QNBFS Daily Market Report February 14, 2019

•

0 gefällt mir•107 views

The QE Index declined 1.2% to close at 10,180.7. Losses were led by the Real Estate and Industrials indices, falling 3.6% and 1.5%, respectively.

Empfohlen

Empfohlen

Weitere ähnliche Inhalte

Was ist angesagt?

Was ist angesagt? (20)

Ähnlich wie QNBFS Daily Market Report February 14, 2019

Ähnlich wie QNBFS Daily Market Report February 14, 2019 (20)

Mehr von QNB Group

Mehr von QNB Group (20)

Kürzlich hochgeladen

Kürzlich hochgeladen (20)

QNBFS Daily Market Report February 14, 2019

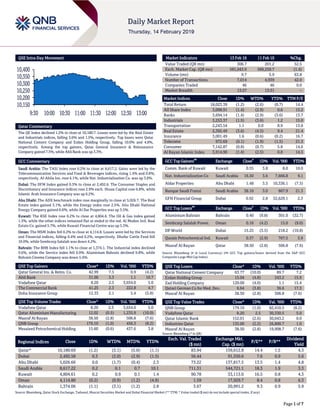

- 1. Page 1 of 7 QSE Intra-Day Movement Qatar Commentary The QE Index declined 1.2% to close at 10,180.7. Losses were led by the Real Estate and Industrials indices, falling 3.6% and 1.5%, respectively. Top losers were Qatar National Cement Company and Ezdan Holding Group, falling 10.0% and 4.8%, respectively. Among the top gainers, Qatar General Insurance & Reinsurance Company gained 7.5%, while Ahli Bank was up 3.3%. GCC Commentary Saudi Arabia: The TASI Index rose 0.2% to close at 8,617.2. Gains were led by the Telecommunication Services and Food & Beverages indices, rising 1.4% and 0.8%, respectively. Al-Ahlia Ins. rose 4.1%, while Nat. Industrialization Co. was up 3.6%. Dubai: The DFM Index gained 0.3% to close at 2,492.6. The Consumer Staples and Discretionary and Insurance indices rose 2.9% each. Shuaa Capital rose 6.8%, while Islamic Arab Insurance Company was up 6.2%. Abu Dhabi: The ADX benchmark index rose marginally to close at 5,026.7. The Real Estate index gained 3.1%, while the Energy index rose 2.5%. Abu Dhabi National Energy Company gained 6.6%, while Al Dar Properties was up 3.5%. Kuwait: The KSE Index rose 0.2% to close at 4,804.6. The Oil & Gas index gained 1.3%, while the other indices remained flat or ended in the red. Al Mudon Intl. Real Estate Co. gained 5.7%, while Kuwait Financial Centre was up 5.3%. Oman: The MSM Index fell 0.2% to close at 4,114.8. Losses were led by the Services and Financial indices, falling 0.4% and 0.2%, respectively. Dhofar Cattle Feed fell 10.0%, while Sembcorp Salalah was down 4.2%. Bahrain: The BHB Index fell 1.1% to close at 1,374.1. The Industrial index declined 9.6%, while the Service index fell 0.9%. Aluminium Bahrain declined 9.8%, while Bahrain Cinema Company was down 5.6%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Qatar General Ins. & Reins. Co. 42.99 7.5 0.9 (4.2) Ahli Bank 31.00 3.3 1.1 10.7 Vodafone Qatar 8.20 2.5 3,654.0 5.0 The Commercial Bank 41.25 2.3 222.8 4.7 Doha Insurance Group 12.33 2.1 5.4 (5.8) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Vodafone Qatar 8.20 2.5 3,654.0 5.0 Qatar Aluminium Manufacturing 12.02 (0.5) 1,235.9 (10.0) Masraf Al Rayan 38.50 (2.8) 506.8 (7.6) QNB Group 179.10 (1.0) 456.3 (8.2) Mesaieed Petrochemical Holding 15.60 (0.6) 437.6 3.8 Market Indicators 13 Feb 19 11 Feb 19 %Chg. Value Traded (QR mn) 306.7 201.2 52.5 Exch. Market Cap. (QR mn) 581,043.9 589,250.7 (1.4) Volume (mn) 9.7 5.9 63.8 Number of Transactions 7,014 4,939 42.0 Companies Traded 46 46 0.0 Market Breadth 13:27 13:31 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 18,023.39 (1.2) (2.6) (0.7) 14.4 All Share Index 3,098.91 (1.4) (2.9) 0.6 15.2 Banks 3,694.14 (1.4) (2.9) (3.6) 13.7 Industrials 3,253.37 (1.5) (3.6) 1.2 15.0 Transportation 2,243.54 1.1 0.0 8.9 13.0 Real Estate 2,392.49 (3.6) (4.5) 9.4 21.4 Insurance 3,001.49 1.6 (0.6) (0.2) 16.7 Telecoms 972.69 (0.1) (1.9) (1.5) 21.3 Consumer 7,142.87 (0.8) (0.7) 5.8 14.6 Al Rayan Islamic Index 3,914.90 (1.4) (2.5) 0.8 14.5 GCC Top Gainers ## Exchange Close # 1D% Vol. ‘000 YTD% Comm. Bank of Kuwait Kuwait 0.55 3.8 8.0 10.0 Nat. Industrialization Co Saudi Arabia 16.50 3.6 7,666.8 9.1 Aldar Properties Abu Dhabi 1.48 3.5 10,336.1 (7.5) Banque Saudi Fransi Saudi Arabia 38.10 3.0 867.9 21.3 GFH Financial Group Dubai 0.92 2.8 32,629.1 2.3 GCC Top Losers ## Exchange Close # 1D% Vol. ‘000 YTD% Aluminium Bahrain Bahrain 0.40 (9.8) 301.0 (32.7) Sembcorp Salalah Power. Oman 0.16 (4.2) 15.0 (9.0) DP World Dubai 15.25 (3.5) 218.2 (10.8) Qurain Petrochemical Ind. Kuwait 0.37 (2.9) 767.5 3.9 Masraf Al Rayan Qatar 38.50 (2.8) 506.8 (7.6) Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the S&P GCC Composite Large Mid Cap Index) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Qatar National Cement Company 63.77 (10.0) 89.7 7.2 Ezdan Holding Group 15.04 (4.8) 243.2 15.9 Zad Holding Company 120.00 (4.0) 1.1 15.4 Qatari German Co for Med. Dev. 6.64 (3.8) 36.6 17.3 Masraf Al Rayan 38.50 (2.8) 506.8 (7.6) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 179.10 (1.0) 82,410.5 (8.2) Vodafone Qatar 8.20 2.5 30,330.5 5.0 Qatar Islamic Bank 152.01 (2.6) 30,043.2 0.0 Industries Qatar 135.00 (2.2) 26,800.7 1.0 Masraf Al Rayan 38.50 (2.8) 19,908.7 (7.6) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 10,180.69 (1.2) (3.1) (5.0) (1.1) 83.94 159,612.8 14.4 1.5 4.3 Dubai 2,492.58 0.3 (2.0) (2.9) (1.5) 56.44 91,550.6 7.6 0.9 5.6 Abu Dhabi 5,026.66 0.0 (1.7) (0.4) 2.3 73.22 137,817.5 13.5 1.4 4.8 Saudi Arabia 8,617.22 0.2 0.1 0.7 10.1 711.31 544,721.1 18.3 1.9 3.3 Kuwait 4,804.61 0.2 0.9 0.1 1.4 90.78 33,113.0 16.5 0.8 4.3 Oman 4,114.80 (0.2) (0.9) (1.2) (4.8) 1.59 17,929.7 8.4 0.8 6.3 Bahrain 1,374.06 (1.1) (3.1) (1.2) 2.8 3.67 20,991.2 9.3 0.9 5.9 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Market and Dubai Financial Market (** TTM; * Value traded ($ mn) do not include special trades, if any) 10,150 10,200 10,250 10,300 10,350 10,400 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE Index declined 1.2% to close at 10,180.7. The Real Estate and Industrials indices led the losses. The index fell on the back of selling pressure from non-Qatari shareholders despite buying support from Qatari and GCC shareholders. Qatar National Cement Company and Ezdan Holding Group were the top losers, falling 10.0% and 4.8%, respectively. Among the top gainers, Qatar General Insurance & Reinsurance Company gained 7.5%, while Ahli Bank was up 3.3%. Volume of shares traded on Wednesday rose by 63.8% to 9.7mn from 5.9mn on Tuesday. Further, as compared to the 30-day moving average of 9.2mn, volume for the day was 4.7% higher. Vodafone Qatar and Qatar Aluminium Manufacturing Company were the most active stocks, contributing 37.8% and 12.8% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 4Q2018 % Change YoY Operating Profit (mn) 4Q2018 % Change YoY Net Profit (mn) 4Q2018 % Change YoY Saudi International Petrochemical Saudi Arabia SR 5,035.8 12.9% 1,095.8 17.2% 583.0 33.3% Ekttitab Holding Co. Kuwait KD 288.5 -46.8% -73.3 N/A -586.2 N/A Awtad Dubai AED – – – – -0.6 N/A Emirates Refreshments Dubai AED 48.4 -11.3% -8.2 N/A -7.5 N/A Arabtec Holding Dubai AED 9,853.0 7.8% – – 256.0 108.1% Dubai Nat. Ins. & Reinsurance Dubai AED 351.0 8.5% – – 52.7 5.2% Emaar Malls Dubai AED 4,445.9 22.5% 2,387.0 4.2% 2,229.9 6.9% Marka Dubai AED 76.3 -23.4% -52.4 N/A -76.9 N/A Al Firdous Holdings Dubai AED 1.8 -31.5% -3.4 N/A -5.1 N/A International Holdings Company Abu Dhabi AED 570.2 35.4% 1.0 -93.0% 21.8 -31.1% Abu Dhabi National Insurance Co. Abu Dhabi AED 2,909.5 10.1% – – 235.6 3.7% Foodco Holding Abu Dhabi AED 389.8 21.1% – – 64.7 -2.5% Aldar Properties Abu Dhabi AED 6,286.5 1.7% – – 1,855.8 -7.0% Emirates Telecom Group Company Abu Dhabi AED 52,388.0 1.5% 12,563.0 10.2% 8,615.0 2.4% Emirates Insurance Abu Dhabi AED 1,043.3 -3.2% – – 114.1 4.1% Bahrain Family Leisure Bahrain BHD 1.4 10.2% 0.1 -41.3% -1.0 N/A Bahrain Car Parks Company Bahrain BHD 1.2 9.7% 0.7 -6.9% 0.7 -9.7% Bahrain Flour Mills Company Bahrain BHD 7.1 1.5% – – 1.2 -76.1% Bahrain Duty Free Shop Complex Bahrain BHD 36.4 13.8% -0.7 N/A 7.5 5.3% Source: Company data, DFM, ADX, MSM, TASI, BHB. (*Financials for FY2018) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 02/13 US Mortgage Bankers Association MBA Mortgage Applications 8-February -3.7% – -2.5% 02/13 US Bureau of Labor Statistics CPI MoM January 0.0% 0.1% 0.0% 02/13 US Bureau of Labor Statistics CPI YoY January 1.6% 1.5% 1.9% 02/13 US Bureau of Labor Statistics CPI Core Index SA January 260.7 260.6 260.1 02/13 US Bureau of Labor Statistics CPI Index NSA January 251.7 251.6 251.2 02/13 UK UK Office for National Statistics CPI MoM January -0.8% -0.7% 0.2% 02/13 UK UK Office for National Statistics CPI YoY January 1.8% 1.9% 2.1% 02/13 UK UK Office for National Statistics CPI Core YoY January 1.9% 1.9% 1.9% 02/13 UK UK Office for National Statistics PPI Input NSA MoM January -0.1% 0.2% -1.6% 02/13 UK UK Office for National Statistics PPI Input NSA YoY January 2.9% 3.8% 3.2% 02/13 UK UK Office for National Statistics PPI Output NSA MoM January 0.0% 0.0% -0.3% 02/13 UK UK Office for National Statistics PPI Output NSA YoY January 2.1% 2.2% 2.4% 02/13 UK UK Office for National Statistics PPI Output Core NSA MoM January 0.4% 0.2% 0.1% Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 32.90% 29.86% 9,305,032.99 Qatari Institutions 16.30% 9.58% 20,611,688.74 Qatari 49.20% 39.44% 29,916,721.73 GCC Individuals 0.27% 0.54% (826,863.39) GCC Institutions 4.17% 2.43% 5,347,079.99 GCC 4.44% 2.97% 4,520,216.60 Non-Qatari Individuals 8.46% 8.33% 412,277.42 Non-Qatari Institutions 37.90% 49.27% (34,849,215.75) Non-Qatari 46.36% 57.60% (34,436,938.33)

- 3. Page 3 of 7 Date Market Source Indicator Period Actual Consensus Previous 02/13 UK UK Office for National Statistics PPI Output Core NSA YoY January 2.4% 2.3% 2.4% 02/13 EU Eurostat Industrial Production SA MoM December -0.9% -0.4% -1.7% 02/13 EU Eurostat Industrial Production WDA YoY December -4.2% -3.3% -3.0% 02/13 Japan Bank of Japan PPI YoY January 0.6% 1.0% 1.5% 02/13 Japan Bank of Japan PPI MoM January -0.6% -0.2% -0.6% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 4Q2018 results No. of days remaining Status MPHC Mesaieed Petrochemical Holding Company 14-Feb-19 0 Due QAMC Qatar Aluminum Manufacturing Company 20-Feb-19 6 Due QOIS Qatar Oman Investment Company 20-Feb-19 6 Due MERS Al Meera Consumer Goods Company 24-Feb-19 10 Due QFLS Qatar Fuel Company 25-Feb-19 11 Due BRES Barwa Real Estate Company 25-Feb-19 11 Due QISI The Group Islamic Insurance Company 25-Feb-19 11 Due QNNS Qatar Navigation (Milaha) 25-Feb-19 11 Due QCFS Qatar Cinema & Film Distribution Company 26-Feb-19 12 Due MCCS Mannai Corporation 26-Feb-19 12 Due AHCS Aamal Company 27-Feb-19 13 Due SIIS Salam International Investment Limited 6-Mar-19 20 Due Source: QSE News Qatar GISS reports net loss of QR137.7mn in 4Q2018 driven by impairments; no dividend declared as was the case in 2017 – Gulf International Services (GISS) reported net loss of QR137.7mn in 4Q2018 as compared to net profit of QR62.8mn in 4Q2017, and net profit of QR5.2mn in 3Q2018. We had estimated net profit of QR24.8mn in 4Q2018 but had warned that rig impairment(s) were possible and could wipe out the profits for the year and cancel the dividends. This is exactly what happened; if we exclude QR159mn in expenses, the majority of which is the write-off of the Al-Doha rig (QR113mn) and write-off of PP&E (another QR37mn), adjusted net income would have been QR21.7mn vs. our estimate of QR24.8mn. The company's revenue came in at QR558.1mn in 4Q2018, which represents an increase of 5.9% YoY. However, on QoQ basis, revenue fell 14.2%. Loss per share amounted to QR0.53 in FY2018 as compared to earnings per share of QR0.46 in FY2017. GISS recorded QR2.5bn in revenue and an EBITDA of QR746mn in FY2018. The group’s revenue for the year is marginally up by QR0.1bn or 5% over the last year. All segments, except the catering segment, reported growth over the previous year. The aviation segment witnessed a marginal growth versus the previous year. Ex-Qatar aviation revenue and revenue from other ancillary services grew moderately. The insurance segment was able to regain some of the previously lost businesses in addition to capturing new businesses in both the energy and medical lines of business, resulting in a significant increase in revenue. The catering segment witnessed a reduction on last year, primarily due to demobilization of some of the projects and reduced occupancy in the camps. Drilling segment witnessed a marginal growth on the previous year, the segment benefited from the deployment of some of the assets that were not previously contracted and recovery in the crude oil price. The reported EBITDA is also up over the last year. An increase in the revenue and reduction in the general and administrative expenses resulted in an increase in EBITDA from last year. Net profit, on the other hand, decreased on last year, and the reported net loss for 2018 was QR98.3mn. This loss was on account of higher finance charges and one-off expenses relating to the impairment of assets in the drilling segment. (QNB FS Research, Company financials, Peninsula Qatar) Vodafone Qatar to hold its AGM and EGM on March 4 – Vodafone Qatar‘s board of directors invited its shareholders to attend Annual General Assembly (AGM) and Extraordinary General Assembly Meeting (EGM) of the company, which will be held on March 4, 2019. In case of lack of quorum, a second meeting will be held on March 12, 2019. (QSE) DOHI reports net profit of ~QR25mn in 4Q2018 – Doha Insurance Group's (DOHI) net profit rose ~230% YoY and from QR0.5mn as of 3Q2018 to ~QR25mn in 4Q2018. In FY2018, DOHI reported net profit of QR60mn as compared to net profit of QR42.2mn in FY2017. EPS increased to QR1.21 in FY2018 from QR0.84 in FY2017. The board of directors has decided to submit a proposal for distribution of cash dividends equal to 8% of the share par value i.e. QR0.80 for each share to the company’s upcoming Annual General Assembly meeting. (QSE) ORDS' bottom line rises ~40% YoY and ~17% QoQ in 4Q2018 – Ooredoo's (ORDS) net profit rose ~40% YoY (+~17% QoQ) to ~QR473mn in 4Q2018. The company's revenue came in at ~QR7,152mn in 4Q2018, which represents a decrease of ~12% YoY (~-5% QoQ). EPS decreased to QR4.89 in FY2018 from QR5.92 in FY2017. In FY2018, ORDS posted net profit of nearly QR1.6bn and revenue of QR29.9bn. Most of ORDS’ operations delivered a ‘solid performance’ in 2018. However, group results were significantly impacted by the market situation in

- 4. Page 4 of 7 Indonesia following the new SIM card registration regulation, challenging market conditions in Algeria and the overall foreign exchange (FX) weakness in emerging markets. The 2018 revenue of QR29.9bn was driven by ‘strong’ contributions from Oman and Kuwait. Group revenue before the FX impact decreased by 6%, while reported revenue decreased by 8% YoY. The fourth quarter (4Q2018) included an adjustment of previous quarters related to the impact of IFRS 15 (a new financial reporting standard on revenue recognition). Excluding this impact 4Q2018 revenue declined by 9% instead of the reported 12%. In FY2018, Group EBITDA was QR12.2bn with a corresponding EBITDA margin of 41% (vs. QR13.6bn and 42%, respectively, in FY2017). Group EBITDA decreased by almost 11% YoY, mainly due to lower revenues. Excluding foreign exchange impact, EBITDA decreased by 9% YoY. Increased monetization of data business, with significant data growth coming from consumer and enterprise customers saw data revenue increasing to 47% of group revenue. Revenue from data contributed QR14.2bn. Commenting on the results, ORDS’ Chairman, Sheikh Abdulla bin Mohamed bin Saud Al-Thani said, “Across emerging markets, new digital technologies offer the chance for people and businesses to achieve their full potential and realize new opportunities. Through our robust and clear strategy, ORDS is well-positioned to support the introduction and sustain the development of these new technologies across all our markets, as demonstrated through our business results for 2018.” The board of directors proposed a cash dividend of QR2.5 per share for 2018. (QSE, Company financials, Gulf-Times.com) MSCI announces quarterly index review for QSE stocks – MSCI Inc. announced the results of the February 11, 2019 Quarterly Index Review with no change on QSE stocks. (QSE) Qatar Petroleum signs five-year light naphtha sales agreement with Marubeni – Qatar Petroleum has concluded a five-year sales agreement to supply Japan’s Marubeni Corporation (Marubeni) an annual total of 200,000 tons of light naphtha starting from January 2019. The deal was executed for and on behalf of Qatar Petroleum for the Sale of Petroleum Products Company (QPSPP). The agreement is the third such one to be concluded with Marubeni since both parties started their naphtha business together over three decades ago. The previous two long-term naphtha sales agreements with Marubeni were concluded in 2018. HE the Minister of State for Energy Affairs, Saad Sherida Al-Kaabi, also President and CEO of Qatar Petroleum said, “We are pleased to sign the third naphtha long-term sales agreement with Marubeni Corporation. This agreement does not just strengthen our relations with Marubeni, but also reflects our strengthened ability to produce and export naphtha to the Asian market safely and reliably.” (Gulf-Times.com) Al-Baker welcomes Doha Declaration that calls for 'serious review' of existing aviation regulatory framework – Qatar Airways’ CEO, HE Akbar Al-Baker welcomed the publication of ‘Doha Declaration,’ a manifesto that calls for a serious review of the existing aviation regulatory framework. The Doha Declaration, which was announced at the conclusion of the CAPA Qatar Aviation, Aeropolitical and Regulatory Summit held in Doha, comes 75 years after the historic Chicago Convention, which established the International Civil Aviation Organization (ICAO) as well as a set of global rules for airspace, air safety and air travel. Commenting on the declaration, Al- Baker said, “Qatar Airways wholeheartedly endorses the Doha Declaration and calls on airlines all over the world to join us in supporting it.” The declaration follows the recent announcement that Qatar and the European Union have concluded their negotiations for a landmark Comprehensive Air Transport Agreement. (Gulf-Times.com) List of 'excise tax goods' not final, says GTA official – The list of consumer products that were chosen by the government for levying excise tax last month is 'not final' even as some goods could either be added or removed from the list, an official of the General Tax Authority (GTA) said at a seminar on excise tax organized by Qatar Chamber. On January 1, Qatar officially imposed excise taxes on carbonated drinks (50% rate) and tobacco products and energy drinks (100%), among other items that fall under ‘excise goods’ to limit consumption of several items, while raising government funds for public services. A statement from Qatar Chamber quoted GTA’s Head of Indirect Tax, Hamad Mohamed Al-Attiyah as saying that “the list of goods of (excise) tax is not final; other goods can be added or existing goods can be removed.” GTA’s Indirect Tax Expert, Sami Nasr said the main intent of imposing excise tax is to reduce consumption of such goods, while also raising revenues for the government. While the amount of revenue generated from the newly imposed tax is yet to be gauged, Nasr said, the new tax will be vital in reducing government’s spending on healthcare services in the country. (Gulf-Times.com, Qatar Tribune) International IEA: Global oil supply to swamp demand in 2019 despite output cuts – The global oil market will struggle this year to absorb fast-growing crude supply from outside OPEC, even with the group’s production cuts and US sanctions on Venezuela and Iran, the International Energy Agency (IEA) stated. The IEA left its demand growth forecast for 2019 unchanged from its last report in January at 1.4mn barrels per day. “It is supported by lower prices and the start-up of petrochemical projects in China and the US. Slowing economic growth will, however, limit any upside,” the agency stated. The IEA raised its estimate of growth in crude supply from outside the OPEC to 1.8mn bpd in 2019, from 1.6mn bpd previously. The agency also lowered its forecast for demand for OPEC crude, production of which the group has pledged to cut by 800,000 bpd this year as part of an agreement with Russia and other non-OPEC producers such as Oman and Kazakhstan. The call on OPEC crude is now forecast at 30.7mn bpd in 2019, down from the IEA’s last estimate of 31.6mn bpd in January. (Reuters) Lower gasoline prices restrain US consumer inflation – US consumer prices were unchanged for a third straight month in January, leading to the smallest annual increase in inflation in more than one-and-a-half years, which could allow the Federal Reserve to hold interest rates steady for a while. The Labor Department’s report supported the Fed’s recent description of price pressures being muted. In a policy statement last month, the US central bank kept rates unchanged, pledged to be patient before tightening monetary policy further and discarded

- 5. Page 5 of 7 promises of further gradual increases in borrowing costs. The Consumer Price Index (CPI) last month was held down by cheaper gasoline, which offset increases in the cost of food, rent, healthcare, recreation, apparel, motor vehicles and household furnishings. In the 12 months through January, the CPI rose 1.6%, the smallest gain since June 2017. The CPI increased 1.9% on a YoY basis in December. (Reuters) US posts another budget deficit as tax revenues sag – The US federal government ran a $14bn budget deficit in December as revenues sagged following last year’s tax cuts even as the economy appeared strong, Treasury Department data showed. Analysts polled by Reuters had expected $11bn deficit for the month and the gap was the latest sign of deterioration in the government’s fiscal position. A strong US job market has appeared to power economic growth this year, an economic setting that tends to help fiscal revenues. Economists suspect some of the economic strength draws from tax cuts that came into effect at the beginning of 2018. However Washington’s accounts have run $319bn into the red since the fiscal year began in October, compared to $225bn deficit over the same period a year earlier. (Reuters) UK’s inflation hits two-year low on falling energy costs – British annual inflation hit a two-year low point in January, undershooting the Bank of England’s 2.0% target on falling oil and other energy costs, official data showed. The Consumer Price Index 12-month rate hit 1.8% last month, down from 2.1% in December, the Office for National Statistics (ONS) stated. That marked the first time since January 2017 that the rate has fallen underneath the Bank of England’s official 2.0% target level. Analysts had forecast a drop to 1.9%. Inflation was pulled lower by a decline in electricity, gas and motor fuel prices between December and January. “The fall in inflation is due mainly to cheaper gas, electricity and petrol, partly offset by rising ferry ticket prices and air fares falling more slowly than this time last year,” ONS inflation Head, Mike Hardie said. (Qatar Tribune) Eurozone’s industrial production falls more than expected in December – Eurozone’s industrial production fell more than expected in December, official estimates showed, pulled down by a drop in the output of capital goods, used for investment. The European Union’s statistics office Eurostat stated industrial output in the 19-country currency union fell 0.9% MoM for 4.2% YoY decline. Economists polled by Reuters had expected 0.4% monthly fall and 3.2 YoY decline. Eurostat stated the production of capital goods, like machinery, fell by 1.5% in December against November and year on year the fall was 5.5%, accelerating from 4.4% in November. The fall in industrial production and the decline in the output of capital goods underline the trend of slowing economic growth in the Eurozone where the European Commission expects growth to decelerate to 1.3% this year from 1.9% in 2018. (Reuters) Japan’s fourth-quarter GDP rebounds but trade frictions remain a concern – Japan’s economy expanded in the fourth quarter as business and consumer spending recovered from natural disasters, however global trade protectionism remained a concern for the country. The 1.4% annualized expansion in October-December matched the median estimate in a Reuters poll. It followed a revised 2.6% annualized contraction in July- September as floods and an earthquake temporarily halted production. The data also showed real exports rose 0.9% in October-December from the previous quarter, which was the fastest gain in a year. Despite the increase in shipments, some economists remain concerned that exports will weaken this year if the US and China do not resolve their trade dispute. (Reuters) China’s January trade beats forecasts; exports up 9.1%, imports dip 1.5% – China’s January Dollar-denominated exports rose 9.1% from a year earlier, while imports dropped 1.5%, both beating analysts’ expectations, official data showed. That left the country with a trade surplus of $39.16bn for the month, the General Administration of Customs stated. Analysts polled by Reuters had expected both exports and imports to fall for a second straight month, but cautioned the trend could be distorted by the timing of the long Lunar New Year holidays, which fell in early February this year. Exports had been forecast to decline 3.2%, after a 4.4% drop in December. Imports were expected to have dropped 10%, after declining 7.6% in the preceding month. Analysts were also expecting China’s trade surplus to have narrowed in January to $33.5bn from $57.06bn in December. (Reuters) China considering measures to adjust lending rates for companies – China is considering measures to drive adjustments in financial institutions’ lending rates for companies to improve credit flow into the economy, the official English-language China Daily reported, citing a central bank official. Sun Guofeng, Head of the People’s Bank of China’s monetary policy department, said that despite rising expectations of a central bank interest rate cut, it is more urgent to allow financial markets, rather than the People's Bank of China to determine lending rates. Policymakers should assess domestic macroeconomic conditions to reduce financing costs before pursuing more interest rate reform. (Reuters) Regional Saudi Arabia's PIF will raise stake in ACWA Power, to expand overseas – Saudi Arabia’s Public Investment Fund (PIF) plans to increase its stake in ACWA Power to 40% from 25% and is looking to invest in electric vehicles and solar power, its Managing Director, Yasir al-Rumayyan said. The sovereign fund also plans to boost its staff to 700 by the end of the year from 450 now, and is aiming to open offices in London and in the US - initially in New York and then in San Francisco, he said. “We will be the largest investor in renewable energy,” he said. “Oil, we think, is very important to us, we don’t want to waste oil only on transportation.” The fund has made substantial commitments to other green projects, including renewables and recycling, and to technology companies, such as a $45bn agreement to invest in a technology fund led by Japan’s SoftBank Group Corp. It also owns stakes in electric car makers Tesla and Lucid Motors. (Reuters) Saudi Arabia’s wealth fund held 8.3mn shares of Tesla at the year-end – Saudi Arabia’s sovereign wealth fund (PIF) has confirmed in a 13F filing with the Securities and Exchange Commission that it held 8.3mn shares of Tesla as of December 31, 2018. (Bloomberg) Tabreed gets 30-year India concession in first foray outside the GCC – National Central Cooling Co. (Tabreed) has won a 30-year

- 6. Page 6 of 7 concession to build, own, operate and transfer a district cooling system in India, its first plant outside the Gulf region. “We see this as an opportunity to establish an initial presence which will be the foundation for further growth,” Tabreed’s Chairman, Khaled Al Qubaisi said. (Bloomberg) Mubadala's venture capital unit will launch $400mn European fund – Mubadala Ventures, the venture capital arm of Abu Dhabi’s state-owned Mubadala Investment Company, plans to launch a $400mn European fund this year to focus on the technology sector, a company executive said. The venture capital unit is also working with international venture capital funds to invest in Abu Dhabi, Head of Mubadala Ventures, Ibrahim Ajami said. Mubadala’s venture capital arm is replicating its US strategy in Europe by launching a $400mn Ventures Fund as well as a fund of funds this year. The US- based Ventures Fund, announced in 2017, is 30% deployed in US firms in sectors such as healthcare, fintech, cyber security and others, he said. Most investments are in Silicon Valley companies but Mubadala is looking at New York companies too. “We are building the same business in Europe, focused on tech funds and companies,” he told reporters. “We will also be working with international venture funds, inviting them to come to Abu Dhabi to play a role here.” Mubadala plans to create a start-up ecosystem in Abu Dhabi and help start-ups in areas such as blockchain, healthcare, food delivery and automotive mobility. (Reuters) UAB posts 345.3% YoY rise in net profit to AED77.2mn in FY2018 – United Arab Bank (UAB) recorded net profit of AED77.2mn in FY2018, an increase of 345.3% YoY. Net operating profit rose 4.6% YoY to AED405.6mn in FY2018. Total assets stood at AED20.5bn at the end of December 31, 2018 as compared to AED20.7bn at the end of December 31, 2017. EPS came in at AED0.04 in FY2018 as compared to AED0.01 in FY2017. (ADX) Dana Gas may sell Iraqi gas to Turkish buyers – UAE-based Dana Gas plans to more than double its gas output in Iraq and may sell a portion of the increased volumes in Turkey, CEO, Patrick Allman-Ward said. The company and its partner Pearl Petroleum will raise output in Iraq by 500mn cf/d over the next 3 years from 400mn cf/d. The half of extra gas will be used in Iraqi Kurdistan power stations; rest can be sold locally or exported. Dana Gas prefers to export via a pipeline to be operated by Rosneft. A fallback option is to build its own link from Erbil to Turkey, he said. Contractors, export credit agencies, gas supply payments and/or a bond issued by Pearl Petroleum will fund the Iraqi projects, he added. (Bloomberg) Kuwait Finance House will start Ahli United Bank merger due- diligence – Kuwait Finance House (KFH) plans to start due diligence to buy Bahrain’s Ahli United Bank, a potential combination that will create the Gulf’s sixth-biggest lender with $92bn in assets. KFH received the central bank’s initial approval to commence the process, according to a statement. (Bloomberg) Oman's budget deficit revised down 10% to OMR2.7bn for 2018 – Oman revised its preliminary 2018 budget deficit estimate to OMR2.7bn from OMR3bn on higher revenue. Budget income reached OMR10.9bn, up from an earlier projection for OMR9.5bn. It has recorded non-oil revenue of OMR2.4bn, state- run Oman News Agency reported. (Bloomberg) Al Salam Bank-Bahrain posts net profit of BHD18.5mn in FY2018 – Al Salam Bank-Bahrain (SALAM) recorded net profit of BHD18.5mn in FY2018, an increase of 2.2% YoY. Finance Income rose 10.2% YoY to BHD49.4mn in FY2018. Total operating income fell 8.8% YoY to BHD56.7mn in FY2018. Total assets stood at BHD1,710.3mn at the end of December 31, 2018 as compared to BHD1,589.2mn at the end of December 31, 2017. Financing assets stood at BHD568.9mn (+6.8% YoY), while placements from customers stood at BHD705.9mn (+17.1% YoY) at the end of December 31, 2018. EPS came in at BHD0.087 in FY2018 as compared to BHD0.085 in FY2017. (DFM) Investcorp and Standard Life will raise around $1bn for Gulf Fund – Bahrain’s Investcorp Bank and Standard Life Aberdeen plan to raise $800mn to $1bn for a fund to invest in infrastructure in the Gulf Cooperation Council (GCC). The venture between the Bahrain-based alternative-assets manager and the Scottish firm’s Aberdeen Standard Investments unit will focus on healthcare, education and utilities. It may also invest in the wider Middle East and Levant. (Bloomberg)

- 7. Contacts Saugata Sarkar, CFA, CAIA Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa Mehmet Aksoy, PhD QNB Financial Services Co. W.L.L. Senior Research Analyst Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6589 PO Box 24025 mehmet.aksoy@qnbfs.com.qa Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services Co. W.L.L. (“QNB FS”) a wholly-owned subsidiary of Qatar National Bank (Q.P.S.C.). QNB FS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange. Qatar National Bank (Q.P.S.C.) is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNB FS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNB FS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNB FS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNB FS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNB FS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNB FS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNB FS. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNB FS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 45.0 70.0 95.0 120.0 Jan-15 Jan-16 Jan-17 Jan-18 Jan-19 QSEIndex S&PPanArab S&PGCC 0.2% (1.2%) 0.2% (1.1%) (0.2%) 0.0% 0.3% (1.5%) (1.0%) (0.5%) 0.0% 0.5% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,306.25 (0.3) (0.6) 1.9 MSCI World Index 2,052.76 0.4 1.6 9.0 Silver/Ounce 15.57 (0.8) (1.7) 0.5 DJ Industrial 25,543.27 0.5 1.7 9.5 Crude Oil (Brent)/Barrel (FM Future) 63.61 1.9 2.4 18.2 S&P 500 2,753.03 0.3 1.7 9.8 Crude Oil (WTI)/Barrel (FM Future) 53.90 1.5 2.2 18.7 NASDAQ 100 7,420.38 0.1 1.7 11.8 Natural Gas (Henry Hub)/MMBtu 2.63 (3.0) 0.4 (19.1) STOXX 600 364.97 0.2 1.4 6.4 LPG Propane (Arab Gulf)/Ton 64.75 0.8 4.9 1.2 DAX 11,167.22 (0.0) 1.9 4.2 LPG Butane (Arab Gulf)/Ton 82.50 2.2 15.0 18.7 FTSE 100 7,190.84 0.5 1.1 7.8 Euro 1.13 (0.6) (0.5) (1.8) CAC 40 5,074.27 (0.0) 1.8 5.6 Yen 111.01 0.5 1.2 1.2 Nikkei 21,144.48 1.0 2.9 5.2 GBP 1.28 (0.4) (0.8) 0.7 MSCI EM 1,041.85 (0.0) 0.6 7.9 CHF 0.99 (0.3) (0.9) (2.7) SHANGHAI SE Composite 2,721.07 2.0 3.7 11.0 AUD 0.71 (0.1) 0.0 0.6 HANG SENG 28,497.59 1.2 2.0 10.0 USD Index 97.13 0.4 0.5 1.0 BSE SENSEX 36,034.11 (0.7) (0.9) (1.8) RUB 66.53 1.0 1.1 (4.6) Bovespa 95,842.40 (1.4) 0.0 12.6 BRL 0.27 (1.2) (0.7) 3.4 RTS 1,190.79 (2.0) (0.7) 11.4 98.0 92.0 79.2