Call Girls Service Nagpur Maya Call 7001035870 Meet With Nagpur Escorts

17 April Daily market report

1. Page 1 of 6

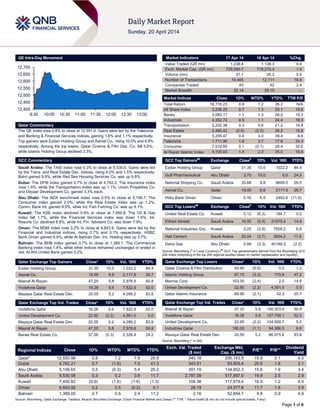

QE Intra-Day Movement

Qatar Commentary

The QE index rose 0.8% to close at 12,551.0. Gains were led by the Telecoms

and Banking & Financial Services indices, gaining 1.6% and 1.1% respectively.

Top gainers were Ezdan Holding Group and Aamal Co., rising 10.0% and 6.9%

respectively. Among the top losers, Qatar Cinema & Film Dist. Co. fell 5.6%,

while Islamic Holding Group declined 3.3%.

GCC Commentary

Saudi Arabia: The TASI index rose 0.3% to close at 9,530.6. Gains were led

by the Trans. and Real Estate Dev. indices, rising 4.0% and 1.5% respectively.

Bahri gained 9.9%, while Red Sea Housing Services Co. was up 9.8%.

Dubai: The DFM index gained 0.7% to close at 4,762.2. The Insurance index

rose 1.4%, while the Transportation Index was up 1.1%. Union Properties Co.

and Deyaar Development Co. gained 3.3% each.

Abu Dhabi: The ADX benchmark index rose 0.5% to close at 5,156.7. The

Consumer index gained 2.0%, while the Real Estate Index was up 1.2%.

Comm. Bank Int. gained 9.5%, while Int. Fish Farming Co. was up 9.1%.

Kuwait: The KSE index declined 0.9% to close at 7,450.8. The Oil & Gas

index fell 1.7%, while the Financial Services index was down 1.6%. Int.

Resorts Co. declined 8.8%, while Int. Fin. Advisers Co. was down 7.9%.

Oman: The MSM index rose 0.2% to close at 6,843.9. Gains were led by the

Financial and Industrial indices, rising 0.7% and 0.1% respectively. HSBC

Bank Oman gained 6.9%, while Al Batinah Dev. Inv. Holding was up 3.7%.

Bahrain: The BHB index gained 0.7% to close at 1,389.1. The Commercial

Banking index rose 1.4%, while other indices remained unchanged or ended in

red. Al Ahli United Bank gained 3.2%.

Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD%

Ezdan Holding Group 31.35 10.0 1,022.2 84.4

Aamal Co. 19.00 6.9 2,117.9 26.7

Masraf Al Rayan 47.20 5.8 2,978.8 50.8

Vodafone Qatar 16.28 5.6 7,822.9 52.0

Mazaya Qatar Real Estate Dev. 20.55 5.2 4,289.2 83.8

Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD%

Vodafone Qatar 16.28 5.6 7,822.9 52.0

United Development Co. 22.60 (2.2) 4,561.0 5.0

Mazaya Qatar Real Estate Dev. 20.55 5.2 4,289.2 83.8

Masraf Al Rayan 47.20 5.8 2,978.8 50.8

Barwa Real Estate Co. 37.00 (0.3) 2,328.4 24.2

Market Indicators 17 Apr 14 16 Apr 14 %Chg.

Value Traded (QR mn) 1,238.4 1,138.3 8.8

Exch. Market Cap. (QR mn) 728,590.7 718,270.3 1.4

Volume (mn) 37.1 35.2 5.5

Number of Transactions 14,405 12,111 18.9

Companies Traded 43 42 2.4

Market Breadth 22:14 25:15 –

Market Indices Close 1D% WTD% YTD% TTM P/E

Total Return 18,716.23 0.8 1.2 26.2 N/A

All Share Index 3,238.25 0.7 1.3 25.1 15.6

Banks 3,083.17 1.1 1.3 26.2 15.3

Industrials 4,352.72 0.5 1.1 24.4 16.3

Transportation 2,252.38 0.3 0.6 21.2 14.8

Real Estate 2,465.42 (0.5) (0.3) 26.2 15.8

Insurance 3,255.47 0.4 3.0 39.4 8.6

Telecoms 1,711.96 1.6 3.7 17.8 24.3

Consumer 7,519.85 0.1 (0.1) 26.4 30.6

Al Rayan Islamic Index 4,100.03 1.4 2.3 35.0 18.8

GCC Top Gainers##

Exchange Close#

1D% Vol. ‘000 YTD%

Ezdan Holding Group Qatar 31.35 10.0 1022.2 84.4

Gulf Pharmaceutical Abu Dhabi 3.70 10.0 0.0 24.5

National Shipping Co. Saudi Arabia 35.68 9.8 6608.0 26.5

Aamal Co. Qatar 19.00 6.9 2117.9 26.7

Hsbc Bank Oman Oman 0.16 6.9 2492.6 (11.9)

GCC Top Losers##

Exchange Close#

1D% Vol. ‘000 YTD%

United Real Estate Co. Kuwait 0.12 (6.3) 194.7 0.0

Etihad Atheeb Saudi Arabia 16.55 (5.5) 21075.4 14.9

National Industries Grp. Kuwait 0.25 (3.8) 7928.2 6.8

Hail Cement Saudi Arabia 25.04 (3.7) 3834.2 17.6

Dana Gas Abu Dhabi 0.89 (3.3) 40189.3 (2.2)

Source: Bloomberg (

#

in Local Currency) (

##

GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD%

Qatar Cinema & Film Distribution 40.60 (5.6) 0.0 1.2

Islamic Holding Group 67.70 (3.3) 170.9 47.2

Mannai Corp 103.00 (2.4) 2.0 14.6

United Development Co. 22.60 (2.2) 4,561.0 5.0

Qatar Islamic Insurance 69.90 (2.1) 42.3 20.7

Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD%

Masraf Al Rayan 47.20 5.8 140,303.4 50.8

Vodafone Qatar 16.28 5.6 127,756.1 52.0

United Development Co. 22.60 (2.2) 104,926.7 5.0

Industries Qatar 180.00 (1.1) 94,386.5 6.6

Mazaya Qatar Real Estate Dev. 20.55 5.2 86,915.6 83.8

Source: Bloomberg (* in QR)

Regional Indices Close 1D% WTD% MTD% YTD%

Exch. Val. Traded

($ mn)

Exchange Mkt.

Cap. ($ mn)

P/E** P/B**

Dividend

Yield

Qatar* 12,550.98 0.8 1.2 7.8 20.9 340.18 200,143.9 15.9 2.1 4.0

Dubai 4,762.21 0.7 (1.6) 7.0 41.3 343.51 93,805.4 20.6 1.8 2.1

Abu Dhabi 5,156.65 0.5 (0.3) 5.4 20.2 391.10 134,852.3 15.6 1.9 3.4

Saudi Arabia 9,530.58 0.3 0.2 0.6 11.7 2,797.09 517,697.0 19.9 2.5 2.9

Kuwait 7,450.82 (0.9) (1.6) (1.6) (1.3) 104.36 117,679.4 16.5 1.2 4.0

Oman 6,843.92 0.2 0.5 (0.2) 0.1 28.19 24,577.6 11.7 1.6 3.9

Bahrain 1,389.05 0.7 0.5 2.4 11.2 2.16 52,854.7 9.8 0.9 4.9

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

12,400

12,450

12,500

12,550

12,600

12,650

12,700

9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

2. Page 2 of 6

Qatar Market Commentary

The QE index rose 0.8% to close at 12,551.0. The Telecoms and

Banking & Financial Services indices led the gains. The index

rose on the back of buying support from non-Qatari shareholders

despite selling pressure from Qatari shareholders.

Ezdan Holding Group and Aamal Co. were the top gainers, rising

10.0% and 6.9% respectively. Among the top losers, Qatar

Cinema & Film Dist. Co. fell 5.6%, while Islamic Holding Group

declined 3.3%.

Volume of shares traded on Thursday rose by 5.5% to 37.1mn

from 35.2mn on Wednesday. Further, as compared to the 30-day

moving average of 22.4mn, volume for the day was 65.4%

higher. Vodafone Qatar and United Development Co. were the

most active stocks, contributing 21.1% and 12.3% to the total

volume respectively.

Source: Qatar Exchange (* as a % of traded value)

Earnings and Global Economic Data

Earnings Releases

Company Market Currency

Revenue

(mn)1Q2014

% Change

YoY

Operating Profit

(mn) 1Q2014

% Change

YoY

Net Profit (mn)

1Q2014

% Change

YoY

ACE Arabia Cooperative

Insurance Co.

Saudi SR 42.8 -12.9% – – 1.8 -71.1%

United Cooperative

Assurance (UCA)

Saudi SR 284.5 -23.8% – – 2.3 -85.7%

Arabian Pipes Co. (APC) Saudi SR – – -0.3 NA -6.8 NA

Al-Tayyar Travel Group

Holding (ATG)

Saudi SR – – 266.0 16.2% 280.0 28.4%

Saudi Printing & Packaging

Co. (SPPC)

Saudi SR – – 21.4 -19.2% 9.5 -30.7%

Arabian Cement Co. (ACC) Saudi SR – – 166.0 4.8% 167.1 6.2%

Saudi ORIX Leasing Co. Saudi SR – – 44.5 15.8% 28.2 20.2%

Nama Chemicals Co. Saudi SR – – -16.7 NA -14.9 NA

SABB Takaful Co. Saudi SR 38.7 9.0% 0.0 0.0% 2.8 3.0%

Bawan Holding Co. Saudi SR – – 68.5 38.7% 46.7 15.8%

Saudi Steel Pipe Co.

(SSPC)

Saudi SR – – 9.1 -63.3% 4.0 -82.6%

Tourism Enterprises Co.

(Shams)

Saudi SR – – 0.8 8.2% 0.6 -89.2%

Saudi Industrial

Development Co. (SIDC)

Saudi SR – – 3.5 -48.5% 20.0 207.7%

United International

Transportation Co. (UITC)

Saudi SR – – 12.8 43.7% 39.9 10.3%

Saudi Transport &

Investment Co. (Mubarrad)

Saudi SR – – -0.7 NA 1.4 300.4%

Takween Advanced

Industries (TAI)

Saudi SR – – 7.7 -61.3% 8.8 -51.6%

Basic Chemical Industries

Co. (BCI)

Saudi SR – – 18.2 -35.7% 8.7 -46.3%

Filling & Packing Materials

Manufacturing Co. (FIPCO)

Saudi SR – – 7.8 1.2% 6.9 0.3%

Saudi Re for Cooperative

Reinsurance Co.

Saudi SR 291.3 37.3% – – 22.5 49.9%

Ash-Sharqiyah Development

Co. (SHADCO)

Saudi SR – – -1.4 NA -1.5 NA

Saudi Arabian Amiantit Co.

(SAAC)

Saudi SR – – 46.5 -34.2% 20.6 -32.1%

Saudi Automotive Services

Co. (SASCO)

Saudi SR – – 3.2 60.7% 7.8 -1.4%

Saudi Kayan Petrochemical

Co.

Saudi SR – – 157.6 NA 9.9 NA

Dar Alarkan Real Estate

Development Co.

Saudi SR – – – – 247.9 4.3%

Insurance House (IH) Abu Dhabi AED 22.6 68.0% – – 4.5 29.0%

Kuwait Finance House

(KFH)

Kuwait KD – – – – 26.1 13.3%

Oman United Insurance Co.

(OUIC)

Oman OMR – – – – 1.7 3.6%

Gulf Mushroom Products

Co. (GMPC)

Oman OMR 1.6 -5.5% – – 0.1 -67.0%

Source: Company data, DFM, ADX, MSM

Overall Activity Buy %* Sell %* Net (QR)

Qatari 71.63% 74.56% (36,305,812.65)

Non-Qatari 28.37% 25.44% 36,305,812.65

3. Page 3 of 6

Global Economic Data

Date Market Source Indicator Period Actual Consensus Previous

04/17 US Department of Labor Initial Jobless Claims 12-April 304K 315K 302K

04/17 US Bloomberg Bloomberg Economic Expectations April -4 – -12

04/17 US Bloomberg Bloomberg Consumer Comfort 13-April -29.1 – -31.9

04/17 Germany Destatis PPI MoM March -0.30% 0.00% 0.00%

04/17 Germany Destatis PPI YoY March -0.90% -0.70% -0.90%

04/18 Italy ISTAT Industrial Sales MoM February -1.50% – 1.20%

04/18 Italy ISTAT Industrial Sales WDA YoY February 1.20% – 3.00%

04/18 Italy ISTAT Industrial Orders MoM February -3.10% – 4.70%

04/18 Italy ISTAT Industrial Orders NSA YoY February 2.80% – 2.60%

04/17 China NBS Foreign Direct Investment YoY March -1.50% 2.00% –

04/17 Japan ESRI Consumer Confidence Index March 37.5 37.7 38.5

04/18 Japan METI Tertiary Industry Index MoM February -1.00% 0.20% 1.60%

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

News

Qatar

QCB to enter China interbank bond market – The People’s

Bank of China (PBOC) and the Qatar Central Bank (QCB) have

signed a deal under which the latter will be allowed to enter

China’s interbank bond market. The access to the market will

enable QCB to purchase Chinese bonds for its foreign exchange

reserves. (GulfBase.com)

QNCD posts net profit of QR129.9mn in 1Q2014 – Qatar

National Cement (QNCD) posted a net profit of QR129.9mn in

1Q2014 vs. QR118.6mn in 1Q2013, up 9.5% YoY. Sales

increased to QR279.9mn in 1Q2014 from QR267.3mn in

1Q2013, up 4.7% YoY. Cost of sales increased marginally to

QR150.2mn vs. QR149.8mn in 1Q2013. Hence, gross profit

increased to QR129.7mn vs. QR117.5mn. Gross margin

improved to 46.3% from 44.0%. QNCD remains a market leader

cashing in on the Qatari infrastructure/construction growth. The

company’s focus on Qatar makes it one of the pure

infrastructure/construction plays on the Qatar growth story. In

order to cash in on Qatar’s anticipated demand for cement,

QNCD recently announced capacity expansion by another 5,000

(previously 7,500) tons per day (tpd). The new line will increase

total clinker capacity to 16,900 tpd from 11,900 tpd (net of an

anticipated sale/retirement of the aging Line 1, which has a

capacity of 1,000 tpd). Furthermore, the new capacity will come

online in mid-2016 instead of early 2016. (QE, QNBFS)

QCFS posts QR4.21mn net income in 1Q2014 – Qatar

Cinema and Film Distribution (QCFS) posted a net profit of QR

4.21mn in 1Q2014 vs. QR4.07mn for the corresponding period

in 2013. Earnings per Share (EPS) amounted to QR0.73 as of

March 31, 2014 versus QR0.71 of the same period in 2013.

(QE)

Kahramaa building mega reservoirs to ensure water

security – In a major step toward achieving water security in the

country, the Qatar General Electricity and Water Corporation

(Kahramaa) has set in motion the process of building five

primary reservoir and pumping station (PRPS) packages as part

of its Water Security Mega Reservoirs project. The objective of

the project is to provide seven days of potable water storage in

new reservoirs, combined with the existing and future secondary

reservoirs, to preserve Qatar’s water quality in line with

Kahramaa and World Health Organization standards. Kahramaa

earlier this week announced the tender for local and

international companies to bid for construction of the PRPS

packages. The project entails the construction of five mega-

reservoir sites and approximately 200km of large-diameter ring

mains. Each reservoir site will ultimately include up to nine

reservoir modules, with up to five per site being included in the

current tender, each of which will be among the largest of its

type in the world. (Gulf-Times.com)

Qatar to establish five bodies to push exports – Qatar will

set up five sectoral commissions to support local companies to

facilitate exports and participate in international trade &

investments. The five commissions will be established for

different sectors which include energy, trade, banking,

arbitration and company’s social responsibility (CSR).

(GulfBase.com)

Support for SMEs can help reduce imports, boost Qatar

economy – Qatar Shell media relations manager Ali Reyad al-

Ansari said extending more support to small and medium-sized

enterprises (SMEs) can boost the supply chain and improve the

economy by reducing the number of imports. (Gulf-Times.com)

QGMD to announce 1Q2014 results in April 30 – Qatar

German for Medical Devices will disclose its first quarter

financial results for the year 2014 on 30th

of April 2014.

Furthermore, QE has announced trading suspension of QGMD

shares on April 20, 2014 due to the company’s scheduled AGM

(QE)

QE announces trading suspension of ZHCD’s shares on

April 20 – The Qatar Exchange (QE) has announced trading

suspension of Zad Holding Company’s (ZHCD) shares on April

20, 2014 due to the company’s scheduled AGM. (QE)

International

Yellen sees muted inflation as unemployment curbs wages

– Federal Reserve president Janet Yellen said that wage gains

continue to proceed at a historically slow pace in this recovery,

with few signs of a broad-based acceleration. Making her first

major monetary-policy framework speech, she further expects

people who have been out of work for a long time to return to

the labor force as job prospects brighten, which will keep a lid on

wages and inflation. She further added that the long-term

unemployed are likely to move back more actively into the labor

force and into the job market & exert pressure on wages and

prices. Yellen stated that they will have to watch unfolding

evidence and evaluate it with an open mind. (Bloomberg)

CBO: Obama budget would boost U.S. tax revenue, cut

deficits – The Congressional Budget Office said President

Barack Obama's fiscal 2015 budget request would boost US tax

revenue by nearly $1.4tn over 10 years if fully enacted, cutting

deficits by $1.05tn while funding new spending. But the non-

4. Page 4 of 6

partisan agency's analysis was less optimistic than the White

House's own projections - showing that the cumulative deficits

would total $6.6tn over a ten-year period as compared to $4.9tn

under the Obama plan when it was released in March. A key

difference between the two deficit pictures is CBO's projection of

slower economic growth, partly resulting in lower revenue

collections. The likelihood that Congress will advance Obama's

plan in its entirety is virtually nil, but the CBO's latest analysis

will feed campaign messaging by Democrats and Republicans

ahead of congressional elections in November. The analysis by

the non-partisan agency compares Obama's request with a new

CBO "baseline" estimate released last week that assumes no

changes to the current tax and spending laws. Obama's budget

plan is loaded with policy changes, including an assumption that

sweeping immigration reforms will be enacted, producing a net

10-year deficit reduction of $158bn. It proposes to boost

revenue by limiting tax breaks for wealthy Americans and

businesses, imposing a new tax on millionaires, raising tobacco

taxes, and restoring estate & gift taxes to their previously higher

2009 levels. (Reuters)

ECB hardliner Weidmann comes in from the cold as

deflation threatens – The Bundesbank chief, Jens Weidman

known for his hardline stances at the ECB and as head of the

German central bank, is now ready to support such quantitative

easing (QE) if he and his ECB colleagues deem it necessary.

Eurozone inflation has slowed to 0.5% from 0.9% in November,

falling far below the ECB's target of just under 2%, stoking fears

the bloc could become stuck in a prolonged period of so-called

"low-flation", or even sink into outright deflation. Such a scenario

risks undermining the efforts of crisis-hit countries on the

Eurozone periphery to shape up their economies, and could

ultimately hit growth across the board if households defer

purchases in anticipation of lower prices in the future. Seeking to

head off such a drop in inflation expectations, the ECB's

governing council said earlier this month that it was unanimous

in its commitment to use unconventional tools - central bank-

speak for things like QE - to counter a protracted period of low

inflation. (Reuters)

Aso: Japan's new growth strategy to include GPIF role –

Japanese Finance Minister Taro Aso said that the government

will include a role of the country's $1.26tn public pension fund in

its growth strategy to be unveiled in June. A senior official said

last week that the Government Pension Investment Fund

(GPIF), the world's largest, is looking at alternative assets as it

seeks to diversify its holdings and generate higher returns to

finance a rapidly ageing population. (Reuters)

China must cut Yuan intervention, says ex-PBOC adviser –

According to former central bank adviser Yu Yongding, China

should rein in Yuan intervention and let the currency advance to

curb growth in its $3.95 trillion foreign exchange reserves. Yu

Yongding said the markets forces should determine the

exchange rate so long as there are “controls on speculative,

short-term capital flows. Liang Hong, vice chairman of the

capital markets committee of China International Capital Corp.,

said that China can no longer bear the cost of forex reserves

and can just let the Yuan appreciate. The comments echo the

view of the US Treasury Department, which two days ago

released a semiannual report that called on China to intervene

less and let markets play a greater role in determining the

Yuan’s value. Dollar purchases to weaken the Yuan are

contributing to the build-up of China’s foreign reserves, which

surged by $128.7bn in the first quarter after a record annual

jump of $509.7bn in 2013. The holdings lose value in Yuan

terms as China’s currency advances. The Yuan strengthened

37% versus the dollar from when a dollar peg was scrapped in

July 2005 to the end of last year, the best performance among

24 emerging-market currencies tracked by Bloomberg. So far in

2014 it has weakened 2.7%, the biggest loss among Asia’s 11

most-used currencies. (Bloomberg)

Regional

Tadawul deposits BSF’s bonus shares in shareholder

portfolios – The Saudi Stock Exchange (Tadawul) announced

the addition of Banque Saudi Fransi’s (BSF) bonus shares into

its investors’ portfolios. Earlier, BSF’s EGM had approved an

increase in the company’s capital via bonus shares. The

fluctuation limit of the company’s shares on April 17, 2014 will

be based on a stock price of SR31.50. (Tadawul)

ZIIC declares SR60mn dividends – Zamil Industrial Investment

Company’s (ZIIC) AGM has approved the board's

recommendation for the distribution of 10% dividends (SR1 per

share) amounting to SR60mn for 2H2013. This brings the total

distribution for the year ended December 31, 2013 to SR1.75

per share representing 17.5% of the paid-up capital. (Tadawul)

Jarir’s BoD recommends cash dividend of SR1.83 for

1Q2014 – Jarir Marketing Company’s (Jarir) board of directors

has recommended the distribution of cash dividend of SR1.83

for 1Q2014. (GulfBase.com)

PetroRabigh to extend unit shutdown to April 25 – Rabigh

Refining & Petrochemical Company (PetroRabigh) said that it

will extend the shutdown of a vacuum gas oil treatment unit to

April 25, 2014. Earlier, the company has announced that the unit

would be closed from March 27 to April 19 for maintenance

work. (GulfBase.com)

US agricultural exports to Saudi Arabia reach SR4.5bn –

According to Dr. Hassan Ahmed the Agricultural Counselor at

the US Embassy in Riyadh, US agricultural exports to Saudi

Arabia reached SR4.5bn in 2013. The US food exports to Saudi

Arabia also include a wide range of high quality well-known

brand names of consumer-ready products worth about SR1.5bn

in 2013. (GulfBase.com)

Saudi telecom regulator awards MVNO licenses to Virgin

Mobile Saudi Arabia and Jawraa Lebara – Saudi Arabia’s

telecom regulator awarded mobile virtual network operator

(MVNO) license to two new companies, Virgin Mobile Saudi

Arabia and Jawraa Lebara. Virgin Mobile Saudi Arabia has

teamed up with the Saudi Telecom Company (STC), while the

London-based Jawraa Lebara will offer the service together with

Mobily. (GulfBase.com)

FGB sets up $1bn Singapore program to fund Asia

expansion – First Gulf Bank, the UAE’s third-biggest lender,

said its Singapore branch has set up negotiable certificates of

deposit program for as much as $1bn to expand in the Asia

Pacific region. According to Bloomberg, the certificates and

instruments used by banks to raise money for short periods,

may be issued in multiple currencies which will allow it to “reach

out to a wider range of institutional investors”. The Singapore

branch is playing an important role in FGB’s plans to expand

internationally and benefit from the growing trade between Asia

and the Middle East. (Gulf-Times.com)

Nakheel awards AED47mn contracts for Deira Islands –

Nakheel has awarded contracts worth over AED47mn for design

and supervision services on Deira Islands. Nakheel appointed

AE7 for the design and supervision services including master

planning, parcelization and infrastructure design for Deira

Islands, its 15.3 square kilometre waterfront city, under a

contract worth AED28mn. AE7 has also awarded another

contract worth AED19.5mn covering the architectural and

5. Page 5 of 6

engineering services for the built form of the night market and

board walk. (Bloomberg)

ZonesCorp signs AED367mn contract with Jindal SAW Gulf

– ZonesCorp has signed an agreement with Jindal Saw Gulf for

the expansion of its current facilities. Jindal Saw Gulf is planning

a AED367mn expansion of its ductile iron pipe facility in

ZonesCorp's Industrial City, which will boost production capacity

by an additional 200,000 tons per year taking the total

production capacity to 500,000 tons per year. (Bloomberg)

TAQA secures $200mn Samurai loan – Abu Dhabi National

Energy Company (TAQA) has signed a $200mn Samurai loan

facility. The five-year loan was arranged by Bank of Tokyo-

Mitsubishi UFJ at a competitive 60 basis points over Japanese

Yen LIBOR and has been fully swapped into USD by Mitsubishi

UFJ Securities. The fund will be used to refinance a portion of

TAQA’s upcoming $1.2bn bond maturity. (ADX)

GCIC receives approval for strategic alliance with AXA –

Green Crescent Insurance Company (GCIC) has received no

objection letters from both the Securities & Commodities

Authority and the Insurance Authority to pursue a long-term

strategic alliance with AXA Group as well as increase its capital

from AED100mn to AED200mn via a convertible bond

instrument. (GulfBase.com)

Bank Dhofar reports net profit of OMR10.2mn for 1Q2014 –

Bank Dhofar reported a net profit of OMR10.2mn for 1Q2014 as

compared to OMR9.4mn for 1Q2013, representing a 8.18%

increase. The bank’s total assets stood at OMR2.76bn at the

end of 1Q2014 as against OMR2.34bn a year earlier. Loans and

advances grew by 17.4% to OMR2bn from OMR1.7bn in

1Q2013. Customer deposits grew by 21.8% to OMR2.2bn from

OMR1.8bn a year earlier. (MSM)

Muscat shipping lines set to move to Sohar – A number of

shipping lines in Muscat will move to Sohar Port and Freezone.

The Oman government has set a deadline of August 2014 to

ensure all commercial activities in Muscat are transferred to

Sohar Port and Freezone. The shipping lines include Maersk

Line and Safmarine. (GulfBase.com)

Bank Muscat’s paid-up capital increases – Bahrain Bourse

announced that the paid-up capital of Bank Muscat has been

increased due to the conversion of the remaining mandatory

convertible bonds equivalent to 30,427,504 shares. This will be

effective on April 20, 2014. The bank’s new total paid-up capital

will be OMR218.3mn as against OMR215.2 before increase,

while the new total outstanding shares will be 2,182,688,188 as

against 2,152,260,684 shares before increase. (Bahrain Bourse)

KHCB signs property finance solutions deal – Khaleeji

Commercial Bank (KHCB) has signed a MoU with Dilmunia at

Bahrain development manager Ithmaar Development Company

for providing property finance solutions. The bank will offer

solutions to potential buyers of units in Dilmunia including

Seavilla, the first project. (GulfBase.com)

Kalaam Bahrain buys Lightspeed from Orange – Kalaam

Telecom Bahrain has acquired Lightspeed Communications

from Jordan Telecommunications, which counts Orange as a

major investor. With this, Kalaam Telecom has become the

country’s second-largest business ISP. (GulfBase.com)

6. Contacts

Saugata Sarkar Keith Whitney Sahbi Kasraoui

Head of Research Head of Sales Manager - HNWI

Tel: (+974) 4476 6534 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 6 of 6

Rebased Performance Daily Index Performance

Source: Bloomberg Source: Bloomberg

Source: Bloomberg (*Market closed on April 18, 2014) Source: Bloomberg (*Market closed on April 18, 2014)

80.0

90.0

100.0

110.0

120.0

130.0

140.0

150.0

160.0

170.0

180.0

190.0

Jun-10 Jan-11 Aug-11 Mar-12 Oct-12 May-13 Dec-13

QE Index S&P Pan Arab S&P GCC

0.3%

0.8%

(0.9%)

0.7%

0.2%

0.5%

0.7%

(1.2%)

(0.8%)

(0.4%)

0.0%

0.4%

0.8%

1.2%

SaudiArabia

Qatar

Kuwait

Bahrain

Oman

AbuDhabi

Dubai

Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD%

Gold/Ounce 1,294.30 (0.1) (1.8) 7.4 DJ Industrial* 16,408.54 0.0 2.4 (1.0)

Silver/Ounce 19.61 (0.2) (2.0) 0.7 S&P 500* 1,864.85 0.0 2.7 0.9

Crude Oil (Brent)/Barrel (FM

Future)*

109.53 0.0 2.0 (1.1) NASDAQ 100* 4,095.52 0.0 2.4 (1.9)

Natural Gas (Henry

Hub)/MMBtu*

4.57 0.0 (1.8) 5.1 STOXX 600* 332.43 0.0 1.1 1.3

LPG Propane (Arab Gulf)/Ton* 112.62 0.0 1.1 (10.8) DAX* 9,409.71 0.0 1.0 (1.5)

LPG Butane (Arab Gulf)/Ton* 124.75 0.0 2.3 (8.6) FTSE 100* 6,625.25 0.0 1.0 (1.8)

Euro 1.38 (0.0) (0.5) 0.5 CAC 40* 4,431.81 0.0 1.5 3.2

Yen 102.43 0.0 0.8 (2.7) Nikkei 14,516.27 0.7 4.0 (10.9)

GBP* 1.68 0.0 0.4 1.4 MSCI EM 1,011.87 0.3 (0.4) 0.9

CHF 1.13 (0.0) (0.8) 1.1 SHANGHAI SE Composite 2,097.75 (0.1) (1.5) (0.9)

AUD 0.93 0.0 (0.7) 4.7 HANG SENG* 22,760.24 0.0 (1.1) (2.3)

USD Index 79.85 0.0 0.5 (0.2) BSE SENSEX* 22,628.84 0.0 (0.0) 6.9

RUB 35.57 (0.1) (0.2) 8.2 Bovespa* 52,111.85 0.0 0.5 1.2

BRL* 0.45 0.0 (0.8) 5.7 RTS 1,200.22 2.4 (0.3) (16.8)

180.4

153.4

139.5