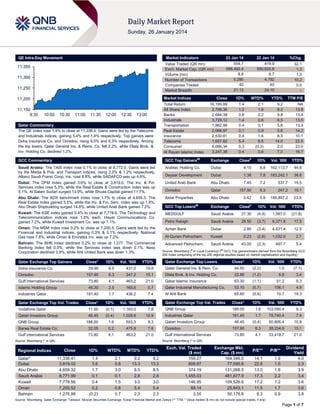

1. QE Intra-Day Movement

Market Indicators

11,350

11,300

11,250

Market Indices

11,200

11,150

9:30

23 Jan 14

554.7

598,492.4

8.8

5,280

40

21:13

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 1.4% to close at 11,338.4. Gains were led by the Telecoms

and Industrials indices, gaining 5.4% and 1.4% respectively. Top gainers were

Doha Insurance Co. and Ooredoo, rising 8.5% and 6.3% respectively. Among

the top losers, Qatar General Ins. & Reins. Co. fell 2.2%, while Dlala Brok. &

Inv. Holding Co. declined 1.2%.

22 Jan 14

419.9

590,620.8

8.7

4,792

40

24:10

%Chg.

32.1

1.3

1.0

10.2

0.0

–

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

16,199.99

2,799.36

2,684.39

3,729.12

1,962.99

2,066.97

2,530.81

1,657.82

6,066.34

3,247.38

1.4

1.2

0.8

1.4

0.4

0.1

0.4

5.4

0.3

0.4

2.1

1.9

2.2

0.8

0.1

0.9

1.6

8.5

(0.3)

0.6

9.2

8.2

9.8

6.5

5.6

5.8

8.3

14.0

2.0

7.0

NA

13.8

13.4

13.5

13.3

14.2

10.1

22.5

23.0

16.7

Close#

1D%

GCC Commentary

GCC Top Gainers##

Exchange

Vol. ‘000

YTD%

Saudi Arabia: The TASI index rose 0.1% to close at 8,772.0. Gains were led

by the Media & Pub. and Transport indices, rising 2.0% & 1.2% respectively.

Allianz Saudi Fransi Coop. Ins. rose 4.8%, while SADAFCO was up 4.6%.

Arabtec Holding Co.

Dubai

4.15

9.8

162,113.7

44.6

Deyaar Development

Dubai

1.38

7.8

183,242.1

36.6

Dubai: The DFM index gained 3.6% to close at 3,819.0. The Inv. & Fin.

Services index rose 5.3%, while the Real Estate & Construction index was up

5.1%. Al Salam Sudan surged 13.9%, while Shuaa Capital gained 11.7%.

United Arab Bank

Abu Dhabi

Ooredoo

Qatar

Abu Dhabi: The ADX benchmark index rose 1.7% to close at 4,655.3. The

Real Estate index gained 5.5%, while the Inv. & Fin. Serv. index was up 1.8%.

Abu Dhabi Shipbuilding surged 14.8%, while United Arab Bank gained 7.2%.

Aldar Properties

Kuwait: The KSE index gained 0.4% to close at 7,778.6. The Technology and

Telecommunication indices rose 1.8% each. Hayat Communications Co.

gained 7.2%, while Kuwait Investment Co. was up 7.1%.

Oman: The MSM index rose 0.2% to close at 7,200.5. Gains were led by the

Financial and Industrial indices, gaining 0.3% & 0.1% respectively. National

Gas rose 7.8%, while Oman & Emirates Inv. was up 7.2%.

Bahrain: The BHB index declined 0.2% to close at 1,277. The Commercial

Banking index fell 0.5%, while the Services index was down 0.1%. Nass

Corporation declined 3.9%, while Ahli United Bank was down 1.3%.

7.45

7.2

537.7

15.5

157.90

6.3

247.2

15.1

Abu Dhabi

3.42

5.9

189,897.2

23.9

GCC Top Losers

Exchange

#

1D% Vol. ‘000

YTD%

MEDGULF

Saudi Arabia

27.30

(4.9)

1,587.0

(21.8)

Petro Rabigh

Saudi Arabia

28.50

(3.7)

6,371.8

17.5

Ajman Bank

Dubai

2.80

(3.4)

4,631.4

12.9

Al-Qurain Petrochem.

Kuwait

0.23

(2.6)

1,032.0

2.7

Advanced Petrochem.

Saudi Arabia

43.00

(2.3)

497.7

5.4

##

Close

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Doha Insurance Co.

Close*

1D%

Vol. ‘000

YTD%

Close*

1D%

Vol. ‘000

YTD%

29.95

Qatar Exchange Top Gainers

8.5

431.0

19.8

Qatar General Ins. & Rein. Co.

44.50

(2.2)

1.0

(7.1)

22.86

(1.2)

6.8

3.4

9.3

Qatar Exchange Top Losers

157.90

6.3

247.2

15.1

Dlala Brok. & Inv. Holding Co.

Gulf International Services

73.80

4.1

463.2

21.0

Qatar Islamic Insurance

63.30

(1.1)

51.2

Islamic Holding Group

46.30

2.5

165.6

0.7

Qatar Industrial Manufacturing Co.

53.10

(0.7)

106.1

4.9

Industries Qatar

181.40

1.7

436.2

7.4

Al Ahli Bank

65.60

(0.6)

10.7

19.3

Qatar Exchange Top Vol. Trades

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

QNB Group

188.00

1.6

103,590.4

9.3

Industries Qatar

181.40

1.7

78,740.4

7.4

48.45

(0.4)

50,806.4

10.9

157.90

6.3

38,234.9

15.1

73.80

4.1

33,418.7

21.0

Ooredoo

Close*

1D%

Vol. ‘000

YTD%

Vodafone Qatar

11.55

(0.1)

1,163.0

7.8

Qatari Investors Group

48.45

(0.4)

1,028.6

10.9

188.00

1.6

553.3

9.3

Qatari Investors Group

Barwa Real Estate Co.

32.05

0.2

475.9

7.6

Ooredoo

Gulf International Services

73.80

4.1

463.2

21.0

QNB Group

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

Gulf International Services

Close

1D%

WTD%

MTD%

YTD%

11,338.41

3,819.02

4,655.32

8,771.99

7,778.56

7,200.52

1,276.98

1.4

3.6

1.7

0.1

0.4

0.2

(0.2)

2.1

5.8

3.0

0.1

1.5

0.8

0.7

9.2

13.3

8.5

2.8

3.0

5.4

2.3

9.2

13.3

8.5

2.8

3.0

5.4

2.3

Exch. Val. Traded

($ mn)

159.27

808.97

374.19

1,455.03

146.95

68.14

3.50

Exchange Mkt.

Cap. ($ mn)

164,346.0

77,095.8

131,268.5

481,677.9

109,526.6

25,643.1

50,178.8

P/E**

P/B**

14.1

22.5

13.0

17.3

17.2

11.5

8.3

1.9

1.5

1.6

2.2

1.2

1.7

0.9

Dividend

Yield

4.0

2.3

3.9

3.4

3.6

3.6

3.8

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 7

2. Qatar Market Commentary

The QE index rose 1.4% to close at 11,338.4. The Telecoms and

Industrials indices led the gains. The index rose on the back of

buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Overall Activity

Sell %*

Net (QR)

Qatari

41.32%

67.29%

(144,035,515.77)

Non-Qatari

Doha Insurance Co. and Ooredoo were the top gainers, rising

8.5% and 6.3% respectively. Among the top losers, Qatar

General Ins. & Reins. Co. fell 2.2%, while Dlala Brok. & Inv.

Holding Co. declined 1.2%.

Buy %*

58.68%

32.71%

144,035,515.77

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Thursday rose by 1.0% to 8.8mn

from 8.7mn on Wednesday. However, as compared to the 30day moving average of 10.8mn, volume for the day was 19.1%

lower. Vodafone Qatar and Qatari Investors Group were the

most active stocks, contributing 13.3% and 11.8% to the total

volume respectively.

Earnings and Global Economic Data

Earnings Releases

Company

Market

Currency

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

Agthia Group*

Abu Dhabi

AED

1512.2

14.0%

158.4

31.6%

160.1

28.4%

Oman Cables Industry*

Oman

OMR

306.1

19.0%

–

–

16.9

42.0%

National Detergent*

Oman

OMR

21.7

3.3%

–

–

1.1

55.5%

Financial Services*

Oman

OMR

1.0

143.6%

–

–

0.5

NA

Oman Cement*

Oman

OMR

56.4

-4.9%

–

–

16.0

-8.3%

Source: Company data, DFM, ADX, MSM (*FY2013 results)

Global Economic Data

Date

Market

Source

Indicator

Period

Actual

Consensus

Previous

01/23

US

Department of Labor

Initial Jobless Claims

18-January

01/23

US

Bloomberg Indices

Markit US PMI Preliminary

January

326K

330K

325K

53.7

55.0

01/23

US

FHFA

House Price Index MoM

November

54.4

0.10%

0.40%

0.50%

01/23

US

Bloomberg

Bloomberg Consumer Comfort

19-January

-31

–

-31

01/23

EU

Markit

PMI Manufacturing

January

53.9

53.0

52.7

01/23

EU

Markit

PMI Composite

January

53.2

52.5

52.1

01/23

EU

Markit

PMI Services

January

51.9

51.4

51

01/23

EU

EC

Consumer Confidence

January

-11.7

-13.0

-13.5

01/23

France

INSEE

Production Outlook Indicator

January

-5

-9

-11

01/23

France

INSEE

Manufacturing Confidence

January

100

100

100

01/23

France

INSEE

Business Confidence

January

94

95

94

01/23

France

Markit

PMI Manufacturing

January

48.8

47.5

47

01/23

France

Markit

PMI Services

January

48.6

48.1

47.8

01/23

Germany

Markit

PMI Manufacturing

January

56.3

54.6

54.3

01/23

Germany

Markit

PMI Services

January

53.6

54.0

53.5

01/23

UK

CBI

CBI Reported Sales

January

14

25

34

01/24

UK

BBA

BBA Loans for House Purchase

December

46,521

47,300

45,394

01/23

Spain

INE

Unemployment Rate

4Q2013

26.03%

26.00%

25.98%

01/24

Spain

INE

PPI MoM

December

1.10%

–

-0.80%

01/24

Spain

INE

PPI YoY

December

0.60%

–

-0.50%

01/24

Italy

ISTAT

Retail Sales MoM

November

0.00%

0.00%

-0.10%

01/24

Italy

ISTAT

Retail Sales YoY

November

0.10%

–

-1.60%

01/23

China

Markit

HSBC/Markit Flash Mfg PMI

January

49.6

50.3

50.5

Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted)

Page 2 of 7

3. News

Qatar

KCBK’s net profit rises 41.8% QoQ in 4Q2013; declares 10%

cash dividend – Core banking income along with net reversals

drives KCBK's net profit QoQ and YoY. Al Khaliji registered a

net profit of QR152.7mn in 4Q2013 (FY2013: QR550.9mn), an

increase of 41.8% QoQ and 14.2% YoY. FY2013 net income

exceeded our estimate by 6.8% (BBG consensus ex-QNBFS:

QR383mn). Net interest income gained by an impressive 15.5%

YoY to reach QR590.4mn. Headline NIM dropped to 1.71% vs.

1.82% in 2012. However, when we look at the NIM on an

adjusted basis, it appears that KCBK's NIM increased by ~3bps.

Moreover, fees & commissions surprised on the upside, surging

by 95.2% YoY to rest at QR142.8mn (FY2012: QR73.1mn).

Another positive surprise stemmed from FX income. The bank

posted QR26.4mn vs. a loss of QR12.1mn in 2012. On the other

hand, investment income plummeted by 55.2%, reaching

QR174.5mn vs. QR389.7mn in 2012. OPEX ticked up by 2.5%

YoY to reach QR382.8mn (FY2012: QR373.3mn). Thus, the

cost-to-income ratio increased to 40.6% (FY2012: 38.5%).

Finally, a determining factor to KCBK's profitability was a net

reversal of QR11.9mn vs. a net provision of QR61.1mn in 2012.

RoAE slightly gained from 9.3% to 9.7% in 2013 (management's

3-year target: 15%). The bank's loan book surged by 58.8%

(QR20.7bn) while deposits expanded 14.8% (QR19.9bn). Thus,

KCBK’s LDR increased to 104% vs. 75% in 2012. Asset quality

remains intact with the bank ending 2013 with NPL and

coverage ratios of 0.34% and 322.9%, respectively. We expect

KCBK to expand its loan book by 20.2% and 20.1% in 2014 and

2015, respectively. This along with a marginal pick up in NIMs

should translate into bottom-line growth of 10.1% and 14.8% in

2014 (QR606.7mn) and 2015 (QR696.5mn), respectively.

(QNBFS Research, QE)

QIIK reports QR750mn net profit in 2013; recommends

QR3.75 dividend – Qatar International Islamic Bank’s (QIIK)

annual net profit reached QR750mn for FY2013, growth of

10.5% YoY. Bloomberg consensus estimate was QR732mn.

The bank earned total revenues of QR1.5bn in 2013. EPS

reached QR4.96 in 2013 as compared to QR4.49 in 2012.

QIIK’s board has recommended the distribution of cash dividend

of 37.5% of the nominal value share, QR3.75 per share, to its

shareholders vs. QR3.50 in 2012. (Peninsula Qatar)

New Port Project crosses 33% completion – The New Port

Project’s (NPP) Executive Director Nabeel Mohamed al-Buenain

said about 33% of the NPP’s construction work has been

completed, which is scheduled for a first phase launch in 2016.

Situated at Mesaieed, 24km south of Doha, the NPP is

estimated to cost QR27bn. Spread over 26.5 square kilometers,

a major part of the project is on reclaimed land. Al-Buenain

added that the construction of the buildings and other areas has

been initiated now, which are expected to be completed by late

2015 or early 2016. The NPP consists of a new seaport, a naval

base for Emiri Navy and the Qatar Economic Zone 3. (GulfTimes.com)

Al Rayyan Tourism buys St Regis Bal Harbour Resort for

QR776mn – Al Rayyan Tourism Investment Company (ARTIC),

the international subsidiary of Al Faisal Holding Company,

acquired St. Regis Bal Harbour Resort in Miami, Florida for

QR776mn. The transaction is aimed to enhance ARTIC’s

presence in the international hotel market. (Peninsula Qatar)

Qatar’s Tram Project to be ready by 2016 – The Qatar

Foundation’s President Saad al-Muhannadi said that the

Education City Tram Project is expected to be fully functional by

September 2016. The trial runs of the trams are expected to

begin by first few months of 2016. He said that the project will be

able to serve around 60,000 people, including the inhabitants of

the Education City. It will also have the flexibility to enhance as

the Education City expands. (GulfTimes.com)

MCGS’ BoD to meet on February 13 – Medicare Group

Holding’s (MCGS) board of directors will meet on February 13,

2014 to discuss the company’s financial results for the period

ending on December 31, 2013. (QE)

QGRI’s BoD to meet on February 9 – Qatar General Insurance

& Reinsurance Company’s (QGRI) board of directors is

scheduled to meet on February 9, 2014 to discuss the

company’s financial results ending on December 31, 2013. (QE)

International

Draghi: Europe’s recovery firming with no deflation in sight

– The European Central Bank’s President Mario Draghi said he

sees signs of a ―dramatic‖ improvement in the health of the

euro-area economy and that inflation will gradually return to

target. Draghi said what they have been seeing in the past three

or four months is both the improvement in financial markets and

that their accommodative monetary policy is finally being passed

through to the real economy. He added that the idea is that now

they have low inflation, and it will move gradually back to the

objective‖ of just under 2%. (Bloomberg)

Central Banks phase out dollar liquidity tenders as crisis

eases – The European Central Bank and global peers will wind

down emergency dollar liquidity facilities that have helped

lenders weather financial turbulence since 2007. ECB said in

view of the considerable improvement in US dollar funding

conditions and the low demand for US dollar liquidity-providing

operations, the ECB, the Bank of England, the Bank of Japan

and the Swiss National Bank jointly decided to reduce the

offering of dollar loans to banks. The ECB will cease to conduct

three-month US dollar liquidity operations as of April this year,

and will conduct one-week US dollar tenders at least until July

31. It will assess the need for further one-week dollar operations

after July. (Bloomberg)

Lagarde: Eurozone inflation way below target – IMF’s

Managing Director Christine Lagarde told the World Economic

Forum that the Eurozone inflation is "way below target" and

deflation is a potential risk for the bloc. Meanwhile the European

Central Bank (ECB) President Mario Draghi said that the ECB

stood ready to act if inflation went lower than forecast and

reaffirmed that interest rates would remain low or go lower for an

extended period of time. (ET)

France’s rating affirmed by Moody’s; retains Negative

outlook – France’s Aa1 credit rating was affirmed by Moody’s,

which maintained a Negative outlook based on the continued

reduction in the competitiveness of the nation’s economy.

Moody’s said that trend risks triggering a further deterioration in

the government’s financial strength and the nation’s long-term

growth prospects. The debt-to-GDP ratio has risen to 93.6% in

2013 from 90.2% in 2012, and Moody’s expects a further

increase to above 95% by the end of 2014. (Bloomberg)

Major trade powers pledge free trade in green goods – The

world’s biggest trading powers committed to achieve global free

trade in environmental goods, to boost the fight against climate

change. A joint statement by the US, the EU, China, Japan and

several other developed economies said the agreement would

take effect once a critical mass of members of the World Trade

Organization (WTO) participate in it. The WTO estimates that

the global market in green goods, technologies and services —

Page 3 of 7

4. ranging from solar panels to wind turbines and water recycling

plants — at around $1.4tn. (Gulf-Times.com)

China expects more capital inflows in 2014 – China’s foreign

exchange regulator said the country’s firmer currency and higher

interest rates could attract more money inflows this year, despite

the possible impact of the US Federal Reserve’s stimulus

tapering. The State Administration of Foreign Exchange’s

(SAFE) Department of International Payments’ Head Guan Tao

said that Chinese authorities are considering a ―Tobin tax‖ on

financial transactions to deter speculative capital flows. A Tobin

tax imposes a small charge on individual currency transactions

to discourage excessive speculation. Guan Tao said Chinese

banks posted a surplus of 1.68tn yuan in their foreign exchange

settlements in 2013, up 210% YoY. The central bank has said

China’s foreign exchange reserves rose by $157bn in 4Q2013 to

$3.82tn. (Gulf-Times.com)

IEA: US oil production to rise beyond forecasts – The

International Energy Agency (IEA) has estimated that oil

production in the US has risen by a record 992,000 barrels per

day in 2013. The increase has taken production to 7.5mn bpd,

with production in November and December estimated to have

crossed over 8mn bpd. The American oil consumption also rose

last year, by 390,000 bpd, or 2.1%, to 18.9mn bpd. IEA

increased its estimate for oil use in the US during 4Q2013,

although it lowered its estimate for some other countries,

including China. Overall, the global consumption rose 1.4%,

making 2013 the first year since 1999 that the use of oil in the

US rose more rapidly than in the rest of the world. (Qatar

Tribune)

QNB Group: WTO must harness innovation for growth –

According to QNB Group, the recent trade agreement reached

by the World Trade Organization (WTO) has the potential to

raise long-term global GDP growth. However, the agreement

does not cover many areas that have been under negotiation

since the Doha Round was launched in 2001. Extending the

recent agreement to these areas would reap substantial

dividends for global growth in the future. In particular, more

could be done to leverage the positive impact of recent

innovations in communications technology on global trade. In

early December 2013, the WTO’s 159-member countries

reached their first ever agreement since the institution was

founded in 1995. The most important part of the ―Bali Package‖

relates to trade facilitation, which legally binds members to

simplified customs procedures for reducing costs and increasing

efficiency of customs clearance. The deal also includes

agreement on difficult issues, such as how the WTO handles

food security programs and better access to advanced-world

economies for the least-developed economies. (Peninsula

Qatar)

Regional

Oil Movement: OPEC to cut exports amid fall in winter

demand – According to Oil Movements, the OPEC will cut crude

shipments through early February as easing growth in Asia adds

to a seasonal slowdown in demand. The OPEC will reduce its

sailings by 210,000 barrels a day (0.9%) to 23.66mn barrels in

the four weeks to February 8. That compares with 23.87mn

barrels in the period to January 11. These figures exclude two

out of OPEC’s 12 members, Angola and Ecuador. (Bloomberg)

S&P Dow Jones launches Shari’ah Index – S&P Dow Jones

Indices has launched the S&P GCC Composite Shari’ah

Dividend Index, which is designed to measure the performance

of the highest yielding, Shari’ah compliant stocks in the GCC

region. These stocks meet respective liquidity, dividend growth,

and dividend sustainability criteria. The S&P GCC Composite

Shari’ah Dividend Index’s universe is drawn from the S&P GCC

Composite Shari’ah Index, which offers investors a Shari’ahcompliant benchmark for the six GCC states – Bahrain, Kuwait,

Oman, Qatar, Saudi Arabia and the UAE. The S&P GCC

Composite Shari’ah Dividend Index consists of the 30 highest

yielding stocks from the eligible universe, subject to a minimum

of two stocks per country. The index constituents are weighted

by their indicated annual dividend yield. (GulfBase.com)

Takween signs MoU with Magna – Takween Advanced

Industries has signed a MoU with Magna Steyr Company for

cooperation in regard to manufacture of automotive parts,

components and vehicle assembly in Saudi Arabia. The MoU

will be effective from January 22, 2014 for 12 months from the

date of signing. Takween and Magna will jointly carry out

feasibility and marketing studies for the Saudi automotive

market. The MOU is in line with Takween’s mission to acquire

and develop technology for industrial development and is in

accordance with the Saudi Government’s initiative to develop

downstream industries. (Tadawul)

CPC plans IPO by June – Saudi-based Construction Products

Holding (CPC) is planning an IPO within the next few months,

possibly paving the way for more listings by family-controlled

Saudi companies. CPC's Chief Executive said that the IPO

would happen before June 2014. The company plans to float

30% of its shares. (GulfBase.com)

Al Bayan Group signs $70mn syndicated finance with

banks – Al Bayan Group Holding Company announced that it

has recently signed a $70mn syndicated Islamic term financing

facility with a group of leading regional and international banks.

ABC Islamic Bank has been appointed as the initial mandated

lead arranger and bookrunner, while the Guidance Financial

Group acted as financial adviser to Al Bayan. The new

financing facility is Al Bayan’s debut syndication in the regional

debt market, which will be used for general corporate purposes.

(GulfBase.com)

NBF reports AED393.1mn net profit in 2013 – The National

Bank of Fujairah (NBF) has reported a net profit of

AED393.1mn, reflecting an increase of 29% in 2013 as

compared to AED305.8mn in the previous year. EPS stood at

AED0.36 in 2013 as compared to AED0.28 in 2012. Loans &

advances worth AED14.3bn were up 17.5% from AED12.2bn.

Customer deposits worth AED15.0bn were up 24.6% in 2013

from AED12.0bn in 2012. Meanwhile, NBF’s board of directors

has recommended cash dividends of 12.5% of paid-up capital, a

growth of 25% from 2012. (Bloomberg)

UAB reports 35% rise in net profit in 2013 – The United Arab

Bank (UAB) has reported a net profit of AED552mn, reflecting

an increase of 35% in 2013. Loans & advances increased by

40% to AED15.29bn in December 2013 from AED10.88bn in

December 2012. Further, customer deposits recorded growth to

reach AED15.03bn, surging 49% in the same period.

Meanwhile, UAB’s board of directors has proposed a cash

dividend of 20% of paid-up capital worth AED199.3mn and a

scrip dividend of 10% of paid-up capital, amounting to

AED99.6mn. (GulfBase.com)

SIB reports AED307.1mn net profit in 2013 – Sharjah Islamic

Bank (SIB) has reported a net profit of AED307.1mn in 2013 as

compared to AED272mn in 2012, achieving a 12.9% increase.

The board of directors proposed a 10% cash dividend worth

AED242.5mn. SIB’s total assets grew by 18.6% to reach

AED21.7bn. Customer deposits rose AED566.5mn to reach

AED11.9bn, achieving 5.0% growth since December 2012.

(Zawya)

Page 4 of 7

5. UAE sets rules for covered warrants – The UAE’s financial

market regulator has issued rules allowing the issuance and

trading of covered warrants, a step toward developing its

equities market. The Securities & Commodities Authority set

conditions for banks and other companies to issue listed,

tradable instruments that give investors the right to trade stocks

and securities at specified prices. The conditions include a

licensing regime for issuers of covered warrants and disclosure

requirements. The SCA also ordered studies of best

international practices so that regulations on bond listing on the

country's securities markets can be implemented in the first half

of this year. (Reuters)

UAE's first independent solar project planned in RAK –

Utico has called for pre-qualifications for a 40MW solar power

project to be built at Ras Al Khaimah. The project, the first of its

kind in the UAE, will go a long way in bringing sustainability and

providing affordable power to consumers in the region. Further,

Utico also closed a well-participated pre-qualification process for

a 100,000 cubic meters per day desalination plant. Over 20

companies participated in the tender process for the first-ever

private independent water project in the world with a take-or-pay

model. (Bloomberg)

Dubai Group completes $6bn debt restructuring,

announces new CEO – Dubai Group has reached a final

agreement with its lenders on debt restructuring worth $6bn

after three years of talks. The group said that lenders agreed to

extend the maturity for secured debt to December 2016, and for

partially secured and unsecured loans to December 2024. A

further $4bn of related party debt has been subordinated to the

claims of the bank creditors. The company also announced a

management change, with Ahmed Al Qassim being appointed

as the Chief Executive Officer, succeeding Fadel Al-Ali, who

becomes chairman. (Bloomberg)

Emaar replaces CEO – According to sources, Emaar

Properties has replaced its Group Chief Executive Low Ping late

last year, appointing Abdulla Lahej as her successor. (Reuters)

SHUAA Capital successfully concludes sale of 3.5mn

treasury shares – SHUAA Capital has successfully concluded

the sale of 3.5mn treasury shares within the deadline as

required by the Securities & Commodities Authority. (DFM)

RTA announces upgrades worth AED1b in Business Bay,

Zabeel – Road upgrades worth AED1bn have been announced

by the Roads and Transport Authority (RTA) that will ease traffic

in Business Bay and Zabeel areas. The project, which is part of

the expanding Parallel Roads network, has been endorsed by

HH Shaikh Mohammad Bin Rashid Al Maktoum, Ruler of Dubai.

RTA’s Chairman of the Board Mattar Al Tayer said that the

project includes construction of several roads, bridges and

tunnels to ensure smooth traffic flow on the parallel roads, and

alleviate congestions in the neighborhood. (Bloomberg)

Emirates starts double daily flights to Moscow – Emirates

Airlines announced that it will serve its Moscow route with a

double daily A380 service from August 1, 2014. This second

A380 replaces the existing Boeing 777 operation and increases

the route’s seat capacity by 15%. (GulfBase.com)

Dubai Exports opens new Mumbai office – Dubai Exports

(DE), the export promotion agency of Dubai Department of

Economic Development, opened an overseas office in Mumbai,

India. The new office will work in coordination with the

representative office of the Department of Tourism & Commerce

Marketing in Mumbai. Exports and re-exports to India were

valued at AED24bn and AED31bn respectively during the first

nine months of 2013. Pearls, precious metals and stones,

copper, iron & steel, plastics and aluminum were some of the

top commodities exported to India through Dubai.

(GulfBase.com)

Dubai adds 2,950 hotel rooms in 2013 – Dubai’s hospitality

market registered only a slight drop in revenue per available

room (RevPAR) performance in November 2013, despite the

year witnessing an addition of 2,950 new branded hotel rooms in

the city. According to Ernst & Young’s Middle East Hotel

Benchmark survey, Dubai’s hospitality market has rapidly

absorbed this influx of new supply and continued to perform

exceptionally well, with RevPAR declining by just 0.3%. Dubai’s

new hotel supply included major five-star hotel openings such as

the Ocean View Hotel, the Ritz Carlton’s extension on Jumeirah

Beach, Sofitel Palm Jumeirah, Anantara Plam Jumeirah, Oberoi

and Conrad. In November, Dubai’s overall average occupancy

decreased by 5.1% as compared to November 2012, however,

average daily rate increased by 5.6%. (GulfBase.com)

CBI seeks shareholder nod for $300mn rights issue –

Commercial Bank International (CBI) said that it would convene

a shareholder meeting on February 20, 2014 to get approval for

a 50% capital increase through a rights issue. The lender, 40%

owned by the Qatar National Bank, is aiming to raise AED1.1bn

by issuing 787.9mn shares at the price of AED1.4 per share.

The price is a 36.1% discount to its closing price of AED2.19 on

Thursday. The rights issue, which has received regulatory

approval, will increase the bank's paid-up capital to AED2.36bn.

(Reuters)

Dana Gas announces convertible sukuk – Dana Gas has

announced that the period for conversion of its convertible sukuk

issued on May 8, 2013 commenced on October 31, 2013 and

will expire 25 trading days prior to October 31, 2017. Sukuk

holders shall have the right to convert all or part of their

convertible sukuk into ordinary shares at Dana Gas during the

conversion period. Meanwhile, the Company has applied to the

competent authorities for an increase in its capital to reach

AED6,703.1mn after the increase. (ADX)

Etihad to raise Dublin service to double-daily – Etihad

Airways will increase its Abu Dhabi–Dublin service from 10

flights per week, to double daily from July 15, 2014. This 40%

frequency boost will provide 8,988 seats each week between the

capital cities of the UAE and Ireland. Etihad Airways will operate

a Boeing 777-300 ER, configured to carry 380 passengers and

an Airbus A330-200, configured to carry 262 passengers.

(GulfBase.com)

Kuwait expects budget spending to slow in FY2015 – Kuwait

is planning to raise its budget spending by 3.2% next fiscal year

as compared to the current year's plan, indicating a much slower

rise than the past decade's double digit average. The major oil

producer country expects to spend KD21.86bn in its draft budget

for the fiscal year starting in April, up by KD681.9mn from the

FY2014’s plan. That is well below the average annual spending

rise of 19.2% over the last decade. (Reuters)

APC, KOC sign SR1.03bn deal to operate 400 oil wells – Al

Khorayef Petroleum Company (APC) has signed a significant

contract worth SR1.03bn with the Kuwait Oil Company (KOC) to

operate around 400 oil producing wells in Kuwait. Top officials

from KOC, APC and its Kuwaiti subsidiary, AlKhorayef Company

for Sale, Maintenance & Repair of Oil Production Equipment,

took part in the signing ceremony. (Bloomberg)

Sakana Housing goes into liquidation – The Industry &

Commerce Ministry's Business Investors Centre announced that

Bahrain-based Sakana Holistic Housing Solutions has gone into

voluntary liquidation. Abdulhakim Al Mutawa, Jamal Hijres,

Page 5 of 7

6. Muhammed Wasif Ijlal and Ziad Azzam have been appointed

liquidators. The company, which had a paid-up capital of

BHD20mn, specialized in property development, home finance

and property consulting. It offered services to Bahrainis,

expatriates living in the country, GCC residents and nonresidents. (GulfBase.com)

Bahrain’s Work Ministry invested BHD50mn in 2013 –

According to a report by the Information Affairs Authority,

Bahrain’s Work Ministry completed around BHD50mn worth of

sewage and construction projects in 2013. Work to improve the

efficiency of the dual biological treatment process at the Tubli

Waste Water Treatment Plant was the most expensive sewage

project at BHD8.75mn. The report also indicated that the

building of the Survey. (Bloomberg)

Page 6 of 7

7. Rebased Performance

Daily Index Performance

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

3.2%

140.0

2.4%

127.6

1.6%

0.8%

1.7%

1.4%

0.4%

0.1%

0.2%

0.0%

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

Global Indices Performance

Close

1D%

WTD%

YTD%

1,270.07

0.5

1.3

5.3

DJ Industrial

15,879.11

(2.0)

(3.5)

(4.2)

19.92

(0.6)

(2.0)

2.3

S&P 500

1,790.29

(2.1)

(2.6)

(3.1)

107.88

0.3

1.3

(2.6)

NASDAQ 100

4,128.17

(2.1)

(1.7)

(1.2)

5.19

(6.6)

18.0

19.4

STOXX 600

324.75

(2.4)

(3.3)

(1.1)

152.38

(0.1)

10.8

20.7

DAX

9,392.02

(2.5)

(3.6)

(1.7)

154.50

(0.6)

2.7

13.2

FTSE 100

6,663.74

(1.6)

(2.4)

(1.3)

1.37

(0.1)

1.0

(0.5)

CAC 40

102.31

(0.9)

(1.9)

(2.8)

Nikkei

GBP

1.65

(0.9)

0.4

(0.5)

MSCI EM

CHF

1.12

0.3

1.7

(0.2)

SHANGHAI SE Composite

AUD

0.87

(1.0)

(1.1)

(2.6)

USD Index

80.46

0.0

(0.9)

RUB

34.55

1.4

3.0

BRL

0.42

(0.2)

(2.1)

(1.5)

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(0.2%)

Qatar

(0.8%)

Saudi Arabia

Jun-10

3.6%

4.0%

162.9

4,161.47

(2.8)

(3.8)

(3.1)

15,391.56

(1.9)

(2.2)

(5.5)

949.90

(1.5)

(2.3)

(5.3)

2,054.39

0.6

2.5

(2.9)

HANG SENG

22,450.06

(1.2)

(3.0)

(3.7)

0.5

BSE SENSEX

21,133.56

(1.1)

0.3

(0.2)

5.1

Bovespa

47,787.38

(1.1)

(2.8)

(7.2)

1,364.11

(1.3)

(2.3)

(5.4)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (―QNBFS‖) a wholly-owned subsidiary of Qatar National Bank (―QNB‖). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 7 of 7