VVIP Pune Call Girls Katraj (7001035870) Pune Escorts Nearby with Complete Sa...

24 November Daily Market Report

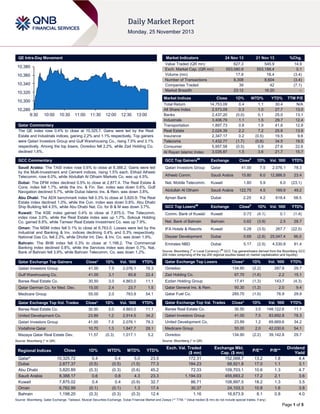

1. QE Intra-Day Movement

Market Indicators

10,380

10,360

10,340

10,320

21 Nov 13

%Chg.

627.3

553,580.9

17.8

8,308

39

23:12

545.9

553,188.4

18.4

8,604

42

16:20

14.9

0.1

(3.4)

(3.4)

(7.1)

–

Market Indices

10,300

10,280

9:30

24 Nov 13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.4% to close at 10,325.7. Gains were led by the Real

Estate and Industrials indices, gaining 2.2% and 1.1% respectively. Top gainers

were Qatari Investors Group and Gulf Warehousing Co., rising 7.5% and 3.1%

respectively. Among the top losers, Ooredoo fell 2.2%, while Zad Holding Co.

declined 1.6%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

14,753.09

2,573.09

2,437.20

3,406.79

1,897.73

2,024.39

2,347.17

1,432.77

5,957.58

3,026.87

0.4

0.3

(0.0)

1.1

0.8

2.2

0.2

(1.7)

(0.5)

1.5

1.1

1.0

0.1

1.5

1.9

7.2

(0.5)

(0.8)

0.9

3.6

30.4

27.7

25.0

29.7

41.6

25.6

19.5

34.5

27.6

21.7

N/A

13.0

13.1

12.4

12.9

13.9

9.6

19.5

22.6

15.7

GCC Commentary

GCC Top Gainers##

Exchange

Close#

Saudi Arabia: The TASI index rose 0.6% to close at 8,388.2. Gains were led

by the Multi-Investment and Cement indices, rising 1.5% each. Etihad Atheeb

Telecomm. rose 6.0%, while Abdullah Al Othaim Markets Co. was up 4.5%.

Qatari Investors Group

1D%

Vol. ‘000

Qatar

41.00

7.5

2,076.1

78.3

Atheeb Comm.

Saudi Arabia

15.80

6.0

12,886.5

23.4

Dubai: The DFM index declined 0.5% to close at 2,877.4. The Real Estate &

Cons. index fell 1.7%, while the Inv. & Fin. Ser. index was down 0.6%. Gulf

Navigation declined 5.7%, while Dubai Islamic Ins. & Rein. was down 3.8%.

Nat. Mobile Telecomm.

Kuwait

Abdullah Al Othaim

Saudi Arabia

Abu Dhabi: The ADX benchmark index fell 0.3% to close at 3,820.9. The Real

Estate index declined 1.0%, while the Con. index was down 0.8%. Abu Dhabi

Ship Building fell 4.5%, while Abu Dhabi Nat. Co. for B & M was down 3.7%.

Ajman Bank

Dubai

GCC Top Losers

Exchange

Kuwait: The KSE index gained 0.4% to close at 7,875.0. The Telecomm.

index rose 3.0%, while the Real Estate index was up 1.7%. Sokouk Holding

Co. gained 8.8%, while Tameer Real Estate Investment Co. was up 7.9%.

Comm. Bank of Kuwait

Kuwait

0.73

(4.1)

0.1

(1.4)

Nat. Bank of Bahrain

Bahrain

0.62

(3.9)

2.5

28.7

Oman: The MSM index fell 0.1% to close at 6,763.0. Losses were led by the

Industrial and Banking & Inv. indices declining 0.4% and 0.3% respectively.

National Gas Co. fell 2.3%, while Dhofar Int. Dev. & Inv. Co. was down 1.9%.

IFA Hotels & Resorts

Kuwait

0.28

(3.5)

267.7

(22.5)

Deyaar Development

Dubai

0.69

(2.8)

25,047.4

96.0

Emirates NBD

Dubai

5.17

(2.5)

4,530.8

81.4

Bahrain: The BHB index fell 0.3% to close at 1,198.2. The Commercial

Banking index declined 0.8%, while the Services index was down 0.7%. Nat.

Bank of Bahrain fell 3.9%, while Bahrain Telecomm. Co. was down 1.2%.

##

YTD%

1.80

5.9

6.0

(23.1)

122.75

4.5

169.9

49.2

2.25

4.2

618.4

58.5

#

Close

1D% Vol. ‘000

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Qatari Investors Group

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Losers

Close*

1D%

Vol. ‘000

YTD%

41.00

Qatar Exchange Top Gainers

7.5

2,076.1

78.3

Ooredoo

134.90

(2.2)

287.8

29.7

67.70

(1.6)

2.2

15.1

(4.3)

Gulf Warehousing Co.

41.00

3.1

60.8

22.4

Zad Holding Co.

Barwa Real Estate Co.

30.50

3.0

4,863.0

11.1

Ezdan Holding Group

17.41

(1.3)

143.7

Qatar German Co. for Med. Dev.

15.00

2.4

23.7

1.5

Qatar General Ins. & Rein.

50.30

(1.2)

2.0

9.4

Medicare Group

55.00

2.0

763.9

54.1

Qatar Fuel Co.

285.70

(1.0)

76.9

29.9

Qatar Exchange Top Val. Trades

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Val. ‘000

YTD%

Barwa Real Estate Co.

30.50

3.0

4,863.0

11.1

Barwa Real Estate Co.

30.50

3.0

148,122.6

11.1

United Development Co.

23.89

1.2

2,914.5

34.2

Qatari Investors Group

41.00

7.5

83,692.8

78.3

Qatari Investors Group

41.00

7.5

2,076.1

78.3

United Development Co.

23.89

1.2

69,669.6

34.2

Vodafone Qatar

10.70

1.3

1,847.7

28.1

Medicare Group

55.00

2.0

42,030.6

54.1

Mazaya Qatar Real Estate Dev.

11.57

(0.3)

1,017.1

5.2

134.90

(2.2)

39,142.8

29.7

Qatar Exchange Top Vol. Trades

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Ooredoo

Close

1D%

WTD%

MTD%

YTD%

10,325.72

2,877.37

3,820.89

8,388.17

7,875.02

6,762.99

1,198.20

0.4

(0.5)

(0.3)

0.6

0.4

(0.1)

(0.3)

0.4

(0.5)

(0.3)

0.6

0.4

(0.1)

(0.3)

5.0

(1.5)

(0.6)

4.3

(0.9)

1.3

(0.3)

23.5

77.3

45.2

23.3

32.7

17.4

12.4

Exch. Val. Traded

($ mn)

172.31

184.23

72.33

1,194.03

86.71

30.37

1.16

Exchange Mkt.

Cap. ($ mn)

152,068.7

68,921.8

109,703.1

455,693.2

108,997.5

24,103.3

16,673.9

P/E**

P/B**

13.2

17.0

10.6

17.2

18.2

10.8

8.1

1.8

1.1

1.3

2.1

1.3

1.6

0.8

Dividend

Yield

4.4

3.1

4.7

3.6

3.5

3.8

4.0

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.4% to close at 10,325.7. The Real Estate

and Industrials indices led the gains. The index rose on the back

of buying support from Qatari shareholders despite selling

pressure from non-Qatari shareholders.

Qatari Investors Group and Gulf Warehousing Co. were the top

gainers, rising 7.5% and 3.1% respectively. Among the top

losers, Ooredoo fell 2.2%, while Zad Holding Co. declined 1.6%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

77.90%

66.54%

71,235,363.79

Non-Qatari

22.11%

33.46%

(71,235,363.79)

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday declined by 3.4% to 17.8mn

from 18.4mn on Thursday. However, as compared to the 30-day

moving average of 9.6mn, volume for the day was 85.1% higher.

Barwa Real Estate Co. and United Development Co. were the

most active stocks, contributing 27.3% and 16.4% to the total

volume respectively.

News

Qatar

DHBK to raise QR2bn through private placement of Tier I

note – Doha Bank (DHBK), which is aiming for a 15-20% asset

growth over the next four to five years, plans to raise up to

QR2bn from the market through a private placement of a Tier I

note. DHBK’s shareholders have approved this issue. Doha

Bank’s Group CEO R. Seetharaman said this issue will raise the

bank’s capital adequacy ratio to 19.1% from the present 13.7%.

The capital mop-up – which is likely to happen either by year

end or by 1Q2014 – is part of the bank’s efforts to significantly

shore up its capital base in view of the Basel III norms. These

instruments will be treated as equity instruments with a fixed

return. Managed by a special purpose vehicle, the issue would

be undertaken through private placements to Qatari institutions,

and its maturity would be perpetual. The investors in this issue

would most likely be government entities or other institutional

investors in Qatar. (Gulf-Times.com)

CBQK’s Turkish unit buys 99.9% stake in ALease for

QR215.2mn – The Commercial Bank of Qatar’s (CBQK) Turkish

subsidiary, Alternatif Bank has purchased 99.9% stake in

Alternatif Finansal Kiralam (ALease). Alternatif Bank purchased

2.73bn shares from Anadolu Endustri Holding and 115.5mn

shares from minority shareholders for a total cost of

QR215.2mn. (QE)

QNB signs deal with QBC to finance Hyundai equipment –

QNB has signed an agreement with the Qatar Building

Company (QBC), an agent for Hyundai, for equipment finance.

As per this agreement, QBC will be referring their Hyundai

customers to QNB for assisting with financing of their

purchases. QNB, through its business banking division, has

launched an equipment finance program tailored to small &

medium enterprises (SMEs) in the construction sector in Qatar.

Financing would range from 75% to 84% of the equipment’s

value and will be available for around one to three years. (GulfTimes.com)

Ashghal to announce plans for Passage of Gulf project –

Qatar’s Public Works Authority (Ashghal) will soon announce the

construction plan for the “Passage of Gulf” project, which will

connect the West Bay district with the southern side of Doha

city, near the Sharq Village & Spa. Ashghal’s President Nasser

bin Ali al-Mawlawi said the massive project, which includes two

tunnels, each having three-way road tracks, would be built both

under sea and above water along the Corniche. He also

announced that the final stage of the Corniche project would

begin in January 2014, which involves conversion of

roundabouts near Sheraton and Four Seasons Hotel into

signalized intersections. (Gulf-Times.com)

Msheireb Downtown Doha to feature extensive retail outlets

– Msheireb Properties’ CEO Sikkat Al Wadi said the Msheireb

Downtown Doha project will feature extensive retail outlets

including a mall. The Galleria will comprise approximately 100

stores placed across four levels of shopping and entertainment

space. This 48,000 square meter gross leasable space will have

an anchor supermarket on the lower ground floor and a sixscreen cinema theatre. On completion in 2016, the project will

include more than 100 buildings that offer housing, workspace,

cultural and community facilities, while preserving key heritage

buildings. (Bloomberg)

Qatar to be global meetings center; WTTC expects tourism

sector to grow 4% during 2013-2023 – A statement from the

Gulf Incentives, Business, Travel & Meetings (GIBTM) said that

Qatar aims to become a global meetings destination by

investing more than $20bn in tourism-related infrastructure that

will boost its meetings, incentives, conferencing, exhibitions

(MICE) credentials. Meanwhile, according to the World Tourism

& Travel Council (WTTC), anticipates the sector to grow at 7.1%

in 2013 and grow at an annual average of 4% between 2013

and 2023. (Peninsula Qatar)

International

Atlanta Fed's President: QE taper talk on table in December

– The Atlanta Federal Reserve President Dennis Lockhart said

debate over reducing the pace of the Federal Reserve's

massive bond buying program will be on the table at its next

policy meeting in December. Dennis Lockhart said he expected

the Federal Open Market Committee, the central bank's policysetting arm, to be debating when to begin cutting back on its

program of $85bn a month in bond purchases over the next

several meetings. The committee next meets on December 1718. (Reuters)

ECB's Coeure: Disinflation to continue in Europe –

European Central Bank Executive board member Benoit Coeure

said slowing price growth, or disinflation, in Europe is likely to

continue for now, but will not progress to deflation because the

economy is recovering and inflation expectations remain

anchored around 2%. Coeure said Europe's economy is

stabilizing and the banking sector is strengthening, but

policymakers need to make progress with structural reforms to

bring down unemployment and encourage business investment.

(Reuters)

IMF: Greek economic recovery fragile – Greece's IMF auditor

Poul Thomsen said the economic recovery touted by Greece's

embattled government is fragile and will be hurt if the

government does not stay the course of fiscal adjustment and

Page 2 of 5

3. structural reform. He also called for new, targeted cuts in the

next two years, whilst noting that horizontal cuts should be

avoided in a country now gripped in a six-year recession. (ET)

Regional

E&Y: Kingdom biggest Islamic banking market with $245bn

assets in 2012 – According to EY's Global Islamic Banking

Center, Saudi Arabia was the biggest market with an estimated

$245bn in assets in 2012. The total global Islamic banking

assets held by commercial banks stood at $1.54tn in 2012,

which included both Islamic banks and Islamic windows of

conventional banks. In the GCC region, Islamic banking assets

reached $452bn in 2012 and are expected to exceed $515bn by

the end of 2013. The UAE’s Islamic banking assets, including

windows were estimated at $80bn, while Qatar’s assets reached

$53bn in 2012. The annual growth in the Islamic banking

industry was 16% (five-year CAGR), which is faster than the

growth of conventional banking assets across all the core

Islamic finance markets. (GulfBase.com)

GE signs 2 maintenance contracts worth SR1.7bn with SEC

– The Saudi Electricity Company (SEC) has signed two

contracts worth SR1.7bn with US-based General Electric (GE)

for the maintenance of gas turbines at its new power plants in

Riyadh. This 25-year contract, which will be split between 8

basic years and 17 optional years, will cover maintenance work

on the 12 gas units for the combined cycle power plants.

(Bloomberg)

Petrofac Saudi Arabia awards EPC contract to CB&I –

Petrofac Saudi Arabia has awarded a contract valued around

$70mn to US-based CB&I. This contract includes engineering,

procurement & construction (EPC) of crude oil storage tanks at

a grassroots refinery that is being constructed in Saudi Arabia.

(Bloomberg)

Takween BoD re-appoints board chairman, managing

director – Takween Advanced Industries’ board of directors has

approved the re-appointment of Abdullah M. Al Othman as the

Chairman of the board and Abdulmohsen M. Al Othman as the

Managing Director of the company. (Tadawul)

NCB opens new Rahwat Albar branch in Baha – The National

Commercial Bank (NCB) has opened its new Rahwat Albar

branch in Baha. This new branch will help achieve NCB’s

mission to provide all customers in Baha region with banking,

finance and investment services that are Shari’ah-compliant.

(GulfBase.com)

IDB sets $5.5bn 2014 budget – Islamic Development Bank

(IDB) President Ahmed Ali Al Madani said the bank has set a

$5.5bn budget for 2014. He expects bank to match 2013’s $1bn

debt sales in financial year started 3 weeks ago. He also said

that the bank is working to develop short-term debt instruments

to tackle liquidity management which is the major challenge to

sukuk industry. (Bloomberg)

S&P affirms ratings on Ras Al Khaimah at A/A-1 – S&P has

affirmed its “A/A-1” rating for long and short-term foreign & local

currency sovereign credit ratings of Ras Al Khaimah with a

Stable outlook. S&P said Ras Al Khaimah’s ratings are

supported by its limited fiscal risks due to government's minimal

spending responsibilities, its strong government balance sheet

and ongoing indirect financial support from the UAE. Meanwhile,

S&P forecasts Ras Al Khaimah's net general government asset

position to be at 4% of GDP during 2013-2016, including debt

and liquid assets of all publicly-owned entities. (GulfBase.com)

Dubai DED signs MoU with HDC to promote business,

investment in halal sector – Dubai’s Department of Economic

Development (Dubai DED) and Malaysia’s Halal Industry

Development Corporation (HDC) have entered into a MoU to

jointly promote business and investment in their respective halal

sectors. Under the MoU, DED and HDC will cooperate in

developing policies as well as an institutional infrastructure for

the halal industry and also encourage their respective halal

companies to engage in trade and investment partnerships.

Further, both the parties will organize joint halal promotion

activities and provide background checks on companies from

both sides. (GulfBase.com)

Emirates Reit signs acquisition leaseback deal with GEMS

Education – Emirates Reit has entered into an acquisition

leaseback deal with Global Education Management Systems

(GEMS Education) to acquire a long leasehold interest in a

school campus in Dubai. This deal will increase Emirates Reit’s

assets to eight properties with a value of around AED1.1bn.

Emirates Reit will own the facilities and related assets of GEMS

World Academy in Dubai. Meanwhile, GEMS Education will

continue to manage the property as usual, and there will be no

impact on the school’s operations. (GulfBase.com)

Lord Corporation opens Dubai office to tap MENA

opportunities – US-based Lord Corporation has opened its

office in Dubai to tap huge business opportunities offered by the

MENA region in the aerospace, construction, infrastructure and

automotive segments. This new office will house Lord

Corporation’s regional management team, marketing staff and a

technical centre, and will cater to 16 countries in the MENA

region. (GulfBase.com)

Swedfund, AHF to invest $6.5mn in Nairobi Women’s

Hospital – Sweden-based Swedfund and the Africa Health

Fund (AHF) through Abraaj Group, have invested $6.5mn in the

Nairobi Women’s Hospital in Kenya. This investment will enable

the hospital to complete the financing of its modernization and

expansion plan in East Africa. This will increase the range of

treatments and services offered to patients in the region.

(GulfBase.com)

OSN closes $200mn syndicated financing facility – Pay-TV

company OSN has successfully closed its first syndicated fiveyear financing facility worth $200mn. Mashreqbank acted as the

sole mandated lead arranger, book runner and underwriter for

this facility. Barclays Bank, BNP Paribas Fortis, Citibank, HSBC

Bank Middle East and National Bank of Kuwait were the

participating banks for this facility. The facility’s proceeds will be

utilized to strengthen OSN’s core business in line with the

company’s objective to provide viewers with the ultimate

entertainment experience. (GulfBase.com)

FH acquires CAPM Investment – The Finance House (FH) has

acquired Abu Dhabi-based CAPM Investment. (ADX)

TNI appoints new CEO – The National Investor (TNI) has

appointed Yasser Geissah as the company’s new CEO Yasser

Geissah replaces Orhan Osmansoy and he joins TNI after

working with Abu Dhabi Investment Company, National Bank of

Abu Dhabi and CAPM Investment. (Reuters)

Moody's assigns Baa3 IFS rating to Al Muthanna Takaful

Insurance – Moody's has assigned a first-time Baa3 insurance

financial strength rating (IFSR) to Kuwait-based Al Muthanna

Takaful Insurance Company. The rating was assigned with a

Stable outlook. (Bloomberg)

Bank Muscat, VMP Co sign MoU for baituna home finance –

Bank Muscat and the Vantage Modern Project Company (VMP

Co) have entered into MoU to provide attractive baituna home

finance for VMP Co’s residential units in the Seeb wilayat.

(GulfBase.com)

Page 3 of 5

4. Oman CMA approves ANC Holdings’ stake purchase in

DFIC – Oman’s Capital Market Authority (Oman CMA) has

approved Dubai-based ANC Holdings’ request to acquire

39.126% stake in Dhofar Fisheries & Food Industries Company

(DFIC) from Flag Holding of Abu Dhabi. (MSM)

Page 4 of 5

5. Rebased Performance

Daily Index Performance

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

0.8%

148.4

0.6%

0.4%

0.4%

0.4%

131.0

119.1

0.0%

(0.1%)

(0.4%)

(0.3%)

(0.3%)

S&P Pan Arab

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Dubai

Oman

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,243.83

0.0

0.0

(25.8)

DJ Industrial

16,064.80

0.0

0.0

22.6

19.87

0.0

0.0

(34.5)

S&P 500

1,807.65

0.0

0.0

26.7

111.05

0.0

0.0

(0.1)

NASDAQ 100

3,991.65

0.0

0.0

32.2

3.77

0.0

0.0

10.1

STOXX 600

322.77

0.0

0.0

15.4

119.75

0.0

0.0

33.8

DAX

9,219.04

0.0

0.0

21.1

143.00

0.0

0.0

(17.3)

FTSE 100

6,674.30

0.0

0.0

13.2

1.36

0.0

0.0

2.8

101.27

0.0

0.0

16.7

Nikkei

GBP

1.62

0.0

0.0

(0.2)

CHF

1.10

0.0

0.0

1.0

AUD

0.92

0.0

0.0

(11.5)

USD Index

80.71

0.0

0.0

RUB

32.77

0.0

0.0

BRL

0.44

0.0

0.0

(10.0)

Yen

Bahrain

Jul-13

Abu Dhabi

QE Index

May-12 Dec-12

Kuwait

Oct-11

Qatar

Jan-10 Aug-10 Mar-11

Saudi Arabia

(0.5%)

(0.8%)

4,278.53

0.0

0.0

17.5

15,381.72

0.0

0.0

48.0

MSCI EM

1,009.17

0.0

0.0

(4.4)

SHANGHAI SE Composite

2,196.38

0.0

0.0

(3.2)

HANG SENG

23,696.30

0.0

0.0

4.6

1.2

BSE SENSEX

20,217.40

0.0

0.0

4.1

7.4

Bovespa

52,800.70

0.0

0.0

(13.4)

1,444.91

0.0

0.0

(5.4)

Source: Bloomberg

CAC 40

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5