QNBFS Daily Market Report March 20, 2019

•

1 gefällt mir•128 views

The QE Index declined 0.2% to close at 9,957.0. Losses were led by the Real Estate and Banks & Financial Services indices, falling 4.1% and 0.9%, respectively.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie QNBFS Daily Market Report March 20, 2019

Ähnlich wie QNBFS Daily Market Report March 20, 2019 (20)

Mehr von QNB Group

Mehr von QNB Group (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

QNBFS Daily Market Report March 20, 2019

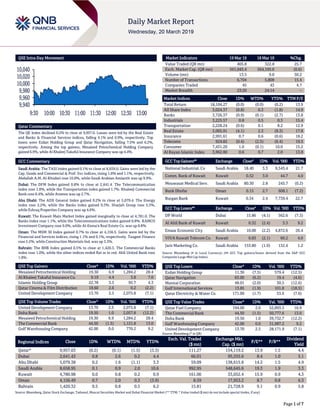

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QE Index declined 0.2% to close at 9,957.0. Losses were led by the Real Estate and Banks & Financial Services indices, falling 4.1% and 0.9%, respectively. Top losers were Ezdan Holding Group and Qatar Navigation, falling 7.5% and 6.2%, respectively. Among the top gainers, Mesaieed Petrochemical Holding Company gained 6.9%, while Al Khaleej Takaful Insurance Company was up 4.4%. GCC Commentary Saudi Arabia: The TASI Index gained 0.1% to close at 8,659.0. Gains were led by the Cap. Goods and Commercial & Prof. Svc indices, rising 1.8% and 1.1%, respectively. Abdullah A.M. Al-Khodari rose 10.0%, while Saudi Arabian Amiantit was up 9.9%. Dubai: The DFM Index gained 0.8% to close at 2,641.4. The Telecommunication index rose 1.8%, while the Transportation index gained 1.7%. Khaleeji Commercial Bank rose 8.4%, while Aramex was up 2.7%. Abu Dhabi: The ADX General Index gained 0.2% to close at 5,079.4. The Energy index rose 2.2%, while the Banks index gained 0.3%. Sharjah Group rose 5.3%, while Eshraq Properties Company was up 4.6%. Kuwait: The Kuwait Main Market Index gained marginally to close at 4,781.0. The Banks index rose 1.1%, while the Telecommunications index gained 0.8%. KAMCO Investment Company rose 9.0%, while Al-Enma'a Real Estate Co. was up 8.8%. Oman: The MSM 30 Index gained 0.7% to close at 4,156.5. Gains were led by the Financial and Services indices, rising 1.1% and 0.1%, respectively. Taageer Finance rose 5.2%, while Construction Materials Ind. was up 3.3%. Bahrain: The BHB Index gained 0.5% to close at 1,420.3. The Commercial Banks index rose 1.0%, while the other indices ended flat or in red. Ahli United Bank rose 1.8%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochemical Holding 19.30 6.9 1,284.2 28.4 Al Khaleej Takaful Insurance Co. 9.19 4.4 3.8 7.0 Islamic Holding Group 22.78 3.5 95.7 4.3 Qatar Cinema & Film Distribution 18.60 2.6 0.2 (2.2) United Development Company 13.70 2.5 2,075.8 (7.1) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% United Development Company 13.70 2.5 2,075.8 (7.1) Doha Bank 19.50 1.0 2,057.8 (12.2) Mesaieed Petrochemical Holding 19.30 6.9 1,284.2 28.4 The Commercial Bank 44.50 (1.5) 1,121.8 13.0 Gulf Warehousing Company 42.00 0.0 770.2 9.2 Market Indicators 19 Mar 19 18 Mar 19 %Chg. Value Traded (QR mn) 405.8 322.8 25.7 Exch. Market Cap. (QR mn) 561,045.4 564,195.0 (0.6) Volume (mn) 13.5 9.0 50.2 Number of Transactions 6,704 5,808 15.4 Companies Traded 45 43 4.7 Market Breadth 23:20 24:14 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,104.27 (0.0) (0.0) (0.2) 13.9 All Share Index 3,024.37 (0.8) 0.3 (1.8) 14.9 Banks 3,726.37 (0.9) (0.1) (2.7) 13.8 Industrials 3,225.57 0.8 0.5 0.3 15.4 Transportation 2,228.24 (0.6) 0.1 8.2 12.9 Real Estate 2,005.91 (4.1) 2.3 (8.3) 17.8 Insurance 2,991.61 0.7 0.6 (0.6) 18.2 Telecoms 924.82 (0.4) (2.5) (6.4) 19.5 Consumer 7,431.20 1.0 (0.1) 10.0 15.2 Al Rayan Islamic Index 3,962.80 0.6 0.7 2.0 13.8 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% National Industrial. Co Saudi Arabia 18.40 3.3 9,545.4 21.7 Comm. Bank of Kuwait Kuwait 0.52 3.0 44.7 4.0 Mouwasat Medical Serv. Saudi Arabia 80.30 2.8 245.7 (0.2) Bank Dhofar Oman 0.15 2.7 608.1 (7.2) Burgan Bank Kuwait 0.34 2.4 7,739.4 22.7 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% DP World Dubai 15.86 (4.1) 562.6 (7.3) Al Ahli Bank of Kuwait Kuwait 0.32 (2.4) 3.3 9.2 Emaar Economic City Saudi Arabia 10.00 (2.2) 4,872.6 26.4 VIVA Kuwait Telecom Co. Kuwait 0.83 (2.1) 60.2 4.0 Jarir Marketing Co. Saudi Arabia 153.80 (1.9) 132.4 1.2 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 11.36 (7.5) 579.4 (12.5) Qatar Navigation 63.00 (6.2) 19.4 (4.6) Mannai Corporation 48.01 (2.0) 30.5 (12.6) Gulf International Services 13.85 (1.9) 101.8 (18.5) Qatar Electricity & Water Co. 171.00 (1.7) 53.6 (7.6) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% Qatar Fuel Company 194.00 2.0 52,893.5 16.9 The Commercial Bank 44.50 (1.5) 50,777.6 13.0 Doha Bank 19.50 1.0 39,732.7 (12.2) Gulf Warehousing Company 42.00 0.0 31,987.2 9.2 United Development Company 13.70 2.5 28,171.9 (7.1) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,957.03 (0.2) (0.1) (1.5) (3.3) 111.27 154,119.2 13.9 1.5 4.4 Dubai 2,641.43 0.8 2.6 0.2 4.4 66.01 95,555.6 8.4 1.0 5.1 Abu Dhabi 5,079.38 0.2 1.6 (1.1) 3.3 59.09 138,615.8 14.2 1.5 4.9 Saudi Arabia 8,658.95 0.1 0.9 2.0 10.6 992.95 548,645.6 19.3 1.9 3.3 Kuwait 4,780.98 0.0 0.8 0.2 0.9 161.00 33,052.4 15.9 0.9 4.3 Oman 4,156.49 0.7 2.0 0.3 (3.9) 8.59 17,953.2 8.7 0.8 6.3 Bahrain 1,420.32 0.5 0.8 0.5 6.2 15.81 21,728.9 9.1 0.9 5.8 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,940 9,960 9,980 10,000 10,020 10,040 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE Index declined 0.2% to close at 9,957.0. The Real Estate and Banks & Financial Services indices led the losses. The index fell on the back of selling pressure from Qatari and GCC shareholders despite buying support from non-Qatari shareholders. Ezdan Holding Group and Qatar Navigation were the top losers, falling 7.5% and 6.2%, respectively. Among the top gainers, Mesaieed Petrochemical Holding Company gained 6.9%, while Al Khaleej Takaful Insurance Company was up 4.4%. Volume of shares traded on Tuesday rose by 50.2% to 13.5mn from 9.0mn on Monday. Further, as compared to the 30-day moving average of 10.1mn, volume for the day was 34.0% higher. United Development Company and Doha Bank were the most active stocks, contributing 15.3% and 15.2% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 4Q2018 % Change YoY Operating Profit (mn) 4Q2018 % Change YoY Net Profit (mn) 4Q2018 % Change YoY Zahrat Al Waha for Trading Co.* Saudi Arabia SR 488.5 15.7% 53.0 -17.0% 34.7 -26.1% Sadara Chemical Company* Saudi Arabia SR 13,115.4 75.2% -1,478.3 – -3,860.0 – Yanbu Cement Co.* Saudi Arabia SR 767.1 -16.3% 94.9 -69.7% 91.2 -71.4% Electrical Industries Co. * Saudi Arabia SR 705.9 -18.8% 29.3 -60.3% 7.1 -87.6% Eastern Province Cement Co.* Saudi Arabia SR 566.0 -11.7% 69.0 -30.3% 70.0 -34.6% Savola Group* Saudi Arabia SR 21,814.6 -8.5% 277.0 -65.5% -520.4 – Nama Chemicals Co. * Saudi Arabia SR 624.3 4.3% 62.2 208.3% 35.3 – Source: Company data, DFM, ADX, MSM, TASI, BHB. (*Financials for FY2018) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 03/19 UK UK Office for National Statistics Jobless Claims Change February 27.0k – 15.7k Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 4Q2018 results No. of days remaining Status MRDS Mazaya Qatar Real Estate Development 20-Mar-19 0 Due AKHI Al Khaleej Takaful Insurance Company 25-Mar-19 5 Due QFBQ Qatar First Bank 27-Mar-19 7 Due QGMD Qatari German Company for Medical Devices 27-Mar-19 7 Due ZHCD Zad Holding Company 30-Mar-19 10 Due Source: QSE Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 25.01% 38.17% (53,385,714.92) Qatari Institutions 45.88% 33.83% 48,885,901.14 Qatari 70.89% 72.00% (4,499,813.78) GCC Individuals 0.62% 0.57% 201,723.66 GCC Institutions 0.43% 1.60% (4,725,955.16) GCC 1.05% 2.17% (4,524,231.50) Non-Qatari Individuals 6.51% 10.99% (18,166,400.55) Non-Qatari Institutions 21.54% 14.84% 27,190,445.83 Non-Qatari 28.05% 25.83% 9,024,045.28

- 3. Page 3 of 7 News Qatar IGRD's bottom line rises ~162% YoY and ~225% QoQ in 4Q2018 – Investment Holding Group's (IGRD) net profit rose ~162% YoY (~+225% QoQ) to ~QR27mn in 4Q2018. In FY2018, IGRD reported net profit of QR58.4mn compared to QR40.7mn in FY2017. EPS increased to QR0.70 in FY2018 from QR0.49 in FY2017. The board of directors recommended distribution of 2.5% of the company’s share capital as cash dividends to the shareholders. (QSE) QIBK completes successful issuance of $750mn Sukuk – Qatar Islamic Bank (QIBK), rated ‘A1/A-/A’ (all ‘Stable’) by Moody’s/Standard & Poor's/Fitch, successfully priced $750mn five-year Sukuk at par with a profit rate of 3.982% (equivalent to a credit spread of 150bps over USD Mid-Swaps). The Sukuk was met with strong investor demand as evidenced by the large order-book which closed at $3.1bn, representing an oversubscription rate of 4.1 times. In terms of geography, 46% of the Sukuk was allocated to Asian investors, followed by Middle Eastern accounts (23%), Europe (21%) and US/other (10%). In total, non-Middle Eastern investors were allocated 77% of the Sukuk, which is a remarkable outcome and one of the highest international allocations achieved by any bank from the region. Of the total, 60% of the investors were fund managers, 26% were banks & private banks and 14% were insurance companies & agencies. More than 140 investors from 28 countries spanning Europe, Asia, US and the Middle East participated in the Sukuk. Barclays, Barwa Bank, Boubyan Bank, Crédit Agricole CIB, QInvest, QNB Capital and Standard Chartered Bank acted as joint lead managers & book-runners on this transaction, with Deutsche Bank as a co-manager. The $750mn Sukuk was a drawdown under QIBK's existing $4bn program and the Trust Certificates will be listed on the Irish Stock Exchange. (QSE) AHCS appoints Sheikh Mohamed bin Faisal Al Thani as CEO – Aamal Company (AHCS) announced the board of directors’ decision of February 26, 2019 to appoint Sheikh Mohamed bin Faisal Al Thani as the CEO of the company. In addition, Sheikh Mohamed will continue to serve in his current position as AHCS’ Managing Director. (QSE) CEO: Nakilat all set to expand fleet to serve new customers; approves cash dividend of QR1 per share – Qatar Gas Transport Company Limited (Nakilat) is all prepared to acquire any number of new vessels to serve new customers once Qatar’s LNG production capacity will increase 43% to 110mn tons per annum (MTPA), the company’s CEO, Abdullah Al Sulaiti said. Al Sulaiti said, “It is for Qatar Petroleum (QP) to decide about the number of new vessels it will require to transport additional LNG to new customers. Once QP places orders with us, we will acquire the new vessels without any delay.” With a fleet strength of 70 vessels, Al Sulaiti said, Nakilat has one of the world’s largest LNG fleet comprising of 65 LNG carriers, as well as four large LPG carriers and one Floating Storage Regasification Unit (FSRU). According to earlier reports, QP will require as many as 60 large LNG vessels once all the expansion projects are complete. Earlier addressing shareholders at the meeting, Nakilat’s Chairman, Mohammed bin Saleh Al Sada said that Nakilat continued to push boundaries and successfully implemented several long-term growth strategies by strengthening its international presence and diversifying its fleet towards maintaining global leadership in LNG transportation. Meanwhile, Nakilat’s AGM approved the distribution of cash dividend of QR1 per share to shareholders. (Qatar Tribune) BRES launches phase three of Madinat Al Mawater project – Barwa Real Estate Company (BRES) announced the award of the construction of the third phase of Madinat Al Mawater project to the Contractor ‘Hassanesco Trading and Contracting (HCC)’ for a value of QR335mn, with the implementation of this phase to be completed within a period of 18 months. The project embraces a total construction built-up area of around 167,072 square meters. BRES’ Vice Chairman and Managing Director, Issa bin Muhammad Al Muhannadi said that the third phase of Madinat Al Mawater project is considered one of the largest phases of the project to date and is to be built with high quality in the construction and with an integrated infrastructure. (Qatar Tribune) QSE holds workshop for listed companies on investor relations mandatory rules – Qatar Stock Exchange (QSE) held a workshop for listed companies in relation to the forthcoming introduction of a mandatory IR (investor relations) Rules regime. QSE has invested in a number of initiatives in the area of IR over recent years and this represents a further commitment to best practice in Qatar. Feedback from local and international investors suggested that Qatari listed companies are making significant strides in this area, but QSE recognizes the need for continuing improvement since good IR has knock-on effects in terms of valuation, liquidity and ultimately trust in the Qatari market. In relation to the IR Rules, QSE’s CEO, Rashid Mansoori said, “The existing disclosure rules are based on regional best practice and Qatari companies clearly meet these regulatory standards. What we are talking about is doing more than the regulatory minimum which is an important differentiating factor for emerging markets.” The IR Rules consist of a number of base line provisions in the QSE Rulebook and further requirements published in February. In summary, as from October 1, 2019, each company listed on QSE will be required to (i) Appoint an Investor Relations Officer, (ii) Create and maintain a dedicated investor relations section on its website, and (iii) Publish an investor presentation and hold at least one investor conference call after publication of its annual, semi-annual and quarterly reports. (QSE) MERS announces date for dividends distribution to shareholders – Al Meera Consumer Goods Company (MERS) announced that starting from March 19, 2019, dividends for the financial year ended December 31, 2018 will be distributed as per the shareholders list as on March 17, 2019, as provided by the Qatar Central Securities Depository. (QSE) ERES’ EGM endorses items on its agenda – Ezdan Holding Group (ERES) announced that the Extraordinary General Assembly (EGM) meeting was held on March 18, 2019 and the company’s EGM endorsed items on its agenda. (QSE) Qatar hosts global launch of world’s first Islamic digital e- token, ‘iDinar’ – Qatar hosted the global launch of ‘iDinar’, the world’s first Islamic digital e-token platform, on the sidelines of

- 4. Page 4 of 7 the ‘5th Doha Islamic Finance Conference’ held in Doha. The iDinar platform is a block-chain based e-token, in which initial value of one Dinar e-token is backed by 1gm of physical gold, Ibadah Inc’s Executive Chairman, Faidzan Hassan said on the sidelines of the launch event. He said, “The iDinar allows the advantages offered by block-chain in terms of confidentiality and ease of transfer, among others. As an exchange, we have what we call a ‘hybrid’ exchange, which is based on barter trading that is Shari’ah-compliant. As a digital exchange, transactions run on real time. Ibadah also offers a market place to be able to trade stocks, shares, bonds, and Sukuk, among others, as well as commodities like gold.” The digital iDinar e- token serves not only as a form of digitalized gold investment portfolio, but also the advances in current block-chain technology enables the iDinar e-token to be used as a value transference and settlement denominator for exchange, trading, and payment settlements. According to Ibadah’s Spokesperson, Abbas Ali, through its incorporated company in Qatar, Ibadah has been given principal approval by Qatar Financial Centre (QFC) to operate the ‘iDinar eXchange’, a multi-product digital trading platform which trades the iDinar with and against other commodities, financial instruments and products, as well as major fiat currencies globally. (Gulf- Times.com) Qatar to launch ‘Energy Bank’ with targeted $10bn capital – Qatar will launch an ‘Energy Bank’ with a targeted capital of $10bn to fund hydrocarbon-centric projects across the world, a move that will make Doha a leading player across verticals in the global oil and gas industry. Qatar Financial Centre (QFC)- based bank, which already has got commitments to the tune of $2bn from international investors (of the $2.5bn paid up), will progressively scale up its capital base to become the world’s largest Islamic lending institution. It is expected to be operational by the fourth quarter of this year. The lender, which is planning to have representative offices in the Middle East and North Africa region and other parts of the world, will specialize in funding projects related to oil and gas, petrochemicals and renewable energy. It will offer competitive and innovative products, corporate and project financing, as well as asset management services. (Gulf-Times.com) Data drives Ooredoo’s nearly QR30bn revenue in 2018; shareholders approve cash dividend of QR2.5 per share – Driven mainly by Ooredoo’s two major markets, Qatar and Indonesia, data revenue contributed QR14.2bn, or 47%, of the group’s total revenue in 2018, Chairman Sheikh Abdulla bin Mohamed bin Saud Al-Thani said. Ooredoo Group earned total revenue of nearly QR29.9bn last year with most of its companies showing robust performance with growth in data business. Addressing the shareholders, Sheikh Abdulla said Ooredoo’s continued support to businesses, SMEs and government was reflected in its B2B revenues, which stood at QR5.2bn in 2018. The Chairman announced that Ooredoo will soon be offering surprise 5G services to its subscribers, which will take effect from the upcoming Emir’s Cup until the FIFA World Cup 2022. The shareholders adopted the Ooredoo’s board of directors recommendation to distribute 25% (of the nominal share value) dividend for 2018, which translates into QR2.5 per share. (Gulf- Times.com, Peninsula Qatar) Qatar’s IPI rises 1.5% MoM in January 2019 – Qatar’s Industrial Production Index (IPI) reached 107.2 points in January 2019, an increase by 1.5% compared to the previous month (December 2018), according to data released by Planning and Statistics Authority (PSA). On YoY basis, the IPI of January 2019 increased by 0.6%. The mining and quarrying index, which has a relative weight of 83.6%, showed an increase of 1.8% in January compared to the previous month, due to the increase in the quantities of crude oil and natural gas by 1.8%. The IPI of mining increased 0.9% YoY. (Qatar Tribune) Commerce Minister: Qatar is the fifth largest Islamic finance market – The Minister of Commerce and Industry, HE Ali bin Ahmed Al Kuwari said Qatar is the fifth largest Islamic finance market with bank assets of around $120bn at a growth rate of over 10%. He said this during a speech at the opening of the fifth Doha Islamic Finance Conference. He said as one of the fastest growing sectors in the country, the Islamic finance industry has witnessed remarkable international and domestic growth. Today, Islamic banking assets account for more than 26% of Qatar’s banking system and Qatar’s Islamic banks are among the largest Islamic banks in the world. The Minister said Islamic banks in Qatar are an important element in the Islamic finance market. In recent years, the State has established ambitious plans to strengthen its capabilities by encouraging it to offer various Islamic financial products and services by taking advantage of the promising opportunities offered by major infrastructure projects being implemented within the framework of Qatar National Vision 2030 and the 2022 FIFA World Cup. Financial technology has played an important role in the development of Islamic finance and its position in the global market, despite various risks and challenges associated with this trend. (Qatar Tribune) Non-Qatari property ownership areas identified – Non-Qataris can have freehold ownership of property in 10 areas, while 16 areas have been identified where they can use real estate for 99 years. This comes in implementation of Law No. 16 of 2018 on the regulation of non-Qatari ownership and use of real estate. The areas where non-Qataris can use real estate for 99 years are: Msheireb (Area 13), Fereej Abdelaziz (14), Doha Al Jadeed (15), New Al Ghanim (16), Al Refaa and Old Al Hitmi (17), Aslata (18), Fereej Bin Mahmoud (22), Fereej Bin Mahmoud (23), Rawdat Al Khail (24), Mansoura and Fereej Bin Dirham (25), Najma (26), Umm Ghuwailina (27), Al Khulaifat (28), Al Sadd (38), Al Mirqab Al Jadeed and Fereej Al Nasr (39) and the Doha International Airport area (48). HE the Minister of Justice and Acting Minister of State for Cabinet Affairs, Issa bin Saad Al-Jafali Al-Nuaimi said the freehold ownership areas are: West Bay (Area 66), The Pearl-Qatar (66), Al Khor Resort (74), Rawdat Al Jahaniyah (investment area), Al Qassar (administrative area 60), Al Dafna (administrative area 61), Onaiza (administrative area 63), Al Wasail (69), Al Khraij (69) and Jabal Theyleeb (69). These areas offer 100% guaranteed return on investment and will represent a new investment model not only in Qatar, but also in the region and the world, as these areas combine capital development and promote cultural co-existence between developers, owners and investors, given their architectural symbolism that combines different world cultures, QNA, citing a statement from the Minister, stated. (Gulf-Times.com)

- 5. Page 5 of 7 Qatar Chamber discusses ways to improve business environment in private education – Qatar Chamber’s education and health committees have held separate meetings to discuss ways to facilitate access to licenses for new medical facilities and mechanisms to support investment in education. During its meeting, the Health Committee called for the need to overcome all obstacles that may face employers in the field of health, and to determine the required standards and prices of medical services with the need to adhere to the quality of services. On the other hand, the Education Committee discussed a number of issues related to the field of education, including the criteria for accreditation of some certificates, student upgrading systems, mechanisms and methodology for determining school fees, the role of the Ministry of Education in supporting and encouraging Qatari investors, supporting schools, and the mechanisms of collecting fees from students to maintain financial flows for the smooth functioning of the educational process. (Gulf- Times.com) International US manufacturing sector slowing as economy loses steam – US manufacturing output fell for a second straight month in February and factory activity in New York state hit nearly a two-year low this month, offering further evidence of a sharp slowdown in economic growth early in the first quarter. The Fed stated manufacturing production dropped 0.4% last month, held down by declines in the output of motor vehicles, machinery and furniture. Data for January was revised up to show output at factories falling 0.5% instead of slumping 0.9% as previously reported. It was the first back-to-back decline since mid-2017. Economists polled by Reuters had forecasted manufacturing output rising 0.3% in February. Production at factories increased 1.0% in February from a year ago. Manufacturing accounts for about 12% of the economy. (Reuters) UK’s employers defy approach of Brexit with hiring spree – British employers ramped up their hiring at the fastest pace since 2015 in the three months to January as the labor market defied broader Brexit weakness in the overall economy. The number of people in work increased by 222,000, helping to push the unemployment rate down to its lowest since the start of 1975 at 3.9%, official data showed. The increase in hiring was stronger than all forecasts in a Reuters poll of economists and pushed the proportion of the population in work to an all-time high. (Reuters) German investors cheered by hopes of Brexit delay, trade progress – The mood among German investors improved by much more than expected in March, a survey by the ZEW research institute showed, as a potential delay to Britain’s departure from the European Union buoyed sentiment. The ZEW research institute stated its monthly survey showed economic sentiment among investors rose to -3.6 from -13.4 in February. Economists had expected an increase to -11.0. A separate gauge measuring investors’ assessment of the economy’s current conditions dipped to 11.1 from 15.0 in the previous month. Markets had predicted a fall to 11.7. The stronger-than-expected ZEW reading bucked a recent run of weak data on the German economy, Europe’s largest, which stalled in the final quarter of last year, just skirting recession. (Reuters) German economic advisors slash 2019 growth forecast to 0.8% – A panel of advisers to the German government slashed its growth forecast for this year to 0.8% and warned risks related to Britain’s departure from the European Union, trade disputes and a sharper than expected slowdown in China remained high. The group that advises the German government on economic policy had in November forecast that Europe’s largest economy would expand by 1.5% this year. The panel stated economic growth had slowed significantly, partly due to problems in the chemical and auto sectors and warned that a spiral of protectionist measures had the potential to push the economy into recession. The group predicted the economy would grow by 1.7% in 2020. (Reuters) INSEE: French growth seen firming as impact of protests wanes – French quarterly growth will firm in the first half the year as consumer spending benefits from improving household incomes and recovering business confidence after protests at the end of last year, the INSEE statistics agency stated. The Eurozone’s second-biggest economy is set to post growth of 0.4% in both the first and second quarters, up from 0.3% in the final three months of last year, INSEE forecasted in its quarterly economic outlook. The economy would have grown 0.4% at the end of last year as well if it were not for the impact of the yellow vest anti-government unrest, which INSEE estimated at 0.1 percentage point. INSEE stated higher incomes would help consumer spending rebound 0.5% in the first quarter after flat lining at the end of last year in the face of the unrest, which forced many stores in central Paris to be boarded up during the peak holiday shopping period. (Reuters) French Finance Minister cuts 2019 growth forecast to 1.4% – The French economy should grow about 1.4% this year, Finance Minister Bruno Le Maire said, revising down the forecast of 1.7% growth in this year’s budget. Le Maire told the Senate’s law and economic affairs commissions that the yellow vest anti-government unrest had in the short-term trimmed 0.2 percentage points off growth in 2018 and 2019. “Growth should be about 1.4% in 2019, a number that I will confirm when the stability program is presented,” Le Maire said. The government usually updates its growth estimate in April when it sends its annual stability program to the European Commission. (Reuters) Japan’s factory mood hits weakest since 2016 as trade rifts bite – Confidence among Japanese manufacturers hit its weakest in two-and-a-half years in March, a Reuters poll showed, as global trade friction fuelled concerns that a postwar record growth cycle driven by Abenomics may be over. The monthly poll, which tracks the Bank of Japan’s (BoJ) closely watched tankan quarterly survey, found confidence fell for a fifth straight month while sentiment in the service sector held steady, suggesting domestic demand is unlikely to offset external risks such as the trade war and China’s slowdown. Both manufacturers’ and service-sector morale is expected to rise just slightly over the coming three months, underscoring a bumpy road ahead for the world’s third largest economy, according to the Reuters Tankan. The BoJ’s last tankan out in December found the business mood held steady from three

- 6. Page 6 of 7 months ago, but business conditions were seen worsening ahead amid trade war and slowdown in China. (Reuters) Regional Saudi Arabia will spend $23bn to improve living in Riyadh – Saudi Arabia stated that it will spend $23bn to boost the quality of life in the capital Riyadh, increasing green space and recreational areas and installing 1,000 works of art across the city. The four projects unveiled are part of efforts to open up Saudi Arabians’ cloistered lifestyles, encourage physical activity and make life more fun in the conservative Kingdom, alongside reforms to diversify the economy away from oil. They are the latest in a series of planned development investments that King Salman has launched at the side of his son, Crown Prince Mohammed bin Salman. (Reuters) Saudi Arabia’s consumer prices fall for second straight month in February – Saudi Arabia’s annual Consumer Price Index (CPI) fell for a second straight month in February, signaling a deflationary environment in the Arab world’s biggest economy. The CPI for February fell 2.2% from a year earlier, as prices for housing, water and energy all dropped, government data showed. The index fell 0.2% from January, according to data from the General Authority for Statistics. In January, it dropped 1.9% from a year earlier, the first decline since 2017, as the effect faded of last year’s implementation of a value-added tax. In February, the housing, water, electricity and fuel component of the index dropped 8.2% from a year earlier. Clothing and footwear slid 1.2%. The restaurant and hotel category rose 1.5% and education went up 1.2% from a year earlier. “A key factor for the deflationary outlook for 2019 is the fall in rental prices, which is dragging down the housing and utility sub- component of the inflation basket,” Chief Economist at Abu Dhabi Commercial Bank, Monica Malik said. ADCB has projected 0.9% drop in CPI in 2019. (Reuters) Saudi Arabia’s new rules set to raise Islamic tax for some banks – Saudi Arabia has set out new rules for the calculation of an Islamic tax on banks that will result in them paying between 10% - 20% of net profit. The General Authority of Zakat & Tax set limits for the taxable asset base of between four times and eight times net profit, according to a statement. That is equivalent to a corridor of between 10% and 20% of net income, Bloomberg Intelligence Analyst, Edmond Christou said. Most of the Kingdom’s major banks will end up paying the lower limit, he wrote in a note. Saudi Arabia was in talks with local banks to increase the tax rate to as high as 20% of net income, Bloomberg News reported. The tax authority denied it has plans to raise the levy. The current rate is 10% after deducting returns on government bonds. Major banks in Saudi Arabia reached settlements worth a combined $4.5bn with the tax authority in December, ending a dispute over accounts stretching back as far as 2002 in some cases. (Gulf-Times.com) ACWA Power buys Marubeni's stakes in Saudi Arabian energy and water plant – ACWA Power bought partner Marubeni’s holdings in Saudi Arabian facility that generates power and desalinates seawater, ACWA stated. Saudi Arabian based ACWA Power bought Marubeni’s 37% stake in 840 MW Rabigh Arabian Water & Electricity Company, doubling ACWA’s holding to 74% in company known as RAWEC. ACWA also bought Marubeni’s 34% holding in Rabigh Power Company, which provides services to RAWEC. RAWEC, on Saudi Red Sea coast, provides power, water and steam to Petro Rabigh refining and petrochemical business, a JV between Saudi Aramco and Japan’s Sumitomo Chemical. Financial terms are not included in the statement. (Bloomberg) Blackstone-backed GEMS to bid for top Saudi Arabian school chain – GEMS Education, the Dubai-based school operator backed by Blackstone Group LP, is in advanced talks to invest in Saudi Arabia’s Maarif for Education & Training chain of schools, according to sources. The deal for the largest owner and operator of private schools in the Kingdom could be worth about $400mn, sources said. Samba Capital is advising the owners who are seeking to sell all or part of the company, sources added. A final decision has not been made and the company’s plans could change, they said. Maarif, owned by the Al Blehed family, runs more than 100 schools across the Kingdom, offering Arabic and internationally recognized curriculums. Under Vision 2030, Saudi Arabia is encouraging private-sector participation in education, as it seeks to wean the economy off oil. Saudi Arabian schools will require over 1mn additional seats in Grades 1-12 by 2020, of which 150,000 should come from around 800 new private schools, according to a report by PwC Middle East. (Bloomberg) RAK Bank said to weigh bond sale to help refinance debt – National Bank of Ras Al Khaimah is considering selling bonds to refinance existing debt, according to sources. The bank is talking to lenders about a possible sale, but has not decided whether to proceed with a deal, sources said. The company has about $700mn of bonds maturing in June, according to data compiled by Bloomberg. RAK Bank is considering a number of options to replace a part or all of its bonds and discussions are underway with various parties, an official at the bank said. (Bloomberg) Indian-Omani group strikes $3.85bn deal to build Sri Lanka oil refinery – India’s Accord Group and Oman’s Ministry of Oil and Gas have signed a $3.85bn deal to build an oil refinery in Sri Lanka, the biggest single pledge of foreign direct investment ever made in the country. The deal represents a challenge to China, which had until recently been on track to be the dominant foreign investor on the island, and a possible coup for India. Sri Lankan officials said the 200,000 bpd refinery will be built on 585 acres near the site of the new Hambantota international port and a related industrial zone on the nation’s southern coast. The refinery, construction of which is expected to begin on March 24 and be completed in 44 months, is set to produce 9mn metric tons of refined products a year for export from the Hambantota port, which serves the busiest East-West shipping route. Privately owned Accord Group will control 70% of the joint venture and the Sultanate of Oman’s Ministry of Oil and Gas the rest. (Reuters) Oman sells OMR75mn 28-day bills at yield 2.473%; bid-cover at 1.07x – Oman sold OMR75mn of bills due on April 17, 2019 on March 18, 2019. Investors offered to buy 1.07 times the amount of securities sold. The bills were sold at a price of 99.811, having a yield of 2.473% and will settle on March 20, 2019. (Bloomberg)

- 7. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mehmet Aksoy, PhD QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mehmet.aksoy@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNB FS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNB FS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNB FS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNB FS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNB FS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNB FS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNB FS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNB FS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNB FS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNB FS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Feb-15 Feb-16 Feb-17 Feb-18 Feb-19 QSE Index S&P Pan Arab S&P GCC 0.1% (0.2%) 0.0% 0.5% 0.7% 0.2% 0.8% (0.5%) 0.0% 0.5% 1.0% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,306.56 0.2 0.3 1.9 MSCI World Index 2,120.43 0.1 0.6 12.6 Silver/Ounce 15.37 0.2 0.5 (0.8) DJ Industrial 25,887.38 (0.1) 0.1 11.0 Crude Oil (Brent)/Barrel (FM Future) 67.61 0.1 0.7 25.7 S&P 500 2,832.57 (0.0) 0.4 13.0 Crude Oil (WTI)/Barrel (FM Future) 59.03 (0.1) 0.9 30.0 NASDAQ 100 7,723.95 0.1 0.5 16.4 Natural Gas (Henry Hub)/MMBtu 2.93 1.0 0.7 (9.8) STOXX 600 384.29 0.8 1.1 12.8 LPG Propane (Arab Gulf)/Ton 67.88 (0.4) (0.7) 6.1 DAX 11,788.41 1.4 1.2 10.8 LPG Butane (Arab Gulf)/Ton 68.13 (0.9) (1.1) (2.0) FTSE 100 7,324.00 0.6 1.2 13.3 Euro 1.14 0.1 0.2 (1.0) CAC 40 5,425.90 0.5 0.7 13.7 Yen 111.39 (0.0) (0.1) 1.5 Nikkei 21,566.85 (0.0) 0.6 6.8 GBP 1.33 0.1 (0.2) 4.0 MSCI EM 1,070.95 0.2 1.3 10.9 CHF 1.00 0.2 0.3 (1.8) SHANGHAI SE Composite 3,090.98 (0.2) 2.3 27.0 AUD 0.71 (0.2) 0.0 0.6 HANG SENG 29,466.28 0.2 1.6 13.8 USD Index 96.38 (0.1) (0.2) 0.2 BSE SENSEX 38,363.47 0.1 0.8 7.4 RUB 64.39 0.0 (0.6) (7.6) Bovespa 99,588.37 0.1 1.6 16.2 BRL 0.26 0.1 0.7 2.4 RTS 1,219.78 0.5 1.9 14.1 99.2 93.1 82.5