure on the brand and this force the brand to an extent where they ask the customers not to buy from online players. Few examples of these conflicts are – Toshiba India stating that “they don‟t have any tie ups with E-Commerce players and they are not authorized to represent quality of Toshiba branded products”. Director from Lenovo India quoted as saying “Largely due to market place kind of set up, there are a lot of resellers that have got added up, which are selling at very low prices. These we believe may or may not be an authorized or genuine product”. Nikon also went ahead and publishing a similar statement last year. We can also notice a small board carrying the picture (sample picture attached above) is displayed in all Nikon showrooms and at the retailers place. It states “Please note that E-Commerce websites like Flipkart and Snapdeal are not our authorized partner/dealer in India, we advise you to check the warranty entitlements while buying from online portals”. Though these statements seem to preserve the customer interests, the real intention is to create panic and discourage buying products through online channel. These conflicts pose a huge challenge for this industry. Reverse Logistics Reverse logistics is the collection of all processes that come into play for goods that move in the reverse direction, i.e., from the customer to the business. The reverse logistics process flows are Retrieve -- Transport -- Receive -- Inspect -- Sort -- Act. Reverse Logistics is of great challenge for the E-Commerce players. In the forward flow, only the sign off for the product receipt is given by the customer and this creates a lot of grey areas related to the right quality of the product received. With forward flow concentrating on only the number of deliveries and on-time delivery and product quality is not verified during delivery, the E-Commerce player has to rely on the customer‟s claim and honor all the return requests.

- 12. The most important activities of Reverse Logistics are explained below: Physical Movement of Goods: Once the return request is authorized, there are different methods by which the goods are received back from the customer. Some E-Commerce organizations organize a pick- up of the product at the door step of the customer and few organizations asks the customer to mail in the goods and they do send the return slips with address during the forward flow itself. Store: The physical goods that are returned by the customers are received at the return warehouses and they are accounted for tracking and stored. All the inventory accountability best practices of the warehousing on forward flow are followed for the return products also. These warehouses normally will have the capability of packing, refurbishing and testing so that the proper action needed on the return product can be done. Sort: Once the products are received and stored at the warehouse, they are sorted based on their condition and fitness for use. Most of the products in good condition which are returned the same day due to order cancellation or any other reasons will be checked and sent back to good stock. This is called the „Return to Origin‟ and even the undelivered products falls into this category. Most of the products returned are due to damages or product not fit to use; these products are repaired or sent back to Supplier based on the terms with the supplier. Other products are either sold as defective products or they are scrapped off. Repair: It is a key step in the reverse logistics supply chain. Predominantly, E-Commerce players are leaving this to a third party who buys these products at lowest price, refurbishes it and then sells them in the second market. The reason is the E-Commerce players could get blocked and stuck with huge returned goods and huge money could get blocked on the return products. Major percentage of reverse logistics involves rejecting and scrapping the goods collected from customers. This needs a lot of policies related to environment to be followed. As a result, a third party specialist provider is needed so that he can dispose them off in a fashion which is compliant with regulation. Tax Structure At E-Commerce Industry, inter and intra state movement of goods are most common and specifically in Buy and sell model, these transactions are more. The basic taxes are the VAT and CST. Value added tax (VAT) is charged by the state government and this is charged on the products sold within a state from the warehouse/facility located within the state. Central sales tax (CST) is charged by Central government and CST is levied at those cross border sale transactions. Non-uniform VAT rates across different state governments, CST and the retention of VAT in case of inter-state stock transfers makes the tax structure so complex; this makes the network planning and the warehouse location planning so tedious. These puts the E-Commerce firms to come up warehouses at each state to avoid paying CST and avoid a cost head on their logistics cost. But, this makes the overall operations so complex. Implementation of Goods and Services tax (GST) is expected to solve this issue but still the implementation of GST is under question and there are a lot of state related issues to be sorted out. The introduction of GST is still under discussion and debate. No conclusion is arrived at yet in GST. There are a lot of issues and call outs raised by each state has to be addressed. The key issue is related to petroleum which constitutes to 26% of the state revenue and the state wants this to be out of the GST scope. Also, the crux of the issues is, state fear that they loss their revenue and may lose their self- sufficient status; hence they want a compensation from the centre. These critical issues have to be sorted out before GST goes live.

- 13. Foreign Direct Investment (FDI) As per current FDI norms, 51% of FDI is allowed in multi brand retails and 100% FDI is allowed in single brand retail. These FDI norms also have some pre-conditions like 50% of the foreign investment to be invested in back end infrastructure (logistics, cold storage, soil testing labs, seed farming and agro-processing units), minimum sourcing of 30% from SME‟s. The above policies are as such applicable for E-Commerce industry also. So defining the policy for E- Commerce industry - As per Exchange Maintenance Act (FEMA), foreign companies can only invest in B2B (Business to Business) companies. But in „Buy and Sell‟ model such foreign investments are not allowed. This adds a lot of complexity to the working model for the E-Commerce companies. In order to establish compliance, both Flipkart and Myntra have moved into a marketplace model, thereby aligning them compliant to foreign funding. Even Amazon which is been into Buy and Sell model, has entered into Indian market as a Market place model to be compliant. Another classic example is, Flipkart creating a separate entity called „WS Retail‟ and on-boarded WS Retail as a seller in the Flipkart‟s market place platform. Also adding to the pain, there are consistent notices from ED for improper routing of FDI into the systems and we have also huge fine being posted for E-Commerce companies in the recent past. Most recent one, June 2014 – Flipkart and Amazon are under the radar by the ED for the same reason. Consumer Value Proposition The current E-Commerce Industry is much customer focused since it is it expansion mod; the E- Commerce whose going to win the maximum customer pie is going to the clear winner. At this industry retaining the customers is tough since there is no switching cost and multiple options are available and the only way to retain the customers is to have a unique value proposition to the customers. Hence, the current E-Commerce Industry provides a lot of value proposition for the customers to give them the value for money, seamless customer service and an excellent shopping experience. Few of the key value propositions for the customers are explained below: Product Cost In the traditional model of Brick and Mortar, the product is manufactured by the manufacturer and he adds a Mark-up on his Cost of Goods sold and sells to the Distributor. Likewise Distributor and Retailer add in Mark-up before it is sold to the customer. On an average, these distribution Mark-ups vary from 20-50% depending on the product category. These mark-up at each stage adds up to the product cost and this is not avoidable in traditional channel, since these channel partners are much needed for the distribution of the product.

- 14. In E-Commerce model, the channel mark-ups are avoided and specifically on the products which are directly sourced from the brand, huge channel mark-ups are saved. This is one of the reasons how the E- Commerce firms are able to give jaw dropping prices for the customers. In addition to this, E-Commerce industry is in Expansion mode and the prime focus is to capture the market and the focus is not profitability. With the back-up of the funding available, E-Commerce players cut off on their margins to provide the best price to the customers and capture the market. At the present scenario, no other traditional channels can match the product pricing in the E-Commerce channel. Product Catalogue Variety is another key value-add for the customers. Specifically, in the market place model huge numbers of suppliers are on-boarded to provide a variety of options to the customers. Amazon which has started operation in India on June 2013 has quickly set up the market place model and currently offers around 17 Million products across 28 categories and it has around 9,000 sellers on-boarded. Bangalore based, Indian E-Commerce player – Flipkart has moved into market place model last year and currently has 30 Million products across 70 categories and has around 3,000 sellers. This provides a huge variety of options at one platform for the customers so that they can select, compare and choose the right product at ease. Other Value Adds Apart from the Product costing and the variety, E-Commerce model has much to offer for the customers. With Free home delivery, Same day delivery, Easy Returns, 30-Day replacement options, Product Exchange, Special offers etc., E-Commerce industry is providing a lot of value proposition for the customer to gain and retain the maximum pie of the market share. Key Issues faced by consumer Online Fraud and Security Concerns In E-Commerce model, the customer has to make the payment for the product through a payment gateway. The exceptions are the post pay options like Cash-On-Delivery, Card-On-Delivery and Check- On-Delivery where-in the payment is paid during the product delivery. In all there instances, the payment is made online through the payment gateway. A payment gateway service authenticates and passes on electronic payments made by online customers to E-Commerce merchants i.e. the movement of funds from the Customer‟s account to the Merchant‟s account. It allows E-Commerce merchants to accept credit cards on their websites. Also there are two different types of payment gateways – (1) Merchant side Application programming interface (API) and (2) Secure Order Form. In the former, the processing code resides in the merchant‟s website and uses API and in the latter, the codes resides on the payment gateway provider and from the merchant‟s website the customer‟s will be re-directed to the payment gateways provider‟s website to make the payment and then return back to the E-Commerce merchant‟s website. Security is one of the growing concerns that restrict customers from engaging with E-Commerce. The integration with third party service providers introduces new security challenges due to the complexity of it. Due to the increase in warnings and growing security concerns and cases of identity theft and financial fraud being reported in news, most customers stay away from performing online transactions and prefer not to shop online or prefer the cash on delivery model. Product Quality Most E-Commerce players are able to provide a wide variety of products by being in the market place model where they don‟t have to hold stocks. The E-Commerce players rely on this huge network of vendors for availability of products and the product quality in the market place model. Right contracts and terms are to be in place to ensure that the genuine product reaches the customer. Though E- Commerce players ensures that they replace any product damages and attend any post sales related issues immediately, this link has good probability for fake products to enter into market. Shopping Experience Though E-Commerce has a lot of benefits and value proposition for the customer, the one critical disadvantage is non-availability of the „touch and feel‟. Specifically for products like Home appliances, Furniture etc., the touch and feel of the product is much needed. E-Commerce companies are trying their best to match to the touch and feel experience. For example, In Lenskart we can upload our picture and test the available frames by wearing it on the picture and most of them gives the options of 360deg

- 15. rotation and Zoom options on the product pictures. Having all this, still the shopping experience in a brick and mortar model couldn‟t be matched. For now, this negative in E-Commerce model is compensated with unbelievable product pricing, product variety and excellent seamless customer service. Attractiveness of E-Commerce Industry - Business Vs Consumer 5 Key Point - Value Analysis The E-Commerce Industry is analysed and also the previous discussion points in this research paper are consolidated against 6 points for Business and the Consumer. From the Business standpoint, the value is analysed against 5 key indicators namely, (1) Attractiveness of the Industry, (2) Growth, (3) Profitability, (4) Government Policies, and (5) Customer Loyalty; From the Consumer standpoint, the value is analysed against 5 key indicators namely (1) Variety, (2) Product Cost, (3) Product Quality, (4) Reach & Security, and (5) Shopping Experience. Business - 5 Key Point Analysis 1. Attractiveness of Industry - Negative With intense competition within the industry, no entry barriers posing threat of new entrants, no product differentiation posing huge threat from substitute products, huge possibility for suppliers to forward integrate and huge bargaining power of customers makes the current E-Commerce industry unattractive. 2. Growth - Positive With E-Commerce grown at a CAGR of 59% from 2009 to 2013 and estimated to reach 56 Billion USD by 2023. This industry has huge potential for explosive growth in the years to come. 3. Profitability - Negative E-Commerce is in expansion mode and all Top E-Commerce companies in India are profitable. This is certainly a huge task ahead and all the players are trying to be profitable in another 1-2 years. 4. Policies - Negative Complex taxation structure (CST/VAT) and FDI norms makes the processes and operations so complex to manage. Though FDI norms is going to support the home grown companies to have the advantage, at a larger picture easier taxation norms and FDI policies are needed for E-Commerce companies to grow at good pace. 5. Customer Loyalty - Negative With no switching cost, no product differentiation, variety of options and all information of product available at ease in the platform, customers have huge bargaining powers. This industry is hugely driven by product cost and customer loyalty is very less. E-Commerce players have to spend huge marketing cost and provide unique value proposition to retain customers which is not an easy task. Consumer - 5 Key Point Analysis 1. Product Variety - Positive Top E-Commerce companies like Flipkart and Amazon offers more than 1 Crore products across 40+ Categories. Certainly, E-Commerce platform is an easier way to view, compare and select the right product. Specially market place model where-in there is no need of inventory to be bought and stored, onboard multiple vendor across country to provide a huge variety of products to the customers. 2. Product Cost E-Commerce model, by cutting the distribution mark-ups is able to provide the best product cost in the market. In today‟s scenario, no other channel is able to match the E-Commerce product costing and that is the unique advantage currently E-Commerce model has. 3. Product Quality - Negative Though there are no much reported quality issues and E-Commerce players have excellent policies around Customer returns and product quality, still this is an area of concern with E-Commerce from the Consumer stand point.

- 16. 4. Reach and Security - Negative E-Commerce is yet to penetrate well into Tier-III cities and overall it is yet to grab a good pie out of the overall market. Also, more security concerns surfacing out at this nascent level of the E-Commerce industry; security related issues are real show stoppers for growth. 5. Shopping Experience - Positive Certainly, Touch and feel is missing in the E-Commerce industry. But, with the maximum value for customers through Cost, Variety, Free Home Delivery, Same day delivery, Easy product exchange, 24x7 Customer Service, and Easy product returns – E-Commerce provides excellent shopping experience on all the categories it operates. Considering the research findings and the survey responses, there are few things which are evident. 1. Current E-Commerce Industry is driven by Cost as a key driver 2. With no switching cost and product differentiation, customer loyalty is very less in this Industry 3. With ease and high visibility of product information, Customer bargaining power is much high in this industry 4. Customers value propositions are the only option to gain market and retain customers, even at the cost of losing margins 5. With no entry barriers, Suppliers have a huge opportunity to forward integrate and reach out to customers directly 6. With immense pressure from Risk Capital funds, E-Commerce organizations have a tough path ahead to become Profitable soon Year 2009 till 2014 is seen as the years of tremendous growth of E-Commerce Industry and from mid- 2015 will be the years of tough ride for the E-Commerce players. The main agenda would be To provide the same value proposition to the customers and also be profitable to keep the investors happy Set right all the systems legally compliant Stay in the competition; Compete not only with the E-Commerce players but also with the traditional Brick and Mortar model who will certainly forward integrate and start their own E- Commerce vertical. With Business having a list of challenges to work on, Consumers can continue the „Value Proposition‟ offered in this E-Commerce Industry and can keep demanding for more and this research paper concludes… “Current E-Commerce Industry is much attractive for the Consumers” References 1. Rebirth of E-Commerce in India by Milan Sheth (Ernst & Young Pvt. Ltd) 2. Ernst & Young Report 2012: Rebirth of e-commerce in India 3. Google India Study Report combining data from Google Trends and online research conducted by TNS Australia 4. The Boston Consulting Group Report: From Buzz to Bucks: Capitalizing on India's Digitally Influenced consumers 5. http://www.iamwire.com/2012/04/india-to-be-the-fastest-growing-e-commerce-market-in-asia-pacific- market-set-to-grow-to-8-8-billion-by-2016/ 6. http://in.myinfoline.com/forum/reply/2065 7. http://articles.timesofindia.indiatimes.com/2013-04-26/internet/38842529_1_indian-internet-internet- shopping-internet-penetration

- 17. 8. www.zdnet.com/.../india-e-commerce-industry-faces-consolidation-7000... 9. http://indiaranker.com/websites/ecommerce 10. http://www.ibm.com/news/in/en/2012/12/17/j586238s98768m83.html 11. http://articles.economictimes.indiatimes.com/2013-11-24/news/44412771_1_e-commerce-space-marketplace- model-cent-fdi 12. http://www.business-standard.com/article/economy-policy/government-plans-to-allow-fdi-in-e-commerce- before-april-113123000754_1.html 13. IBEF Report on E-Commerce 14. ASSOCHAM Report on E- Commerce 15. http://articles.economictimes.indiatimes.com/2013-11-04/news/43658867_1_indiatimes-shopping-flipkart- courier-companies 16. http://www.mxmindia.com/2013/12/40-preferred-cod-in-their-online-diwali-shopping- iamai/#sthash.VlYNoC8R.dpuf 17. http://articles.economictimes.indiatimes.com/2014-03-28/news/48662657_1_lowe-lintas-advertising-agency- happy-creative-services 18. http://www.digit.in/internet/e-commerce-vs-brands-a-serious-conflict-23040.html 19. http://articles.economictimes.indiatimes.com/2014-05-26/news/50098927_1_idg-ventures-india-tiger-global- lee-fixel Article by : Alvis Lazarus Social Entrepreneur | Award Winning 'Supply Chain Consultant' | Ex India Head Supply Chain Ops at Flipkart.com Bengaluru, Karnataka, India Logistics and Supply Chain Current 1. My One Tenth, 2. Infollion Research Services Pvt. Ltd., 3. Guidepoint Global Advisors Previous1. Flipkart.com, 2. 3M, 3. CATERPILLAR Education1. Indian Institute of Management, Calcutta International Supply Chain Education Alliance - SCNext India, Pune nikhil.oswal@scnext.org www.scnext.org/countries/india Connect with us on